|

市場調查報告書

商品編碼

1692497

五氧化二鈮-市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)Niobium Pentoxide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

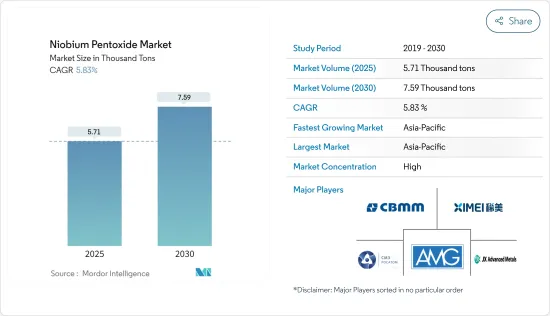

預計 2025 年五氧化二鈮市場規模將達到 5,710 噸,2030 年將達到 7,590 噸,預測期內(2025-2030 年)的複合年成長率為 5.83%。

受新冠疫情影響,五氧化二鈮市場遭遇挫折。全球停工和嚴格的政府監管導致大面積生產停工。然而,預計市場將在 2021 年復甦,並在未來幾年經歷顯著成長。

主要亮點

- 短期內,光學產業對五氧化二鈮的需求不斷成長以及製造業對優質鋼材的需求不斷增加是推動研究市場需求的主要因素。

- 然而,由於急性接觸五氧化二鈮而導致的健康問題預計將阻礙市場成長。

- 然而,生物醫藥領域不斷成長的需求預計將為市場帶來新的機會。

- 預計亞太地區將主導全球市場,其中中國和印度的需求將佔據大部分市場佔有率。

五氧化二鈮市場趨勢

製造業對優質鋼材的需求不斷增加

- 五氧化二鈮的驅動力是製造業對優質鋼材的需求激增。在鋼鐵生產中加入五氧化二鈮可以提高強度、韌性和耐腐蝕性,鞏固其作為各種鋼鐵應用中關鍵合金元素的作用。

- 五氧化二鈮可提高高強度低合金鋼(HSLA)的強度和韌性,這種鋼廣泛應用於建築、運輸和能源領域。

- 在不銹鋼中,五氧化二鈮可提高耐腐蝕性,使其可用於食品加工、化學加工和醫療設備等領域。

- 此外,它還能增強管道鋼的強度,這對於石油和天然氣運輸至關重要。

- 根據世界鋼鐵協會(Worldsteel)的數據,全球粗鋼產量將從2023年11月的1.449億噸下降至2023年12月的1.357億噸。然而,到 2024 年 7 月,產量回升至 1.528 億噸。然而,與 2023 年 7 月相比下降了 4.7%,凸顯了該行業面臨的挑戰。然而,隨著新興經濟體加大基礎設施開發和建設舉措,預計未來幾年鋼鐵需求將會復甦。

- 此外,中國、日本和美國等國家的鋼鐵生產能力增強,進一步推動了全球鋼鐵產量,從而支持了研究市場的成長。

- 根據世界鋼鐵協會的數據,日本 2024 年 7 月鋼鐵產量為 710 萬噸,較 2023 年同期下降 3.8%。累計產量49.8噸,較去年同期下降2.8%。

- 美國是世界第四大粗鋼生產國,報告稱,2024 年 7 月粗鋼產量為 690 萬噸,小幅增加 2.1%。不過,根據世界鋼鐵協會的數據,今年迄今的總產量為 4,690 萬噸,下降了 1.8%。

- 德國呈現正面趨勢,預計2024年7月產量將成長4.8%,達310萬噸。根據世界鋼鐵協會的數據,德國年產量達2,250萬噸,大幅增加4.5%。

- 巴西的增幅最高,2024年7月產量為3.1噸,增幅高達11.6%。世界鋼鐵協會報告稱,巴西年產量增加3.3%,至19.4噸。

- 2023年南非粗鋼產量將達到約487.10萬噸,與前一年同期比較增約10.64%。國際鋼鐵協會(Worldsteel)報告稱,產量激增凸顯了該國的鋼鐵業和五氧化二鈮市場。

- 鋼鐵對於建築、鐵路、汽車製造和消費品等許多行業都至關重要。過去十幾年來,開發中國家特別是印度的工業化進程大幅拉動了鋼鐵需求。

- 鑑於這些動態,五氧化二鈮市場在未來幾年可能會顯著成長。

亞太地區可望主導市場

- 亞太地區將主導五氧化二鈮市場,並將成為預測期內成長最快的地區。這種成長是由於鈮金屬在光學玻璃、超級電容、高溫合金和陶瓷等各種應用領域的需求增加,尤其是在中國、印度、韓國、日本和東南亞國家。

- 五氧化二鈮及其衍生物在鋼鐵生產中扮演重要角色。鈮的添加增加了鋼的強度,使其更耐高溫氧化和腐蝕。鈮還能降低韌脆轉變溫度,提高焊接性和成形性。它在高級結構鋼、高強度低合金鋼(HSLA)和不銹鋼的生產中尤其重要。

- 富含鈮的 HSLA 鋼主要用於汽車和建築業。值得注意的是,大約 80% 的汽車鋼板都添加了鈮微合金,以確保車輛的燃油效率、安全性和耐用性。

- 根據印度汽車製造商工業(SIAM)的數據,2024年1月至3月,印度的乘用車、商用車、三輪車、二輪車和四輪車產量為739萬輛。其中,乘用車114萬輛,商用車26.8萬輛。

- 到2024年,印度的經濟適用住宅預計將成長70%。據投資印度 (Invest India) 稱,預計到 2025 年,建築業的估值將達到 1.4 兆美元。預計到 2030 年,超過 30% 的人口將成為居住者,因此迫切需要超過 2,500 萬套中型和經濟適用住宅。 《房地產法》、商品及服務稅和房地產投資信託基金等近期改革旨在透過加速核准和加強建設產業來刺激市場成長。

- 中國是世界主要鋼鐵生產國之一,鋼鐵產品供應國內和國際市場。根據世界鋼鐵協會的數據,中國仍維持最大生產國地位,但 2024 年 7 月產量下降 9.0% 至總合萬噸。全年中國產量為613.7噸,較2023年下降2.2%。

- BigMint 預計,到 2024/2025 財政年度結束(截至 2025 年 3 月),印度鋼鐵產量將與前一年同期比較增近 6%,達到 1.52 億噸。預計大部分產量將來自使用高爐的鋼廠。

- 鈮合金在建築中也極為重要,尤其是結構和承重部件。中國在全球建築領域處於領先地位,佔全球投資的20%,預計2030年將在建築領域投資約13兆美元,市場前景看好。

- 根據塑膠出口促進委員會的數據,2023 年 12 月,印度的眼鏡和護目鏡月出口量創下新高。印度眼鏡市場目前正面臨低價競爭、依賴進口鏡片以及快速變化的消費者偏好等挑戰。 2023 年,印度隱形眼鏡市場價值約為 1.643 億美元。

- 根據波音公司的《商業展望(2023-2042)》,預計2042年中國將交付約8,560架新飛機。交付的激增預計將推動飛機零件(特別是引擎葉片)製造對五氧化二鈮的需求。

- 五氧化二鈮因其高表面積、優異的電導性、穩定性和耐用性而成為高性能超級超級電容開發的主要參與者。

- 根據中國國家能源局的數據,預計2023年將安裝超過31吉瓦的新型能源儲存系統,2024年將達到36吉瓦。這些包括鋰離子電池、超級電容和液流電池在內的新型能源儲存解決方案得到了中國領導層的支持。

- 考慮到這些動態,預計亞太地區五氧化二鈮市場在預測期內將實現穩定成長。

五氧化二鈮產業概況

五氧化二鈮市場本質上呈現整合狀態。主要企業(排名不分先後)包括 CBMM、Ximei Resources Holding Limited、JSC Solikamsk Magnesium Plant、AMG、JX Advanced Metals Corporation 等。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 調查前提

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 驅動程式

- 光學產業對五氧化二鈮的需求不斷成長

- 製造業對優質鋼材的需求不斷增加

- 其他促進因素

- 限制因素

- 急性接觸五氧化二鈮的健康問題

- 其他阻礙因素

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章市場區隔

- 年級

- 工業級(純度99.0%至99.8%)

- 3N

- 4N

- 應用

- 鈮金屬

- 光學玻璃

- 超級電容

- 高溫合金

- 陶瓷

- 其他用途

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 馬來西亞

- 泰國

- 印尼

- 越南

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐國家

- 土耳其

- 俄羅斯

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 卡達

- 阿拉伯聯合大公國

- 奈及利亞

- 埃及

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章競爭格局

- 合併、收購、合資、合作和協議

- 市場佔有率(%)**/排名分析

- 主要企業策略

- 公司簡介

- AMG

- CBMM

- Chengdu Huarui Industrial Co., Ltd.

- F&X Electro-Materials Limited

- Hebei Suoyi New Material Technology Co., Ltd.

- JSC Solikamsk Magnesium Plant

- JX Advanced Metals Corporation

- Kurt J. Lesker Company

- Merck KGaA

- Mitsui Mining & Smelting Co. Ltd.

- MPIL

- Taki Chemical Co., Ltd.

- XIMEI Resources Holding Limited

第7章 市場機會與未來趨勢

- 生物醫學領域的需求不斷成長

- 其他機會

The Niobium Pentoxide Market size is estimated at 5.71 thousand tons in 2025, and is expected to reach 7.59 thousand tons by 2030, at a CAGR of 5.83% during the forecast period (2025-2030).

The niobium pentoxide market faced setbacks due to COVID-19. Global lockdowns and stringent government regulations led to widespread shutdowns of production hubs. However, the market rebounded in 2021 and is projected to see significant growth in the upcoming years.

Key Highlights

- Over the short term, the growing demand for niobium pentoxide in the optics industry and the increasing demand for high-quality steel from the manufacturing sector are the major factors driving the demand for the market studied.

- However, concerns about health issues caused by acute exposure to niobium pentoxide are expected to hinder the market's growth.

- Nevertheless, the growing demand from the biomedical sector is expected to create new opportunities for the market studied.

- Asia-Pacific region is expected to dominate the market across the world, with the majority of demand coming from China and India.

Niobium Pentoxide Market Trends

Increasing Demand for High-quality Steel from the Manufacturing Sector

- The manufacturing sector's surging demand for high-quality steel is driving the rising trend of niobium pentoxide. Its incorporation in steel production enhances strength, toughness, and corrosion resistance, solidifying its role as a vital alloying element across diverse steel applications.

- Niobium pentoxide bolsters the strength and toughness of high-strength, low-alloy (HSLA) steel, which is widely utilized in the construction, transportation, and energy sectors.

- In stainless steel, niobium pentoxide enhances corrosion resistance, benefiting sectors like food processing, chemical processing, and medical equipment.

- Additionally, it strengthens pipeline steel, which is crucial for oil and gas transportation.

- According to the World Steel Association (worldsteel), global crude steel production dipped to 135.7 million tonnes (Mt) in December 2023 from 144.9 million tonnes (Mt) in November 2023. However, July 2024 saw a rebound to 152.8 million tonnes (Mt). Despite this, it represented a 4.7% decline from July 2023, highlighting the industry's challenges. However, as emerging economies intensify their infrastructure and construction initiatives, steel demand is set to recover in the coming years.

- Additionally, bolstered steel production capacities in nations like China, Japan, and the United States have further fueled global steel output, thereby supporting the growth of the market studied.

- As per the World Steel Association, Japan's steel production in July 2024 stood at 7.1 Mt, marking a 3.8% decline from the same month in 2023. Year-to-date figures show a production of 49.8 Mt, reflecting a 2.8% year-on-year drop.

- The United States, ranked as the fourth-largest producer of crude steel globally, reported a production of 6.9 Mt in July 2024, witnessing a modest increase of 2.1%. However, the year-to-date production figures were at 46.9 Mt, indicating a decline of 1.8%, as per the World Steel Association.

- Germany showcased a positive trend, producing an estimated 3.1 Mt in July 2024, which is a 4.8% increase. Year-to-date, Germany's production reached 22.5 Mt, marking a notable 4.5% rise, according to data from the World Steel Association.

- Brazil led the pack with the highest growth, producing 3.1 Mt in July 2024, an impressive increase of 11.6%. Year-to-date, Brazil's production stood at 19.4 Mt, up by 3.3%, as reported by the World Steel Association.

- In 2023, South Africa's crude steel production reached approximately 4,871.0 kilotons, marking a growth rate of about 10.64% from the previous year. This surge in production, as reported by the World Steel Association (worldsteel), underscored the country's steel sector and niobium pentoxide market.

- Steel is integral to various sectors, from construction and railroads to automotive manufacturing and consumer goods. Over the last decade, industrialization in developing nations, especially India, has significantly boosted steel demand.

- Given these dynamics, the niobium pentoxide market is poised for substantial growth in the coming years.

Asia Pacific Region is Expected to Dominate the Market

- Asia-Pacific is set to dominate the niobium pentoxide market, emerging as the fastest-growing region during the forecast period. This growth is driven by rising demands across various applications, such as niobium metal, optical glass, supercapacitors, superalloys, and ceramics, especially in countries like China, India, South Korea, Japan, and several Southeast Asian nations.

- Niobium pentoxide and its derivatives play a crucial role in iron and steel production. Adding niobium enhances steel's strength and boosts its resistance to high-temperature oxidation and corrosion. Niobium also lowers the ductile-brittle transition temperature and enhances welding properties and formability. It's particularly vital in producing high-grade structural steel, high-strength low alloy (HSLA) steels, and stainless steel.

- HSLA steels, enriched with niobium, find primary applications in the automotive and construction sectors. Notably, around 80% of all automotive sheet steel grades are micro-alloyed with niobium, ensuring vehicles are fuel-efficient, safe, and durable.

- In India, data from the Society of Indian Automobile Manufacturers (SIAM) indicates that from January to March 2024, the production of passenger vehicles, commercial vehicles, three wheelers, two wheelers and quadricycle reached 7.39 million units. Specifically, sales for passenger and commercial vehicles were 1.14 million and 268 thousand units, respectively.

- In 2024, India is set to witness a 70% surge in the availability of affordable housing. According to Invest India, the construction sector is projected to attain a valuation of USD 1.4 trillion by 2025. With forecasts suggesting that over 30% of the population will be urban dwellers by 2030, there's a pressing need for 25 million more mid-end and affordable housing units. Recent reforms, such as the Real Estate Act, GST, and REITs, aim to expedite approvals and strengthen the construction industry, driving market growth.

- China stands as the globe's leading producer of iron and steel, with its output serving both domestic and international markets. As per the data from the World Steel Association, while China retained its title as the largest producer, it saw a 9.0% dip in output for July 2024, totaling 82.9 million tonnes (Mt). Year-to-date figures show China's production at 613.7 Mt, reflecting a 2.2% drop from 2023.

- According to BigMint, India's steel production is projected to grow by nearly 6% year-on-year, reaching 152 million tons by the close of FY2024/2025 (ending March 2025). The bulk of this projected output is anticipated to stem from steel mills utilizing blast furnaces.

- Niobium alloys are also pivotal in construction, especially for structural and load-bearing components. China, leading the global construction arena with 20% of worldwide investments, is set to spend nearly USD 13 trillion on buildings by 2030, signaling a robust market outlook.

- Data from the Plastics Export Promotion Council highlights that India achieved its highest monthly export of spectacles and goggles in December 2023, a milestone not seen in 60 months. The Indian optical market currently grapples with challenges like low-cost competition, reliance on imported lenses, and swiftly evolving consumer preferences. In 2023, the market for contact lenses in India was valued at approximately USD 164.30 million.

- According to the Boeing's Commercial Outlook (2023-2042) anticipates around 8,560 new aircraft deliveries in China by 2042. This surge in deliveries is expected to elevate the demand for niobium pentoxide in manufacturing aircraft components, particularly engine blades.

- Niobium pentoxide is emerging as a key player in developing high-performance supercapacitors, owing to its high surface area, excellent electrical conductivity, stability, and durability..

- Data from China's National Energy Administration indicates that in 2023, the country installed over 31 gigawatts of new energy storage systems, with projections reaching 36 gigawatts by 2024. Endorsed by Chinese leadership, these new energy storage solutions encompass lithium-ion batteries, supercapacitors, and flow batteries.

- Given these dynamics, the niobium pentoxide market in the Asia-Pacific region is poised for steady growth during the forecast period.

Niobium Pentoxide Industry Overview

The niobium pentoxide market is consolidated in nature. The major players (not in any particular order) include CBMM, Ximei Resources Holding Limited, JSC Solikamsk Magnesium Plant, AMG, and JX Advanced Metals Corporation, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Report

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Demand for Niobium Pentoxide in the Optics Industry

- 4.1.2 Increasing Demand for High-quality Steel from the Manufacturing Sector

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Concerns about Health Issues Caused by Acute Exposure to Niobium Pentoxide

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Grade

- 5.1.1 Industrial Grade (purity: 99.0% to 99.8%)

- 5.1.2 3N

- 5.1.3 4N

- 5.2 Application

- 5.2.1 Niobium Metal

- 5.2.2 Optical Glass

- 5.2.3 Supercapacitors

- 5.2.4 Superalloys

- 5.2.5 Ceramics

- 5.2.6 Other Applications

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 NORDIC Countries

- 5.3.3.7 Turkey

- 5.3.3.8 Russia

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 Qatar

- 5.3.5.3 United Arab Emirates

- 5.3.5.4 Nigeria

- 5.3.5.5 Egypt

- 5.3.5.6 South Africa

- 5.3.5.7 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers, Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/ Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 AMG

- 6.4.2 CBMM

- 6.4.3 Chengdu Huarui Industrial Co., Ltd.

- 6.4.4 F&X Electro-Materials Limited

- 6.4.5 Hebei Suoyi New Material Technology Co., Ltd.

- 6.4.6 JSC Solikamsk Magnesium Plant

- 6.4.7 JX Advanced Metals Corporation

- 6.4.8 Kurt J. Lesker Company

- 6.4.9 Merck KGaA

- 6.4.10 Mitsui Mining & Smelting Co. Ltd.

- 6.4.11 MPIL

- 6.4.12 Taki Chemical Co., Ltd.

- 6.4.13 XIMEI Resources Holding Limited

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Demand from the Biomedical Sector

- 7.2 Other Opportunities

2026-2034年全球五氧化二鈮市場規模、佔有率、趨勢和成長分析報告

2026-2034年全球五氧化二鈮市場規模、佔有率、趨勢和成長分析報告 鈮及鈮合金市場按類型、應用、終端用戶產業、形態、等級及生產方法分類-2026-2032年全球預測

鈮及鈮合金市場按類型、應用、終端用戶產業、形態、等級及生產方法分類-2026-2032年全球預測 鈮:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)五氧化二鈮市場依應用、終端用戶產業、等級、製造流程、形狀及粒徑分類-2025-2032年預測

鈮:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)五氧化二鈮市場依應用、終端用戶產業、等級、製造流程、形狀及粒徑分類-2025-2032年預測 五氧化二鈮市場規模、佔有率及成長分析(按等級、應用和地區)-產業預測,2025-2032

五氧化二鈮市場規模、佔有率及成長分析(按等級、應用和地區)-產業預測,2025-2032 全球五氧化二鈮市場

全球五氧化二鈮市場 2032 年鈮市場預測:按類型、純度等級、通路、應用、最終用戶和地區進行的全球分析

2032 年鈮市場預測:按類型、純度等級、通路、應用、最終用戶和地區進行的全球分析 全球鈮市場規模研究,按類型(鈮鐵、鈮氧化物、鈮金屬)、按應用(結構鋼、汽車鋼、管道鋼、不銹鋼等)和區域預測 2022-2032

全球鈮市場規模研究,按類型(鈮鐵、鈮氧化物、鈮金屬)、按應用(結構鋼、汽車鋼、管道鋼、不銹鋼等)和區域預測 2022-2032 五氧化二鈮市場- 按等級(3N、4N)按應用(鈮金屬、光學玻璃、合金製造、金屬提取、電容器)、按最終用途行業(催化、儲能、陶瓷和玻璃)和預測,2024 - 2032 年

五氧化二鈮市場- 按等級(3N、4N)按應用(鈮金屬、光學玻璃、合金製造、金屬提取、電容器)、按最終用途行業(催化、儲能、陶瓷和玻璃)和預測,2024 - 2032 年