|

市場調查報告書

商品編碼

1906988

北美作物保護化學品:市場佔有率分析、行業趨勢、統計數據和成長預測(2026-2031 年)North America Crop Protection Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

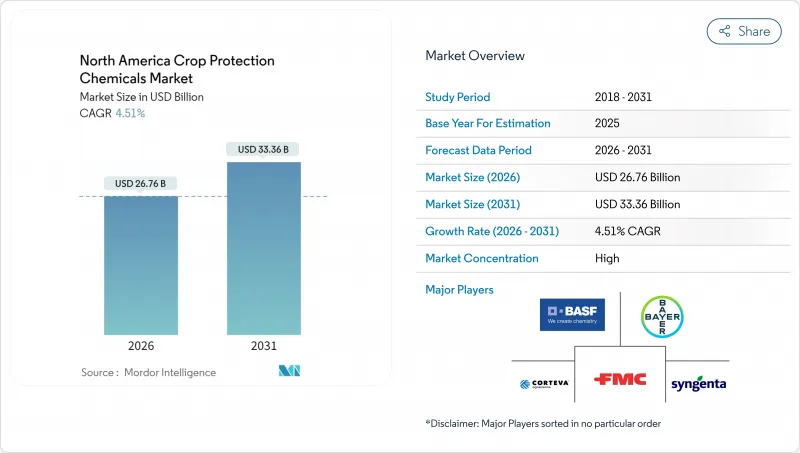

預計到 2026 年,北美作物保護化學品市場價值將達到 267.6 億美元,高於 2025 年的 256 億美元。

預計到 2031 年將達到 333.6 億美元,2026 年至 2031 年的複合年成長率為 4.51%。

雜草抗藥性、真菌病害激增以及監管機構對低風險活性成分日益成長的偏好,正在推動化學品需求,而精密農業工具則在減少浪費方面發揮重要作用。儘管種植者仍然青睞合成除草劑,因為它們在大面積田地中高效,但美國環保署 (EPA) 的快速核准流程正在推動生物製劑和生物合理性製劑的迅速擴張。該地區大規模的糧食生產基地、美國墨加協定 (USMCA) 下穩定的出口管道以及保護性耕作措施的碳權激勵,都有助於維持支出,儘管傳統化學品面臨訴訟。隨著主要企業整合種子、化學品和數位農藝技術以贏得市場佔有率,同時應對日益嚴格的基準值,競爭仍然激烈。

北美作物保護化學品市場趨勢與洞察

加速採用耐除草劑性狀

在主要產區,耐除草劑大豆的推廣率已超過95%,玉米的推廣率也達到了89%。這些特性使得除草劑的後處理窗口期得以延長,從而增加了季節性除草劑的使用量,並提高了作物輪作的柔軟性。隨著抗Glyphosate雜草(例如長芒莧)日益受到關注,美國環保署批准了基於麥草畏和2,4-D的平台,引入了新的作用機制。諸如科迪華的Enlist E3和拜耳的XtendFlex等組合技術正在推高價格,並促進化學品和種子捆綁包裝的銷售。整合變數施藥技術最佳化了特定區域的用藥劑量,進一步鞏固了這些特性在現代農藝中的地位。儘管面臨來自非專利藥的價格壓力,基因技術與精準儀器的協同作用仍維持著對選擇性除草劑的需求。

精準噴灑設備可降低每英畝成本

正如約翰迪爾的「目視噴灑」田間試驗所證明的那樣,電腦視覺噴霧器能夠逐一識別雜草,在保持有效控制的同時,減少高達77%的化學藥劑用量。美國農業部農民補助津貼(美國 FARMER grants)的公共支持正在加速這項技術的普及,因為它可以抵消設備成本。機載感測器能夠即時調整噴灑量,最大限度地減少重疊和漂移,從而降低投入成本,並解決監管方面對脫靶行為的擔憂。減少補藥時間和節省人力成本提高了管理數千英畝土地的大型農場的運作效率。設備經銷商現在將數據分析服務的訂閱服務捆綁銷售,使種植者能夠檢驗節省的成本,並鼓勵他們繼續購買相容的化學藥劑。

加拿大提案的最大殘留限量基準值將限制出口

加拿大衛生署提案將幾種活性成分(包括2,4-D)的最大殘留基準值(MRL)減半,這些成分適用於可能因國際買家採用更嚴格標準而面臨出口風險的農產品。標準的差異將要求生產商達到最低標準,從而增加分析檢測成本,並促使他們轉向使用低殘留農藥。依賴出口的卑詩省和安大略省的生產商預計運輸時間將縮短,合規文件工作量將增加。化學品製造商正在為殘留研究和標籤修訂撥出額外預算,這可能會延長新產品的投資回收期。

細分市場分析

到2025年,除草劑將佔北美作物保護化學品市場收入的51.65%,反映出1.8億英畝玉米和大豆田普遍依賴化學除草。精準施藥技術和性狀驅動的選擇性促使種植者繼續偏好後處理產品,以在整個生長季節保護產量潛力。抗性管理需要多種作用機制,加上保護性耕作措施導致除草劑用量增加,預計到2031年,該細分市場將以4.88%的複合年成長率成長。同時,焦油斑病和大豆銹病的日益普遍正在加速殺菌劑的使用,並使整體支出更加多元化。雖然殺蟲劑面臨著來自生物競爭和日益嚴格的授粉媒介保護條例法規的壓力,但它們在針對西部玉米根蟲零星爆發的綜合防治方案中仍然至關重要。

可疊加使用的生物除草劑正逐漸被採用,尤其是在對殘留基準值有限制的蔬果面積。主要企業正在推出微膠囊配方,將合成活性成分和微生物活性成分結合,以延長藥效持續時間,同時滿足環境標準。產品管理舉措正在教育種植者輪作和使用覆蓋作物來減少抗藥性的產生。這些趨勢共同作用,使得除草劑即使在整體化學成分變化的情況下,仍能保持其在市場上的基石地位。

北美作物保護化學品市場報告按功能(殺菌劑、除草劑、殺蟲劑等)、施用方法(化學灌溉、葉面噴布、燻蒸、種子處理等)、作物類型(經濟作物、果蔬作物、穀類等)和地區(加拿大、墨西哥等)進行細分。市場預測以價值(美元)和數量(公噸)兩種單位提供。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

- 調查方法

第2章 報告

第3章執行摘要和主要發現

第4章 主要產業趨勢

- 每公頃農藥消費量

- 活性成分價格分析

- 法律規範

- 加拿大

- 墨西哥

- 美國

- 價值鍊和通路分析

- 市場促進因素

- 加速採用耐除草劑性狀

- 精準噴灑設備可降低每英畝成本

- 大豆銹病和焦油斑病迅速增加。

- 美國環保署 (EPA) 加速核准生物活性成分

- 排碳權計畫旨在鼓勵犁地

- 墨西哥政府對IPM工具的補貼

- 市場限制

- Glyphosate訴訟導致零售商停業

- 擬議降低加拿大最大基準值(MRL)限制了出口

- 生物替代品的興起對合成農藥的利潤率帶來壓力

- 由於西海岸港口堵塞,投入成本上漲

第5章 市場規模和成長預測(價值和數量)

- 按功能

- 消毒劑

- 除草劑

- 殺蟲劑

- 殺軟體動物劑

- 殺線蟲劑

- 透過應用方法

- 化學灌溉

- 葉面噴布

- 燻蒸

- 種子處理

- 土壤處理

- 按作物類型

- 經濟作物

- 水果和蔬菜

- 穀物和雜糧

- 豆類和油籽

- 草坪和觀賞植物

- 按地區

- 加拿大

- 墨西哥

- 美國

- 北美其他地區

第6章 競爭情勢

- 重大策略舉措

- 市佔率分析

- 企業趨勢

- 公司簡介

- Corteva Agriscience

- Syngenta Group

- Bayer AG

- BASF SE

- FMC Corporation

- Sumitomo Chemical Co. Ltd.

- UPL Limited

- Nufarm Ltd.

- Albaugh LLC

- American Vanguard Corp.

- Bioceres Crop Solutions

- Gowan Company LLC

- Atticus LLC

- Helm Agro US Inc.

- Certis Biologicals

第7章:CEO們需要思考的關鍵策略問題

The North America crop protection chemicals market size in 2026 is estimated at USD 26.76 billion, growing from 2025 value of USD 25.6 billion with 2031 projections showing USD 33.36 billion, growing at 4.51% CAGR over 2026-2031.

Rising weed resistance, surging fungal outbreaks, and the widening regulatory preference for reduced-risk actives are reinforcing chemical demand even as precision-agriculture tools curb waste. Growers continue to favor synthetic herbicides for broad-acre efficiency, yet biological and biorational products are scaling rapidly under the United States Environmental Protection Agency (EPA) fast-track pathway. The region's large grain footprint, stable export channels under the United States-Mexico-Canada Agreement, and carbon-credit incentives for conservation tillage all sustain spending despite litigation over legacy chemistries. Competitive intensity remains high as leading firms bundle seeds, chemistry, and digital agronomy to capture wallet share while navigating tightening residue thresholds.

North America Crop Protection Chemicals Market Trends and Insights

Accelerated herbicide-tolerant trait adoption

Adoption rates of herbicide-tolerant soybeans now exceed 95% while corn reaches 89% across principal production areas. These traits allow wider post-emergence windows that lift seasonal herbicide volumes and expand rotational flexibility. The EPA clearance of dicamba- and 2,4-D-based platforms delivers new modes of action just as glyphosate-resistant weeds such as Palmer amaranth intensify. Stacked technologies like Corteva Enlist E3 and Bayer XtendFlex foster premium pricing and encourage bundled chemistry-seed packages. Integrated variable-rate spraying optimizes dose by zone, further embedding these traits into modern agronomy. The resulting synergy between genetics and precision hardware sustains demand for selective herbicides despite price pressure from generics.

Precision-spraying equipment lowering cost per acre

Computer-vision sprayers identify individual weeds and reduce chemical volumes by up to 77% while maintaining control levels, as field trials of John Deere See and Spray demonstrate. Public support through the United States Department of Agriculture (USDA) FARMER grants accelerates adoption by offsetting equipment costs. On-board sensors adjust rates in real time, minimizing overlaps and drift, which lowers input spend and addresses regulatory scrutiny of off-target movement. The time saved on refills and the labor reductions boost operational efficiency for large farms that manage thousands of acres. Equipment dealers now bundle data analytics subscriptions that help growers verify savings, reinforcing repeat purchases of compatible chemistries.

Canada's proposed MRL cutbacks limiting exports

Health Canada proposes halving MRLs for several actives, such as 2,4-D, in agricultural exports at risk if foreign buyers adopt stricter thresholds. Divergent standards compel growers to meet the lowest common denominator, adding analytical testing costs and encouraging shifts toward lower-residue actives. Export-dependent producers in British Columbia and Ontario foresee tighter shipment windows and higher compliance documentation. Chemical firms allocate extra budget to residue studies and label amendments, elongating return-on-investment timelines for new products.

Other drivers and restraints analyzed in the detailed report include:

- Surge in soybean rust and tar spot outbreaks

- U.S. EPA fast-track approvals for biorational actives

- Rising biological alternatives squeezing synthetic margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Herbicides generated 51.65% of the North America crop protection chemicals market revenue in 2025, reflecting widespread reliance on chemical weed control across 180 million corn and soybean acres. Precision application and trait-driven selectivity support continuous grower preference for post-emergence products that safeguard season-long yield potential. The segment is projected to expand at a 4.88% CAGR through 2031 as resistance management requires multiple modes of action and as conservation tillage increases herbicide intensity. At the same time, fungicide usage accelerates due to expanding tar spot and soybean rust zones, further diversifying overall spending. Insecticides face pressure from biological competitors and tightened pollinator safety rules, yet remain essential in integrated programs for sporadic outbreaks of Western corn rootworm.

A shift toward stackable biological herbicides is emerging, particularly in fruit and vegetable acreage where buyers impose residue caps. Leading firms launch micro-encapsulated formulations that combine synthetic and microbial actives to prolong efficacy while meeting environmental standards. Product stewardship initiatives now educate growers on rotating chemistries and incorporating cover crops to slow resistance. Collectively these trends ensure that herbicides remain market linchpins even as the broader mix evolves.

The North America Crop Protection Chemicals Market Report is Segmented by Function (Fungicide, Herbicide, Insecticide, and More), Application Mode (Chemigation, Foliar, Fumigation, Seed Treatment and More), Crop Type (Commercial Crops, Fruits and Vegetables, Grains and Cereals, and More), and Geography (Canada, Mexico, and More). The Market Forecasts are Provided in Terms of Both Value (USD) and Volume (Metric Tons).

List of Companies Covered in this Report:

- Corteva Agriscience

- Syngenta Group

- Bayer AG

- BASF SE

- FMC Corporation

- Sumitomo Chemical Co. Ltd.

- UPL Limited

- Nufarm Ltd.

- Albaugh LLC

- American Vanguard Corp.

- Bioceres Crop Solutions

- Gowan Company LLC

- Atticus LLC

- Helm Agro US Inc.

- Certis Biologicals

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY AND KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Consumption of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 Canada

- 4.3.2 Mexico

- 4.3.3 United States

- 4.4 Value Chain and Distribution Channel Analysis

- 4.5 Market Drivers

- 4.5.1 Accelerated herbicide-tolerant trait adoption

- 4.5.2 Precision-spraying equipment lowering cost per acre

- 4.5.3 Surge in soybean rust and tar spot outbreaks

- 4.5.4 U.S. EPA fast-track approvals for biorational actives

- 4.5.5 Carbon-credit programs rewarding reduced tillage

- 4.5.6 Mexican government subsidies for IPM tools

- 4.6 Market Restraints

- 4.6.1 Glyphosate litigation-driven retailer delisting

- 4.6.2 Canada's proposed MRL cutbacks limiting exports

- 4.6.3 Rising biological alternatives squeezing synthetic margins

- 4.6.4 West Coast port congestion inflating input prices

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 Function

- 5.1.1 Fungicide

- 5.1.2 Herbicide

- 5.1.3 Insecticide

- 5.1.4 Molluscicide

- 5.1.5 Nematicide

- 5.2 Application Mode

- 5.2.1 Chemigation

- 5.2.2 Foliar

- 5.2.3 Fumigation

- 5.2.4 Seed Treatment

- 5.2.5 Soil Treatment

- 5.3 Crop Type

- 5.3.1 Commercial Crops

- 5.3.2 Fruits and Vegetables

- 5.3.3 Grains and Cereals

- 5.3.4 Pulses and Oilseeds

- 5.3.5 Turf and Ornamental

- 5.4 Geography

- 5.4.1 Canada

- 5.4.2 Mexico

- 5.4.3 United States

- 5.4.4 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 Corteva Agriscience

- 6.4.2 Syngenta Group

- 6.4.3 Bayer AG

- 6.4.4 BASF SE

- 6.4.5 FMC Corporation

- 6.4.6 Sumitomo Chemical Co. Ltd.

- 6.4.7 UPL Limited

- 6.4.8 Nufarm Ltd.

- 6.4.9 Albaugh LLC

- 6.4.10 American Vanguard Corp.

- 6.4.11 Bioceres Crop Solutions

- 6.4.12 Gowan Company LLC

- 6.4.13 Atticus LLC

- 6.4.14 Helm Agro US Inc.

- 6.4.15 Certis Biologicals

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

作物保護化學品市場:2026-2032年全球市場預測(依產品類型、作物類型、施用方法、配方及銷售管道)

作物保護化學品市場:2026-2032年全球市場預測(依產品類型、作物類型、施用方法、配方及銷售管道) 作物保護化學品市場規模、佔有率和趨勢分析報告:按產品、應用、地區和細分市場分類(2026-2033 年)

作物保護化學品市場規模、佔有率和趨勢分析報告:按產品、應用、地區和細分市場分類(2026-2033 年) 作物保護化學品市場規模、佔有率、成長率和全球市場分析:按類型、應用和地區分類,並預測至2026-2034年

作物保護化學品市場規模、佔有率、成長率和全球市場分析:按類型、應用和地區分類,並預測至2026-2034年 越南農作物保護化學品:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)非洲作物保護化學品:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)全球作物保護化學品市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

越南農作物保護化學品:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)非洲作物保護化學品:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)全球作物保護化學品市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年全球作物保護化學品市場報告

2026年全球作物保護化學品市場報告 作物保護化學品市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、原料、應用方法、地區和競爭格局分類,2021-2031年化肥和農藥市場按產品類型、作物類型、配方、原料、作用方式、施用方法、最終用戶和分銷管道分類-全球預測(2026-2032 年)呋蟲胺技術市場按作物類型、製劑、應用、最終用途產業和分銷管道分類,全球預測,2026-2032年

作物保護化學品市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、原料、應用方法、地區和競爭格局分類,2021-2031年化肥和農藥市場按產品類型、作物類型、配方、原料、作用方式、施用方法、最終用戶和分銷管道分類-全球預測(2026-2032 年)呋蟲胺技術市場按作物類型、製劑、應用、最終用途產業和分銷管道分類,全球預測,2026-2032年