|

市場調查報告書

商品編碼

1906987

印度紙包裝市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)India Paper Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

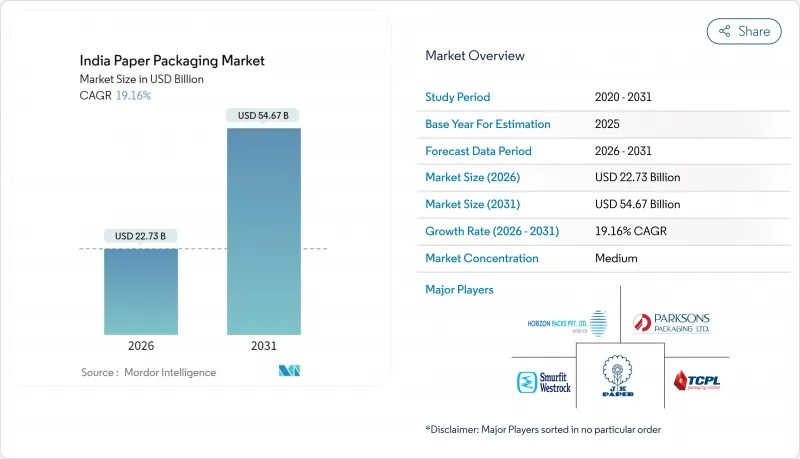

印度紙包裝市場規模預計到 2026 年將達到 227.3 億美元,高於 2025 年的 190.7 億美元。

預計到 2031 年,該產業規模將達到 546.7 億美元,2026 年至 2031 年的複合年成長率為 19.16%。

電子商務的蓬勃發展、塑膠使用限制以及快速消費品(FMCG)需求的不斷成長,正推動著輕質、可回收基材在初級和二級包裝領域的需求。印度所有28個邦/州對某些一次性塑膠的監管禁令加速了替代進程,同時,品牌所有者正投資於優質阻隔塗層紙板,以履行其永續性並滿足消費者期望。數位印刷技術在標籤生產線上的滲透率已達18%,支援靈活生產、生產線末端客製化以及防偽。儘管市場成長,但牛皮紙價格波動帶來的原料風險以及來自具有成本競爭力的免稅東協進口產品的壓力正在擠壓利潤空間,迫使國內造紙廠擴大規模、後向整合並保障再生纖維原料的供應。總體而言,印度紙包裝市場的參與企業正在投資塗層、模塑纖維和智慧標籤技術,以增強產品完整性並獲得價值鏈上的高價值應用。

印度紙包裝市場趨勢與洞察

電子商務物流需求加速成長

預計到2024年,印度線上訂單量將達52億件,高於上年的38億件。這將推動對瓦楞紙箱的需求,並促使企業採用更輕、更堅固的瓦楞紙箱。各大電商平台已部署自動化包裝線,以規範紙箱尺寸並減少空隙。快消業者則傾向於使用專為微型倉配中心設計的緊湊型紙箱。都市區的數位支付普及率已達87%,這使得貨到付款的包裝插頁得以取消,並減少了材料消耗。訂閱制電商模式提供了可預測的需求,使加工商能夠獲得專用生產線並簽訂原料契約,從而穩定生產量。

快速消費品及包裝食品銷售成長

預計到2024年,包裝食品產業將成長8.2%,這主要得益於全國12%的零售滲透率和大都會圈35%的零售滲透率。雀巢印度公司正投資260億盧比(約29.28億美元)擴大產能,顯示其對消費持續成長充滿信心。農村收入支持措施刺激了對小包裝品牌產品的需求,從而促進了塗佈紙板包裝的發展。乳製品分銷通路12%的年成長率主要由用於低溫運輸物流的保溫瓦楞紙包裝推動。這些變化正在加強食品巨頭與包裝供應商之間的多年期契約,穩定訂單量,而訂單量對印度紙包裝市場至關重要。

牛皮紙原物料價格波動

受海運運費上漲和能源成本波動的影響,2024年牛皮紙現貨價格波動幅度預計在15%至20%之間。這擠壓了缺乏避險能力的中小型瓦楞紙生產商的利潤空間。擁有自有紙漿廠的造紙企業則將影響降至最低,凸顯了產業整合的價值。價格的不確定性正在減緩產能擴張,因為投資回報模式變得更加靈活,也阻礙了企業與期望成本曲線穩定的品牌所有者簽訂長期合約。

細分市場分析

預計到2025年,瓦楞紙板將維持其在印度紙包裝市場53.65%的佔有率,這主要得益於電子商務對耐用性的要求以及工業承重需求。同時,預計到2031年,塗佈紙的複合年成長率將達到20.95%,這主要受高階日常消費品(FMCG)和醫藥應用領域對防潮防油性能的需求不斷成長的推動。印度紙板包裝市場預計將從2025年的59億美元成長到2031年的184.7億美元。政府採購優先考慮可再生基材,尤其是在公共食品分銷管道,這也促進了塗佈紙需求的成長。反映這些結構性利多因素的投資包括ITC投資80億印度盧比(約9.011億美元)建設的阻隔塗佈生產線。

先進的多層牛皮紙創新技術在減輕水泥袋重量的同時,保持了其抗破強度,從而幫助水泥袋從聚丙烯編織袋手中奪取市場佔有率。再生纖維含量的增加,以及FSC認證的廣泛應用,正幫助品牌達成範圍3碳減量目標。材料多樣化使造紙廠免受牛皮紙價格波動的影響,並擴大了印度特種紙包裝市場。

到2025年,軟包裝將佔印度紙質包裝市場53.74%的佔有率,主要得益於專為零食、糖果甜點和個人保健產品最佳化的包裝袋、小袋和包裝紙。由於阻隔塗層技術的應用,無塑膠複合材料得以普及,預計該細分市場將實現21.55%的複合年成長率。數位捲筒印刷機能夠根據細分市場的偏好定製圖形,從而推動銷售成長。同時,隨著全通路品牌協調商店和店內配送的設計,硬式折疊紙盒和瓦楞紙箱的市場佔有率也不斷擴大。

由於微瓦楞紙板和膠印覆膜等創新技術的出現,硬質包裝在化妝品和電子產品產業的滲透率不斷提高。這些技術可減少8-10%的纖維用量,同時提升印刷精度。專為藥品序列化設計的紙板生產線增加了防篡改功能,這對於符合監管要求至關重要,從而加速了硬包裝的普及。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 電子商務物流需求加速履約

- 快速消費品(FMCG)和包裝食品銷售成長

- 政府禁止使用某些一次性塑膠製品

- 品牌擁有者轉而使用優質輕質紙板

- 數位印刷和客製印刷的快速普及

- 供應鏈可追溯性與智慧標籤應用

- 市場限制

- 牛皮紙原料價格波動

- 東協免稅進口商品對利潤率帶來壓力

- 印度再生纖維的結構性短缺

- 國內瓦楞紙包裝製造設施產能過剩及市場細分

- 產業價值鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 宏觀經濟因素如何影響市場

- 價格分析——瓦楞紙箱和折疊紙箱

- 印度造紙業統計數據

- 目前紙張和紙板生產能力

- 生產量、銷售量和運轉率

- 書寫紙和印刷紙的分解

- 紙板和包裝紙的分解

- 特種紙和MG紙概述

第5章 市場規模與成長預測

- 依材料類型

- 牛皮紙

- 紙板

- 紙板

- 其他材料類型

- 依產品類型

- 軟紙包裝

- 小袋和包裝袋

- 包裝膜和薄膜

- 其他軟紙包裝

- 硬紙包裝

- 折疊紙箱

- 瓦楞紙箱

- 其他硬紙包裝

- 軟紙包裝

- 按包裝類型

- 初級包裝

- 二級包裝

- 三級/運輸包裝

- 按最終用途行業分類

- 食物

- 飲料

- 醫療和藥品

- 個人護理和化妝品

- 工業/電子設備

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Smurfit WestRock

- ITC Ltd.-Paperboards and Specialty Papers Div.

- JK Paper Ltd.

- Parksons Packaging Ltd.

- TCPL Packaging Ltd.

- Horizon Packs Pvt. Ltd.

- Oji Holdings Corp.(Oji India Packaging Pvt. Ltd.)

- Astron Paper and Board Mill Ltd.

- Kapco Packaging Ltd.

- Chaitanya Packaging Pvt. Ltd.

- Trident Paper Box Industries Pvt. Ltd.

- TGI Packaging Pvt. Ltd.

- Packman Packaging Pvt. Ltd.

- Emami Paper Mills Ltd.

- Andhra Paper Ltd.

- Pakka Ltd.

- PR Packagings Ltd.

- Total Pack Ltd.

第7章 市場機會與未來展望

India paper packaging market size in 2026 is estimated at USD 22.73 billion, growing from 2025 value of USD 19.07 billion with 2031 projections showing USD 54.67 billion, growing at 19.16% CAGR over 2026-2031.

Expansive e-commerce operations, plastic-use restrictions, and rising fast-moving consumer goods (FMCG) volumes combine to lift demand for lightweight, recyclable substrates across primary and secondary formats. Regulatory bans on selected single-use plastics in all 28 states accelerate substitution, while brand owners invest in premium barrier-coated paperboard to meet sustainability pledges and consumer expectations. Digital printing adoption, already at 18% penetration in label lines, supports agile production, late-stage customization, and counterfeit deterrence. Amid growth, raw-material exposure to kraft-paper price swings and cost-competitive zero-duty ASEAN imports pressure margins, prompting domestic mills to scale, backward-integrate, and secure recovered-fiber feedstock. Overall, India paper packaging market participants deploy capital toward coating, molded-fiber, and smart-label technologies that strengthen product stewardship credentials and capture higher-value applications along the supply chain.

India Paper Packaging Market Trends and Insights

Accelerating E-commerce Fulfillment Demand

India processed 5.2 billion online shipments in 2024 compared with 3.8 billion a year earlier, boosting corrugated-box volumes and encouraging adoption of lightweight high-strength grades. Large platforms added automated packing lines that standardize dimensions and reduce empty space. Quick-commerce operators favor compact corrugated formats designed for micro-fulfillment centers. Digital payment penetration reached 87% in urban areas, allowing removal of cash-on-delivery inserts and lowering material usage. Subscription-commerce models provide predictable demand, enabling converters to dedicate lines and secure raw-material contracts, thereby stabilizing throughput.

FMCG and Packaged-Food Volume Expansion

The packaged-food sector grew 8.2% in 2024, supported by organized retail penetration of 12% nationally and 35% in metros. Nestle India allocated INR 2,600 crore (USD 29.28 crore ) for capacity upgrades, underscoring confidence in sustained consumption growth. Rural-income support schemes stimulated demand for branded goods sold in small pack sizes that favor coated paperboard. Growth in the organized dairy channel at 12% annually requires insulated corrugated containers for cold-chain logistics. These shifts reinforce multiyear contracting between food majors and packaging suppliers, anchoring baseline order volumes for the India paper packaging market.

Kraft-paper input-price volatility

Spot kraft prices fluctuated 15-20% in 2024 due to ocean-freight spikes and energy-cost swings, eroding SME corrugator margins that lack hedging capacity. Mills with captive pulping muted exposure, underscoring integration's value. Price uncertainty delays capacity upgrades as payback models become fluid, and it hampers long-term contracts with brand owners expecting stable cost curves.

Other drivers and restraints analyzed in the detailed report include:

- Government Ban on Select Single-Use Plastics

- Rapid Adoption of Digital and On-Demand Printing

- Zero-duty ASEAN imports squeezing margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Corrugated board maintained 53.65% India paper packaging market share in 2025, driven by e-commerce durability requirements and industrial stacking needs. Yet coated paperboard registers a 20.95% CAGR to 2031, propelled by premium FMCG and pharmaceutical applications that demand moisture and grease barriers. India paper packaging market size for paperboard is projected to reach USD 18.47 billion by 2031, up from USD 5.9 billion in 2025. Coated variants also leverage government procurement favoring recyclable substrates, particularly in public food-distribution channels. Investments such as ITC's INR 800 crore (USD 9.011 crore) barrier-coating line reflect this structural tailwind.

Advanced multiwall kraft innovations cut weight in cement sacks without sacrificing burst strength, winning share from woven polypropylene. Recovered-fiber content rises alongside FSC certification uptake, helping brands achieve Scope-3 carbon reductions. Material diversification cushions mills against kraft price cycles and broadens the India paper packaging market addressable for specialized grades.

Flexible structures secured 53.74% India paper packaging market share during 2025 thanks to pouches, sachets, and wraps optimized for snack, confectionery, and personal-care items. The sub-category posts a 21.55% CAGR as barrier coatings allow plastic-free laminates. Digital web presses tune graphics to micro-market preferences, reinforcing volume gains. Meanwhile, rigid folding cartons and corrugated cases expand as omnichannel brands harmonize shelf-ready and ship-in-own-container designs.

Rigid formats benefit from micro-flute and litho-lam innovations that reduce fiber by 8-10% yet elevate print fidelity, deepening penetration in cosmetics and electronics. Cartonboard lines tailored for pharmaceutical serialization add tamper evidence crucial to regulatory compliance, accelerating rigid adoption.

The India Paper Packaging Market Report is Segmented by Material Type (Kraft Paper, Paperboard, Corrugated Board, and More), Product Type (Flexible Paper Packaging, Rigid Paper Packaging), Packaging Format (Primary Packaging, Secondary Packaging, Tertiary/Transit Packaging), End-Use Industry (Food, Beverage, Healthcare and Pharmaceuticals, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Smurfit WestRock

- ITC Ltd. - Paperboards and Specialty Papers Div.

- JK Paper Ltd.

- Parksons Packaging Ltd.

- TCPL Packaging Ltd.

- Horizon Packs Pvt. Ltd.

- Oji Holdings Corp. (Oji India Packaging Pvt. Ltd.)

- Astron Paper and Board Mill Ltd.

- Kapco Packaging Ltd.

- Chaitanya Packaging Pvt. Ltd.

- Trident Paper Box Industries Pvt. Ltd.

- TGI Packaging Pvt. Ltd.

- Packman Packaging Pvt. Ltd.

- Emami Paper Mills Ltd.

- Andhra Paper Ltd.

- Pakka Ltd.

- P.R. Packagings Ltd.

- Total Pack Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating e-commerce fulfilment demand

- 4.2.2 FMCG and packaged-food volume expansion

- 4.2.3 Government ban on select single-use plastics

- 4.2.4 Brand-owner switch to premium, lightweight board

- 4.2.5 Rapid adoption of digital and on-demand printing

- 4.2.6 Supply-chain traceability and smart-label adoption

- 4.3 Market Restraints

- 4.3.1 Kraft-paper input-price volatility

- 4.3.2 Zero-duty ASEAN imports squeezing margins

- 4.3.3 Structural shortage of recovered fibre in India

- 4.3.4 Excess domestic corrugator capacity and fragmentation

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

- 4.9 Pricing Analysis - Corrugated and Folding Carton

- 4.10 India Paper Industry Statistics

- 4.10.1 Current Capacity of Paper and Paperboard

- 4.10.2 Production, Sales and Utilisation Rates

- 4.10.3 Writing and Printing Paper Breakdown

- 4.10.4 Paperboard and Packaging Paper Breakdown

- 4.10.5 Specialty and MG Paper Overview

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Kraft Paper

- 5.1.2 Paperboard

- 5.1.3 Corrugated Board

- 5.1.4 Other Material Types

- 5.2 By Product Type

- 5.2.1 Flexible Paper Packaging

- 5.2.1.1 Pouches and Bags

- 5.2.1.2 Wraps and Films

- 5.2.1.3 Other Flexible Paper Packaging

- 5.2.2 Rigid Paper Packaging

- 5.2.2.1 Folding Carton

- 5.2.2.2 Corrugated Boxes

- 5.2.2.3 Other Rigid Paper Packaging

- 5.2.1 Flexible Paper Packaging

- 5.3 By Packaging Format

- 5.3.1 Primary Packaging

- 5.3.2 Secondary Packaging

- 5.3.3 Tertiary / Transit Packaging

- 5.4 By End-Use Industry

- 5.4.1 Food

- 5.4.2 Beverage

- 5.4.3 Healthcare and Pharmaceuticals

- 5.4.4 Personal Care and Cosmetics

- 5.4.5 Industrial and Electronic

- 5.4.6 Other End-Use Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Smurfit WestRock

- 6.4.2 ITC Ltd. - Paperboards and Specialty Papers Div.

- 6.4.3 JK Paper Ltd.

- 6.4.4 Parksons Packaging Ltd.

- 6.4.5 TCPL Packaging Ltd.

- 6.4.6 Horizon Packs Pvt. Ltd.

- 6.4.7 Oji Holdings Corp. (Oji India Packaging Pvt. Ltd.)

- 6.4.8 Astron Paper and Board Mill Ltd.

- 6.4.9 Kapco Packaging Ltd.

- 6.4.10 Chaitanya Packaging Pvt. Ltd.

- 6.4.11 Trident Paper Box Industries Pvt. Ltd.

- 6.4.12 TGI Packaging Pvt. Ltd.

- 6.4.13 Packman Packaging Pvt. Ltd.

- 6.4.14 Emami Paper Mills Ltd.

- 6.4.15 Andhra Paper Ltd.

- 6.4.16 Pakka Ltd.

- 6.4.17 P.R. Packagings Ltd.

- 6.4.18 Total Pack Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

可拉伸紙包裝市場:依材料等級、包裝形式、應用、終端用戶產業及銷售管道分類-2026-2032年全球市場預測紙包裝材料市場:依產品類型、材料類型、印刷技術和應用分類-2026-2032年全球預測

可拉伸紙包裝市場:依材料等級、包裝形式、應用、終端用戶產業及銷售管道分類-2026-2032年全球市場預測紙包裝材料市場:依產品類型、材料類型、印刷技術和應用分類-2026-2032年全球預測 紙包裝市場規模、佔有率、趨勢和預測:按產品類型、等級、包裝等級、最終用途產業和地區分類,2026-2034年

紙包裝市場規模、佔有率、趨勢和預測:按產品類型、等級、包裝等級、最終用途產業和地區分類,2026-2034年 全球再生紙包裝市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球再生紙包裝市場規模、佔有率、趨勢和成長分析報告(2026-2034) 中國紙包裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)亞太地區紙包裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)歐洲紙包裝市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)越南紙包裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)全球紙包裝市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球紙墊製造機械市場規模、佔有率、趨勢和成長分析報告(2026-2034)

中國紙包裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)亞太地區紙包裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)歐洲紙包裝市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)越南紙包裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)全球紙包裝市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球紙墊製造機械市場規模、佔有率、趨勢和成長分析報告(2026-2034)