|

市場調查報告書

商品編碼

1906206

歐洲物流自動化市場:市場佔有率分析、產業趨勢、統計數據和成長預測(2026-2031 年)Europe Intralogistics Automation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

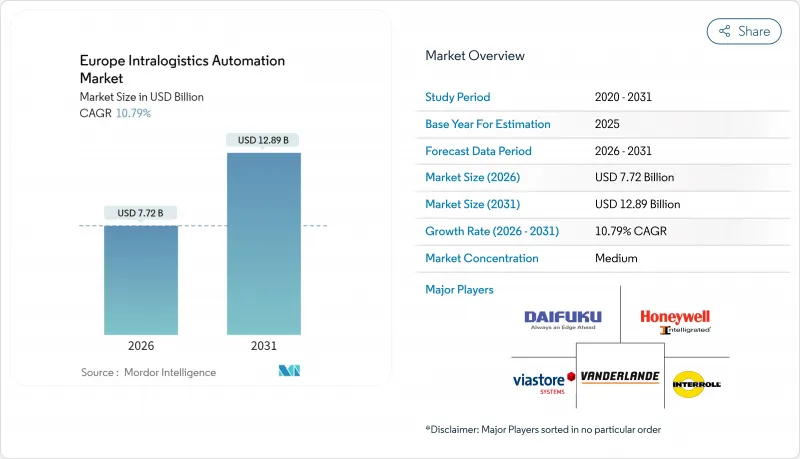

歐洲物流自動化市場規模預計到 2026 年將達到 77.2 億美元,高於 2025 年的 69.7 億美元,預計到 2031 年將達到 128.9 億美元,2026 年至 2031 年的複合年成長率為 10.79%。

電子商務交易量的激增、結構性勞動力短缺以及歐盟永續性嚴格的永續發展法規,正在加速對自動化儲存、揀选和物料輸送方案的資本投資。全設施專用5G網路支援的即時調整提高了資產利用率,而人工智慧驅動的預測性維護數位雙胞胎軟體則提高了系統運作。德國仍然是關鍵的需求中心和技術研發中心,而新興的東歐供應商正開始降低價格並縮短投資回收期。這些因素共同推動歐洲物流自動化市場在未來十年實現兩位數的成長。

歐洲物流自動化市場趨勢與洞察

電子商務的快速成長以及支援全通路的壓力

線上銷售的爆炸性成長正在重塑歐洲的履約格局。奧托集團投資2.6億歐元在伊爾瓦建造了一座高吞吐量的物流中心,每小時可處理18,000件商品,目標是實現60%訂單的隔天達。零售商和第三方物流(3PL)公司正在採用模組化的立方體和穿梭車系統,這些系統能夠在批量補貨和單件揀貨之間靈活切換,而不會中斷營運。都市區房地產的限制正在加速「貨到人」(G2P)微型倉配中心的普及。同時,立方體儲存系統使現有建築的SKU密度提高了三倍,提高了生產效率,並縮短了自動化投資的投資回收期,即使是中型企業也能從中受益。預計這些趨勢將推動資金持續流入擴充性的軟體定義解決方案,以確保物流配送能夠適應不斷變化的訂單履約。

歐盟27國面臨勞動力短缺和薪資上漲問題

勞動力老化、英國脫歐後的移民趨勢以及嚴格的工時法規,導致歐盟許多地區的物流業空缺率超過12%。在中歐和東歐,隨著企業使用協作機器人填補勞動力短缺,機器人採用率成長了28%,德國機械工程產業正向東歐出口承包系統以滿足此需求。每年6-8%的薪資成長進一步推高了成本效益,使資本投資更具優勢。這種轉變也體現在品質方面:企業越來越傾向於聘用能夠管理車輛軟體的技術人員,而不是人工負責人,這加速了原始設備製造商(OEM)與職業培訓機構之間的合作,以提升工人的技能。總而言之,勞動力短缺正在將自動化從歐洲物流自動化市場的可選項轉變為必需品。

高額資本投入和較長的投資回收期

全面的物流自動化通常需要500萬至1000萬歐元的前期投資,這對主導區域物流營運的中小型企業構成了一大障礙。一項調查發現,儘管生產力提升已得到證實,但仍有82%的倉庫經理對投資規模感到擔憂。利率上升進一步加劇了資金籌措壓力。雖然將成本分攤到多年合約中的「機器人即服務」(RaaS)模式越來越受歡迎,但大多數金融機構仍然傾向於資產抵押貸款。儘管像Heemskerk Fresh & Easy的生鮮設施這樣投資回收期不到四年的計劃緩解了人們的擔憂,但許多運營商仍在等待宏觀經濟前景更加明朗後再進行擴張。因此,資本支出的高度敏感度限制了歐洲物流自動化市場在低利潤細分領域的滲透。

細分市場分析

儘管自主移動機器人 (AMR) 在 2025 年的收入佔比相對小規模,但預計其在歐洲物流自動化市場中將以 11.21% 的複合年成長率 (CAGR) 實現最快成長。這一細分市場的成長動能主要得益於其對固定基礎設施的極低要求,這意味著可以在幾週內而非幾個月內完成車隊的添加或重新部署。同時,自動化倉庫/零售系統 (AS/RS) 將在 2025 年繼續保持歐洲物流自動化市場最大的佔有率 (27.32%),這主要得益於其成熟的立方體和穿梭車平台,這些平台已廣泛應用於食品雜貨和時尚產業的履約。

視覺SLAM導航部署成本的降低正推動自主移動機器人(AMR)在從電子商務到備件配送等各個領域的應用。凱傲集團的模組化機器人正是這種轉變的體現,使中型企業能夠即插即用。自動化立體倉庫(AS/RS)供應商正積極回應,推出將機器人穿梭車整合到高密度立方體中的混合設計,以維護其現有基本客群。自動化分類、堆疊和輸送子系統仍然是連接貨物處理工作站和運送碼頭的重要補充功能。這些類別之間日益增強的整合促使買家傾向於選擇能夠協調不同類型機器人控制軟體的平台供應商,從而加速歐洲物流自動化市場向整合生態系統的轉型。

汽車工廠憑藉著數十年的精益生產經驗,率先採用者了自動化牽引車隊、扭力追蹤揀選系統和即時品質分析等技術,預計到2025年將佔據歐洲物流自動化市場32.10%的佔有率。然而,醫藥和醫療保健產業正以11.40%的複合年成長率加速發展,反映出日益嚴格的序列化法規和低溫運輸需求。連鎖藥局Dr. Max憑藉其自動化物流中心,支援了55%的電子商務成長,為可追溯性要求如何直接轉化為自動化預算提供了一個真實案例。

郵政和小包裹業者正在部署高速分類機以應對B2C小包裹的激增,而食品和飲料加工商則正在實現箱揀自動化,以確保產品在24小時送達窗口期內保持新鮮度。機場和一般製造商分別透過現代化行李處理系統和準時制套件組裝來滿足需求。這帶來了更廣泛的基本客群,使歐洲物流自動化市場免受行業低迷的影響,同時也凸顯了對適應性強、符合監管要求的解決方案的需求。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 電子商務的快速成長以及支援全通路的壓力

- 歐盟27國面臨勞動力短缺和薪資上漲問題

- 人工智慧賦能的移動機器人和物聯網領域正快速發展。

- 部署 5G/專用 LTE 以實現即時調整

- 歐盟綠色交易對低碳物流的獎勵

- 城市微型倉配模式推動高密度自動化

- 市場限制

- 高額資本投入和較長的投資回收期

- 傳統 IT/OT 整合的複雜性

- 網路機器人面臨的日益嚴峻的網路安全威脅

- 由於半導體供應鏈中斷,計劃延期

- 監管環境

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 鄰近市場影響分析

- 拉伸纏繞機市場

- 貨運電梯市場

第5章 市場規模與成長預測

- 依產品類型

- 移動機器人

- 自動化倉庫系統(AS/RS)

- 自動分類系統

- 碼垛和卸垛系統

- 自動運輸系統

- 揀貨系統

- 按最終用戶行業分類

- 飛機場

- 郵件和小包裹

- 一般製造業

- 車

- 食品/飲料

- 零售、倉儲和配送

- 其他終端用戶產業

- 按組件

- 硬體

- 軟體

- 服務

- 按功能

- 貯存

- 揀選和回收

- 分類和收集

- 包裝和托盤堆垛

- 運輸和配送

- 按國家/地區

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- ABB Ltd.

- AutoStore ASA

- BEUMER Group GmbH and Co. KG

- Daifuku Co., Ltd.

- Dematic GmbH(KION Group)

- Exotec SAS

- Honeywell International Inc.

- Interroll Holding AG

- Jungheinrich Aktiengesellschaft

- Kardex Holding AG

- KNAPP AG

- KUKA Aktiengesellschaft

- Linde Material Handling GmbH

- Murata Machinery, Ltd.

- Ocado Group plc

- SSI Schafer AG

- Swisslog Holding AG

- TGW Logistics Group GmbH

- Toyota Industries Corporation

- Vanderlande Industries BV

- Viastore Systems GmbH

- WITRON Logistik+Informatik GmbH

第7章 市場機會與未來展望

Europe intralogistics automation market size in 2026 is estimated at USD 7.72 billion, growing from 2025 value of USD 6.97 billion with 2031 projections showing USD 12.89 billion, growing at 10.79% CAGR over 2026-2031.

Surging e-commerce volumes, structural labor shortages, and tightening EU sustainability mandates are accelerating capital spending on automated storage, picking, and material-handling solutions. Real-time orchestration made possible by facility-wide private 5G networks is raising asset utilization, while AI-driven predictive maintenance and digital-twin software are boosting system uptime. Germany remains the pivotal demand center and technology incubator, yet emerging Eastern European suppliers are beginning to lower price points and shorten payback periods. Taken together, these forces position the Europe intralogistics automation market for a decade of double-digit expansion.

Europe Intralogistics Automation Market Trends and Insights

E-commerce Boom and Omnichannel Fulfillment Pressure

Explosive online sales growth is rewriting fulfillment blueprints across Europe. Otto Group invested EUR 260 million in a high-throughput facility in Ilowa that processes 18,000 items per hour and targets next-day delivery for 60% of orders. Retailers and 3PLs are specifying modular cube and shuttle systems that can flex between bulk replenishment and single-item picking without halting operations. Urban real-estate constraints are accelerating adoption of goods-to-person micro-fulfillment centers, while cube-based storage allows operators to triple SKU density in legacy buildings. The resulting productivity gains are shortening the payback period on automation investments even for mid-tier merchants. These dynamics are expected to keep capital flowing toward scalable, software-defined solutions that future-proof fulfillment against shifting order profiles.

Labor Shortages and Wage Inflation Across EU27

An aging workforce, post-Brexit migration patterns, and stringent working-time regulations have pushed vacancy rates in logistics above 12% in many EU regions. Robot installations climbed 28% in Central and Eastern Europe as companies offset staff gaps with collaborative automation, and Germany's mechanical-engineering sector is exporting turnkey systems eastward to capture that demand. Wage inflation averaging 6-8% annually is further tilting the cost-benefit equation toward capital investment. The shift is also qualitative: facilities seek technicians who can manage fleet software rather than manual pickers, spurring partnerships between OEMs and vocational institutes to upskill workers. Collectively, labor scarcity is transforming automation from optional to essential across the Europe intralogistics automation market.

High CAPEX and Long ROI Horizons

Comprehensive intralogistics automation often requires EUR 5-10 million upfront, a hurdle for SMEs that dominate regional logistics. Survey work shows 82% of warehouse leaders remain uneasy about investment volumes despite proven productivity gains; rising interest rates add to financing strain. A growing Robotics-as-a-Service model spreads costs over multi-year contracts, yet most banks still prefer asset-backed lending. Projects demonstrating sub-four-year payback-such as Heemskerk Fresh & Easy's produce facility-are easing concerns, but many operators still delay scope expansion until macro-economic clarity improves. CAPEX sensitivity therefore constrains penetration of the Europe intralogistics automation market in lower-margin verticals.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Advances in AI-Powered Mobile Robotics and IoT

- 5G/Private-LTE Roll-outs Enabling Real-Time Orchestration

- Legacy IT/OT Integration Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Autonomous Mobile Robots (AMRs) accounted for a comparatively modest slice of 2025 revenue but are forecast to grow at 11.21% CAGR, the fastest within the Europe intralogistics automation market. The segment's momentum rests on minimal fixed infrastructure requirements: a fleet can be added or relocated in weeks rather than months. In contrast, Automated Storage and Retrieval Systems (AS/RS) retained the largest 27.32% share of Europe intralogistics automation market size in 2025 thanks to proven cube and shuttle platforms widely adopted in grocery and fashion fulfillment.

AMR adoption is spreading from e-commerce to spare-parts distribution as vision-SLAM navigation lowers commissioning costs. KION Group's modular robots illustrate this pivot by offering plug-and-play deployment for mid-cap firms. AS/RS suppliers are countering with hybrid designs that embed robot shuttles inside dense cubes, protecting their installed base. Automated sorting, palletizing, and conveyor subsystems remain critical complements that tie goods-to-person workstations into outbound docks. Convergence across these categories is prompting buyers to favor platform providers able to harmonize control software across mixed fleets, reinforcing the Europe intralogistics automation market's move toward integrated ecosystems.

Automotive plants locked in 32.10% of Europe intralogistics automation market share in 2025 as decades of lean-manufacturing expertise made them early adopters of automated tugger trains, torque-tracking pick systems, and real-time quality analytics. Yet the pharmaceuticals and healthcare vertical is accelerating at 11.40% CAGR, reflecting stricter serialization rules and cold-chain demands. Pharmacy chain Dr. Max commissioned an automated distribution hub that supports 55% e-commerce growth and illustrates how traceability requirements convert directly into automation budgets.

Post and parcel operators are embedding high-speed sorters to keep pace with B2C parcel surges, while food and beverage processors automate case picking to protect freshness under 24-hour delivery windows. Airports and general manufacturers round out demand with baggage-handling overhauls and just-in-sequence kitting respectively. The result is a broadening customer base that shields the Europe intralogistics automation market from sector-specific downturns and underscores the need for adaptable, regulation-aware solutions.

The Europe Intralogistics Automation Market Report is Segmented by Product Type (Mobile Robots, AS/RS, and More), End-User Industry (Airport, Post and Parcel, General Manufacturing, Automotive, Retail and Distribution, and More), Component (Hardware, Software, and Services), Function (Storage, Order Picking, Sorting, Packaging, Transportation), and Geography. Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- ABB Ltd.

- AutoStore ASA

- BEUMER Group GmbH and Co. KG

- Daifuku Co., Ltd.

- Dematic GmbH (KION Group)

- Exotec SAS

- Honeywell International Inc.

- Interroll Holding AG

- Jungheinrich Aktiengesellschaft

- Kardex Holding AG

- KNAPP AG

- KUKA Aktiengesellschaft

- Linde Material Handling GmbH

- Murata Machinery, Ltd.

- Ocado Group plc

- SSI Schafer AG

- Swisslog Holding AG

- TGW Logistics Group GmbH

- Toyota Industries Corporation

- Vanderlande Industries B.V.

- Viastore Systems GmbH

- WITRON Logistik + Informatik GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-commerce boom and omnichannel fulfilment pressure

- 4.2.2 Labour shortages and wage inflation across EU27

- 4.2.3 Rapid advances in AI-powered mobile robotics and IoT

- 4.2.4 5G / private-LTE roll-outs enabling real-time orchestration

- 4.2.5 EU Green Deal incentives for low-carbon intralogistics

- 4.2.6 Urban micro-fulfilment model driving high-density automation

- 4.3 Market Restraints

- 4.3.1 High CAPEX and long ROI horizons

- 4.3.2 Legacy IT / OT integration complexity

- 4.3.3 Rising cyber-security threats to networked robotics

- 4.3.4 Semiconductor supply-chain disruptions delaying projects

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Adjacent Market Influence Analysis

- 4.7.1 Stretch-Wrapping Machines Market

- 4.7.2 Goods Elevator Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Mobile Robots

- 5.1.2 Automated Storage and Retrieval Systems (AS/RS)

- 5.1.3 Automated Sorting Systems

- 5.1.4 Palletising and De-palletising Systems

- 5.1.5 Automated Conveyors

- 5.1.6 Order-Picking Systems

- 5.2 By End-user Industry

- 5.2.1 Airport

- 5.2.2 Post and Parcel

- 5.2.3 General Manufacturing

- 5.2.4 Automotive

- 5.2.5 Food and Beverage

- 5.2.6 Retail, Warehousing and Distribution

- 5.2.7 Other End-user Industries

- 5.3 By Component

- 5.3.1 Hardware

- 5.3.2 Software

- 5.3.3 Services

- 5.4 By Function

- 5.4.1 Storage

- 5.4.2 Order Picking and Retrieval

- 5.4.3 Sorting and Consolidation

- 5.4.4 Packaging and Palletising

- 5.4.5 Transportation and Conveyance

- 5.5 By Country

- 5.5.1 United Kingdom

- 5.5.2 Germany

- 5.5.3 France

- 5.5.4 Italy

- 5.5.5 Spain

- 5.5.6 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ABB Ltd.

- 6.4.2 AutoStore ASA

- 6.4.3 BEUMER Group GmbH and Co. KG

- 6.4.4 Daifuku Co., Ltd.

- 6.4.5 Dematic GmbH (KION Group)

- 6.4.6 Exotec SAS

- 6.4.7 Honeywell International Inc.

- 6.4.8 Interroll Holding AG

- 6.4.9 Jungheinrich Aktiengesellschaft

- 6.4.10 Kardex Holding AG

- 6.4.11 KNAPP AG

- 6.4.12 KUKA Aktiengesellschaft

- 6.4.13 Linde Material Handling GmbH

- 6.4.14 Murata Machinery, Ltd.

- 6.4.15 Ocado Group plc

- 6.4.16 SSI Schafer AG

- 6.4.17 Swisslog Holding AG

- 6.4.18 TGW Logistics Group GmbH

- 6.4.19 Toyota Industries Corporation

- 6.4.20 Vanderlande Industries B.V.

- 6.4.21 Viastore Systems GmbH

- 6.4.22 WITRON Logistik + Informatik GmbH

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

物流自動化市場:按組件、物流類型、技術、運作模式、部署類型、應用和最終用戶產業分類-2026-2032年全球市場預測

物流自動化市場:按組件、物流類型、技術、運作模式、部署類型、應用和最終用戶產業分類-2026-2032年全球市場預測 2026年全球容器化物流系統市場報告2026年全球數位雙胞胎物流控制塔顯示器市場報告

2026年全球容器化物流系統市場報告2026年全球數位雙胞胎物流控制塔顯示器市場報告 物流自動化市場分析與預測(至2035年):依類型、產品類型、服務、技術、元件、應用、流程、部署模式、最終使用者、解決方案分類2026年全球物流自動化市場報告

物流自動化市場分析與預測(至2035年):依類型、產品類型、服務、技術、元件、應用、流程、部署模式、最終使用者、解決方案分類2026年全球物流自動化市場報告 物流自動化市場-全球產業規模、佔有率、趨勢、機會及預測(按組件、功能、產業垂直領域、地區及競爭格局分類,2021-2031年)按車輛類型、自動駕駛等級、推進類型、應用程式和最終用戶分類的全球自動駕駛物流解決方案市場預測(2026-2032 年)

物流自動化市場-全球產業規模、佔有率、趨勢、機會及預測(按組件、功能、產業垂直領域、地區及競爭格局分類,2021-2031年)按車輛類型、自動駕駛等級、推進類型、應用程式和最終用戶分類的全球自動駕駛物流解決方案市場預測(2026-2032 年) 物流自動化:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

物流自動化:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 物流自動化市場規模、佔有率、成長及全球產業分析:按類型、應用和地區劃分的洞察與預測(2026-2034)

物流自動化市場規模、佔有率、成長及全球產業分析:按類型、應用和地區劃分的洞察與預測(2026-2034) 日本物流自動化市場報告(按組件、功能、企業規模、產業垂直領域和地區分類,2026-2034 年)

日本物流自動化市場報告(按組件、功能、企業規模、產業垂直領域和地區分類,2026-2034 年)