|

市場調查報告書

商品編碼

1906133

聚對苯二甲酸丙二醇酯:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Polytrimethylene Terephthalate - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

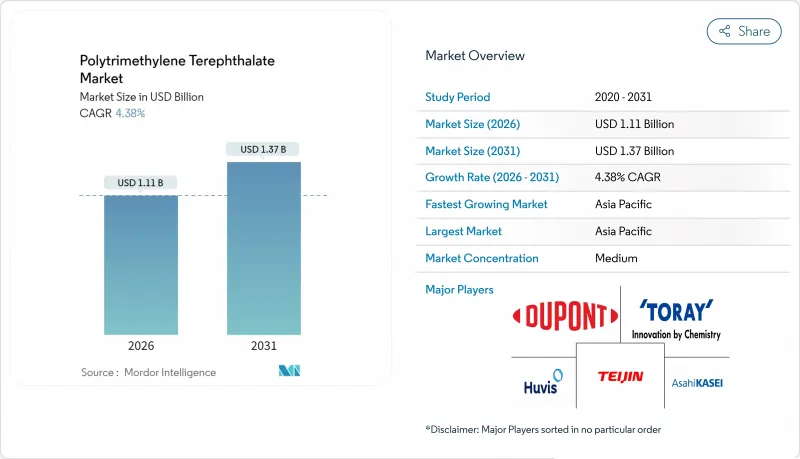

預計到 2025 年,聚對苯二甲酸丙二醇酯市值將達到 10.6 億美元,到 2026 年將成長至 11.1 億美元,到 2031 年將成長至 13.7 億美元,在預測期(2026-2031 年)內將成長到 4.38%。

這種適度的成長速度得益於該聚合物能夠彌合普通PET和高階工程塑膠之間的差距,其彈性回復率超過95%,染色鮮豔,且具有固有的抗污性。對舒適拉伸服飾的需求不斷成長、地毯產量擴大以及永續性需求,持續支撐著亞太、北美和歐洲市場的穩定銷售成長。持續存在的不利因素包括:與PET相比,其生產成本高出20-30%;1,3-丙二醇原料價格波動;以及PET和PBT生產商不斷拓展化學回收途徑帶來的持續競爭。然而,自2025年1月起禁止在紡織品上使用PFAS塗層,使得PTT固有的抗污性更具商業性吸引力,提升了其價值提案。

全球聚對苯二甲酸丙二醇酯市場趨勢及洞察

對彈性舒適布料的需求不斷成長

全球運動服和休閒品牌紛紛選用聚噻唑啉酮(PTT)布料,因為PTT纖維在拉伸後能比普通滌綸更可靠地恢復原長,從而延長服裝的使用壽命並保持其合身性。亞洲紡織品製造商正在拓展PTT與氨綸混紡的專用生產線,中國主要製造商報告稱,高彈針織布料的訂單實現了兩位數的成長。帝人前沿(Teijin Frontier)的多功能聚酯纖維布料系列展示瞭如何在不犧牲舒適性的前提下,將PTT與防紫外線和透氣性相結合。隨著零售商將銷售策略轉向利潤更高的功能性服飾,PTT在價格敏感型細分市場中的應用正在加速成長。

永續性發展推動生物基和可再生聚酯纖維的發展

PTT可透過利用玉米衍生的葡萄糖來生產1,3-丙二醇組分,從而達到31%的生物基含量。杜邦公司自2015年起已將此方法商業化。儘管生物基等級產品價格溢價高達15-20%,但歐盟和美國針對範圍3排放的政策壓力正加速服裝企業簽訂多年採購合約的步伐。 Nova Research預測,生物聚合物產能將於2023年達到440萬噸,年均成長率達17%。 PTT是該領域為數不多的幾種可商購的芳香族聚酯之一。目前,化學回收公司正在測試酵素解聚技術,以同時處理PET和PTT,在避免複雜分類流程的同時,拓展循環經濟的選擇範圍。

高昂的生產成本

生物來源1,3-丙二醇的價格仍比石油化學衍生的乙二醇高出25-30%,這限制了其與PET纖維的成本競爭力,尤其是在大眾市場T恤和包裝領域。有限的工廠規模(年產量均不超過20萬噸)限制了固定成本的多元化。預計到2024年,亞洲烯烴的利潤率將進一步下降,這將進一步擠壓特種聚合物的經濟效益。因此,PTT供應商正將目光投向高性能運動服、地毯和工程化合物等高階細分市場,以保護其利潤空間。

細分市場分析

到2025年,石油基聚對苯二甲酸丙二醇酯(PDT)仍將佔據66.05%的市場佔有率,這反映了其成熟的供應鏈和相對的成本優勢。然而,隨著品牌商力爭2030年實現聚酯中25-50%的可再生含量,生物基PDT的生產正以5.29%的複合年成長率快速成長。這一轉變推動生物基PDT市場的成長速度超過了整體產業需求。自2023年以來,發酵技術的進步已使生物基PDT的單位成本降低了12%。甘油在產品中的特定應用也降低了原料成本。該細分市場的收入成長在歐盟和美國最為顯著,這兩個國家的碳排放揭露法規正在提升綠色高級產品的經濟效益。

同時投資建造的酵素回收工廠使得利用回收的PTT和生物基PTT生產混合顆粒成為可能,從而可以在不影響紗線強度的前提下混合兩種材料。種植者認為這種方法可以有效對沖玉米價格波動,因為它使他們能夠根據市場相關人員靈活調整生物基PTT的含量。利害關係人預計,到2028年,隨著年產能達到40萬噸,生產規模的擴大將縮小與石油基PTT的價格差距,進一步增強聚對苯二甲酸丙二醇酯市場的長期永續性。

區域分析

預計到2025年,亞太地區將佔聚對苯二甲酸丙二醇酯(PTA)市場收入的60.20%,並在2031年之前以5.21%的複合年成長率成長,這主要得益於中國龐大的紗線生產基地以及Triexta地毯生產線在該地區的快速普及。中石化位於江蘇省的300萬噸級PTA工廠將於2024年運作,這標誌著上游產業的持續強勁發展,並確保了PTT一體化生產商對苯二甲酸的穩定供應。日本紡織製造商正致力於超細長絲的精密紡絲技術,而韓國樹脂供應商則在積極推進生物基材料的整合,鞏固了其在該地區市場領先地位。

北美仍然是杜邦公司第二大生產基地,這要歸功於杜邦TriExta地毯的成功經驗以及住宅對不含PFAS、易於打理的地板材料的青睞。美國地板材料製造商正在建造專門用於生產PTT連續長絲的新擠出工廠,分銷管道也透過性能保證計劃銷售這種纖維,以吸引養寵物的家庭。

政策主導的需求成長在歐洲尤其顯著,生態設計指令和生產者延伸責任制正在推動對低碳材料的需求。德國和斯堪地那維亞品牌指定使用生物基PTT纖維以達到科學碳目標,而義大利加工商則將回收的PTT與原生生物基材料混合,用於奢華時尚品牌。

南美洲和中東及非洲地區尚處於採用的早期階段,但巴西和埃及不斷成長的纖維出口表明,一旦當地紡紗廠建立供應協議,該地區將具有潛力。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 對拉伸舒適布料的需求不斷成長

- 致力於永續性:向生物基和可再生聚酯過渡

- 利用 TRIEXTA 拓展地毯和地板材料的應用

- 聚對苯二甲酸丙二醇酯(PTT)在3D列印原型製作耗材的應用

- 輕質複合材料在電動車的應用

- 市場限制

- 高昂的生產成本

- 與現有聚對苯二甲酸乙二醇酯 (PET) 和聚丁烯對苯二甲酸酯(PBT) 生產商的競爭

- 原料供應波動

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 按來源

- 石油衍生的聚對苯二甲酸丙二醇酯(PTT)

- 生物基聚對苯二甲酸丙二醇酯(PTT)

- 透過使用

- 服飾

- 家用紡織品

- 工業纖維

- 其他用途(汽車內裝零件等)

- 按地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 東南亞國協

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- Asahi Kasei Corporation

- DuPont

- Huvis

- RTP Company

- Shell plc

- Shenghong Holding Group Co., Ltd.

- Technip Energies NV

- Teijin Limited

- TORAY INDUSTRIES, INC.

- Xianglu Tenglong Group

第7章 市場機會與未來展望

The Polytrimethylene Terephthalate Market was valued at USD 1.06 billion in 2025 and estimated to grow from USD 1.11 billion in 2026 to reach USD 1.37 billion by 2031, at a CAGR of 4.38% during the forecast period (2026-2031).

This moderate pace comes from the polymer's ability to bridge commodity PET and higher-end engineering plastics, offering elastic recovery above 95%, vivid dye uptake, and inherent stain resistance. Rising demand for comfort-stretch apparel, expanding carpet output, and mounting sustainability mandates continue to underpin steady volume gains in Asia-Pacific, North America, and Europe. Persistent headwinds include 20-30% higher production costs versus PET, feedstock price volatility for 1,3-propanediol, and entrenched competition from PET and PBT producers who are scaling up chemical-recycling routes. Nonetheless, the shift away from PFAS coatings in textiles effective January 2025 lifts the value proposition of PTT by making its built-in stain repellence more commercially attractive.

Global Polytrimethylene Terephthalate Market Trends and Insights

Rising Textile Demand for Stretch-Comfort Fibres

Global activewear and athleisure brands are specifying PTT because the fibre recovers its original length after stretching more reliably than standard polyester, extending garment life and fit. Asian fabric mills are scaling dedicated lines to blend PTT with spandex, and leading mills in China are quoting double-digit order growth for high-elastic knit fabrics. Teijin Frontier's multifunctional polyester fabric range illustrates how PTT can be paired with UV protection and breathability finishes without compromising comfort. As retailers shift merchandising toward higher-margin performance clothing, adoption accelerates even in price-sensitive segments.

Sustainability Push Toward Bio-Based and Recyclable Polyester

PTT can reach 31% bio-content when its 1,3-propanediol component is derived from corn glucose, an approach already commercialised by DuPont since 2015. Policy pressure in the EU and US on Scope 3 emissions is prompting apparel groups to sign multiyear offtake agreements for bio-based grades despite premiums of 15-20%. The nova-Institut estimated bio-polymer capacity at 4.4 million t in 2023, growing 17% annually, with PTT one of the few commercial aromatic polyesters in the mix. Chemical recyclers are now trialling enzymatic depolymerisation that processes PET and PTT together, opening circularity options while avoiding complex sorting.

High Production Costs

Biological 1,3-propanediol remains 25-30% dearer than petrochemically derived ethylene glycol, hampering cost parity with PET fabrics, particularly in mass-market T-shirts and packaging. Limited plant scales-none exceeding 200 ktpa-restrict fixed-cost dilution. Asian olefin margins tightened through 2024, further squeezing specialty polymer economics. PTT suppliers therefore target premium niches such as performance sportswear, carpets, and engineering compounding to defend margins.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Carpet/Flooring Applications Using Triexta

- Polytrimethylene Terephthalate Adoption in 3D Printing Filaments for Prototyping

- Competition from PET and PBT Incumbents

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Petro-based grades retained a 66.05% position within the Polytrimethylene Terephthalate market in 2025, reflecting entrenched supply chains and relative cost advantages. Yet bio-based output is expanding at a 5.29% CAGR as brand owners commit to 25-50% renewable content in polyester by 2030. This shift keeps the Polytrimethylene Terephthalate market size for bio grades on a steeper curve than overall industry demand. Fermentation improvements have trimmed unit costs for bio-PDO by 12% since 2023, while side-stream valorisation of glycerol lowers net feedstock expenses. The segment's revenue gains are strongest in the EU and US, where carbon-intensity disclosure rules raise the economic return on green-premium products.

Parallel investments in enzymatic recycling plants enable hybrid pellets that blend recycled and bio-based PTT without compromising yarn tenacity. Producers see the route as a hedge against corn-price swings because bio-feedstock share can flex depending on market signals. Once capacity reaches 400 kt annually by 2028, stakeholders expect operating scale to narrow the price gap with petro-PTT, reinforcing the long-term sustainability narrative of the Polytrimethylene Terephthalate market.

The Polytrimethylene Terephthalate Market Report is Segmented by Source (Petro-Based PTT and Bio-Based PTT), Application (Apparel, Household Textiles, Industrial Fabrics, and Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific captured 60.20% of Polytrimethylene Terephthalate market revenue in 2025 and is projected to register a 5.21% CAGR to 2031, propelled by China's vast yarn spinning base and the rapid adoption of Triexta carpet lines in the region. Sinopec's 3 million t PTA plant commissioned in Jiangsu during 2024 signals ongoing upstream strength, ensuring reliable terephthalic acid flows to integrated PTT producers. Japanese fibre makers emphasise precision spinning for ultra-microfilaments, while South Korean resin suppliers push bio-feedstock integration, supporting regional leadership.

North America remains the second-largest cluster, underpinned by DuPont's legacy in Triexta carpets and the migration of residential homeowners toward PFAS-free, easy-clean flooring. US floor-covering mills have installed new extrusion capacity dedicated to PTT bulk-continuous-filament yarns, and distribution chains now market the fibre under performance warranty programmes that resonate with pet-owning households.

Europe reflects a policy-driven pull, with eco-design directives and extended-producer-responsibility schemes elevating demand for low-carbon materials. Brands in Germany and Scandinavia specify bio-PTT fabrics to meet Science-Based Targets, and converters in Italy blend recycled PTT with virgin bio content for luxury fashion houses.

South America and the Middle East and Africa remain early-stage adopters, yet rising textile exports from Brazil and Egypt suggest latent potential once local yarn spinners establish supply agreements.

- Asahi Kasei Corporation

- DuPont

- Huvis

- RTP Company

- Shell plc

- Shenghong Holding Group Co., Ltd.

- Technip Energies N.V.

- Teijin Limited

- TORAY INDUSTRIES, INC.

- Xianglu Tenglong Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Textile Demand for Stretch-Comfort Fibres

- 4.2.2 Sustainability Push Toward Bio-Based and Recyclable Polyester

- 4.2.3 Expansion of Carpet/Flooring Applications using Triexta

- 4.2.4 Polytrimethylene Terephthalate (PTT) Adoption in 3-D-Printing Filaments for Prototyping

- 4.2.5 Use in EV Lightweight Composite Components

- 4.3 Market Restraints

- 4.3.1 High Production Costs

- 4.3.2 Competition from Polyethylene Terephthalate (PET) And Polybutylene Terephthalate (PBT) Incumbents

- 4.3.3 Feed-Stock Supply Volatility

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Source

- 5.1.1 Petro-based Polytrimethylene Terephthalate (PTT)

- 5.1.2 Bio-based Polytrimethylene Terephthalate (PTT)

- 5.2 By Application

- 5.2.1 Apparel

- 5.2.2 Household Textiles

- 5.2.3 Industrial Fabrics

- 5.2.4 Other Applications (Automotive Interior Parts, etc.)

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 India

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 NORDIC Countries

- 5.3.3.8 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Asahi Kasei Corporation

- 6.4.2 DuPont

- 6.4.3 Huvis

- 6.4.4 RTP Company

- 6.4.5 Shell plc

- 6.4.6 Shenghong Holding Group Co., Ltd.

- 6.4.7 Technip Energies N.V.

- 6.4.8 Teijin Limited

- 6.4.9 TORAY INDUSTRIES, INC.

- 6.4.10 Xianglu Tenglong Group

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

再生聚對苯二甲酸乙二醇酯市場:2026-2032年全球市場預測(依原料種類、形態、等級、製造流程、顏色及應用分類)

再生聚對苯二甲酸乙二醇酯市場:2026-2032年全球市場預測(依原料種類、形態、等級、製造流程、顏色及應用分類) 2026年全球聚對苯二甲酸乙二醇酯(PET)杯市場報告

2026年全球聚對苯二甲酸乙二醇酯(PET)杯市場報告 全球聚對苯二甲酸乙二醇酯(PET)市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球聚對苯二甲酸乙二醇酯(PET)市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 聚對苯二甲酸乙二醇酯(PET)杯市場規模、佔有率和成長分析:按杯子設計與應用、原料、製造技術、最終用途和地區分類-2026-2033年產業預測

聚對苯二甲酸乙二醇酯(PET)杯市場規模、佔有率和成長分析:按杯子設計與應用、原料、製造技術、最終用途和地區分類-2026-2033年產業預測 生物基聚對苯二甲酸丙二醇酯(BioPTT)市場:市場規模-按地區、應用和預測至2034年

生物基聚對苯二甲酸丙二醇酯(BioPTT)市場:市場規模-按地區、應用和預測至2034年 聚對苯二甲酸乙二醇酯市場分析及預測(至2035年):類型、產品類型、應用、形態、材料類型、製程、最終用戶、功能、安裝類型

聚對苯二甲酸乙二醇酯市場分析及預測(至2035年):類型、產品類型、應用、形態、材料類型、製程、最終用戶、功能、安裝類型 南美洲聚對苯二甲酸乙二酯(PET):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)非洲聚對苯二甲酸乙二醇酯(PET):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)全球再生聚對苯二甲酸乙二醇酯市場規模、佔有率、趨勢和成長分析報告(2026-2034年)2026年全球再生聚對苯二甲酸乙二酯市場報告

南美洲聚對苯二甲酸乙二酯(PET):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)非洲聚對苯二甲酸乙二醇酯(PET):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)全球再生聚對苯二甲酸乙二醇酯市場規模、佔有率、趨勢和成長分析報告(2026-2034年)2026年全球再生聚對苯二甲酸乙二酯市場報告