|

市場調查報告書

商品編碼

1906082

綠石油焦和鍛燒石油焦:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)Green Petroleum Coke And Calcined Petroleum Coke - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

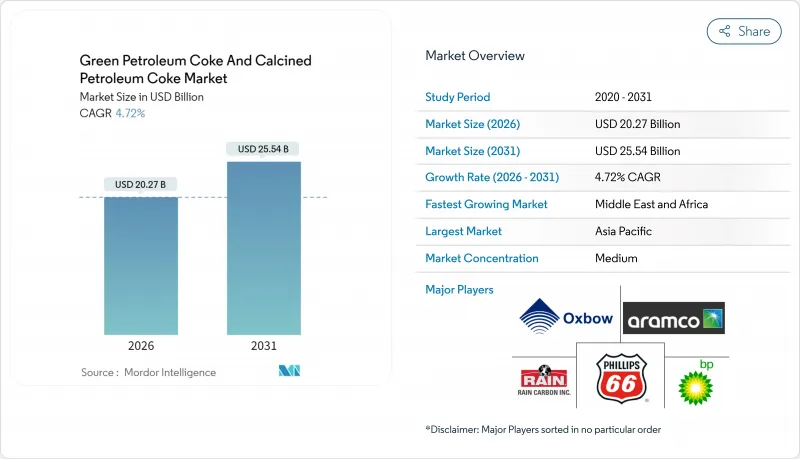

2025年,綠色石油焦和鍛燒石油焦市場價值為193.6億美元,預計從2026年的202.7億美元成長到2031年的255.4億美元,在預測期(2026-2031年)內複合年成長率為4.72%。

這一穩步成長反映了中東和亞太地區焦炭投資的延遲、中國陽極行業中硫含量限制的收緊,以及低硫焦炭和高硫焦炭之間價格差異的擴大。亞太地區保持需求主導,鋁提煉和水泥廠正在消化不斷成長的需求,而沙烏地阿拉伯、阿拉伯聯合大公國和奈及利亞的新煉焦廠則增加了可出口的供應。歐盟和北美的環境法規正在重塑貿易路線,有利於低排放源和垂直整合的供應商。競爭格局顯示,煉油廠對生焦原料的控制力增強,獨立鍛燒儘管面臨利潤壓力,仍在提高產能,而超低硫焦等特殊焦作為鋰離子電池負極材料,價格溢價較高。

全球綠色石油焦和鍛燒石油焦市場趨勢及洞察

擴大鋁提煉產能

2024年,全球鋁生產需要大量的鍛燒焦。這項需求鞏固了高品質、低硫原料的市場結構性基礎。作為主導力量的中國消耗了其中很大一部分。然而,隨著電價下跌和新建冶煉廠簽訂長期液化天然氣契約,區域冶煉廠的成長重點轉向了印度和波灣合作理事會(GCC)國家。阿曼和巴西新建的鍛燒計劃加劇了全球競爭,但其中許多設施仍依賴其他地區進口的低硫生焦。日益嚴格的品質標準,例如硫含量上限和釩含量限制,有利於能夠自主管理原料流的綜合煉廠,從而擠壓了高硫焦生產商的利潤空間。此外,冶煉廠目前已將範圍1二氧化碳排放上限納入長期承購契約,進一步提升了低排放焦炭的價值。

與煤炭相比,石油焦在水泥窯燃料使用上具有成本優勢。

2025年,高硫石油焦與煤炭的價格差異顯著,儘管運費波動,仍能支撐窯爐需求。印度降低了進口關稅,土耳其取消了對美國石油焦的關稅,擴大了需求基礎。展望未來,颶風季期間價格差異可能會縮小,促使一些生產商簽訂多季合約。脫碳路線藍圖設想到2050年,窯爐燃料將過渡為石油焦、煤炭和生質能的組合,預計即使碳成本上升,石油焦在中期內仍將保持一定的市場地位。印度和美國港口強制實施的倉儲設施將增加裝卸成本,但在大多數價格情境下,石油焦在燃料成本方面仍優於煤炭。

歐盟更嚴格的硫氧化物/粒狀物排放法規和碳邊境調節機制

歐盟的碳邊境調節機制正進入過渡性通報階段,預計在未來幾年內引入附加稅。石油焦等殘餘產品預計將逐步納入監管。進口商將被要求揭露直接和間接排放以及原產國的碳價格,這將降低高硫焦的成本優勢。在美國,儘管單煅燒爐會產生大量的二氧化硫排放,但許多工廠仍缺乏脫硫設備。如果加強聯邦法規以符合歐盟標準,維修固定成本的增加可能會促使貿易結構調整,轉向低排放工廠。

細分市場分析

2025年,燃料級產品佔生石油焦和鍛燒石油焦市場佔有率的60.95%,主要受水泥窯和鍋爐需求的驅動。儘管價格仍低於煤炭,但與歷史水準相比,價格差距已縮小。許多煉油廠正在最佳化延時焦爐的運作條件,優先生產燃料級產品,以最大程度地提高真空殘渣的產量而非品質。預計在預測期內,燃料級生石油焦和鍛燒石油焦的市場規模將穩定成長。

鍛燒焦的複合年成長率 (CAGR) 為 5.76%,主要受鋁陽極市場擴張以及對二氧化鈦、再碳化劑和石墨電極等特殊產品需求成長的推動。未來幾年,全球鍛燒焦產能可望大幅成長,主要得益於印度、阿曼和中國新增工廠的建設。然而,嚴格的硫含量限制了原料供應,迫使煉油廠添加脫硫添加劑並混合原料以滿足其應用需求。儘管該領域因振動引起的堆積密度溢價和較低的金屬雜質容忍度而享有較高的利潤率,但短期內供應過剩的風險可能會對現貨價格差構成壓力。

區域分析

到2025年,亞太地區將佔全球收入佔有率的47.90%,這主要得益於中國對石油焦和鋁預焙設備的巨大需求。鍛燒焦的進口量將逐年成長,主要來源國為美國、俄羅斯和沙烏地阿拉伯。日本和韓國擁有先進的針狀焦技術,而東南亞國協則在液化天然氣價格波動的情況下,在其水泥窯中使用高硫石油焦替代煤炭以控制成本。

受沙烏地阿拉伯、阿拉伯聯合大公國、科威特、埃及和奈及利亞新建焦化裝置帶來的原料供應增加的推動,中東和非洲的綠色石油焦和鍛燒石油焦市場預計到2031年將以5.62%的複合年成長率成長。像丹格特煉油廠這樣的綜合煉油廠正在逐步減少輕量產品的出口,轉而將重質殘渣油商業化。巴林和阿曼的鋁冶煉廠接近性,縮短了供應鏈,而阿拉伯中質原油的低硫特性也有利於生產高品質的鍛燒焦。

北美仍然是最大的出口地區,佔全球綠焦產量的大部分。然而,由於美國西海岸和墨西哥灣沿岸港口的環境法規導致物流成本上升,一些煉油商已與亞洲簽訂長期的船上交貨(FOB)合約。在歐洲,由於煉油廠產能下降,國內供應受到限制,對低硫焦炭的需求仍然強勁。歐盟的碳邊境調節附加稅(CBAM)將於2026年生效,預計將促使買方轉向使用來自中東、範圍1排放較低的原料。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 鋁提煉產能擴張趨勢

- 在水泥窯中,燃料石油焦比煤炭具有成本優勢。

- 中東焦化產能擴充延遲

- 電爐煉鋼石墨電極用針狀焦的需求

- 用於鋰離子電池的超低硫焦

- 市場限制

- 原油裂解價差的波動正在影響GPC的供應。

- 加強歐盟對硫氧化物(SOx)和顆粒物(PM)的監管以及碳邊境調節措施

- 港口城市當地民眾反對石油焦貿易

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 按類型

- 燃油等級

- 鍛燒焦

- 目的

- 綠色石油焦

- 鋁

- 燃料

- 鋼

- 金屬矽

- 其他(磚塊、玻璃、碳製品等)

- 鍛燒石油焦

- 鋁

- 二氧化鈦

- 再碳化市場

- 其他(針狀焦、碳製品等)

- 綠色石油焦

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- Aluminium Bahrain BSC(Alba)

- BP plc

- Chevron Corp

- China Petroleum & Chemical Corporation(Sinopec)

- CNOOC Limited

- ELSID SA

- Exxon Mobil Corp

- Indian Oil Corporation

- Maniayargroup

- Marathon Petroleum

- Numaligarh Refinery Limited

- Oxbow Corporation

- Petrocoque

- Phillips 66 Company

- Rain Carbon Inc.

- Reliance Industries Ltd

- Rio Tinto

- Saudi Aramco

- Saudi Calcined Petroleum Coke Company(SCPC)

- Valero Energy Corp

- Zhenjiang Coking And Gas Group Co. Ltd

第7章 市場機會與未來展望

The Green Petroleum Coke And Calcined Petroleum Coke Market was valued at USD 19.36 billion in 2025 and estimated to grow from USD 20.27 billion in 2026 to reach USD 25.54 billion by 2031, at a CAGR of 4.72% during the forecast period (2026-2031).

This steady climb reflects delayed coking investments in the Middle East and Asia-Pacific, tightening sulfur limits in China's anode sector, and widening price spreads between low-sulfur and high-sulfur grades. The Asia-Pacific region retains its demand leadership as aluminium smelters and cement plants absorb growing volumes, while new complexes in Saudi Arabia, the United Arab Emirates, and Nigeria increase exportable supply. Environmental regulations in the European Union and North America are reshaping trade lanes, favoring low-emission origins and vertically integrated suppliers. Competitive dynamics reveal refiners tightening their control over green coke feedstock, independent calciners adding capacity despite margin pressure, and specialty grades, such as ultra-low-sulfur coke, capturing premiums for use in lithium-ion battery anodes.

Global Green Petroleum Coke And Calcined Petroleum Coke Market Trends and Insights

Rising Aluminium Smelting Capacity Expansions

In 2024, the global aluminium output necessitated a significant amount of calcined coke. This demand solidifies a structural floor for premium low-sulfur feedstocks. China, the dominant player, consumed a substantial share. However, as power prices decline and new smelters secure long-term LNG contracts, regional smelter growth is pivoting towards India and the Gulf Cooperation Council states. While new calcining projects in Oman and Brazil heighten global competition, many of these facilities still rely on imported low-sulfur green coke from other regions. Tightening quality standards-such as stricter sulfur caps and vanadium restrictions-benefit integrated refiners who can manage streams internally, thereby squeezing margins for high-sulfur producers. Additionally, smelters are now incorporating scope-1 CO2 intensity ceilings into long-term offtake contracts, further elevating the value of low-emission coke grades.

Fuel-Grade Petcoke Cost Advantage Over Coal in Cement Kilns

In 2025, high-sulfur petcoke maintained a significant discount to coal, sustaining kiln demand despite volatile freight. India reduced import duties, while Turkey removed tariffs on U.S. supplies, broadening accessible demand pools. Forward trends indicate that discounts are narrowing during hurricane season, prompting some producers to secure multi-quarter contracts. Decarbonization roadmaps envision a transitional kiln fuel split of petcoke, coal, and biomass by 2050, preserving a medium-term niche for petcoke even as carbon costs rise. Covered storage mandates at Indian and U.S. ports add handling costs, yet the net fuel advantage over coal remains intact under most price scenarios.

Stricter SOx/PM Limits and Carbon Border Adjustment in European Union

The EU Carbon Border Adjustment Mechanism has entered transitional reporting and will impose fees in the coming years, with residual products, such as petcoke, positioned for phased inclusion in the future. Importers must disclose direct and indirect emissions, as well as the carbon prices in their origin countries, narrowing the cost advantages for high-sulfur coke. In the United States, stand-alone calciners emitted significant levels of SO2, yet many still lack scrubbers. If federal limits tighten to match EU standards, retrofits could add fixed costs, reshaping trade toward lower-emission plants.

Other drivers and restraints analyzed in the detailed report include:

- Capacity Build-Out of Delayed Coking Units in Middle-East Refineries

- Ultra-Low-Sulfur Coke for Li-Ion Battery Anodes

- Community Opposition to Petcoke Handling in Port Cities

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fuel-grade material held 60.95% of the Green Petroleum Coke and Calcined Petroleum Coke Market share in 2025, driven by demand from cement kilns and boilers. Prices are still undercutting coal, although the discount has narrowed against historical norms. Many refineries optimize delayed-coker operating severity to favor fuel-grade volumes, maximizing vacuum resid destruction over quality. The green petroleum coke and calcined petcoke market size for fuel-grade supply is expected to grow steadily during the forecast period.

Calcined coke is advancing at a 5.76% CAGR, stimulated by aluminium anode expansions and specialty demands in titanium dioxide, recarburizers, and graphite electrodes. Plant additions in India, Oman, and China could significantly increase global calcined capacity in the coming years. Yet sulfur tightening below 3% crimps effective feedstock, prompting refiners to apply desulfurizing additives and blend fit-for-purpose streams. The segment captures higher margins owing to vibrated bulk-density premiums and low metal impurity thresholds, although oversupply risk in the near future may pressure spot differentials.

The Green Petroleum Coke and Calcined Petroleum Coke Market Report is Segmented by Type (Fuel Grade and Calcined Coke), Application (Green Petroleum Coke: Aluminum, Fuel, Iron and Steel, Silicon Metal, and Others; Calcined Petroleum Coke: Aluminum, Titanium Dioxide, Re-Carburizing Market, and Others), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific captured 47.90% revenue share in 2025, anchored by China's substantial petcoke requirement and aluminium prebake capacity. Imports of uncalcined coke increased year over year, with the United States, Russia, and Saudi Arabia supplying the bulk. Japan and South Korea maintain advanced needle coke technology, while ASEAN cement kilns substitute high-sulfur pet coke for coal to manage costs amid volatile LNG prices.

The Middle East and Africa Green Petroleum Coke and Calcined Petroleum Coke Market is projected to grow at a 5.62% CAGR through 2031, driven by the introduction of new coking trains in Saudi Arabia, the UAE, Kuwait, Egypt, and Nigeria, which is expected to increase feedstock availability. Integrated complexes such as Dangote's refinery are moving beyond light-product exports to monetize heavy residue streams. Proximity to aluminium smelters in Bahrain and Oman shortens supply chains, while lower sulfur in Arabian medium crudes enables premium calcined output.

North America remains the largest exporter, accounting for a significant portion of the global green coke production. However, port-side environmental constraints on the U.S. West Coast and Gulf Coast increase logistics costs, prompting some refiners to enter long-term contracts for Asia-bound shipments delivered ex-ship. Europe's declining refinery slate curbs indigenous supply even as demand for low-sulfur CPC persists; EU CBAM fees, starting from 2026, will likely shift buyers toward Middle Eastern streams with lower scope-1 emissions profiles.

- Aluminium Bahrain B.S.C. (Alba)

- BP p.l.c

- Chevron Corp

- China Petroleum & Chemical Corporation (Sinopec)

- CNOOC Limited

- ELSID SA

- Exxon Mobil Corp

- Indian Oil Corporation

- Maniayargroup

- Marathon Petroleum

- Numaligarh Refinery Limited

- Oxbow Corporation

- Petrocoque

- Phillips 66 Company

- Rain Carbon Inc.

- Reliance Industries Ltd

- Rio Tinto

- Saudi Aramco

- Saudi Calcined Petroleum Coke Company (SCPC)

- Valero Energy Corp

- Zhenjiang Coking And Gas Group Co. Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising aluminium smelting capacity expansions

- 4.2.2 Fuel-grade petcoke cost advantage over coal in cement kilns

- 4.2.3 Capacity build-out of delayed coking units in Middle-East refineries

- 4.2.4 Needle-grade CPC demand from graphite electrodes for EAF steel

- 4.2.5 Ultra-low-sulfur coke for Li-ion battery anodes

- 4.3 Market Restraints

- 4.3.1 Volatile crude-oil crack spreads impacting GPC availability

- 4.3.2 Stricter SOx/PM limits and Carbon Border Adjustment in European Union

- 4.3.3 Community opposition to petcoke handling in port cities

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 Type

- 5.1.1 Fuel Grade

- 5.1.2 Calcined Coke

- 5.2 Application

- 5.2.1 Green Petroleum Coke

- 5.2.1.1 Aluminum

- 5.2.1.2 Fuel

- 5.2.1.3 Iron and steel

- 5.2.1.4 Silicon Metal

- 5.2.1.5 Others (Bricks, Glass, Carbon Products, etc)

- 5.2.2 Calcined Petroleum Coke

- 5.2.2.1 Aluminum

- 5.2.2.2 Titanium Dioxide

- 5.2.2.3 Re-carburizing Market

- 5.2.2.4 Others (Needle Coke, Carbon Products, etc)

- 5.2.1 Green Petroleum Coke

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 Aluminium Bahrain B.S.C. (Alba)

- 6.4.2 BP p.l.c

- 6.4.3 Chevron Corp

- 6.4.4 China Petroleum & Chemical Corporation (Sinopec)

- 6.4.5 CNOOC Limited

- 6.4.6 ELSID SA

- 6.4.7 Exxon Mobil Corp

- 6.4.8 Indian Oil Corporation

- 6.4.9 Maniayargroup

- 6.4.10 Marathon Petroleum

- 6.4.11 Numaligarh Refinery Limited

- 6.4.12 Oxbow Corporation

- 6.4.13 Petrocoque

- 6.4.14 Phillips 66 Company

- 6.4.15 Rain Carbon Inc.

- 6.4.16 Reliance Industries Ltd

- 6.4.17 Rio Tinto

- 6.4.18 Saudi Aramco

- 6.4.19 Saudi Calcined Petroleum Coke Company (SCPC)

- 6.4.20 Valero Energy Corp

- 6.4.21 Zhenjiang Coking And Gas Group Co. Ltd

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

石油焦市場:2026-2032年全球市場預測(依產品類型、形態、硫含量、應用、終端用戶產業及分銷通路分類)鍛燒石油焦市場:2026-2032年全球市場預測(依產品類型、純度等級、應用、最終用戶及通路分類)

石油焦市場:2026-2032年全球市場預測(依產品類型、形態、硫含量、應用、終端用戶產業及分銷通路分類)鍛燒石油焦市場:2026-2032年全球市場預測(依產品類型、純度等級、應用、最終用戶及通路分類) 全球石油焦市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球石油焦市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 石油焦市場規模、佔有率、趨勢及預測(按類型、應用和地區分類),2026-2034年

石油焦市場規模、佔有率、趨勢及預測(按類型、應用和地區分類),2026-2034年 2026年全球石油焦市場報告

2026年全球石油焦市場報告 鍛燒石油焦全球市場銷售報告、競爭分析及區域機會(2026-2032年)

鍛燒石油焦全球市場銷售報告、競爭分析及區域機會(2026-2032年) 石油焦化學品市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、地區和競爭格局分類,2021-2031年石油燃料市場-全球產業規模、佔有率、趨勢、機會、預測:依實體形態、應用、區域和競爭格局分類,2021-2031年綠色石油焦市場-全球產業規模、佔有率、趨勢、機會和預測:按產品類型、應用、終端用戶產業、地區和競爭格局分類,2021-2031年石油焦市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、應用、地區和競爭格局分類,2020-2030年預測

石油焦化學品市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、地區和競爭格局分類,2021-2031年石油燃料市場-全球產業規模、佔有率、趨勢、機會、預測:依實體形態、應用、區域和競爭格局分類,2021-2031年綠色石油焦市場-全球產業規模、佔有率、趨勢、機會和預測:按產品類型、應用、終端用戶產業、地區和競爭格局分類,2021-2031年石油焦市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、應用、地區和競爭格局分類,2020-2030年預測