|

市場調查報告書

商品編碼

1852192

氫氧化鋰:市場佔有率分析、產業趨勢、統計數據、成長預測(2025-2030)Lithium Hydroxide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

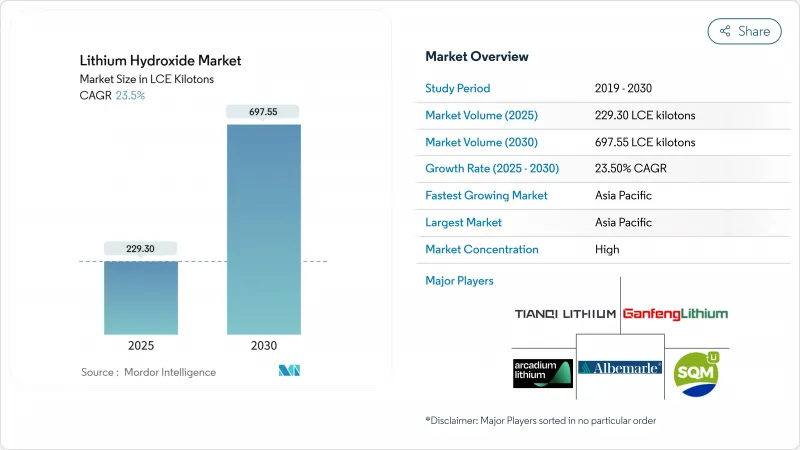

預計到 2025 年,氫氧化鋰市場規模將達到 229.30 千噸 LCE,到 2030 年將達到 697.55 千噸 LCE,在預測期(2025-2030 年)內複合年成長率為 23.5%。

電池化學品市場競爭加劇、電動車銷售激增以及直接鋰提取(DLE)技術的快速規模化應用,正在重塑全球供應鏈格局。亞太地區是最大的消費區域,佔全球消費量的40%,預計到2030年將以27.66%的年成長率成為成長最快的地區。汽車製造商已簽署長期採購契約,有效期至2024年,以確保高純度原料的供應;多家電池製造商也加快了垂直整合策略,以規避價格波動風險。同時,原物料價格的波動仍為計劃融資模式帶來挑戰,預計到2023年,原物料價格將從每噸81,500美元跌至每噸22,500美元。

全球氫氧化鋰市場趨勢與洞察

電動工具的需求增加

在建築和工業維護領域,無線電動工具正日益取代有線工具,因為鋰離子電池組具有更長的運作時間和更高的功率重量比。製造商正在推出針對高放電循環次數最佳化的電池規格,並傾向於採用富含氫氧化鋰的鎳鈷錳正極材料。北美和歐洲的專業承包商對無線工具的需求最為旺盛,因為勞動市場緊張,生產效率的提升至關重要。隨著建築資訊模型(BIM)工作流程的不斷普及,工人們需要在工地上擁有不受束縛的移動性,無線工具的普及速度將進一步加快。雖然這一細分市場的需求量不如電動車,但對於供應特殊正極材料的氫氧化物製造商而言,其利潤空間卻高於平均水準。

直接鋰萃取(DLE)的商業化釋放低成本原料的潛力

在IBAT位於猶他州的工廠,採用模組化吸附柱的現場規模試驗表明,鋰的回收率在幾小時內即可達到80-90%,而傳統的池塘蒸發法則需要數月時間。位於加州的ATLiS計劃獲得了13.6億美元的有條件貸款擔保,用於每年從地熱鹵水中生產2萬噸氫氧化鋰,這印證了貸款方對DLE公司擴充性的信心。更高的產量降低了每噸產品的資本密集度,並使在缺水地區也能運作成為可能,因為許多離子交換和薄膜分離技術消費量的補充水量比池塘法更少。這些經濟優勢增強了氫氧化鋰市場的長期供應前景,同時減少了對環境的影響。

高昂的生產成本

電池級氫氧化鋰工廠需要精密的雜質控制和昂貴的結晶迴路。雅寶公司已取消位於澳洲凱默頓工廠的擴建計劃,使其原計劃產能減半,現場員工人數減少40%。多年的投資回收期、嚴格的環境授權以及有限的濕式冶金人才儲備,都構成了高准入門檻,並減緩了新廠建設的步伐,尤其是在能源價格較高的地區。

細分市場分析

預計到2024年,鋰離子電池將佔氫氧化鋰市場需求的63%,並在2030年之前以26.77%的複合年成長率成長。光是這一領域就佔據了氫氧化鋰市場規模的最大佔有率,預計也將是噸位成長最快的領域。鎳鈷錳(NCM)和鎳鈷鋁(NCA)等以範圍為導向的化學體系,由於其合成需要氫氧化鋰而非碳酸鹽,因此支撐了結構性需求。相較之下,潤滑脂、空氣淨化系統和特殊合成預計將穩定貢獻,但貢獻幅度不大。歐盟日益嚴格的回收規定預計將在預測期後期建立二次供應管道,從而緩解而非取代原生需求。

儲能部署是成長最快的子應用領域。大型電池電站與可再生能源資產結合,需要具有長循環壽命的化學材料。例如,加州的多吉瓦時儲能裝置等計劃擴大採用富鎳正極材料,從而增加了氫氧化鋰的消耗量。隨著成本的下降,規模較小的商業和工業用戶電錶後端系統也加入了這一行列,確保氫氧化鋰市場保持多元化成長,涵蓋固定式和行動應用。

預計到2024年,電池級材料將佔據70%的市場佔有率,複合年成長率(CAGR)為25.55%。對鈉、鈣和重金屬雜質含量的嚴格監管,支撐了電池級材料與技術級材料之間的價格差異。像Livent這樣的製造商正在加大對重結晶和離子交換模組的投資,以實現總雜質含量低於100 ppm的目標。這項投資增加了資本密集度,但也加劇了市場競爭。技術級材料主要面向對雜質含量閾值較為寬鬆的潤滑脂和陶瓷市場,而工業級材料則主要面向水處理和特定合成過程。

隨著OEM廠商規格的不斷提高,電池級氫氧化鋰的市佔率將持續成長。新一代固態和高矽負極設計依賴精確的化學計量比和超低的含水量,從而提升了產品品質的溢價。擁有內部精煉能力的垂直整合型鹽水或硬岩原料生產商最能掌握這項利潤空間。

氫氧化鋰市場報告按應用(鋰離子電池、潤滑脂、其他)、終端用戶行業(汽車、家用電器、其他)、等級(電池級、技術級、工業級)、形態(一水合物、無水物)和地區(亞太地區、北美、歐洲、南美、中東和非洲)進行細分。

區域分析

亞太地區預計到2024年將佔據40%的氫氧化鋰市場佔有率,這得益於其無可比擬的電池製造能力以及下游正極、負極和電池組組裝的密集叢集。中國目前的政策方針優先考慮國產化率,並鼓勵大力開發內陸鹽沼資源和吸引外資;而日本和韓國則憑藉其在材料科學領域的長期優勢保持競爭力。印度也加入了競爭,在2025-2026會計年度聯邦預算中推出了國家製造業發展計劃,並對關鍵礦產實行關稅豁免,從而刺激了本土氫氧化鋰轉化提案。

北美地區的擴張取決於一項重要的資金支持計劃。美國能源部已向雅寶公司撥款1.5億美元,用於支持其位於金斯山的鋰輝石選礦廠建設,該選礦廠每年可供應160萬輛電動車所需的鋰輝石。現代汽車集團和SK安集團已核准在喬治亞建造一座價值50億美元的電池工廠,以滿足該地區對本地氫氧化物陰極材料的需求。這些舉措旨在減少對亞洲供應鏈的依賴,並符合美國《通膨控制法案》的採購標準。

南美洲仍然是重要的鋰供應中心。智利的國家鋰策略在維持國家監管的同時,吸引了私人企業的參與,新的地質勘測使蘊藏量估計值提高了28%。阿根廷吸引了力拓集團25億美元的礦業投資,並獲得了許多汽車製造商的訂單。預計到2024年,巴西的電動車銷量將激增85%,其中比亞迪佔70%的市場佔有率,顯示未來巴西國內對氫氧化物轉化的需求日益成長。

歐洲正透過嚴格的二氧化碳排放法規和全面的回收強制措施來加速產能擴張。德國在下一代正極材料的研發方面處於領先地位,歐盟電池法規規定了自2025年起鋰回收的最低配額。預計到2027年,芬蘭、法國和葡萄牙將有多家待開發區的轉化工廠運作,將豐富氫氧化鋰市場的供應基礎。追求戰略自主的地區可能會重新調整貿易流向,尤其是在中國實施擬議的技術出口管制措施的情況下。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 電動車需求不斷成長

- 電動工具的需求增加

- 直接鋰萃取 (DLE) 的商業化釋放了低成本氫氧化物原料的潛力

- 透過長期OEM合約降低拉丁美洲新增氫氧化物產能的風險

- 支持電池供應鏈的政府政策

- 市場限制

- 高昂的生產成本

- 原物料價格波動阻礙計劃資金籌措

- 人們越來越關注毒性問題

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模及成長預測(數量與價值)

- 透過使用

- 鋰離子電池

- 潤滑脂

- 純化

- 其他用途(聚合物、特殊化學合成)

- 按最終用途行業分類

- 車

- 消費性電子產品

- 能源儲存系統

- 其他(工業機械/非道路機械)

- 按年級

- 電池等級(LiOH*H2O 含量 56.5% 或更高)

- 技術級

- 工業級

- 按形式

- 一水合物

- 無水

- 按地區

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐國家

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 智利

- 其他南美洲

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Albemarle Corporation

- Arcadium Lithium

- Chengxin Lithium

- Ganfeng Lithium Group Co. Ltd.

- IGO Limited

- LevertonHELM Limited

- Nemaska Lithium(Investissement Quebec)

- Piedmont Lithium Inc.

- Shandong Ruifu Lithium Co., Ltd.

- Sinomine Resource Group

- SQM SA

- Tianqi Lithium Corporation

- Yahua Industrial Group Co.

第7章 市場機會與未來展望

The Lithium Hydroxide Market size is estimated at 229.30 LCE kilotons in 2025, and is expected to reach 697.55 LCE kilotons by 2030, at a CAGR of 23.5% during the forecast period (2025-2030).

Intensifying competition for battery-grade chemicals, fast-rising electric vehicle (EV) sales, and the rapid scale-up of direct lithium extraction (DLE) technologies are reshaping supply networks worldwide. Asia-Pacific commands the largest regional position with 40% of global consumption, delivering the fastest growth rate of 27.66% through 2030. Automakers locked in long-term procurement contracts in 2024 to secure high-purity feedstock, and several battery manufacturers accelerated vertical-integration strategies to hedge price swings. At the same time, stark feedstock price volatility-from USD 81,500/t to USD 22,500/t during 2023-continues to challenge project finance models.

Global Lithium Hydroxide Market Trends and Insights

Increasing Demand for Power Tools

Cordless power tools are replacing corded alternatives in construction and industrial maintenance because lithium-ion packs deliver longer run-time and a superior power-to-weight ratio. Manufacturers have launched cell formats optimized for high-discharge cycles, a profile that favors lithium hydroxide-rich nickel-cobalt-manganese cathodes. Uptake is strongest among professional contractors in North America and Europe, where tight labor markets place a premium on productivity gains. Continuous adoption of building-information-modeling workflows further accelerates cordless tool penetration because crews require untethered mobility on-site. Though smaller than EV demand, this niche yields above-average price realization for hydroxide producers supplying specialty cathode blends.

Commercialization of Direct Lithium Extraction (DLE) Unlocking Low-Cost Feedstock

Field-scale success at IBAT's Utah plant, utilizing modular adsorption columns, demonstrated 80-90% lithium recovery in hours versus the months needed for conventional pond evaporation. Project ATLiS in California secured a USD 1.36 billion conditional loan guarantee to deliver 20,000 t/y of lithium hydroxide from geothermal brine, affirming lender confidence in DLE scalability. Higher yields cut capital intensity per ton and enable operations in water-stressed regions because many ion-exchange and membrane variants consume less make-up water than pond systems. These economics bolster the long-run supply outlook for the lithium hydroxide market while reducing environmental footprints.

High Production Costs

Battery-grade lithium hydroxide plants demand sophisticated impurity control and costly crystallization circuits. Albemarle halted expansion of its Kemerton facility in Australia, slicing planned nameplate capacity in half and reducing onsite headcount by 40%. Multiyear payback periods, strict environmental licensing, and a limited pool of hydro-metallurgical talent maintain high entry barriers and slow new-build momentum, especially in regions with elevated energy tariffs.

Other drivers and restraints analyzed in the detailed report include:

- OEM-Backed Long-Term Contracts De-Risking New Capacity in Latin America

- Government Policies Supporting Battery Supply Chains

- Feedstock Price Volatility Hindering Project Financing

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Lithium-ion batteries generated 63% of 2024 demand and are forecast to expand at 26.77% CAGR through 2030. This segment alone accounts for the largest slice of the lithium hydroxide market size and delivers the highest incremental tonnage. Range-oriented chemistries such as nickel-cobalt-manganese (NCM) and nickel-cobalt-aluminum (NCA) require lithium hydroxide for synthesis rather than carbonate, anchoring structural demand. In contrast, lubricating greases, purified-air systems, and specialty synthesis remain steady but modest contributors. Growing recycling mandates in the European Union are expected to generate a secondary supply channel later in the forecast period, tempering but not displacing primary demand.

Energy storage deployments form the fastest-rising sub-application. Large-scale battery farms linked to renewable assets need long cycle-life chemistries. Projects such as California's multi-gigawatt-hour installations increasingly specify nickel-rich cathodes, reinforcing hydroxide consumption. As costs decline, smaller commercial and industrial behind-the-meter systems join the opportunity set, ensuring the lithium hydroxide market retains a diversified growth engine across stationary and mobile domains.

Battery-grade material held a commanding 70% share in 2024 and posts a forecast 25.55% CAGR, the highest within this segmentation. Stringent impurity controls on sodium, calcium, and heavy metals underpin price differentials over technical grade. Manufacturers such as Livent have invested in additional recrystallization and ion-exchange modules to achieve less than 100 ppm aggregate impurity limits. That investment raises capital intensity but also deepens competitive moats. Technical grade serves grease and ceramic markets where tolerance thresholds are looser, while industrial grade addresses water treatment and select synthesis routes.

The lithium hydroxide market share for battery-grade will keep rising as OEM specification sheets lengthen. Next-generation solid-state and high-silicon-anode designs rely on precise stoichiometry and ultra-low moisture content, factors that amplify quality premiums. Producers with vertically integrated brine or hard-rock feedstock plus in-house purification are best placed to capture this margin pool.

The Lithium Hydroxide Market Report is Segmented by Application (Lithium-Ion Batteries, Lubricating Grease, and More), End-Use Industry (Automotive, Consumer Electronics, and More), Grade (Battery Grade, Technical Grade, and Industrial Grade), Form (Monohydrate and Anhydrous), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa).

Geography Analysis

Asia-Pacific, with a 40% lithium hydroxide market share in 2024, benefits from unrivaled cell-manufacturing capacity and a dense cluster of downstream cathode, anode, and pack assemblers. Chinese policy directives now favor domestic sourcing, prompting active development of inland salt-lake brine as well as overseas equity stakes, while Japan and South Korea leverage long-standing material science expertise to stay competitive. India entered the fray with a National Manufacturing Mission and duty exemptions for critical minerals under the 2025-26 Union Budget, stimulating local hydroxide conversion proposals.

North America's expansion rests on large-scale funding packages. The DOE's USD 150 million grant to Albemarle supports a spodumene concentrator at Kings Mountain capable of feeding 1.6 million EVs annually. Hyundai Motor Group and SK On approved a USD 5 billion battery cell plant in Georgia, anchoring regional cathode demand for locally produced hydroxide. These initiatives aim to cut reliance on Asian supply chains and meet US Inflation Reduction Act sourcing thresholds.

South America remains the primary feedstock hub. Chile's National Lithium Strategy invites private participation while safeguarding state oversight, and new geological surveys lifted estimated reserves by 28%. Argentina attracted Rio Tinto's USD 2.5 billion mine investment and multiple OEM offtakes. Brazil saw EV sales jump 85% in 2024, led by BYD with 70% share, hinting at future domestic hydroxide conversion requirements.

Europe accelerates capacity with stringent CO2 regulations and comprehensive recycling mandates. Germany spearheads R&D on next-generation cathodes, while the EU Battery Regulation sets minimum lithium recovery quotas from 2025 onward. Several greenfield conversion plants in Finland, France, and Portugal are scheduled for commissioning by 2027, adding diversity to the lithium hydroxide market supply base. The bloc's push for strategic autonomy may reshape trade flows, especially if China enacts proposed technology export restrictions.

- Albemarle Corporation

- Arcadium Lithium

- Chengxin Lithium

- Ganfeng Lithium Group Co. Ltd.

- IGO Limited

- LevertonHELM Limited

- Nemaska Lithium (Investissement Quebec)

- Piedmont Lithium Inc.

- Shandong Ruifu Lithium Co., Ltd.

- Sinomine Resource Group

- SQM S.A.

- Tianqi Lithium Corporation

- Yahua Industrial Group Co.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Demand for Electric Vehicles

- 4.2.2 Increasing Demand for Power Tools

- 4.2.3 Commercialisation of Direct Lithium Extraction (DLE) Unlocking Low-Cost Hydroxide Feedstock

- 4.2.4 OEM-Backed Long-Term Contracts De-Risking New Hydroxide Capacity in Latin America

- 4.2.5 Government Policies Supporting Battery Supply Chains

- 4.3 Market Restraints

- 4.3.1 High Production Costs

- 4.3.2 Feedstock Price Volatility Hindering Project Financing

- 4.3.3 Rising concern About the Toxicity

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Volume and Value)

- 5.1 By Application

- 5.1.1 Lithium-ion Batteries

- 5.1.2 Lubricating Greases

- 5.1.3 Purification

- 5.1.4 Other Application (Polymer and Specialty Chemical Synthesis)

- 5.2 By End-use Industry

- 5.2.1 Automotive

- 5.2.2 Consumer Electronics

- 5.2.3 Energy Storage Systems

- 5.2.4 Others (Industrial and Off-Road Machinery)

- 5.3 By Grade

- 5.3.1 Battery Grade (Greater than or equal to 56.5% LiOH*H2O)

- 5.3.2 Technical Grade

- 5.3.3 Industrial Grade

- 5.4 By Form

- 5.4.1 Monohydrate

- 5.4.2 Anhydrous

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 Japan

- 5.5.1.3 South Korea

- 5.5.1.4 India

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Nordics

- 5.5.3.7 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Chile

- 5.5.4.4 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Albemarle Corporation

- 6.4.2 Arcadium Lithium

- 6.4.3 Chengxin Lithium

- 6.4.4 Ganfeng Lithium Group Co. Ltd.

- 6.4.5 IGO Limited

- 6.4.6 LevertonHELM Limited

- 6.4.7 Nemaska Lithium (Investissement Quebec)

- 6.4.8 Piedmont Lithium Inc.

- 6.4.9 Shandong Ruifu Lithium Co., Ltd.

- 6.4.10 Sinomine Resource Group

- 6.4.11 SQM S.A.

- 6.4.12 Tianqi Lithium Corporation

- 6.4.13 Yahua Industrial Group Co.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Rising Demand for Portable Electronic Devices