|

市場調查報告書

商品編碼

1851878

揮發性有機化合物(VOC)氣體感測器:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)Volatile Organic Compound Gas Sensor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

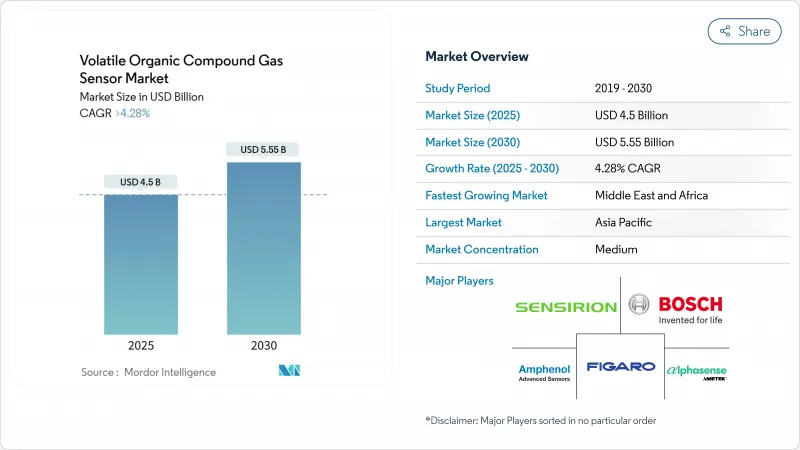

VOC感測器市場預計到2025年將達到45億美元,到2030年將達到55.5億美元,複合年成長率為4.28%。

隨著室內空氣品質法規收緊揮發性有機化合物(VOC)的允許暴露限值,商業建築紛紛安裝連續監測設備,市場需求也隨之增強。智慧家庭中心供應商將VOC檢測功能與高級產品捆綁銷售,以凸顯其差異化優勢;汽車製造商和電池製造商則依賴快速反應感測器來檢測電動車生產線中的溶劑洩漏。低功耗電子機械系統光電離檢測器使得工業人員能夠佩戴徽章式設備,而綠色建築認證也為即時空氣品質報告提供加分。這些趨勢共同推動了全球VOC感測器市場的成長。

全球揮發性有機化合物(VOC)氣體感測器市場趨勢及洞察

北美和歐洲正在收緊室內空氣品質標準

建築物業主必須證明其持續遵守日益嚴格的甲醛、苯和其他揮發性有機化合物(VOC)暴露法規。大規模採購固定式壁掛式檢測器和BACnet閘道器,有助於醫院、學校、交通樞紐等場所快速維修。市場需求主要集中在符合ASHRAE-62.1和EN-16798標準的計劃中,這將推動VOC感測器市場在短期內保持成長勢頭。

將VOC感測器整合到智慧家居物聯網平台

語音助理中心和智慧溫控器正將VOC(揮發性有機化合物)檢測定位為一項健康功能。功耗低於20mW的MOS晶片透過I2C或BLE介面整合,而Matter 1.2互通性則實現了與供應商無關的配對。高出貨量將擴大潛在用戶群並降低單價,從而維持VOC感測器市場的中期成長。

高濕度環境下PID感測器的校準漂移

在相對濕度高於 85% 的環境中,水分子會抑制光電離,這可能導致 PID 輸出降低 15%。使用者需要承擔補償演算法和頻繁重新校準的額外成本,這限制了其在東南亞和南美洲一些食品加工廠和紙漿廠的短期應用。

細分市場分析

MOS元件憑藉其優異的性價比,將在2024年佔據最大的VOC感測器市場佔有率,達到26%的銷售額。光電離檢測器)到2030年將維持8.2%的複合年成長率,超過VOC感測器市場的整體成長速度。高階工業用戶需要反應時間小於3秒且化學成分檢測範圍廣的感測器,這推動了PID模組VOC感測器市場規模的成長。未來的MOS藍圖將採用多像素陣列來實現物種選擇性,而PID供應商正在探索石墨烯視窗技術以實現亞ppm級的靈敏度。

即使晶圓成本下降和溫度調製演算法推動了PID和石英微天平設計等細分應用的發展,MOS元件整體市場佔有率仍將保持現有水準。參與企業必須克服涵蓋加熱器驅動模式的叢集智慧財產權,這構成了VOC感測器市場的一大障礙。

到2024年,壁掛式面板將佔總收入的41.5%,並將繼續作為依賴PoE供電的建築自動化維修的核心。穿戴式徽章的複合年成長率將達到9.6%,成為成長最快的產品,反映出監管機構對數位日誌中個人暴露資料的重視。隨著MEMS-PID設計實現8小時的電池續航時間,徽章相關VOC感測器的市場規模將穩定成長。

可攜式手持檢測器對緊急應變人員仍然有用,但其市場佔有率正被支援合規性文件的連續式固定監測器蠶食。多參數室內空氣品質監測儀仍然是揮發性有機化合物(VOC)感測器市場的重要組成部分,儘管它們面臨來自智慧恆溫器廠商的競爭,這些廠商將各個感測器直接整合到主機板子卡上。

區域分析

亞太地區預計到2024年將佔全球銷售額的31.9%,主要得益於中國、日本和韓國的超級工廠以及正極活性材料產能的擴張。 PID感測器與邊緣分析設備相結合,能夠滿足快速合規性審核的需求,並可向當地環保部門即時提供數據看板。對電池和半導體供應鏈的投資使亞太地區成為VOC感測器市場最重要的區域。

北美正受益於聯邦稅額扣抵抵免資助的建築維修週期,該抵免補貼了整合 VOC 監測的高效 HVAC 系統;企業園區正在使用 LoRaWAN IAQ 節點來追蹤職場的健康狀況;加拿大綠色建築委員會正在為持續報告授予 LEED 積分,從而加強了 VOC 感測器市場。

歐盟生態設計指令鼓勵製造商揭露產品在使用過程中的揮發性有機化合物(VOC)效能。在德國的汽車噴漆車間,固定監測器將丙酮蒸氣控制在10ppm以下。中東和非洲地區的複合年成長率(CAGR)最高,達9.2%。沙烏地阿拉伯和阿拉伯聯合大公國的智慧城市試點計畫在市政指揮中心引入了室內空氣品質(IAQ)儀表板,南非的礦山試點計畫則為井下工人佩戴穿戴式徽章,這些舉措都推動了該地區VOC感測器市場的擴張。

南美洲正經歷穩定成長。巴西已將其國家暴露限值與美國政府工業衛生學家協會(ACGIH)標準表接軌,從而促進了其位於聖保羅附近石化聯合體的採購。墨西哥的加工出口走廊正在增加低成本的金屬氧化物半導體(MOS)感測器,以符合美墨加協定(USMCA)的環境條款,從而推動了該地區揮發性有機化合物(VOC)感測器市場的發展。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 北美和歐洲的室內空氣品質標準日益嚴格

- 將VOC感測器整合到智慧家居物聯網平台

- 亞洲電動車電池生產線對溶劑外洩檢測的需求

- 低功耗MEMS-PID感測器可協助實現穿戴式VOC徽章

- 綠建築認證系統要求持續監測揮發性有機化合物(VOC)。

- 市場限制

- 高濕度環境下PID感測器校準漂移

- 感測器品牌之間缺乏統一的互通性通訊協定

- 智慧家庭市場細分領域的價格敏感性

- 半導體感測器材料供應鏈的波動

- 價值/供應鏈分析

- 監管和技術展望

- 波特五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 透過感測器技術

- 光電離檢測器(PID)

- 金屬氧化物半導體(MOS)

- 電化學感測器

- 光纖感測器

- 石英晶體共振器(QCM)

- 其他

- 按設備外形規格

- 固定式/壁掛式顯示器

- 手持式/可攜式檢測器

- 穿戴式徽章

- 整合式多參數室內空氣品質監測儀

- 嵌入式感測器模組

- 連結性別

- 有線(BACnet、Modbus、乙太網路、CAN)

- 無線的

- Wi-Fi

- Bluetooth/ BLE

- Zigbee/ Thread

- LoRaWAN/ NB-IoT/LTE-M

- 按最終用途行業分類

- 工業製程安全

- 石油天然氣和石化

- 汽車/運輸設備

- 家用電器和智慧家居

- 商業大樓和辦公大樓

- 醫療保健和製藥

- 食品和飲料製造

- 學術和研發實驗室

- 其他

- 透過檢測範圍

- 低於1ppm

- 1~10 ppm

- 10-100 ppm

- 100ppm 或更高

- 透過分銷管道

- 直銷

- 分銷商/加值經銷商通路

- 電子商務

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 亞太其他地區

- 中東

- 以色列

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 埃及

- 其他非洲地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- ABB Ltd.

- Alphasense Ltd.

- Aeroqual Limited

- Ion Science Ltd.

- EcoSensors Inc.

- SGX Sensortech Ltd.

- Renesas Electronics Corp.

- Sensirion AG

- Amphenol Advanced Sensors

- Figaro Engineering Inc.

- Bosch Sensortec GmbH

- AMS OSRAM AG

- City Technology(Honeywell Intl.)

- GfG Europe Ltd.

- MicroJet Technology Co., Ltd.

- Riken Keiki Co., Ltd.

- Dragerwerk AG and Co. KGaA

- Kaiterra

- Siemens AG

- Spec Sensors LLC

- NevadaNano Inc.

- Zhengzhou Winsen Electronics Tech. Co., Ltd.

第7章 市場機會與未來展望

The VOC sensors market stands at USD 4.5 billion in 2025 and is projected to reach USD 5.55 billion by 2030, reflecting a 4.28% CAGR.

Demand strengthens as indoor-air-quality codes narrow permissible volatile-organic-compound exposure limits, prompting commercial buildings to install continuous monitors. Smart-home hub vendors bundle VOC detection to distinguish premium offerings, while automotive and battery manufacturers rely on rapid-response sensors to detect solvent leakage on electric-vehicle production lines. Low-power micro-electromechanical-system photoionization detectors allow badge-style wearables for industrial staff, and green-building certifications award points for real-time air-quality reporting. These converging trends anchor growth across the VOC sensors market worldwide.

Global Volatile Organic Compound Gas Sensor Market Trends and Insights

Stricter Indoor-Air-Quality Standards across North America & Europe

Building owners must demonstrate continuous compliance with tightened exposure limits for formaldehyde, benzene and other VOCs. Bulk procurement of fixed wall-mounted detectors and BACnet gateways supports rapid retrofits in hospitals, schools and transit hubs. Demand concentrates on projects governed by ASHRAE-62.1 and EN-16798 guidelines, anchoring short-term momentum for the VOC sensors market.

Integration of VOC Sensors into Smart-Home IoT Platforms

Voice-assistant hubs and connected thermostats position VOC sensing as a wellness feature. MOS chips drawing less than 20 mW integrate over I2C or BLE, while Matter 1.2 interoperability enables vendor-agnostic pairing. High shipment volumes widen the addressable base and lower unit prices, sustaining medium-term growth for the VOC sensors market.

Calibration Drift of PID Sensors in High-Humidity Climates

PID output can drop 15% in environments above 85% relative humidity as water molecules quench photoionisation. Users incur added costs for compensation algorithms and frequent recalibration, tempering near-term uptake in food-processing plants and pulp mills across Southeast Asia and parts of South America.

Other drivers and restraints analyzed in the detailed report include:

- Demand from EV Battery Manufacturing Lines in Asia

- Adoption of Low-Power MEMS-PID Sensors Enabling Wearable Badges

- Lack of Harmonised Interoperability Protocols among Sensor Brands

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

MOS devices generated 26% of revenue in 2024, holding the largest VOC sensors market share because they balance price and performance. Photoionization detectors will post an 8.2% CAGR through 2030, outpacing the overall VOC sensors market. Premium industrial users require sub-3-second response times and wide chemical coverage, driving the VOC sensors market size for PID modules upward. Future MOS roadmaps incorporate multi-pixel arrays for species selectivity, while PID vendors explore graphene windows to reach sub-ppm sensitivity.

Across the MOS segment, falling wafer costs and temperature-modulation algorithms safeguard incumbent share even as niche applications shift to PID or quartz-crystal microbalance designs. Entrants must navigate intellectual-property clusters covering heater-drive patterns, which raise barriers in the VOC sensors market.

Wall-mounted panels captured 41.5% of 2024 revenue and remain core to building-automation retrofits that rely on PoE cabling. Wearable badges post the highest 9.6% CAGR, reflecting regulatory emphasis on personal exposure data in digital logbooks. The VOC sensors market size tied to badges climbs steadily as MEMS-PID designs prove eight-hour battery life.

Portable handheld detectors retain relevance for first responders but cede volume to continuous fixed monitors that support compliance documentation. Multi-parameter IAQ cubes face competition from smart-thermostat OEMs that integrate individual sensors directly onto motherboard daughtercards, yet they still contribute meaningfully to the VOC sensors market.

The Volatile Organic Compound Gas Sensor Market Report is Segmented by Sensor Technology (Photoionization Detector, Optical, and More), Device Form Factor (Wearable Badges, and More), Connectivity (Wired, Wireless), End-Use Industry (Industrial Safety, and More), Detection Range (Less Than 1 Ppm, and More), Distribution Channel (Direct Sales, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific contributed 31.9% of 2024 turnover, supported by gigafactory and cathode-active-material capacity expansions in China, Japan and South Korea. PID sensors pair with edge-analytics boxes to meet rapid compliance audits that require real-time dashboards delivered to provincial environmental bureaus. Investments in battery and semiconductor supply chains position Asia-Pacific as the foremost region within the VOC sensors market.

North America benefits from a building-retrofit cycle funded by federal tax credits that subsidize high-efficiency HVAC systems integrating VOC monitoring. Enterprise campuses use LoRaWAN IAQ nodes to track workplace wellness, and Canada's green-building council awards LEED points for continuous reporting, reinforcing the VOC sensors market.

Europe's Ecodesign directive pushes manufacturers to disclose VOC performance in use. Fixed monitors maintain acetone vapors below 10 ppm in German automotive paint shops. The Middle East and Africa post the quickest 9.2% CAGR as smart-city pilots in Saudi Arabia and the United Arab Emirates embed IAQ dashboards into municipal command centers, and South African mines trial wearable badges for underground crews, enlarging the regional VOC sensors market.

South America experiences steadier growth. Brazil aligns national exposure limits with ACGIH tables, driving procurement by petrochemical complexes near Sao Paulo. Mexico's maquiladora corridor adds low-cost MOS sensors to comply with USMCA environmental clauses, supporting the VOC sensors market across the region.

- ABB Ltd.

- Alphasense Ltd.

- Aeroqual Limited

- Ion Science Ltd.

- EcoSensors Inc.

- SGX Sensortech Ltd.

- Renesas Electronics Corp.

- Sensirion AG

- Amphenol Advanced Sensors

- Figaro Engineering Inc.

- Bosch Sensortec GmbH

- AMS OSRAM AG

- City Technology (Honeywell Intl.)

- GfG Europe Ltd.

- MicroJet Technology Co., Ltd.

- Riken Keiki Co., Ltd.

- Dragerwerk AG and Co. KGaA

- Kaiterra

- Siemens AG

- Spec Sensors LLC

- NevadaNano Inc.

- Zhengzhou Winsen Electronics Tech. Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Tightening Indoor Air-Quality Standards across North America and Europe

- 4.2.2 Integration of VOC Sensors into Smart-Home IoT Platforms

- 4.2.3 Demand from EV Battery Manufacturing Lines in Asia for Solvent-Leak Detection

- 4.2.4 Adoption of Low-Power MEMS-PID Sensors Enabling Wearable VOC Badges

- 4.2.5 Green-Building Certification Schemes Mandating Continuous VOC Monitoring

- 4.3 Market Restraints

- 4.3.1 Calibration Drift of PID Sensors in High-Humidity Climates

- 4.3.2 Lack of Harmonised Interoperability Protocols among Sensor Brands

- 4.3.3 Price Sensitivity in Mass-Market Smart-Home Segment

- 4.3.4 Supply-Chain Volatility for Semiconductor Sensor Materials

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory or Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Sensor Technology

- 5.1.1 Photoionization Detector (PID)

- 5.1.2 Metal Oxide Semiconductor (MOS)

- 5.1.3 Electrochemical Sensor

- 5.1.4 Optical Fiber Sensor

- 5.1.5 Quartz Crystal Microbalance (QCM)

- 5.1.6 Others

- 5.2 By Device Form Factor

- 5.2.1 Fixed/Wall-Mounted Monitors

- 5.2.2 Handheld/Portable Detectors

- 5.2.3 Wearable Badges

- 5.2.4 Integrated Multi-Parameter IAQ Monitors

- 5.2.5 Embedded Sensor Modules

- 5.3 By Connectivity

- 5.3.1 Wired (BACnet, Modbus, Ethernet, CAN)

- 5.3.2 Wireless

- 5.3.2.1 Wi-Fi

- 5.3.2.2 Bluetooth/BLE

- 5.3.2.3 Zigbee/Thread

- 5.3.2.4 LoRaWAN/NB-IoT/LTE-M

- 5.4 By End-use Industry

- 5.4.1 Industrial Process Safety

- 5.4.2 Oil and Gas and Petrochemical

- 5.4.3 Automotive and Transportation

- 5.4.4 Consumer Electronics and Smart Homes

- 5.4.5 Commercial Buildings and Offices

- 5.4.6 Healthcare and Pharmaceuticals

- 5.4.7 Food and Beverage Production

- 5.4.8 Academic and RandD Laboratories

- 5.4.9 Others

- 5.5 By Detection Range

- 5.5.1 Less than 1 ppm

- 5.5.2 1 - 10 ppm

- 5.5.3 10 - 100 ppm

- 5.5.4 Greater than 100 ppm

- 5.6 By Distribution Channel

- 5.6.1 Direct Sales

- 5.6.2 Distributor / VAR Channel

- 5.6.3 E-commerce

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 United Kingdom

- 5.7.2.2 Germany

- 5.7.2.3 France

- 5.7.2.4 Italy

- 5.7.2.5 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 Japan

- 5.7.3.3 India

- 5.7.3.4 South Korea

- 5.7.3.5 Rest of Asia-Pacific

- 5.7.4 Middle East

- 5.7.4.1 Israel

- 5.7.4.2 Saudi Arabia

- 5.7.4.3 United Arab Emirates

- 5.7.4.4 Turkey

- 5.7.4.5 Rest of Middle East

- 5.7.5 Africa

- 5.7.5.1 South Africa

- 5.7.5.2 Egypt

- 5.7.5.3 Rest of Africa

- 5.7.6 South America

- 5.7.6.1 Brazil

- 5.7.6.2 Argentina

- 5.7.6.3 Rest of South America

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 ABB Ltd.

- 6.4.2 Alphasense Ltd.

- 6.4.3 Aeroqual Limited

- 6.4.4 Ion Science Ltd.

- 6.4.5 EcoSensors Inc.

- 6.4.6 SGX Sensortech Ltd.

- 6.4.7 Renesas Electronics Corp.

- 6.4.8 Sensirion AG

- 6.4.9 Amphenol Advanced Sensors

- 6.4.10 Figaro Engineering Inc.

- 6.4.11 Bosch Sensortec GmbH

- 6.4.12 AMS OSRAM AG

- 6.4.13 City Technology (Honeywell Intl.)

- 6.4.14 GfG Europe Ltd.

- 6.4.15 MicroJet Technology Co., Ltd.

- 6.4.16 Riken Keiki Co., Ltd.

- 6.4.17 Dragerwerk AG and Co. KGaA

- 6.4.18 Kaiterra

- 6.4.19 Siemens AG

- 6.4.20 Spec Sensors LLC

- 6.4.21 NevadaNano Inc.

- 6.4.22 Zhengzhou Winsen Electronics Tech. Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment