|

市場調查報告書

商品編碼

1851825

機器人領域的人工智慧:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)Artificial Intelligence In Robotics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

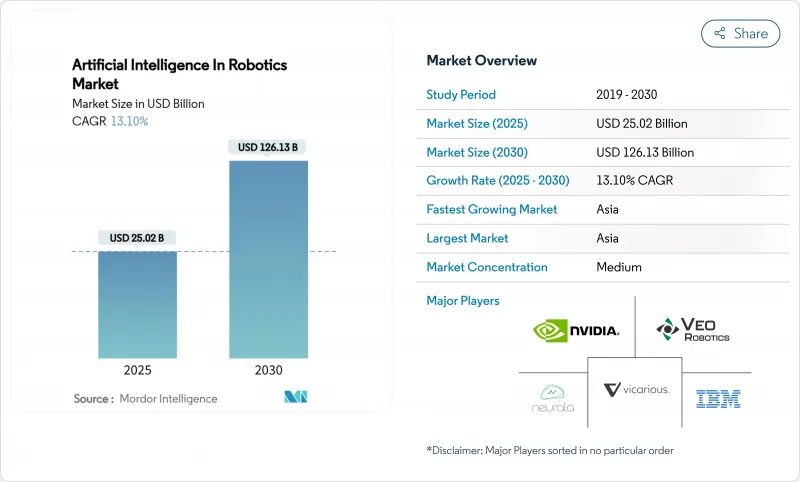

預計到 2025 年,機器人人工智慧市場規模將達到 250.2 億美元,到 2030 年將達到 1,261.3 億美元,預測期(2025-2030 年)複合年成長率為 13.10%。

這一發展勢頭得益於邊緣運算、機器學習演算法和高解析度感測器的快速進步,這些技術使機器人能夠在毫秒內解讀周圍環境並自主行動。製造業正從純粹的機械升級轉向以智慧為中心的改進,引入客製化的人工智慧處理器模組,以減少生產線和服務環境中的決策延遲。亞洲製造業的投資、北美電子商務的蓬勃發展以及歐洲的合作研究項目正在匯聚,從而拓展部署場景並加速價值實現。儘管硬體仍然是重要的成本促進因素,但軟體採用率的不斷提高表明,價值創造正在轉向感知、推理和自適應控制堆疊,使機器人成為互聯工廠和物流系統中持續學習的資產。這些趨勢的綜合作用正在催生一個日益龐大的智慧機器用戶群,這些機器是對人類操作員的補充而非取代,從而擴大了機器人人工智慧市場的潛在需求。

全球機器人人工智慧市場趨勢與洞察

整合邊緣人工智慧晶片以實現機器人即時決策

邊緣AI處理器將決策延遲從秒級縮短至毫秒級,使自主移動機器人(AMR)無需依賴雲端即可在動態生產車間中導航。研華科技在2025年的產品展示中,將NVIDIA Jetson Thor模組整合到其AMR叢集後,響應速度提升了75%。深圳和水原的電子產品製造商報告稱,由於視覺和運動數據在本地進行處理,一次產量比率和節拍時間均得到了顯著提升。更低的延遲也增強了預測性維護的回饋迴路,從而減少了精密組裝的非計劃性停機時間。隨著邊緣最佳化AI模型的日益成熟,處理器成本不斷下降,這促使中端供應商對現有機器人進行改造升級,而不是購買新設備。因此,這項驅動力將推動不同類型工廠更廣泛地採用邊緣AI技術,從而積極促進機器人AI市場的發展。

人口快速老化將推動對老年護理機器人的需求。

由Panasonic、Softbank Corporation和日本政府支持的新興企業正在部署行動社交陪伴機器人,這些機器人利用深度神經網路來偵測跌倒、提醒服藥時間並進行自然對話。臨床試驗表明,這些機器人透過重新分配重複性的搬運和監測任務來提高醫護人員的工作效率,使護理人員能夠專注於與病人的直接互動。面臨類似的人口結構挑戰,韓國正透過其「2030年機器人產業願景」計畫投資人工智慧機器人護理員,為醫院和家庭護理試驗的部署津貼。這兩個文化上的先驅的成功為歐洲的醫療保健提供者樹立了標桿,歐洲人口老化加劇,未來機器人市場對人工智慧的需求也將不斷成長。

針對特定機器人感知任務的高品質領域數據匱乏

《機器人與人工智慧前沿》指出,不一致和不完整的資料集導致人機協作的可靠性降低。例如,農業收割機難以準確判斷不同作物的成熟度,限制了其在試點農場以外的商業性部署。資料缺失也阻礙了安全檢驗,迫使供應商過度設計感知系統,延長了產品上市時間。專有資料集為大型企業建構了競爭優勢,使小型創新者難以達到效能基準。雖然合成資料生成和遷移學習正在緩解這一障礙,但資料短缺仍然阻礙著人工智慧在機器人市場的整體發展。

細分市場分析

到2024年,硬體將佔機器人人工智慧市場佔有率的62%,這主要體現在賦予機器人物理形態的感測器、致動器、驅動裝置和結構框架等方面。配備內置力感測器的資本密集型工業機械手臂仍然是焊接、噴漆和精密物料輸送等作業的必備設備。供應商目前正在推出模組化設計,用戶無需對整個系統進行全面改造即可更換夾爪、攝影機和人工智慧邊緣模組,從而降低整體擁有成本並延長設備使用壽命。硬體藍圖強調節能伺服控制器和輕質複合材料關節,以實現更高的承重能力重量比,這對於在狹窄工廠通道中穿梭的機器人至關重要。

機器學習和深度學習軟體正以24%的複合年成長率快速成長,並且通常以預訓練感知和運動規劃庫的形式捆綁銷售。這些技術堆疊無需外部編程即可實現缺陷檢測、預測性維護和自適應抓取,從而從現有設備中挖掘更多價值。早期用戶報告稱,僅軟體升級就能使整體設備效率提升兩位數,這表明儘管基準較小,軟體的成長速度仍然超過了硬體投入。隨著客戶對生命週期支援的需求不斷成長,涵蓋整合、遠端監控和持續模型重訓練等服務正在為供應商創造不斷成長的收益。這種轉變清晰地表明,在人工智慧機器人市場中,真正區分競爭者的是智慧,而非機械。

到2024年,工業機器人將佔據機器人人工智慧市場規模的68%,這主要得益於汽車和電子產品生產中應用的多關節臂。全球工廠中機器人的裝置量已超過428萬台,並以每年10%的速度成長,凸顯了市場對機器人的強勁需求。人工智慧升級使這些系統能夠處理各種幾何形狀的零件,無需停機重新示教,從而提高了資產利用率。雖然協作機器人目前出貨量仍佔少數,但隨著靈活自動化在多品種、小批量生產環境中變得至關重要,它們正經歷顯著成長。

醫療和保健機器人是成長最快的類別,2025年至2030年的複合年成長率將達到26%。融合電腦視覺和力回饋技術的手術系統可輔助臨床醫師進行微創手術,從而減少術後併發症和縮短住院時間。醫院物流機器人利用同步定位與地圖建構(SLAM)技術,結合人工智慧決策引擎,可在擁擠的走廊中自主運送床單和藥品。消費者對機器人的接受度也不斷提高,例如,居家照護機器人可以幫助老年人完成日常生活任務。總而言之,這些趨勢將透過多元化收入來源和緩解以汽車為中心的需求週期性波動,使機器人人工智慧市場受益。

機器人人工智慧市場按組件(硬體、其他)、機器人類型(工業機器人、服務機器人、其他)、應用(製造和組裝、物流和倉儲、醫療保健和手術、其他)、最終用戶行業(汽車、電子、半導體、其他)和地區進行細分。

區域分析

亞太地區預計到2024年將佔全球銷售額的47%,這主要得益於中國、日本和韓國的大規模自動化項目。光是中國一國,2023年就將安裝276,288台工業機器人,佔全球出貨量的51%。這得歸功於地方政府提供稅收優惠和低利率貸款,以提升製造業競爭力。韓國電子公司正在將邊緣人工智慧視覺技術應用於貼片單元,以將晶圓級公差控制在微米級;而日本汽車製造商則正在部署人工智慧協作機器人,用於需要類似人類靈巧度的最終修整任務。該地區預計18%的複合年成長率不僅反映了其製造業的主導地位,也反映了醫療保健和服務機器人試點計畫的快速發展。

北美排名第二,這主要得益於蓬勃發展的新興企業和資金籌措,尤其是在美國,人工智慧軟體領域的專業知識十分豐富。一家物流巨頭正在對現有的輸送機系統維修,引入人工智慧移動機器人,以實現兩小時內送達的目標。汽車製造商正在利用人工智慧監控新型輕質材料的焊接質量,並隨著工廠適應電池式電動車的生產,加速這些材料的應用。加拿大的採礦業正在試驗使用自動駕駛卡車,這些卡車利用人工智慧感知系統在低GPS訊號環境的露天礦場中導航,從而將人工智慧機器人的應用範圍擴展到工廠之外。墨西哥的工業園區也積極進行人工智慧維修,以保持競爭力,並符合美墨加協定(USMCA)的內容規則。

歐洲對符合倫理、安全可靠且值得信賴的人工智慧的重視,正在重塑技術發展和法律規範。德國在機器人密度方面處於領先地位,預計2023年將新增28,355台機器人。 「地平線歐洲」津貼鼓勵在農業技術、醫療保健和綠色製造領域建立機器人-學術叢集。然而,對CE認證和人工智慧責任的不同解讀減緩了跨境部署,尤其是協作機器人的部署。中歐和東歐仍然是一個充滿潛力的成長區域,勞動力短缺推動了工廠投資。雖然南美、中東和非洲等規模較小的市場仍在發展中,但它們正受益於承包和機器人即服務契約,這些合約降低了前期投資門檻,有助於推動全球機器人人工智慧市場的擴張。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 將邊緣人工智慧晶片整合到亞洲電子製造業中,以實現即時機器人決策

- 人口快速老化將推動日本和韓國對老年護理機器人的需求。

- 歐盟「地平線」計畫的歐洲資助簡化了人工智慧機器人合作研究聯盟的運作。

- 電子商務物流的履約發展推動北美人工智慧倉庫自動化

- 自主移動機器人在德國汽車組裝線上迅速普及

- 隨著視覺感測器成本的下降,用於改造傳統機器人的 AI套件在全球範圍內對中小企業越來越受歡迎。

- 市場限制

- 針對特定機器人感知任務的高品質領域數據匱乏

- 分散的安全標準阻礙了協作機器人跨國應用

- 食品加工業者使用的AI處理器模組初始成本高,利潤率低。

- 網實整合安全問題限制了醫院中雲端連線服務機器人的應用。

- 市場促進因素

- 價值/供應鏈分析

- 監理與標準展望

- 技術展望

- 波特五力模型

- 供應商的議價能力

- 買方/消費者的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 投資分析

第5章 市場規模與成長預測

- 按組件

- 硬體

- 感應器

- 致動器

- 電力系統

- 控制系統

- 軟體

- 機器學習和深度學習

- 電腦視覺

- 自然語言處理

- 情境感知/決策

- 服務

- 整合與部署

- 支援與維護

- 硬體

- 按機器人類型

- 工業機器人

- 關節機器人

- SCARA機器人

- 笛卡兒機器人

- 協作機器人(Cobots)

- 服務機器人

- 專業服務機器人

- 物流機器人

- 醫療和保健機器人

- 國防與安全機器人

- 田間機器人(農業和採礦)

- 個人/家用機器人

- 家用機器人

- 娛樂和陪伴機器人

- 工業機器人

- 透過使用

- 製造和組裝

- 物流/倉儲

- 醫療保健和外科手術

- 零售與電子商務業務

- 食品和飲料加工

- 檢查和維護

- 其他用途

- 按最終用戶行業分類

- 車

- 電子和半導體

- 零售與電子商務

- 衛生保健

- 飲食

- 航太/國防

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐國家

- 其他歐洲地區

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 埃及

- 其他非洲地區

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- ASEAN

- 亞太其他地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- NVIDIA Corporation

- IBM Corporation

- Microsoft Corporation

- ABB Ltd.

- FANUC Corporation

- KUKA AG

- Yaskawa Electric Corp.

- Universal Robots A/S

- Hanson Robotics Ltd.

- Boston Dynamics, Inc.

- Brain Corporation

- Vicarious AI

- Neurala, Inc.

- Kindred AI

- Preferred Networks, Inc.

- Veo Robotics, Inc.

- Fetch Robotics, Inc.

- Blue River Technology(John Deere)

- UiPath Inc.

- SoftBank Robotics Group Corp.

第7章 市場機會與未來展望

The Artificial Intelligence In Robotics Market size is estimated at USD 25.02 billion in 2025, and is expected to reach USD 126.13 billion by 2030, at a CAGR of 13.10% during the forecast period (2025-2030).

Momentum is underpinned by rapid advances in edge computing, machine learning algorithms, and high-resolution sensor suites that allow robots to interpret their surroundings and act autonomously in milliseconds. Manufacturers are shifting from purely mechanical upgrades to intelligence-centric improvements, embedding custom AI processor modules that shorten decision latency on production lines and in service environments. Asia's manufacturing investments, North America's e-commerce boom, and Europe's coordinated research programs are converging to expand deployment scenarios and accelerate time-to-value. Hardware remains a large cost driver, yet rising software attach rates illustrate how value creation is migrating toward perception, reasoning, and adaptive-control stacks, turning robots into continuously learning assets within connected factory and logistics ecosystems. The combined effect of these trends is creating an ever-larger installed base of intelligent machines that complement, rather than displace, human operators, widening addressable demand for the AI in robotics market.

Global Artificial Intelligence In Robotics Market Trends and Insights

Integration of Edge-AI Chips Enabling Real-Time Robot Decision-Making

Edge-AI processors cut decision-making latency from seconds to milliseconds, enabling autonomous mobile robots (AMR) to navigate dynamic production floors without cloud dependence. Advantech's 2025 showcase highlighted 75% faster response times after integrating NVIDIA Jetson Thor modules into AMR fleets. Electronics manufacturers in Shenzhen and Suwon report measurable gains in first-pass yield and takt-time reduction when vision and motion data are processed locally. Lower latency also tightens feedback loops for predictive maintenance, decreasing unscheduled downtime in precision assembly lines. As edge-optimized AI models mature, processor costs are falling, encouraging mid-tier suppliers to retrofit existing robots instead of purchasing new units. The driver, therefore, widens adoption across diverse factory footprints and contributes positively to the AI in robotics market .

Rapid Aging Population Accelerating Demand for Elder-Care Robots

Japan's share of residents aged 65 plus exceeded 29% in 2025, amplifying a projected shortfall of 377,000 caregivers.Panasonic, SoftBank, and startups backed by the Japanese government are rolling out mobility and social-companion robots that use deep neural networks to detect falls, remind medication schedules, and interact through natural speech. Clinical pilots show robots increase staff efficiency by reallocating repetitive lifting or monitoring tasks, letting nurses focus on direct patient engagement. South Korea faces similar demographic headwinds and is investing in AI robotic caregivers through its "Robot Industry Vision 2030" plan, which subsidizes hospital deployments and homecare trials. Success in these two cultural early adopters sets benchmarks for healthcare providers in Europe as their populations age, broadening future addressable demand for AI in the robotics market.

Scarcity of High-Quality Domain Data for Niche Robot-Perception Tasks

Frontiers in Robotics and AI highlights that inconsistent, incomplete datasets reduce the reliability of human-robot collaboration, especially where robots must recognize uncommon objects. For example, agricultural harvesters struggle to gauge ripeness across diverse crop varieties, limiting commercial deployment beyond pilot farms. Data gaps also impede safety validation, forcing vendors to over-engineer perception stacks and prolong time-to-market. Proprietary datasets give large incumbents a moat, making it harder for smaller innovators to match performance benchmarks. While synthetic data generation and transfer learning mitigate the barrier, the shortage remains a drag on the overall expansion of AI in the robotics market.

Other drivers and restraints analyzed in the detailed report include:

- EU Horizon Europe Funding Streamlining Collaborative AI-Robot Research

- E-Commerce Fulfilment Boom Driving AI-Enabled Warehouse Automation

- Fragmented Safety Standards Hindering Cross-Border Cobot Deployment

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware accounted for 62% of the AI in robotics market share in 2024, reflecting the sensors, actuators, drives, and structural frames that give robots their physical presence. Capital-intensive industrial arms with integrated force-torque sensors remain indispensable for welding, painting, and precision material handling. Vendors are now shipping modular designs that let manufacturers swap grippers, cameras, or AI edge modules without full system overhauls, lowering total cost of ownership and prolonging equipment life cycles. Hardware roadmaps emphasize power-efficient servo controllers and lightweight composite joints, enabling higher payload-to-weight ratios crucial for mobile robots in tight factory aisles.

Machine Learning & Deep Learning software is expanding at a 24% CAGR and is increasingly bundled as pre-trained perception and motion-planning libraries. These stacks extract more value from existing machines by enabling defect detection, predictive maintenance, and adaptive grasping without external programming. Early adopters report that software upgrades alone can raise overall equipment effectiveness by double digits, illustrating why software is outpacing physical spend despite its smaller baseline. Services covering integration, remote monitoring, and continuous model retraining form a rising annuity stream for vendors as customers seek lifecycle support. The shift underlines how intelligence rather than mechanics now differentiates competitors in the AI in robotics market.

Industrial robots commanded 68% of the AI in robotics market size in 2024, led by articulated arms deployed in automotive and electronics production. Their installed base surpassed 4.28 million units in factories worldwide, a 10% annual gain that highlights entrenched demand. AI upgrades are letting these systems handle variable part geometries without downtime for re-teaching, boosting asset utilization. Cobots, still a minority of shipments, enjoy outsized growth as flexible automation becomes essential for high-mix, low-volume environments.

Medical & healthcare robots represent the fastest-growing class at a 26% CAGR for 2025-2030. Surgical systems incorporating computer vision and force feedback assist clinicians in minimally invasive procedures, trimming post-operative complications and length of stay. Hospital logistics robots autonomously ferry linens and medications through crowded corridors using simultaneous localization and mapping (SLAM) fused with AI decision engines. Consumer acceptance is widening, evidenced by homecare robots that support daily living tasks for seniors. Altogether, these trends diversify revenue pools and mitigate cyclicality inherent in automotive-centric demand, benefiting the AI in robotics market.

The Artificial Intelligence in Robotics Market is Segmented by Component (Hardware and More), Robot Type (Industrial Robots, Service Robots and More), Application (Manufacturing and Assembly, Logistics and Warehousing, Healthcare and Surgery and More), End-User Industry (Automotive, Electronics, and Semiconductors, and More), and Geography.

Geography Analysis

Asia Pacific generated 47% of global revenue in 2024 driven by extensive automation programs in China, Japan, and South Korea. China alone installed 276,288 industrial robots in 2023, equal to 51% of world shipments, as local authorities provide tax incentives and low-interest loans to upgrade manufacturing competitiveness ifr.org. Korean electronics firms add edge-AI vision to pick-and-place cells to manage wafer-level tolerances measured in microns, while Japanese automakers deploy AI cobots for final trim operations that require human-like dexterity. The region's projected 18% CAGR reflects not only manufacturing dominance but also fast-emerging healthcare and service robotics pilots.

North America ranks second, anchored by the United States where AI software expertise seeds robust startup formation and venture funding. Logistics giants retrofit existing conveyor grids with AI mobile robots to meet two-hour delivery windows. Automakers accelerate adoption as factories retool for battery electric vehicles, using AI to monitor weld quality on new lightweight materials. Canada's mining sector pilots autonomous haulage trucks that leverage AI perception stacks to navigate open-pit sites in low-GPS conditions, extending AI in robotics market penetration beyond factory walls. Mexico's industrial corridors likewise embrace AI retrofits to stay competitive following USMCA content rules.

Europe emphasizes ethical, safe, and trustworthy AI, shaping both technology development and regulatory frameworks. Germany leads robot density with 28,355 new installations in 2023, aided by government subsidies for Mittelstand automation projects. Horizon Europe grants encourage academic-industry clusters in robotics for agri-tech, healthcare, and green manufacturing. Nonetheless, diverging interpretations of CE marking and AI liability delay cross-border deployments, particularly for cobots. Growth potential in Central and Eastern Europe remains high as labor shortages push factories to invest. Smaller markets in South America, the Middle East, and Africa are nascent but benefit from turnkey Robot-as-a-Service contracts that lower upfront capital barriers, nudging global uptake of the AI in robotics market.

- NVIDIA Corporation

- IBM Corporation

- Microsoft Corporation

- ABB Ltd.

- FANUC Corporation

- KUKA AG

- Yaskawa Electric Corp.

- Universal Robots A/S

- Hanson Robotics Ltd.

- Boston Dynamics, Inc.

- Brain Corporation

- Vicarious AI

- Neurala, Inc.

- Kindred AI

- Preferred Networks, Inc.

- Veo Robotics, Inc.

- Fetch Robotics, Inc.

- Blue River Technology (John Deere)

- UiPath Inc.

- SoftBank Robotics Group Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.1.1 Market Drivers

- 4.1.1.1 Integration of Edge-AI Chips Enabling Real-Time Robot Decision-Making in Asia-s Electronics Manufacturing

- 4.1.1.2 Rapid Aging Population Accelerating Demand for Elder-Care Robots in Japan and South Korea

- 4.1.1.3 EU Horizon Europe Funding Streamlining Collaborative AI-Robot Research Consortia

- 4.1.1.4 E-Commerce Fulfilment Boom Driving AI-Enabled Warehouse Automation in North America

- 4.1.1.5 Surge in Autonomous Mobile Robots within German Automotive Final Assembly Lines

- 4.1.1.6 Falling Vision-Sensor Costs Allowing SMB AI-Retrofit Kits for Legacy Robots Globally

- 4.1.2 Market Restraints

- 4.1.2.1 Scarcity of High-Quality Domain Data for Niche Robot-Perception Tasks

- 4.1.2.2 Fragmented Safety Standards Hindering Cross-Border Cobot Deployment

- 4.1.2.3 High Up-Front Cost of AI Processor Modules for Low-Margin Food Processors

- 4.1.2.4 Cyber-Physical Security Concerns Limiting Cloud-Connected Service Robots in Hospitals

- 4.1.1 Market Drivers

- 4.2 Value / Supply-Chain Analysis

- 4.3 Regulatory and Standards Outlook

- 4.4 Technological Outlook

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.1.1 Sensors

- 5.1.1.2 Actuators

- 5.1.1.3 Power Systems

- 5.1.1.4 Control Systems

- 5.1.2 Software

- 5.1.2.1 Machine Learning and Deep Learning

- 5.1.2.2 Computer Vision

- 5.1.2.3 Natural Language Processing

- 5.1.2.4 Context Awareness / Decision-Making

- 5.1.3 Services

- 5.1.3.1 Integration and Deployment

- 5.1.3.2 Support and Maintenance

- 5.1.1 Hardware

- 5.2 By Robot Type

- 5.2.1 Industrial Robots

- 5.2.1.1 Articulated Robots

- 5.2.1.2 SCARA Robots

- 5.2.1.3 Cartesian Robots

- 5.2.1.4 Collaborative Robots (Cobots)

- 5.2.2 Service Robots

- 5.2.2.1 Professional Service Robots

- 5.2.2.1.1 Logistics Robots

- 5.2.2.1.2 Medical and Healthcare Robots

- 5.2.2.1.3 Defense and Security Robots

- 5.2.2.1.4 Field Robots (Agriculture and Mining)

- 5.2.2.2 Personal and Domestic Robots

- 5.2.2.2.1 Household Robots

- 5.2.2.2.2 Entertainment and Companion Robots

- 5.2.1 Industrial Robots

- 5.3 By Application

- 5.3.1 Manufacturing and Assembly

- 5.3.2 Logistics and Warehousing

- 5.3.3 Healthcare and Surgery

- 5.3.4 Retail and E-Commerce Operations

- 5.3.5 Food and Beverage Processing

- 5.3.6 Inspection and Maintenance

- 5.3.7 Other Applications

- 5.4 By End-user Industry

- 5.4.1 Automotive

- 5.4.2 Electronics and Semiconductors

- 5.4.3 Retail and E-Commerce

- 5.4.4 Healthcare

- 5.4.5 Food and Beverage

- 5.4.6 Aerospace and Defense

- 5.4.7 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Nordics

- 5.5.3.7 Rest of Europe

- 5.5.4 Middle East

- 5.5.4.1 United Arab Emirates

- 5.5.4.2 Saudi Arabia

- 5.5.4.3 Turkey

- 5.5.4.4 Rest of Middle East

- 5.5.5 Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Nigeria

- 5.5.5.3 Egypt

- 5.5.5.4 Rest of Africa

- 5.5.6 Asia Pacific

- 5.5.6.1 China

- 5.5.6.2 Japan

- 5.5.6.3 South Korea

- 5.5.6.4 India

- 5.5.6.5 ASEAN

- 5.5.6.6 Rest of Asia Pacific

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products and Services, Recent Developments)}

- 6.4.1 NVIDIA Corporation

- 6.4.2 IBM Corporation

- 6.4.3 Microsoft Corporation

- 6.4.4 ABB Ltd.

- 6.4.5 FANUC Corporation

- 6.4.6 KUKA AG

- 6.4.7 Yaskawa Electric Corp.

- 6.4.8 Universal Robots A/S

- 6.4.9 Hanson Robotics Ltd.

- 6.4.10 Boston Dynamics, Inc.

- 6.4.11 Brain Corporation

- 6.4.12 Vicarious AI

- 6.4.13 Neurala, Inc.

- 6.4.14 Kindred AI

- 6.4.15 Preferred Networks, Inc.

- 6.4.16 Veo Robotics, Inc.

- 6.4.17 Fetch Robotics, Inc.

- 6.4.18 Blue River Technology (John Deere)

- 6.4.19 UiPath Inc.

- 6.4.20 SoftBank Robotics Group Corp.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

2034年機器人人工智慧市場預測:按組件、部署模式、機器人類型、技術、最終用戶和地區分類的全球分析

2034年機器人人工智慧市場預測:按組件、部署模式、機器人類型、技術、最終用戶和地區分類的全球分析 具身人工智慧(EAI)機器人資料產業佈局(2026 年)人工智慧機器人市場預測至2034年——全球機器人類型、技術、組件、應用、最終用戶和區域分析人工智慧機器人控制平台市場預測至2034年-全球分析(按組件、部署模式、機器人類型、技術、應用、最終用戶和地區分類)人工智慧機器人晶片市場預測至2034年——按晶片類型、組件、技術節點、應用、最終用戶和地區分類的全球分析具身人工智慧機器人(包括VLA)的大規模模型(2026)

具身人工智慧(EAI)機器人資料產業佈局(2026 年)人工智慧機器人市場預測至2034年——全球機器人類型、技術、組件、應用、最終用戶和區域分析人工智慧機器人控制平台市場預測至2034年-全球分析(按組件、部署模式、機器人類型、技術、應用、最終用戶和地區分類)人工智慧機器人晶片市場預測至2034年——按晶片類型、組件、技術節點、應用、最終用戶和地區分類的全球分析具身人工智慧機器人(包括VLA)的大規模模型(2026) 人工智慧機器人市場:按組件、技術、機器人類型、應用和最終用戶分類——2026-2032年全球市場預測

人工智慧機器人市場:按組件、技術、機器人類型、應用和最終用戶分類——2026-2032年全球市場預測 2026年全球個人人工智慧(AI)助理市場報告2026年機器人空間計算全球市場報告2026年機器人領域生成式人工智慧全球市場報告

2026年全球個人人工智慧(AI)助理市場報告2026年機器人空間計算全球市場報告2026年機器人領域生成式人工智慧全球市場報告