|

市場調查報告書

商品編碼

1940558

整合通訊與協作 (UC&C):市場佔有率分析、產業趨勢與統計、成長預測 (2026-2031)Unified Communications And Collaboration - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

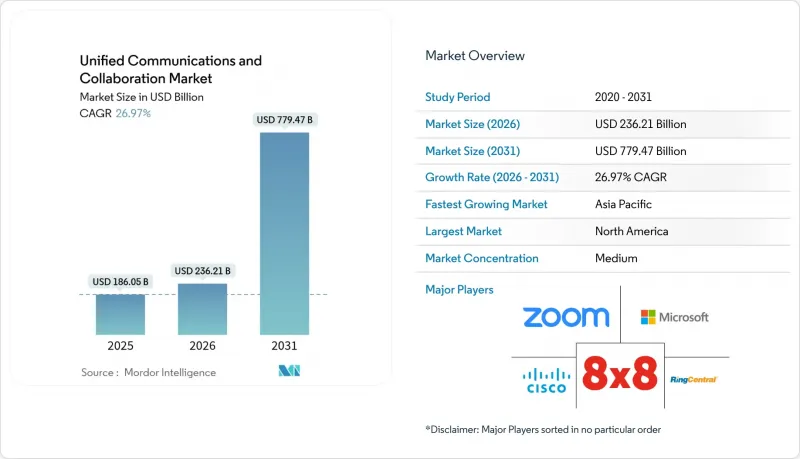

整合通訊與協作 (UC&C) 市場預計將從 2025 年的 1860.5 億美元成長到 2026 年的 2362.1 億美元,預計到 2031 年將達到 7794.7 億美元,2026 年至 2031 年的複合年成長率為 26.97%。

這項成長的驅動力來自於混合辦公模式的擴展、人工智慧增強的生產力提升,以及將分散式語音、視訊、通訊和工作流程應用整合到單一雲端環境中的需求。企業正持續將數位轉型預算重新分配給能夠提升分散式團隊員工參與度的溝通工具。微軟、思科和RingCentral等現有企業正透過橫向平台深度來捍衛市場佔有率,而以人工智慧為先導的挑戰者則瞄準了細分領域的工作流程空白。策略併購(例如RingCentral以6.5億美元收購Mitel,以及愛立信以62億美元收購Vonage)表明,供應商如何將整合通訊與客服中心功能和API能力相結合,從而擴大其目標市場。

全球整合通訊與協作 (UC&C) 市場趨勢與洞察

混合辦公需求加速了統一通訊即服務 (UCaaS) 的轉型

一些公司在將工作負載遷移到 Microsoft Teams Phone 後,取代了傳統的 PBX 系統,並報告維護成本降低,運作延長。例如,Florida Crystals 公司將通訊成本降低了 78%。加拿大中型企業採用率的上升也呈現類似的趨勢,證實了雲端統一通訊 (UC) 對地理位置分散的員工隊伍的有效性。將語音、視訊、聊天和工作流程應用程式捆綁在單一許可證下的供應商正在取代傳統的獨立解決方案,並提高客戶留存率。這種轉變給缺乏雲端規模的傳統電話供應商帶來了壓力,同時也為能夠快速執行全球部署的 UCaaS 專家帶來了收入成長。北美大規模的用戶基數意味著該地區仍然是新功能採用的標竿。

人工智慧增強的會議效率和自動化工具

微軟的人工智慧業務憑藉其整合到 Teams 會議、通話和訊息功能中的 Copilot 服務,在 2025 年第二季度實現了 130 億美元的年收入。同樣,RingCentral 也實現了其人工智慧接待員功能的商業化,客戶數量超過 1000 家,年經常性收入超過 5000 萬美元。即時轉錄、多語言翻譯和自動會議摘要功能正在推動統一通訊從被動連接到主動決策支援轉變。已實施人工智慧呼叫分流功能的醫療整合通訊報告稱,預約取消率降低,回應時間縮短,展現了切實的臨床成效。競爭的焦點正從功能數量轉向推理準確性和無縫工作流程整合。

嚴格的安全和合規要求減緩了採用速度。

醫療保健領域的 HIPAA、支付領域的 PCI-DSS 以及歐洲用戶資料的 GDPR 等法規要求額外的加密、審核和本地化層,從而延長了實施時間。 Smash 於 2025 年 2 月收購了 Call Cabinet,並將人工智慧驅動的通話錄音和分析功能整合到其歸檔平台中,從而加強了其合規性。金融公司必須記錄所有形式的通訊,包括音訊、影片和聊天記錄,以符合 MiFID II 的要求,這推動了對嚴格的供應商實質審查和專業合規解決方案的需求。未獲得端到端認證的供應商可能面臨被排除在受監管的競標的風險,從而限制其商機。

細分市場分析

2025年,雲端服務將佔總支出的66.18%,維持28.55%的複合年成長率,成為整合通訊與協作(UC&C)市場的核心。隨著企業逐步淘汰老舊的PBX硬體,雲端部署的UC&C市場規模預計將快速成長。供應商不斷推動先進的整合通訊技術、自主雲端選項和業界標準認證,促使即使是受監管的企業也開始採用純SaaS環境。同時,在需要空氣間隙環境的領域,本地部署和託管模式仍然可行,但它們的總合收入貢獻逐年下降。混合架構透過在本地保留關鍵的呼叫控制功能,同時將彈性工作負載擴展到雲端,為規避風險的企業提供了一個過渡期,因此正日益受到青睞。整合遷移工具、零接觸設備配置和按用戶訂閱選項預計將在未來五年內進一步降低本地部署的市場佔有率。

到2025年,語音/IP電話將維持34.88%的收入佔有率,反映出銷售、服務和事件回應領域對即時對話的持續依賴。然而,協作/內容共用將以27.20%的複合年成長率實現最快成長,這主要得益於向整合聊天、協作編輯、白板和任務追蹤等功能的多工具工作空間的轉變。隨著企業傾向於將非同步媒體與業務應用程式整合,語音在整合通訊與協作(UC&C)市場的佔有率將逐漸縮小。在整合通訊與協作(UC&C)市場中,供應商正透過將文件協作、數位白板和全天候聊天功能整合到視訊會議中,模糊各個組件之間的界線。

區域分析

北美地區將佔2025年總收入的25.12%,凸顯了其作為領先的整合通訊平台,這反映了該地區較高的寬頻普及率和分散辦公模式。墨西哥近岸製造業的蓬勃發展正在增加對跨境協作的需求,並推動統一通訊套件中西班牙語和英語雙語支援的發展。

亞太地區是成長最快的區域,年複合成長率高達18.05%。中國的雲端通訊供應商受益於國家主導的5G部署和企業數位化計劃,而資料主權法規則有利於國內託管合作夥伴。日本的5G投資藍圖目標是到2026會計年度實現4.362兆日圓(約310億美元)的通訊設備銷售額,顯示其在身臨其境型協作基礎設施的投入將持續成長。印度的「Bharat 6G聯盟」在與美國和其他國家簽署的政府間合作備忘錄的支持下,旨在大幅推進高頻寬應用,並擴大統一通訊供應商的長期潛在市場規模(TAM)。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 對混合辦公模式日益成長的需求推動了統一通訊即服務 (UCaaS) 的轉型。

- 人工智慧增強的會議效率和自動化工具

- 透過整合統一通訊和CCaaS,簡化客戶體驗

- 5G和邊緣運算實現低延遲身臨其境型協作

- 行業工作流程整合(例如,用於遠端醫療的UC套件)

- 永續性,節能型雲端統一通訊解決方案更受青睞。

- 市場限制

- 嚴格的安全和合規要求減緩了採用速度。

- 舊有系統整合的複雜性和高昂的切換成本

- 通訊API的商品化對服務提供者的利潤率帶來壓力。

- 資料主權區域碎片化推高了營運成本。

- 供應鏈分析

- 監管環境

- 技術展望

- 波特五力模型

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

- 對影響市場的宏觀經濟因素進行評估

第5章 市場規模與成長預測

- 按部署模式

- 本機部署/託管

- 雲

- 按組件

- 語音/IP電話

- 視訊會議

- 通訊和線上狀態

- 協作/內容共用

- 其他

- 按組織規模

- 小型企業

- 主要企業

- 按最終用戶行業分類

- BFSI

- 醫療保健和生命科學

- 零售與電子商務

- 公共部門和教育

- 資訊科技和電信

- 製造/物流

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 德國

- 英國

- 法國

- 荷蘭

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲和紐西蘭

- 亞太其他地區

- 中東和非洲

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 其他非洲地區

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Microsoft

- Cisco Systems

- Zoom Video Communications

- RingCentral

- 8x8

- Avaya

- Mitel

- Google(Google Workspace and Voice)

- GoTo(GoToConnect)

- Verizon

- ATandT

- T-Mobile US

- Vonage

- Dialpad

- Nextiva

- Alcatel-Lucent Enterprise

- NEC Corporation

- Sangoma Technologies

- Ericsson(Vonage APIs)

- Fuze

- Twilio(Flex and UC APIs)

- Slack(Salesforce)

- Amazon Web Services(Chime, Connect)

- Tencent Cloud

- Orange Business Services

- Comcast Business/Masergy

第7章 市場機會與未來展望

The unified communications and collaboration market is expected to grow from USD 186.05 billion in 2025 to USD 236.21 billion in 2026 and is forecast to reach USD 779.47 billion by 2031 at 26.97% CAGR over 2026-2031.

Expanding hybrid-work programs, AI-augmented productivity features, and the need to collapse disparate voice, video, messaging, and workflow applications into a single cloud environment drive this momentum. Enterprises continue reallocating digital-transformation budgets toward communication tools that raise employee engagement across distributed teams. Incumbents such as Microsoft, Cisco, and RingCentral defend share through horizontal platform depth, while AI-first challengers target niche workflow gaps. Strategic mergers-RingCentral's USD 650 million purchase of Mitel and Ericsson's USD 6.2 billion acquisition of Vonage-illustrate how vendors bundle unified communications with contact-center and API capabilities to widen addressable markets.

Global Unified Communications And Collaboration Market Trends and Insights

Hybrid-Work Demand Accelerates UCaaS Migration

Enterprises replacing legacy PBX systems report lower maintenance costs and improved uptime after moving workloads into Microsoft Teams Phone, achieving a 78% telecom-expense reduction at Florida Crystals Corporation. Rising adoption rates among Canadian mid-market firms show the same trajectory, validating cloud UC for geographically dispersed staff. Providers that bundle voice, video, chat, and workflow apps on one license displace point solutions and deepen customer stickiness. The shift squeezes traditional telephony vendors that lack cloud scale, bolstering revenue for UCaaS specialists able to execute global roll-outs quickly. Larger install bases in North America mean the region remains the bellwether for new functionality introductions.

AI-Augmented Meeting Productivity and Automation Tools

Microsoft's AI business exited Q2 2025 at a USD 13 billion annual run rate, driven by Copilot services embedded in Teams meetings, calls, and messages. RingCentral likewise monetizes AI Receptionist capabilities, crossing 1,000 customers with over USD 50 million in annual recurring revenue. Real-time transcription, multilingual translation, and automated meeting summaries move unified communications from passive connectivity to active decision support. Healthcare providers using AI call-triage features report lower no-show rates and faster response times, demonstrating tangible clinical outcomes. Competitive focus now centers on inference quality and seamless workflow integration rather than raw feature counts.

Stringent Security and Compliance Requirements Slow Adoption

HIPAA for healthcare, PCI-DSS for payments, and GDPR for European user data add encryption, audit, and localization layers that lengthen deployment timelines. Smarsh reinforced its compliance position by acquiring CallCabinet in February 2025, bundling AI-driven call recording and analytics into its archive platform. Financial firms must capture every modality-voice, video, chat-for MiFID II, prompting rigorous vendor due-diligence and driving demand for specialty compliance stacks. Providers without end-to-end certifications risk exclusion from regulated tenders, limiting addressable revenue.

Other drivers and restraints analyzed in the detailed report include:

- UC-CCaaS Convergence to Streamline Customer Experience

- 5G and Edge Computing Enable Low-Latency Immersive Collaboration

- Legacy System Integration Complexity and High Switching Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud services represented 66.18% of spending in 2025 and maintain the highest trajectory at 28.55% CAGR, making the segment the nucleus of the unified communications and collaboration market. The unified communications and collaboration market size for cloud deployments is forecast to widen sharply as companies phase out depreciated PBX hardware. Vendors continue to certify advanced encryption, sovereign-cloud options, and industry templates, convincing even regulated firms to adopt pure SaaS footprints. Conversely, on-premises and hosted models persist where air-gapped environments are mandatory, though their collective revenue contribution declines each year. Hybrid architectures gain traction by retaining critical call control on-site while bursting elastic workloads into the cloud, giving risk-averse enterprises a transition runway. Over the next five years, bundled migration tooling, zero-touch device provisioning, and per-user subscription options will further compress the on-premises share.

Voice/IP telephony retained 34.88% revenue share in 2025, reflecting continued reliance on live conversations for sales, service, and incident response. Yet collaboration/content sharing climbs fastest at 27.20% CAGR, underscoring moves toward multitool workspaces that combine chat, co-editing, whiteboarding, and task tracking. The unified communications and collaboration market share for voice will gradually compress as organizations favor asynchronous media that integrates with business applications. Inside the unified communications and collaboration market, vendors embed document co-authoring, digital whiteboards, and persistent chat into video meetings, blurring component boundaries.

The Unified Communications and Collaboration Market is Segmented by Deployment Model (On-premises/Hosted, Cloud), Component (Voice/IP Telephony, Video Conferencing, Messaging and Presence and More), Organization Size (SMEs, Large Enterprises), End-User Industry (BFSI, Healthcare and Life Sciences, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD)

Geography Analysis

North America contributed 25.12% of 2025 revenue, underscoring its role as the primary R&D and early-adopter region for unified communications platforms. U.S. enterprises accelerated cloud migrations as Microsoft's commercial cloud sales surpassed USD 42.4 billion in Q3 2025, up 20% year over year. Canadian mid-market adoption tops three quarters of medium-sized firms, reflecting favorable broadband penetration and distributed workforce patterns. Mexico's near-shoring manufacturing boom increases cross-border collaboration demand, encouraging Spanish-English language services within UC suites.

Asia-Pacific is the fastest-growing territory at an 18.05% CAGR. China's cloud-communications vendors benefit from state-backed 5G roll-outs and enterprise digitization drives, although data-sovereignty rules favor domestic hosting partners. Japan's 5G investment roadmap, targeting JPY 4.362 trillion (USD 0.031 trillion) in telecom equipment sales by FY 2026, signals sustained spending on immersive collaboration infrastructure. India's Bharat 6G alliance, supported by government memoranda of understanding with the United States and others, aims to leapfrog high-bandwidth application readiness, enhancing long-term TAM for UC vendors.

- Microsoft

- Cisco Systems

- Zoom Video Communications

- RingCentral

- 8x8

- Avaya

- Mitel

- Google (Google Workspace and Voice)

- GoTo (GoToConnect)

- Verizon

- ATandT

- T-Mobile US

- Vonage

- Dialpad

- Nextiva

- Alcatel-Lucent Enterprise

- NEC Corporation

- Sangoma Technologies

- Ericsson (Vonage APIs)

- Fuze

- Twilio (Flex and UC APIs)

- Slack (Salesforce)

- Amazon Web Services (Chime, Connect)

- Tencent Cloud

- Orange Business Services

- Comcast Business / Masergy

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Hybrid?work demand accelerates UCaaS migration

- 4.2.2 AI-augmented meeting productivity and automation tools

- 4.2.3 UC-CCaaS convergence to streamline customer experience

- 4.2.4 5G and edge computing enable low-latency immersive collaboration

- 4.2.5 Vertical-specific workflow integration (e.g., tele-health UC kits)

- 4.2.6 Sustainability mandates favor energy-efficient cloud UC solutions

- 4.3 Market Restraints

- 4.3.1 Stringent security and compliance requirements slow adoption

- 4.3.2 Legacy system integration complexity and high switching costs

- 4.3.3 Telecom-API commoditization squeezing provider margins

- 4.3.4 Regional data-sovereignty fragmentation inflates operating costs

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assesment of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Model

- 5.1.1 On-premises / Hosted

- 5.1.2 Cloud

- 5.2 By Component

- 5.2.1 Voice / IP Telephony

- 5.2.2 Video Conferencing

- 5.2.3 Messaging and Presence

- 5.2.4 Collaboration/Content Sharing

- 5.2.5 Others

- 5.3 By Organization Size

- 5.3.1 SMEs

- 5.3.2 Large Enterprises

- 5.4 By End-user Industry

- 5.4.1 BFSI

- 5.4.2 Healthcare and Life Sciences

- 5.4.3 Retail and E-commerce

- 5.4.4 Public Sector and Education

- 5.4.5 IT and Telecom

- 5.4.6 Manufacturing and Logistics

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Netherlands

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Microsoft

- 6.4.2 Cisco Systems

- 6.4.3 Zoom Video Communications

- 6.4.4 RingCentral

- 6.4.5 8x8

- 6.4.6 Avaya

- 6.4.7 Mitel

- 6.4.8 Google (Google Workspace and Voice)

- 6.4.9 GoTo (GoToConnect)

- 6.4.10 Verizon

- 6.4.11 ATandT

- 6.4.12 T-Mobile US

- 6.4.13 Vonage

- 6.4.14 Dialpad

- 6.4.15 Nextiva

- 6.4.16 Alcatel-Lucent Enterprise

- 6.4.17 NEC Corporation

- 6.4.18 Sangoma Technologies

- 6.4.19 Ericsson (Vonage APIs)

- 6.4.20 Fuze

- 6.4.21 Twilio (Flex and UC APIs)

- 6.4.22 Slack (Salesforce)

- 6.4.23 Amazon Web Services (Chime, Connect)

- 6.4.24 Tencent Cloud

- 6.4.25 Orange Business Services

- 6.4.26 Comcast Business / Masergy

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment