|

市場調查報告書

商品編碼

1851741

機器人流程自動化(RPA):市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)Robotic Process Automation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

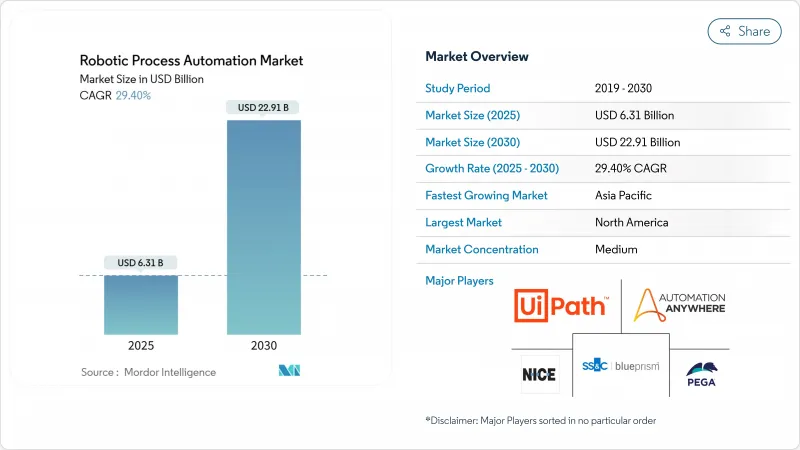

預計到 2025 年,機器人流程自動化 (RPA) 市場規模將達到 63.1 億美元,到 2030 年將達到 229.1 億美元,預測期(2025-2030 年)的複合年成長率為 29.40%。

生成式人工智慧與現有RPA平台的日益融合,正在拓展可自動化任務的範圍,從而解決以往需要人工干預的非結構化流程。雲端原生部署也透過縮短引進週期和將支出重新分配到營運預算中,推動了市場成長。北美地區憑藉嚴格的合規性和成熟的技術生態系統,預計到2024年將佔據最大的機器人流程自動化(RPA)市場佔有率,達到39.6%;而亞太地區預計將以34.5%的複合年成長率(CAGR)實現最快成長,這主要得益於政府支持的自動化項目以及中小企業採用付費使用制機器人。供應商之間的競爭日益激烈,他們透過專注於人工智慧的收購和合作,將智慧文件處理、低程式碼設計和自主代理功能整合到各自的平台藍圖中。

全球機器人流程自動化 (RPA) 市場趨勢與洞察

全通路零售訂單履行自動化

為了滿足消費者對即時購物的期望,零售商正在推動庫存核對、出貨編配和退貨管理的自動化。 Grupo Exito實施了一項企業級RPA(機器人流程自動化)項目,將其電商前端與原有ERP數據連接起來,訂單處理時間縮短了高達75%。透過整合電腦視覺模組,該公司在高峰期保持了98%以上的準確率,而人工智慧驅動的需求預測則幫助零售商在供應鏈不確定性的情況下應對利潤壓力。因此,無論是在成熟市場或新興電商市場,零售商都將自動化視為應對物流中斷和勞動力短缺的必要保障。

中小企業採用雲端原生RPA平台

基於消費的SaaS模式降低了中小企業的進入門檻。 Jana Small Finance Bank在遷移到UiPath雲端服務後,無需部署本地基礎設施,關鍵流程的周轉時間縮短了約70%。隨著超大規模服務供應商將RPA整合到其市場中,中小企業可以在幾天內部署安全的機器人,並僅根據交易量的成長擴展許可證。分析師預測,隨著公民開發者工具的成熟和特定產業模板的普及,到2027年,中小企業將佔新機器人部署量的40%以上。

由於使用者介面變更導致機器人持續故障

企業和SaaS應用頻繁的介面更新會讓選擇器感到困惑,並導致機器人無法正常運作。 Tarsus Distribution在供應商格式變更後不得不重新設計其發票工作流程,這凸顯了其舊版螢幕抓取機器人的脆弱性。雖然新平台增加了物件式的選擇器和自癒功能,但變更管理方面的不足仍然拖慢了擴展計劃的步伐,並削弱了人們對這個新興專案的信心。

細分市場分析

到2024年,本地部署將佔機器人流程自動化 (RPA) 市場54.3%的佔有率。儘管如此,雲端採用率仍將以38.2%的複合年成長率 (CAGR) 保持最高水平,但隨著安全認證的普及,這一差距將會縮小。 UiPath表示,超過80%的新訂單來自雲端訂閱,客戶的部署速度比本地部署快50%。歐洲銀行正在採用混合模式,在內部管理敏感的支付工作流程,同時利用雲端租戶進行設計、測試和分析。這種靈活性使企業能夠在滿足居住要求的同時,保持彈性容量。

隨著邊緣運算技術的成熟,供應商正在打包輕量級運行時環境,這些環境可在本地運行,但可從雲端接收編配。此類架構可降低工廠車間機器人的延遲,同時最大限度地減少伺服器管理開銷。因此,許多製造商計劃在未來三年內將其非生產機器人遷移到 SaaS 平台,理由是 SaaS 可以簡化修補程式管理並即時取得 AI 升級。因此,訂閱收入很可能超過永久授權收入,並繼續推動機器人流程自動化 (RPA) 市場的發展。

到2024年,軟體平台將佔總營收的51.3%,而隨著企業意識到以人為本的變革管理是成功的關鍵,服務業正以35.1%的複合年成長率快速成長。越來越多的企業將需求探索、流程再造和開發人員輔導等服務打包在一起,這些服務約佔整體轉型預算的60%。 SS&C Technologies將Blue Prism軟體與諮詢服務結合,使其機器人數量增加了兩倍,並節省了1億美元的成本。

由於智慧自動化需要不斷調整人工智慧模型,因此對持續改善服務的需求也日益成長。供應商現在提供的託管服務以服務等級協定 (SLA) 為基礎,而非以單一計劃里程碑為導向,從而保證最終成果。這種轉變進一步擴大了機器人流程自動化 (RPA) 服務市場的佔有率,凸顯了該產業正從工具實施向重塑整個企業營運模式的轉變。

機器人流程自動化 (RPA) 市場配置(本地部署、雲端/SaaS)、解決方案元件(軟體、服務)、公司規模(中小企業、大型企業)、技術類型(有人值守 RPA、無人值守 RPA、智慧/認知 RPA)、最終用戶產業(銀行、金融服務和保險 (BFSI)、IT 和電信、醫療保健、其他地區)以及電信、醫療保健地區進行細分、其他地區進行區域醫療保健市場預測以美元計價。

區域分析

北美地區將在2024年繼續保持領先地位,市佔率將達到39.6%,這主要得益於該地區早期採用率較高,以及政府和金融服務領域嚴格的合規要求。例如,美國住房與城市發展部等機構正在採用RPA(機器人流程自動化)和機器學習相結合的方法來改善福利處理流程。加州機動車輛管理局等州級機構則利用機器人來加速數位化駕照服務,並確保在疫情期間服務不會中斷。供應商格局受益於豐富的系統整合能力和熟練的自動化專業人員,從而確保了業務的持續成長。

亞太地區是成長最快的地區,複合年成長率高達34.5%。日本的RPA系統Robopat DX在中小企業中的安裝量已超過1700套,顯示在勞動市場緊張的情況下,RPA系統擁有強大的市場基礎。印度馬尼帕爾醫院已實現財務工作流程自動化,以符合日益完善的數位化醫療法規。政府補貼和本地語言介面支援預計將進一步擴大製造商和外包中心對RPA系統的應用,從而推動該地區機器人流程自動化(RPA)市場的發展。

在歐洲,《數位營運韌性法案》要求銀行記錄並對其自動化工作流程進行壓力測試。金融機構已累計多年預算,每家銀行的預算高達1500萬歐元,以確保在2025年之前達到合規要求。德國製造商正在推動後勤部門自動化,而北歐醫療保健系統則在全部區域部署共用的機器人庫。採用本地數據和透過雲端主機編配的混合部署結構正逐漸成為主流,穩步提升了機器人流程自動化(RPA)市場在歐盟成員國的影響力。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 零售全通路履約自動化

- 中小企業採用雲端原生RPA平台

- 基於 GEN-AI 的機器人設計助手

- 超大規模市場的計量收費機器人

- DORA 和 HIPAA 之後的合規主導自動化

- 全球共享服務中心人才短缺

- 市場限制

- UI 變更導致機器人持續故障

- 無人機器人的管治與倫理審查

- 從傳統RPA套件轉換過來成本高昂

- 新興市場流程標準化程度低

- 產業價值鏈分析

- 監管環境

- 技術展望

- 產業吸引力:波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 宏觀經濟因素如何影響市場

第5章 市場規模與成長預測

- 透過部署

- 本地部署

- 雲/SaaS

- 按解決方案組件

- 軟體(平台和許可)

- 服務(實施、卓越中心、支援)

- 按公司規模

- 中小企業

- 主要企業

- 依技術類型

- 參加了RPA

- 無人值守的RPA

- 智慧型/認知型RPA

- 按最終用戶行業分類

- BFSI

- 資訊科技和電訊

- 衛生保健

- 零售及消費品

- 製造業

- 其他終端用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 智利

- 其他南美洲

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 新加坡

- 馬來西亞

- 澳洲

- 亞太其他地區

- 中東和非洲

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- UiPath Inc.

- Automation Anywhere Inc.

- SS&C Blue Prism Ltd.

- NICE Ltd.(Robotic Automation)

- Pegasystems Inc.

- Kofax Inc.

- WorkFusion Inc.

- Kryon Systems Ltd.

- EdgeVerve Systems Ltd.

- AntWorks Pte Ltd.

- Laiye Technology Ltd.

- Cyclone Robotics Co. Ltd.

- AutomationEdge Technologies Inc.

- Datamatics Global Services Ltd.

- Nividous Software Solutions

- Soroco

- Redwood Software Inc.

- Microsoft Corp.(Power Automate)

- Servicetrace GmbH

- Jidoka(Novayre Solutions)

- Fortra LLC(ex-HelpSystems)

- ElectroNeek Robotics Inc.

- Robocorp Technologies Inc.

- Robiquity Ltd.

- Rocketbot SpA

- OpenConnect Systems Inc.

第7章 投資分析

第8章 市場機會與未來趨勢

- 閒置頻段與未滿足需求評估

The Robotic Process Automation Market size is estimated at USD 6.31 billion in 2025, and is expected to reach USD 22.91 billion by 2030, at a CAGR of 29.40% during the forecast period (2025-2030).

Increasing integration of generative AI with established RPA platforms widens the range of automatable tasks and lets enterprises address unstructured processes that once required human intervention. Expansion is also fueled by cloud-native deployments that shorten implementation cycles and shift spending to operating budgets. North America held the largest Robotic Process Automation market share at 39.6% in 2024, supported by stringent compliance mandates and mature technology ecosystems, while Asia-Pacific is registering the fastest regional CAGR of 34.5% as governments sponsor automation programs and SMEs adopt pay-as-you-go bots. Vendor competition is intensifying through AI-focused acquisitions and partnerships that bundle intelligent document processing, low-code design, and autonomous agent capabilities into platform roadmaps.

Global Robotic Process Automation Market Trends and Insights

Retail Omni-Channel Order-Fulfilment Automation

Retailers are automating inventory reconciliation, shipment orchestration, and return management to keep pace with real-time consumer expectations. Grupo Exito cut order-processing times by up to 75% after deploying an enterprise-wide RPA program that links e-commerce front ends with legacy ERP data. Integration of computer-vision modules maintains accuracy above 98% during peak seasons, while AI-assisted demand forecasting helps retailers manage margin pressure amid supply-chain volatility. Retailers in both mature and emerging e-commerce markets, therefore, view automation as an essential hedge against logistics disruptions and labor shortages.

SME Adoption of Cloud-Native RPA Platforms

Consumption-based SaaS models are lowering entry barriers for small firms. Jana Small Finance Bank shortened critical process turnaround times by nearly 70% after migrating to UiPath's cloud service, with no on-premise infrastructure required. As hyperscale providers embed RPA into their marketplaces, SMEs can deploy secure bots within days and scale licenses only when transaction volumes rise. Analysts expect SMEs to drive more than 40% of net-new bot deployments by 2027 as citizen-developer tools mature and industry-specific templates proliferate.

Persistent Bot Breakage from UI Changes

Frequent interface updates in enterprise and SaaS apps disrupt selectors and render bots inoperable, consuming up to 40% of annual automation budgets for reactive maintenance. Tarsus Distribution had to redesign invoice workflows when supplier formats shifted, highlighting the fragility of legacy, screen-scraping bots. Newer platforms add object-based selectors and self-healing functions, yet change-management shortcomings continue to delay scaling plans and erode confidence in early-stage programs.

Other drivers and restraints analyzed in the detailed report include:

- Gen-AI-Powered Bot-Design Assistants

- Pay-as-You-Go Bots on Hyperscale Marketplaces

- Governance and Ethical Scrutiny of Unattended Bots

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

On-premise installations remained dominant at 54.3% of the Robotic Process Automation market in 2024 because heavily regulated sectors required local control. Cloud deployments nevertheless posted the highest 38.2% CAGR and will narrow the gap as security certifications expand. UiPath stated that more than 80% of new bookings stem from cloud subscriptions, and customers achieve rollouts 50% faster than on-premise equivalents. The hybrid pattern is gaining ground as European banks keep sensitive payment workflows in-house while using cloud tenants for design, test, and analytics. This flexibility lets firms satisfy residency mandates without forfeiting elastic capacity.

As edge computing matures, vendors package lightweight run-times that execute locally yet receive orchestration from the cloud. Such architectures reduce latency for factory-floor bots while minimizing server administration overhead. Consequently, many manufacturers plan to migrate their non-production robots to SaaS within three years, citing simplified patching and immediate access to AI upgrades. The resulting shift will continue to boost the Robotic Process Automation market as subscription revenue overtakes perpetual licenses.

Software platforms controlled 51.3% of revenue in 2024, but services are expanding at a 35.1% CAGR as organizations recognize that people-centric change management dictates success. Implementers increasingly bundle discovery, re-engineering, and citizen-developer coaching, representing roughly 60% of total transformation budgets. SS&C Technologies realized USD 100 million in cost savings by pairing Blue Prism software with advisory services that tripled its bot count.

Demand for continuous-improvement retainers is also rising because intelligent automation requires ongoing AI model tuning. Vendors now position managed service offers that guarantee SLA-based outcomes rather than discrete project milestones. This pivot further inflates the Robotic Process Automation market size allocated to services and underscores the sector's progression from tool adoption toward enterprise-wide operating model redesign.

Robotic Process Automation Market is Segmented by Deployment (On-Premise and Cloud/SaaS), Solution Component (Software and Services), Enterprise Size (Small and Medium Enterprises and Large Enterprises), Technology Type (Attended RPA, Unattended RPA, and Intelligent/Cognitive RPA), End-User Industry (BFSI, IT and Telecom, Healthcare, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained leadership with a 39.6% share in 2024, propelled by early adoption curves and rigorous compliance mandates across government and financial services. Agencies such as the U.S. Department of Housing and Urban Development employ combined RPA and machine-learning approaches to modernize benefit processing. State entities like the California DMV leveraged bots to accelerate digital licensing services, allowing continuity during pandemic disruptions. The vendor landscape benefits from abundant system-integrator capacity and skilled automation professionals, ensuring continuous pipeline growth.

Asia-Pacific is the fastest-growing geography at 34.5% CAGR. Japan's RPA Robopat DX passed 1,700 SME implementations, signaling grassroots demand in a tight labor market. India's Manipal Hospitals automated finance workflows to comply with expanding digital health regulations. Government subsidy schemes and local-language interface support will further widen adoption among manufacturers and outsourcing hubs, magnifying the Robotic Process Automation market in the region.

Europe's trajectory is shaped by the Digital Operational Resilience Act, which compels banks to document and stress-test automated workflows. Institutions have earmarked multi-year budgets reaching EUR 15 million per entity to meet the 2025 compliance deadline. German manufacturers showcase deep back-office automation, while Nordic healthcare systems deploy region-wide shared-bot libraries. Hybrid deployment structures that retain data on-premise yet orchestrate via cloud consoles are becoming the norm, steadily increasing the Robotic Process Automation market presence across European Union member states.

- UiPath Inc.

- Automation Anywhere Inc.

- SS&C Blue Prism Ltd.

- NICE Ltd. (Robotic Automation)

- Pegasystems Inc.

- Kofax Inc.

- WorkFusion Inc.

- Kryon Systems Ltd.

- EdgeVerve Systems Ltd.

- AntWorks Pte Ltd.

- Laiye Technology Ltd.

- Cyclone Robotics Co. Ltd.

- AutomationEdge Technologies Inc.

- Datamatics Global Services Ltd.

- Nividous Software Solutions

- Soroco

- Redwood Software Inc.

- Microsoft Corp. (Power Automate)

- Servicetrace GmbH

- Jidoka (Novayre Solutions)

- Fortra LLC (ex-HelpSystems)

- ElectroNeek Robotics Inc.

- Robocorp Technologies Inc.

- Robiquity Ltd.

- Rocketbot SpA

- OpenConnect Systems Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Retail omni-channel order-fulfilment automation

- 4.2.2 SME adoption of cloud-native RPA platforms

- 4.2.3 Gen-AI powered bot-design assistants

- 4.2.4 Pay-as-you-go bots on hyperscale marketplaces

- 4.2.5 Compliance-driven automation post-DORA and HIPAA

- 4.2.6 Global talent shortages in shared-service centres

- 4.3 Market Restraints

- 4.3.1 Persistent bot breakage from UI changes

- 4.3.2 Governance and ethical scrutiny of unattended bots

- 4.3.3 High switching cost from legacy RPA suites

- 4.3.4 Low process standardisation in emerging markets

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Deployment

- 5.1.1 On-premise

- 5.1.2 Cloud/SaaS

- 5.2 By Solution Component

- 5.2.1 Software (Platforms and Licences)

- 5.2.2 Services (Implementation, CoE, Support)

- 5.3 By Enterprise Size

- 5.3.1 Small and Medium Enterprises (SMEs)

- 5.3.2 Large Enterprises

- 5.4 By Technology Type

- 5.4.1 Attended RPA

- 5.4.2 Unattended RPA

- 5.4.3 Intelligent/Cognitive RPA

- 5.5 By End-user Industry

- 5.5.1 BFSI

- 5.5.2 IT and Telecom

- 5.5.3 Healthcare

- 5.5.4 Retail and CPG

- 5.5.5 Manufacturing

- 5.5.6 Other End-user Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Chile

- 5.6.2.4 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Singapore

- 5.6.4.6 Malaysia

- 5.6.4.7 Australia

- 5.6.4.8 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 United Arab Emirates

- 5.6.5.1.2 Saudi Arabia

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 UiPath Inc.

- 6.4.2 Automation Anywhere Inc.

- 6.4.3 SS&C Blue Prism Ltd.

- 6.4.4 NICE Ltd. (Robotic Automation)

- 6.4.5 Pegasystems Inc.

- 6.4.6 Kofax Inc.

- 6.4.7 WorkFusion Inc.

- 6.4.8 Kryon Systems Ltd.

- 6.4.9 EdgeVerve Systems Ltd.

- 6.4.10 AntWorks Pte Ltd.

- 6.4.11 Laiye Technology Ltd.

- 6.4.12 Cyclone Robotics Co. Ltd.

- 6.4.13 AutomationEdge Technologies Inc.

- 6.4.14 Datamatics Global Services Ltd.

- 6.4.15 Nividous Software Solutions

- 6.4.16 Soroco

- 6.4.17 Redwood Software Inc.

- 6.4.18 Microsoft Corp. (Power Automate)

- 6.4.19 Servicetrace GmbH

- 6.4.20 Jidoka (Novayre Solutions)

- 6.4.21 Fortra LLC (ex-HelpSystems)

- 6.4.22 ElectroNeek Robotics Inc.

- 6.4.23 Robocorp Technologies Inc.

- 6.4.24 Robiquity Ltd.

- 6.4.25 Rocketbot SpA

- 6.4.26 OpenConnect Systems Inc.

7 INVESTMENT ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 8.1 White-Space and Unmet-Need Assessment

2025 年至 2033 年機器人流程自動化市場報告(按組件、營運、部署模型、組織規模、最終用戶和地區)

2025 年至 2033 年機器人流程自動化市場報告(按組件、營運、部署模型、組織規模、最終用戶和地區) 按組件和部署類型分類的機器人流程自動化市場 - 2025-2032 年全球預測

按組件和部署類型分類的機器人流程自動化市場 - 2025-2032 年全球預測 自動化 COE 市場 - 全球產業規模、佔有率、趨勢、機會和預測(按服務、組織規模、垂直產業、地區和競爭細分,2020-2030 年預測)

自動化 COE 市場 - 全球產業規模、佔有率、趨勢、機會和預測(按服務、組織規模、垂直產業、地區和競爭細分,2020-2030 年預測) 2032 年金融合規機器人流程自動化市場預測:按組件、部署模型、公司規模、應用、最終用戶和地區進行的全球分析

2032 年金融合規機器人流程自動化市場預測:按組件、部署模型、公司規模、應用、最終用戶和地區進行的全球分析 2025年BFSI全球市場機器人流程自動化報告2025年金融機器人流程自動化全球市場報告

2025年BFSI全球市場機器人流程自動化報告2025年金融機器人流程自動化全球市場報告 自動化 COE 的全球市場全球法律服務機器人流程自動化市場:預測至 2032 年—按解決方案類型、流程類型、部署方法、應用、最終用戶和地區進行分析RPA 平台培訓市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測全球自動化卓越中心市場

自動化 COE 的全球市場全球法律服務機器人流程自動化市場:預測至 2032 年—按解決方案類型、流程類型、部署方法、應用、最終用戶和地區進行分析RPA 平台培訓市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測全球自動化卓越中心市場