|

市場調查報告書

商品編碼

1851707

美國油漆和塗料:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)United States Paints And Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

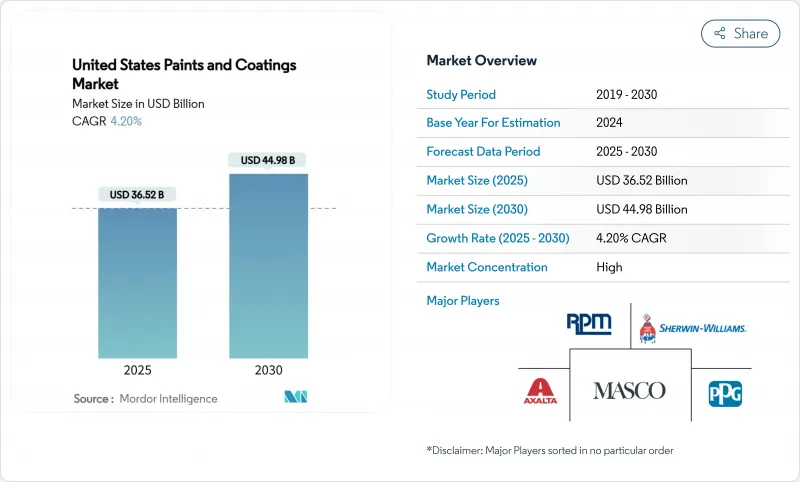

預計到 2025 年,美國油漆和塗料市場規模將達到 365.2 億美元,到 2030 年將達到 449.8 億美元,預測期(2025-2030 年)的複合年成長率為 4.20%。

當前市場擴張主要得益於建築塗料翻新市場的持續強勁成長、水性配方塗料的迅速普及以及聯邦政府基礎設施建設浪潮對防護塗料需求的推動。人口向陽光地帶遷移、製造業向東南部集中以及電商塗料銷售額的穩定成長也提振了潛在需求。此外,由於二氧化鈦價格波動和勞動力市場緊張導致價格上漲,生產商也受益於短期定價權。然而,隨著私募股權支持的整合者運用收購合併策略,以及大型現有企業縮減業務組合以專注於利潤更高的行業細分領域,市場競爭日益加劇。

美國油漆及塗料市場趨勢及洞察

聯邦基礎設施投資和就業法案

自採用IIJA以來,已資助超過4萬個橋樑和道路計劃,並使公路和道路支出增加了36%。高性能環氧樹脂、聚天冬胺酸酯和富鋅底漆受益於此,因為美國交通部(DOT)的規範優先考慮防腐蝕性能而非最低價格的塗層系統。隨著聯邦政府在飲用水基礎設施方面的支出激增62%,水務設施中NSF認證襯裡的規範也不斷擴展。預計到2025年,交通運輸建設將再成長8%,這將為防護塗層施工商帶來未來兩年的穩定訂單。雖然通貨膨脹正在吸收部分撥款並限制訂單量的成長,但由於各機構指定使用更長壽命的系統,價格結構仍保持積極態勢。勞動力短缺是一個主要限制因素,導致計劃工期延長,支出分散到更多季度。

房屋翻新熱潮

由於“鎖定效應”,房屋翻新需求彌補了新房屋建設的疲軟,這種效應促使抵押房屋抵押貸款低於3%的業主選擇重建而非搬遷。剪切機-Williams)報告稱,到2024年,房屋翻新市場將保持高個位數成長。千禧世代組成首個家庭以及嬰兒潮世代維修老舊房屋的需求將支撐塗料銷售的持續成長。數位色彩工具和隔天送達服務正在擴大DIY人群,而專業油漆工則利用行動訂購來減少到店次數。雖然房屋改造需求本質上屬於非必需消費,但人口結構的基本面和老舊住宅存量使其能夠抵禦經濟週期波動。

二氧化鈦價格波動劇烈

二氧化鈦佔建築白色塗料原料成本的50%之多,配方師也證實了這一點。 2024年夏季的價格飆升擠壓了利潤空間,導致立邦塗料等公司宣布2025年合約價格上漲高達9%。大型製造商透過簽訂多年供應協議和採用顏料稀釋技術來規避風險,而小型製造商則面臨庫存損失的風險。目前,針對不透明度最佳化的樹脂體系和奈米顆粒分散體的研究正在加速推進,這些技術能夠在不犧牲遮蓋力的前提下降低二氧化鈦的用量,但商業化應用仍需三到四年。

細分市場分析

丙烯酸樹脂將佔最大佔有率,到2024年將佔總銷售額的35%,這得益於其在牆面塗料和養護塗料中兼具的硬度和柔韌性。終端用戶青睞新一代水性丙烯酸樹脂的低溫成膜和減少異味的特性。隨著汽車製造商和地板塗料規範制定者採用耐久性可與溶劑型配方媲美的雙組分水性配方,聚氨酯的複合年成長率(CAGR)達到5.10%。配方師正在利用脂肪族異氰酸酯的進步,這種材料即使在強烈的紫外線照射下也能抵抗泛黃。醇酸樹脂的市場佔有率正在下降,但它仍然服務於快乾金屬底漆和對成本敏感的承包商市場。聚酯樹脂正在圍欄和暖通空調面板的粉末塗料領域開闢一片天地。特種混合體系利潤豐厚,使中型製造商能夠與丙烯酸樹脂的通用供應商競爭。在美國塗料市場,聚氨酯預計將在工業和汽車應用領域削弱丙烯酸的主導,而丙烯酸將在消費品和建築應用領域保持其統治地位。

2024年,水性塗料系統將佔銷售額的67%,反映了監管和消費者需求的成長趨勢。流變改質劑和非團聚黏合劑的持續進步正在縮小水性塗料與溶劑型塗料的性能差距,隨著美國塗料市場向更環保的選擇轉型,水性塗料的成長速度將高於平均水平。粉末塗料技術憑藉零VOC認證和可再生噴塗工藝,在電器、金屬家具和汽車輪轂等領域的市場佔有率不斷成長。雖然溶劑型塗料在一些對固化條件要求苛刻的重型和海洋環境中仍然不可或缺,但由於空氣品質法規的日益嚴格,其市場佔有率將繼續下降。需要色彩靈活性和高塗膜性能的塗裝車間正在興起混合型粉末和液體塗料生產線。總而言之,這些變化正在重塑技術組合,並推動對固化能量模型、粉末噴塗機器人和LED-UV燈系統的投資。

美國油漆市場細分報告按樹脂類型(丙烯酸樹脂、醇酸樹脂、聚氨酯樹脂、環氧樹脂、聚酯樹脂、其他樹脂類型)、技術(水性塗料、溶劑型塗料、粉末塗料、UV技術)、配銷通路(公司自營商店、獨立油漆分銷商、其他)和最終用戶行業(建築、汽車、木材、防護塗料、一般工業、其他)對行業進行細分。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 聯邦基礎設施投資和就業法案推動橋樑和公路被覆劑需求

- 家居裝修熱潮帶動了DIY建築塗料的銷售量。

- 轉向粉末塗料和紫外光固化塗料推動美國空氣排放標準提高

- 製造業回流刺激了美國地區對工業塗料的需求

- 汽車產業的成長

- 市場限制

- 二氧化鈦價格波動對生產商的淨利率帶來壓力。

- 工業塗裝技術人員短缺導致計劃工期延誤

- 運費上漲擾亂油漆零售商的庫存週期

- 改用PVC牆板和複合材料牆板可以減少外牆塗料的消耗。

- 價值鏈分析

- 監理展望

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 產業間競爭

第5章 市場規模與成長預測

- 依樹脂類型

- 丙烯酸纖維

- 醇酸

- 聚氨酯

- 環氧樹脂

- 聚酯纖維

- 其他樹脂類型

- 透過技術

- 水溶液

- 溶劑型

- 粉末塗裝

- 紫外線技術

- 透過分銷管道

- 直營店

- 獨立油漆經銷商

- 大型超市和五金店

- 直接向工業OEM廠商銷售

- 電子商務

- 按最終用戶行業分類

- 建築學

- 車

- 木頭

- 保護漆

- 一般工業

- 運輸

- 包裝

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Akzo Nobel NV

- Axalta Coating Systems, LLC

- BASF

- Beckers Group

- Benjamin Moore & Co.

- Carboline

- Diamond Vogel

- Dunn-Edwards Corporation

- Hempel A/S

- Masco Corporation

- Nippon Paint Holdings Co., Ltd.

- Parker Hannifin

- PPG Industries, Inc.

- RPM International Inc.

- Rust-Oleum Corporation

- Sika AG

- The Sherwin-Williams Company

- Tnemec

- Wacker Chemie AG

第7章 市場機會與未來展望

The United States Paints And Coatings Market size is estimated at USD 36.52 billion in 2025, and is expected to reach USD 44.98 billion by 2030, at a CAGR of 4.20% during the forecast period (2025-2030).

The current expansion rests on the sustained strength of architectural repaint activity, the sharp pivot toward waterborne formulations, and a federal infrastructure wave lifting volumes of protective products. Underlying demand is reinforced by population migration to the Sun Belt, manufacturing reshoring in the Southeast, and a steady rise in e-commerce paint sales. Producers also benefit from near-term pricing power as volatile titanium-dioxide costs and tight labor conditions make price increases stick. Competitive intensity, however, is heightening as private-equity backed consolidators apply a buy-and-build playbook while large incumbents prune portfolios to favor higher-margin industrial niches.

United States Paints And Coatings Market Trends and Insights

Federal Infrastructure Investment and Jobs Act

The IIJA has funded more than 40,000 bridge and roadway projects, lifting highway and street spending by 36% since its adoption. High-performance epoxy, polyaspartic, and zinc-rich primers benefit because DOT specifications prioritize corrosion protection over lowest-bid paint systems. Specifications for NSF-certified linings in water projects are expanding alongside a 62% federal outlay jump in drinking-water infrastructure. Transportation construction is projected to climb another 8% in 2025, creating a visible two-year order pipeline for protective-coatings applicators. Inflation is absorbing a portion of allocated funds, tempering volume upside, yet price-mix remains positive as agencies specify longer-life systems. Labor availability is the main gating factor, prolonging project schedules and stretching consumption over more calendar quarters.

Home Remodeling Boom

Residential repaint volumes have offset softness in new-build housing thanks to a "lock-in" effect that encourages owners with sub-3% mortgages to renovate rather than relocate. Sherwin-Williams reported high-single-digit growth in repaint categories through 2024. Millennials forming first-time households and baby boomers retrofitting aging homes underpin sustained gallonage. Digital color tools and next-day delivery have expanded the addressable DIY audience, while pro painters use mobile ordering to cut store trips. Remodel demand is inherently discretionary, yet demographic fundamentals and an aging housing stock provide resilience through economic cycles.

Volatile TiO2 Pricing

TiO2 constitutes up to 50% of a white architectural coating's raw-material cost, exposing formulators. Margins compressed during the 2024 summer spike, prompting Nippon Paint and others to announce up to 9% price rises for 2025 contracts. Larger players hedge through multi-year supply deals and pigment-extension technology, while smaller producers risk inventory losses. R&D is intensifying around opacity-optimized resin systems and nanoparticle dispersions that lower TiO2 loading without sacrificing hide, yet widespread commercial scale is still three to four years away.

Other drivers and restraints analyzed in the detailed report include:

- Shift to Powder and UV-Curable Coatings

- Manufacturing Reshoring

- Shortage of Skilled Industrial Painters

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Acrylic chemistries generated the largest slice of 2024 revenue at 35% because they balance hardness and flexibility across both wall paints and maintenance finishes. End-users appreciate low-temperature film formation and odor reduction in next-generation waterborne acrylics. The polyurethane cohort is advancing at a 5.10% CAGR as automakers and floor-coating specifiers adopt two-component water-borne versions that rival solvent-borne durability. Formulators capitalize on aliphatic isocyanate advances that resist yellowing under harsh UV. Alkyds are losing share yet still serve quick-dry metal primers and cost-sensitive contractor markets. Polyester resins are carving powder-coating niches on fencing and HVAC panels. Specialty hybrid systems fetch higher margins, allowing mid-size producers to defend pricing against bulk commodity acrylic suppliers. Over the forecast horizon, the US paints and coatings market will see polyurethane chip away at acrylic leadership in industrial and automotive uses, although acrylic will stay dominant in consumer and builder channels.

Water-borne systems held 67% of 2024 sales, reflecting regulatory and consumer momentum. Continuous advances in rheology modifiers and coalescent-free binders have closed historical performance gaps versus solvent alternatives, driving above-trend growth as the US paints and coatings market shifts toward greener options. Powder technology is gaining share in appliances, metal furniture, and automotive wheels thanks to zero-VOC credentials and reclaimable overspray. Solvent-borne platforms remain essential in select heavy-duty and marine settings where cure conditions are severe, but successive air-quality rules will keep eroding their share. Hybrid powder-liquid lines are emerging in job-coat shops that need color flexibility and high film build capabilities. Collectively, these shifts are reshaping the technology mix and fueling investment in cure-energy modeling, powder spray robots, and LED-UV lamp systems.

The United States Paints and Coatings Market Report Segments the Industry by Resin Type (Acrylic, Alkyd, Polyurethane, Epoxy, Polyester, and Other Resin Types), Technology (Water-Borne, Solvent-Borne, Powder Coating, and UV Technology), Distribution Channel (Company-Owned Stores, Independent Paint Dealers, and More), and End-User Industry (Architectural, Automotive, Wood, Protective Coatings, General Industrial, and More).

List of Companies Covered in this Report:

- Akzo Nobel N.V.

- Axalta Coating Systems, LLC

- BASF

- Beckers Group

- Benjamin Moore & Co.

- Carboline

- Diamond Vogel

- Dunn-Edwards Corporation

- Hempel A/S

- Masco Corporation

- Nippon Paint Holdings Co., Ltd.

- Parker Hannifin

- PPG Industries, Inc.

- RPM International Inc.

- Rust-Oleum Corporation

- Sika AG

- The Sherwin-Williams Company

- Tnemec

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Federal Infrastructure Investment and Jobs Act Catalyzing Bridge and Highway Coatings Demand

- 4.2.2 Home Remodeling Boom Elevating DIY Architectural Paint Volumes

- 4.2.3 Shift to Powder and UV-Curable Coatings to Meet U.S. Air-Emission Standards

- 4.2.4 Manufacturing Reshoring Spurring Industrial Coatings Demand in U.S. Southeast

- 4.2.5 Growth in the Automotive Sector

- 4.3 Market Restraints

- 4.3.1 Volatile TiO2 Pricing Compressing Producer Margins

- 4.3.2 Shortage of Skilled Industrial Painters Delaying Project Completions

- 4.3.3 Freight-Cost Inflation Disrupting Paint-Retailer Inventory Cycles

- 4.3.4 Shift to PVC and Composite Siding Reducing Exterior Paint Consumption

- 4.4 Value Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Industry Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Resin Type

- 5.1.1 Acrylic

- 5.1.2 Alkyd

- 5.1.3 Polyurethane

- 5.1.4 Epoxy

- 5.1.5 Polyester

- 5.1.6 Other Resin Types

- 5.2 By Technology

- 5.2.1 Water-borne

- 5.2.2 Solvent-borne

- 5.2.3 Powder Coating

- 5.2.4 UV technology

- 5.3 By Distribution Channel

- 5.3.1 Company-Owned Stores

- 5.3.2 Independent Paint Dealers

- 5.3.3 Big-Box Retailers and Home Centers

- 5.3.4 Direct to Industrial OEM

- 5.3.5 E-Commerce

- 5.4 By End-user Industry

- 5.4.1 Architectural

- 5.4.2 Automotive

- 5.4.3 Wood

- 5.4.4 Protective Coatings

- 5.4.5 General Industrial

- 5.4.6 Transportation

- 5.4.7 Packaging

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Akzo Nobel N.V.

- 6.4.2 Axalta Coating Systems, LLC

- 6.4.3 BASF

- 6.4.4 Beckers Group

- 6.4.5 Benjamin Moore & Co.

- 6.4.6 Carboline

- 6.4.7 Diamond Vogel

- 6.4.8 Dunn-Edwards Corporation

- 6.4.9 Hempel A/S

- 6.4.10 Masco Corporation

- 6.4.11 Nippon Paint Holdings Co., Ltd.

- 6.4.12 Parker Hannifin

- 6.4.13 PPG Industries, Inc.

- 6.4.14 RPM International Inc.

- 6.4.15 Rust-Oleum Corporation

- 6.4.16 Sika AG

- 6.4.17 The Sherwin-Williams Company

- 6.4.18 Tnemec

- 6.4.19 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

- 7.2 Self-Healing Protective Coatings for Offshore Wind Infrastructure

石膏板紋理:全球市場佔有率和排名、總收入和需求預測(2025-2031年)

石膏板紋理:全球市場佔有率和排名、總收入和需求預測(2025-2031年) 建築塗料和塗料市場(按樹脂類型、技術、應用、最終用途和分銷管道)—全球預測,2025-2032木材壓榨油市場按產品類型、應用、分銷管道和最終用戶分類-2025-2032年全球預測煅燒頁岩市場按產品類型、應用、終端用戶產業和分銷管道分類 - 全球預測 2025-2032油漆和塗料市場(按樹脂類型、技術、產品類型、基材、最終用途產業和分銷管道)—2025-2030 年全球預測

建築塗料和塗料市場(按樹脂類型、技術、應用、最終用途和分銷管道)—全球預測,2025-2032木材壓榨油市場按產品類型、應用、分銷管道和最終用戶分類-2025-2032年全球預測煅燒頁岩市場按產品類型、應用、終端用戶產業和分銷管道分類 - 全球預測 2025-2032油漆和塗料市場(按樹脂類型、技術、產品類型、基材、最終用途產業和分銷管道)—2025-2030 年全球預測 全球燒頁岩市場

全球燒頁岩市場 全球油漆和被覆劑市場:行業分析、規模、佔有率、成長、趨勢和預測(2025-2032)

全球油漆和被覆劑市場:行業分析、規模、佔有率、成長、趨勢和預測(2025-2032) 亞太地區油漆塗料:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)

亞太地區油漆塗料:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年) 2025年石膏板和隔熱材料承包商全球市場報告

2025年石膏板和隔熱材料承包商全球市場報告 2025-2029 年全球乾牆紋理市場

2025-2029 年全球乾牆紋理市場