|

市場調查報告書

商品編碼

1851643

自動內容識別:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)Automatic Content Recognition - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

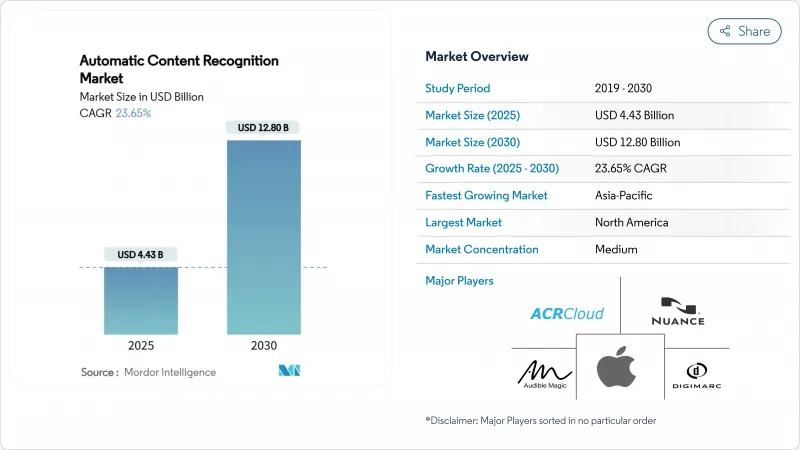

預計到 2025 年,自動內容辨識市場規模將達到 44.3 億美元,到 2030 年將達到 128 億美元,年複合成長率為 23.65%。

2025 年的基準反映了智慧型電視的廣泛普及、預算向定向廣告的重大轉移,以及邊緣人工智慧的穩步發展——這些進步使得指紋識別任務能夠在本地以極低的能耗完成。諸如蘋果 Shazam 在 2024 年實現 1000 億次歌曲識別等突破性部署,展現了在日常消費環境中可以達到的規模。設備製造商正在常規地將自動內容識別 (ACR) 晶片整合到電路板上,從而能夠在無需用戶干預的情況下,從線性廣播、串流應用和 HDMI 輸入中持續提取特徵碼。這種硬體轉型擴大了自動內容識別市場的可尋址資料池,同時降低了延遲。

關鍵數據也印證了這一成長動能。儘管軟體仍佔營收的64%,但隨著品牌將合規性和模型調優外包,託管雲端服務正以24.48%的速度成長。音訊和影像指紋辨識仍是領先技術,佔46%的市場佔有率,但汽車和醫療保健領域的語音驅動應用案例成長最快,複合年成長率達24.11%。安全與版權保護解決方案支出佔比最高,達29%,但面向快速通路的即時分析成長最快,複合年成長率達23.89%。就最終用戶組成而言,媒體和娛樂產業以38%的市場佔有率領先,但受語音商務試點計畫的推動,汽車資訊娛樂產業正以23.78%的複合年成長率迅速縮小差距。按地區分類,北美佔據41%的市場佔有率,預計到2030年亞太地區將佔據24.63%的市場佔有率,這進一步增強了成熟地區和新興地區自動內容識別市場的活力。

全球自動內容識別市場趨勢與洞察

內建ACR晶片的智慧型電視的普及

智慧型電視品牌現在將自動內容識別 (ACR) 處理功能路由到位於應用層下方的系統晶片)模組,即使隱私開關關閉,也能持續進行指紋識別。三星電視大約每分鐘傳輸一次指紋,而 LG 電視則每 15 秒傳輸一次,從而在直播、串流媒體應用和任何 HDMI 來源之間創建不間斷的遠端檢測串流。這些低延遲管道縮短了廣告最佳化的回饋週期,並擴展了自動內容識別市場的數據資源。

可尋址電視廣告預算增加

廣告主正將廣告支出轉向可尋址格式,利用幀級自動內容辨識 (ACR) 的洞察。到 2025 年,可尋址電視廣告預算預計將超過電視廣告總支出的三分之一,到 2027 年將達到 42%。透過將這些洞察與其程序化工作流程結合,FAST 經銷商能夠超越人口統計定向,實現更高的用戶參與度,而歐洲新推出的 HbbTV-TA 認證則規範了技術基準。自動內容辨識市場正受惠於依賴精準即時內容標記的廣告插入技術。

《電子隱私權法》修正案收緊了選擇加入式同意規則。

從2024年底開始,歐洲監管機構將強制執行更複雜的同意橫幅和「同意或付費」指南,這將迫使智慧型電視廠商創建精細化的開關,將自動內容識別(ACR)數據與核心功能區分開來。合規性要求可能會增加工程成本並減少資料量,從而減緩歐洲自動內容識別市場的成長前景。

細分市場分析

到2024年,軟體收入將佔據自動內容辨識市場的大部分佔有率,這主要得益於電視作業系統和串流媒體SDK中緊密嵌入的程式碼。然而,隨著OEM廠商和廣播公司將模型調優、合規性和執行時間管理外包,雲端託管管理服務正以24.48%的複合年成長率快速成長。 Digimarc的年度經常性收入飆升44%至2,390萬美元,顯示在不斷變化的隱私法規下,那些希望獲得承包合規解決方案的客戶更傾向於訂閱收費模式。

服務的激增反映了企業 IT 領域向營運支出 (OPEX) 友善合約的轉變,這些合約通常包含維護、審核日誌和服務等級協定 (SLA) 保障。對於許多中階設備品牌而言,獲得端到端服務的授權比建構必須適應特定地區授權框架的內部技術堆疊更具優勢。因此,分析師預計,到 2030 年,服務在自動內容辨識市場的佔有率將逐年略有成長,而軟體仍將佔據基礎地位,成長速度將放緩。

由於語音和視訊指紋辨識技術成熟,且在直播電視和點播庫中展現出卓越的準確性,因此目前仍佔總收入的 46%。然而,以語音為中心的辨識技術是自動內容辨識領域成長最快的市場,在車載語音助理、遠端健康監測和客服中心分析等領域的推動下,其成長率高達 24.11%。 NTT 的超低延遲語音轉換技術充分展現了即時品質如何滿足企業閾值。

與雲端相比,邊緣晶片功耗降低了92%,使得在電池供電設備和汽車ECU上進行語音分析成為可能。同時,數位浮水印對版權所有者的重要性日益凸顯,而光學字元辨識技術則推動了零售業的銷售量成長。這些發展趨勢豐富了自動內容辨識的產業套件,但並未取代指紋辨識演算法。

自動內容識別市場報告按組件(軟體和服務)、技術(音訊和視訊指紋識別、數位數位浮水印等)、解決方案(即時內容分析、語音和語音介面等)、最終用戶行業(媒體和娛樂、消費性電子 OEM、電信和 IT 等)以及地區進行細分。

區域分析

到2024年,北美將佔據自動內容識別市場41%的收入佔有率,這主要得益於智慧電視家庭普及率超過75%以及成熟的定向廣告供應鏈。各平台正在整合伺服器端插入技術,該技術高度依賴幀級識別,進一步鞏固了該地區的數據優勢。儘管聯邦隱私立法仍處於草案階段,但州級法規和消費者意識的不斷提高可能會在中期內促進資料流動,促使供應商加強用戶許可流程。

亞太地區是自動成長的引擎,預計到2030年將以24.63%的複合年成長率成長。智慧型電視的普及、可支配收入的增加以及對人工智慧實驗室的政策支援共同推動了這一成長。韓國SK Telecom和LG CNS正在基於同一自動內容辨識(ACR)語音技術,建構多語言即時翻譯層。日本的人工智慧法案目前正在國會審議,預計將為研發提供平衡的監管框架,並為供應商提供明確的監管指導。在中國,本土晶片製造企業和演算法公司正在推動在地化技術棧的開發,而國際企業也在努力克服出口障礙。這些因素累積刺激了亞太地區各子區域的自動內容辨識市場。

歐洲既充滿機會也面臨挑戰。 HbbTV-TA認證統一了廣告交易的技術路徑,但歐洲日益嚴格的ePrivacy和GDPR法規使得用戶選擇加入率成為一個不確定因素。嘗試聯邦學習的供應商希望在準確性和匿名性之間取得平衡,從而創建可推廣至其他地區的最佳實踐。因此,歐洲自動內容識別市場的前景取決於該行業能否在遵守監管機構要求的同時,保留對盈利至關重要的數據密集型工作流程。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 內建ACR晶片的智慧型電視的普及

- 可尋址電視廣告預算增加

- 將ACR整合到汽車資訊娛樂系統中

- FAST(免費廣告支援型串流電視)頻道的成長

- 邊緣AI最佳化降低了裝置上的ACR功耗

- 一種新的隱私保護型聯邦學習模型

- 市場限制

- 《電子隱私權法》修正案收緊了選擇加入同意規則

- 蘋果和谷歌採取措施,透過作業系統更新阻止指紋辨識。

- 傳統線性機上盒的 SKU 等級分析能力有限

- 關於浮水印智慧財產權組合的版稅糾紛

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 波特五力模型

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 按組件

- 軟體

- 服務

- 透過技術

- 音訊/視訊指紋識別

- 數位浮水印

- 語音辨識

- 光學字元辨識

- 透過解決方案

- 即時內容分析

- 安全性和權限管理

- 語音/言語介面

- 資料管理和元資料

- 其他

- 按最終用戶行業分類

- 媒體與娛樂

- 消費性電子產品OEM廠商

- 廣告與行銷

- 電訊和資訊技術

- 車

- 衛生保健

- 其他(零售、教育)

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 阿根廷

- 巴西

- 其他南美洲

- 歐洲

- 英國

- 法國

- 德國

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 亞太其他地區

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 土耳其

- 其他中東地區

- 非洲

- 奈及利亞

- 南非

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Apple Inc.(Shazam)

- Audible Magic Corp.

- ACRCloud

- Digimarc Corp.

- Vobile Group Ltd.

- Nuance Communications Inc.

- Kantar Media SAS

- Signalogic Inc.

- VoiceInteraction SA

- Beatgrid BV

- Gracenote(Nielsen)

- SoundHound AI Inc.

- Clarivate(ComScore ACR)

- Yospace Ltd.

- Alphonso(Verizon Media)

- Sorenson Media

- Enswers Inc.

- Intrasonics Ltd.

- Audible Insights LLC

- Civolution BV

第7章 市場機會與未來展望

The Automatic Content Recognition market stood at USD 4.43 billion in 2025 and is on course to touch USD 12.80 billion by 2030, translating into a brisk 23.65% CAGR.

The 2025 baseline reflects broad-based adoption of smart TVs, a decisive budget shift toward addressable advertising, and steady improvements in edge AI that allow fingerprinting tasks to run locally with minimal energy draw. Milestone deployments such as Apple's Shazam logging 100 billion cumulative song recognitions in 2024 showcase the scale now achieved in everyday consumer settings. Device makers routinely embed ACR silicon at the board level, enabling continuous signature extraction from linear broadcasts, streaming apps, and HDMI inputs without user intervention. This hardware pivot enlarges the Automatic Content Recognition market addressable data pool while lowering latency, a combination that keeps advertisers, broadcasters, and analytics providers firmly invested in the technology.

Key data points confirm this momentum. Software still accounts for 64% revenue but managed cloud services are expanding at a 24.48% pace as brands outsource compliance and model tuning. Audio and video fingerprinting remains the leading technology with 46% share, yet speech-driven use cases in cars and healthcare are widening fastest at 24.11% CAGR. Security and copyright protection dominate solution spending with 29% share, although real-time analytics for FAST channels is the quickest riser at 23.89% CAGR. End-user mix is led by media and entertainment at 38%, while automotive infotainment is closing the gap at 23.78% CAGR thanks to voice commerce pilots. Regionally, North America commands 41% value share, whereas Asia Pacific is compounding at 24.63% through 2030-together reinforcing the Automatic Content Recognition market's vitality across both mature and emerging geographies.

Global Automatic Content Recognition Market Trends and Insights

Proliferation of Smart TVs with Embedded ACR Chips

Smart-TV brands now route ACR processing through system-on-chip blocks situated beneath the application layer, allowing continuous fingerprint capture even when privacy toggles are off. Samsung units dispatch signatures roughly every minute, while LG models do so every 15 seconds, creating an uninterrupted telemetry stream that spans live broadcasts, streaming apps, and any HDMI source. These low-latency pipelines shorten the feedback loop for ad optimization and broaden the Automatic Content Recognition market's data inventory.

Expansion of Addressable-TV Advertising Budgets

Advertisers are redirecting spend toward addressable formats that exploit frame-level ACR insights. Budgets dedicated to addressable TV surpassed one-third of total TV outlays in 2025 and are on track for 42% by 2027. FAST distributors pair these insights with programmatic workflows to lift engagement beyond demographic targeting, while new HbbTV-TA certifications in Europe standardize technical baselines. The Automatic Content Recognition market benefits as every incremental ad insertion relies on precise, real-time content labeling.

Stricter Opt-in Consent Rules Under Refreshed ePrivacy Law

European authorities began enforcing refined consent banners and "consent-or-pay" guidance in late 2024, pressuring smart-TV vendors to create granular toggles that isolate ACR data from core functions. Compliance adds engineering overhead and may shrink data volumes, dampening the Automatic Content Recognition market growth outlook within the bloc.

Other drivers and restraints analyzed in the detailed report include:

- Integration of ACR into Automotive Infotainment Systems

- Growth of FAST (Free Ad-Supported Streaming TV) Channels

- Apple/Google Anti-Fingerprinting Moves in OS Updates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software revenue formed the lion's share of the Automatic Content Recognition market size in 2024, thanks to code tightly woven into TV operating systems and streaming SDKs. However, cloud-hosted managed offerings are scaling at 24.48% CAGR as OEMs and broadcasters outsource model tuning, compliance, and uptime management. Digimarc's 44% jump in annual recurring revenue to USD 23.9 million underlines how subscription billing is resonating with customers who prefer turnkey compliance amid changing privacy rules.

The services surge mirrors a broader pivot in enterprise IT toward OPEX-friendly contracts that bundle maintenance, audit logs, and SLA guarantees, for many mid-tier device brands, licensing an end-to-end service beats building an in-house stack that must keep pace with region-specific consent frameworks. Accordingly, analysts expect services to nibble incremental Automatic Content Recognition market share each year through 2030 while software remains foundational yet slower growing.

Audio and video fingerprinting still anchors 46% of revenue due to its maturity and proven accuracy across live TV and on-demand libraries. Yet speech-centric recognition is the Automatic Content Recognition market's quickest riser, compounding at 24.11% on the back of in-car voice assistants, tele-health monitoring, and contact-center analytics. NTT's ultra-low-latency voice conversion work highlights how real-time quality now meets enterprise thresholds.

Edge silicon capable of shaving 92% power relative to cloud chains makes voice analytics feasible in battery-run devices and automotive ECUs. Meanwhile, watermarking gains renewed importance for rights holders, and optical character recognition adds incremental volume in retail. Together, these trajectories diversify the Automatic Content Recognition industry toolkit without displacing staple fingerprinting algorithms.

The Automatic Content Recognition Market Report is Segmented by Component (Software and Services), Technology (Audio and Video Fingerprinting, Digital Watermarking, and More), Solution (Real-Time Content Analytics, Voice and Speech Interfaces, and More), End-User Industry (Media and Entertainment, Consumer Electronics OEMs, Telecom and IT, and More), and Geography.

Geography Analysis

North America generated 41% of Automatic Content Recognition market revenue in 2024, benefiting from smart-TV household penetration above 75% and a well-established addressable-advertising supply chain. Platforms integrate server-side insertion that leans heavily on frame-level recognition, amplifying the region's data advantages. While federal privacy bills remain in draft form, state-level rules and greater consumer awareness could temper data flows mid-term, prompting vendors to reinforce consent flows.

Asia Pacific is the automatic growth engine, expanding at 24.63% CAGR through 2030. Mass-market smart-TV adoption, rising disposable incomes, and policy backing for AI labs act in concert. Korea's SK Telecom and LG CNS are adding multilingual real-time translation layers that rely on the same underlying ACR voices. Japan's AI Bill, now progressing through the Diet, is poised to set balanced R&D guardrails, giving suppliers regulatory clarity. In China, domestic chip fabrication and algorithm houses spur localized stacks even as international players navigate export hurdles. The cumulative effect keeps the Automatic Content Recognition market vibrant across APAC sub-regions.

Europe offers a mix of opportunity and constraint. HbbTV-TA certification has harmonized technical pathways for ad replacement, but the continent's reinforced ePrivacy and GDPR regimes make opt-in rates a swing factor. Vendors experimenting with federated learning expect to reconcile accuracy with anonymity, potentially birthing best practices that later export to other territories. The Automatic Content Recognition market outlook in Europe therefore hinges on the industry's ability to align with regulators while sustaining data-rich workflows critical for monetization.

- Apple Inc. (Shazam)

- Audible Magic Corp.

- ACRCloud

- Digimarc Corp.

- Vobile Group Ltd.

- Nuance Communications Inc.

- Kantar Media SAS

- Signalogic Inc.

- VoiceInteraction SA

- Beatgrid BV

- Gracenote (Nielsen)

- SoundHound AI Inc.

- Clarivate (ComScore ACR)

- Yospace Ltd.

- Alphonso (Verizon Media)

- Sorenson Media

- Enswers Inc.

- Intrasonics Ltd.

- Audible Insights LLC

- Civolution BV

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of Smart TVs with embedded ACR chips

- 4.2.2 Expansion of addressable-TV advertising budgets

- 4.2.3 Integration of ACR into automotive infotainment systems

- 4.2.4 Growth of FAST (Free Ad-Supported Streaming TV) channels

- 4.2.5 Edge AI optimisation lowering on-device ACR power draw

- 4.2.6 Emerging privacy-preserving federated learning models

- 4.3 Market Restraints

- 4.3.1 Stricter opt-in consent rules under refreshed ePrivacy law

- 4.3.2 Apple/Google anti-fingerprinting moves in OS updates

- 4.3.3 Limited SKU-level analytics from legacy linear STBs

- 4.3.4 Royalty disputes over watermark IP portfolios

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Technology

- 5.2.1 Audio and Video Fingerprinting

- 5.2.2 Digital Watermarking

- 5.2.3 Speech and Voice Recognition

- 5.2.4 Optical Character Recognition

- 5.3 By Solution

- 5.3.1 Real-time Content Analytics

- 5.3.2 Security and Copyright Management

- 5.3.3 Voice and Speech Interfaces

- 5.3.4 Data Management and Metadata

- 5.3.5 Others

- 5.4 By End-User Industry

- 5.4.1 Media and Entertainment

- 5.4.2 Consumer Electronics OEMs

- 5.4.3 Advertising and Marketing

- 5.4.4 Telecom and IT

- 5.4.5 Automotive

- 5.4.6 Healthcare

- 5.4.7 Others (Retail, Education)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Argentina

- 5.5.2.2 Brazil

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 France

- 5.5.3.3 Germany

- 5.5.3.4 Rest of Europe

- 5.5.4 Asia Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 Rest of Asia Pacific

- 5.5.5 Middle East

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 Nigeria

- 5.5.6.2 South Africa

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Apple Inc. (Shazam)

- 6.4.2 Audible Magic Corp.

- 6.4.3 ACRCloud

- 6.4.4 Digimarc Corp.

- 6.4.5 Vobile Group Ltd.

- 6.4.6 Nuance Communications Inc.

- 6.4.7 Kantar Media SAS

- 6.4.8 Signalogic Inc.

- 6.4.9 VoiceInteraction SA

- 6.4.10 Beatgrid BV

- 6.4.11 Gracenote (Nielsen)

- 6.4.12 SoundHound AI Inc.

- 6.4.13 Clarivate (ComScore ACR)

- 6.4.14 Yospace Ltd.

- 6.4.15 Alphonso (Verizon Media)

- 6.4.16 Sorenson Media

- 6.4.17 Enswers Inc.

- 6.4.18 Intrasonics Ltd.

- 6.4.19 Audible Insights LLC

- 6.4.20 Civolution BV

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

自動內容識別市場:按組件、技術、內容、平台、應用和產業分類-2026年至2032年全球市場預測

自動內容識別市場:按組件、技術、內容、平台、應用和產業分類-2026年至2032年全球市場預測 2026年全球自動內容辨識市場報告

2026年全球自動內容辨識市場報告 自動內容辨識市場分析及預測(至2035年):依類型、產品類型、技術、應用、元件、設備、功能、部署類型及最終使用者分類

自動內容辨識市場分析及預測(至2035年):依類型、產品類型、技術、應用、元件、設備、功能、部署類型及最終使用者分類 全球自動內容識別市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球自動內容識別市場規模、佔有率、趨勢和成長分析報告(2026-2034) 自動內容辨識市場 - 全球產業規模、佔有率、趨勢、機會、預測(按組件、平台、技術、部署、公司規模、最終用戶產業、應用、地區和競爭格局分類),2021-2031年自動內容辨識市場-2026-2031年預測自動內容辨識軟體市場:2025-2030 年全球預測(依技術、內容、平台、公司規模、部署類型、應用程式和產業垂直分類)

自動內容辨識市場 - 全球產業規模、佔有率、趨勢、機會、預測(按組件、平台、技術、部署、公司規模、最終用戶產業、應用、地區和競爭格局分類),2021-2031年自動內容辨識市場-2026-2031年預測自動內容辨識軟體市場:2025-2030 年全球預測(依技術、內容、平台、公司規模、部署類型、應用程式和產業垂直分類) 自動內容識別市場規模、佔有率、內容、技術、平台、垂直領域和地區成長分析 - 產業預測,2025 年至 2032 年

自動內容識別市場規模、佔有率、內容、技術、平台、垂直領域和地區成長分析 - 產業預測,2025 年至 2032 年 自動內容認識市場,規模,佔有率,產業分析報告:各零件,各部署類型,各技術,各組織規模,各終端用戶,各地區,2025年~2034年的市場預測

自動內容認識市場,規模,佔有率,產業分析報告:各零件,各部署類型,各技術,各組織規模,各終端用戶,各地區,2025年~2034年的市場預測 自動內容識別市場(按產品、最終用途行業和地區)

自動內容識別市場(按產品、最終用途行業和地區)