|

市場調查報告書

商品編碼

1851593

植絨黏合劑:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)Flock Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

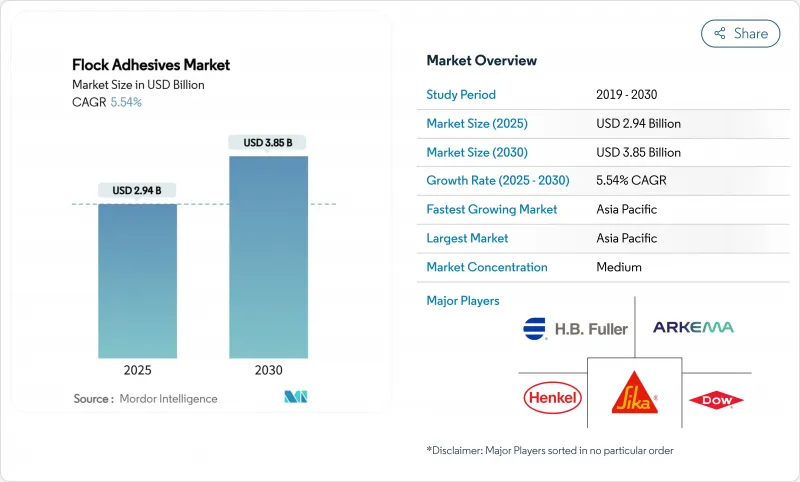

預計到 2025 年,植絨黏合劑市場規模將達到 29.4 億美元,到 2030 年將達到 38.5 億美元,在預測期(2025-2030 年)內,複合年成長率將達到 5.54%。

成長將主要受汽車內裝需求的推動,而汽車內裝需求的增加又得益於電動車 (EV) 產量的成長,同時,注重觸感舒適性和隔熱性能的高階包裝需求也將促進市場成長。監管政策向水性及無揮發性有機化合物 (VOC) 化學品的轉變正在推動產品快速改進,尤其是在歐盟限制二異氰酸酯的使用以及中國收緊車內排放法規的情況下。到 2024 年,汽車應用將佔據植絨膠黏劑市場 42.56% 的最大佔有率,並將以 6.42% 的複合年成長率 (CAGR) 實現最快成長。亞太地區將繼續保持其地理領先地位,到 2024 年將佔據 51.84% 的市場佔有率,並預計到 2030 年將以 6.19% 的複合年成長率成長。同時,聚氨酯樹脂體系佔據主導地位,市場佔有率為 38.19%,而「其他」化學品將以 6.65% 的複合年成長率實現最高成長。

全球植絨膠黏劑市場趨勢及洞察

對塗層織物和高檔成品的需求激增

汽車和奢侈品製造商正加大植絨材料的使用力度,以彰顯卓越品質。車內零件,例如儀錶板、立柱和收納托盤,都能透過植絨工藝營造奢華觸感,提升握持感並消除異響。奢侈品包裝製造商也採用相同的技術,確保珠寶盒和手機殼從第一觸感就散發出高階質感。這種觸感上的提升有助於提高零售價格,並增強品牌差異化。這些因素共同造就了植絨黏合劑更廣泛、更穩定的需求基礎。

輕量化、低碳的汽車內裝零件推動了其普及應用

汽車製造商正用黏合複合材料面板替代笨重的緊固件,從而為每款車型減重。植絨黏合劑能夠牢固地固定薄塑膠和織物層壓板,並通過碰撞、振動和耐久性測試。重量減輕直接轉化為更長的電動車續航里程,這是消費者和監管機構密切關注的指標。組裝也從中受益,因為更少的卡扣和螺絲縮短了生產週期,並簡化了回收流程。隨著電氣化日益普及,輕量化概念正不斷推動群體解決方案成為工程領域的有力競爭者。

揮發性異氰酸酯/丙烯酸酯原料價格

黏合劑生產商依賴石油化學衍生物,其成本隨油價和供應鏈波動而波動。近期甲基丙烯酸供應過剩導致價格下跌12%,但幾週後樹脂生產商大幅漲價。與汽車原始設備製造商簽訂的長期固定價格合約限制了他們轉嫁額外費用的能力。規模較小的配方商尤其面臨風險,因為它們缺乏規模或多元化的產品組合來進行對沖。利潤率的不確定性抑制了企業在動盪時期進行積極資本投資的意願。

細分市場分析

聚氨酯在2024年佔據植絨膠黏劑市場38.19%的佔有率,主要得益於其與汽車基材的廣泛相容性和高耐熱性。然而,異氰酸酯的監管審查正在改變市場需求,其他樹脂類型的預期複合年成長率將達到6.65%。隨著非異氰酸酯植絨膠黏劑作為丙烯酸樹脂和環氧樹脂的替代品(其VOC含量更低且更易於操作)日益普及,預計其市場規模將超過傳統樹脂。漢高的生物基聚氨酯產品,其可再生成分含量高達71%,與標準配方相比,二氧化碳排放量減少了60%,顯示永續發展概念可以影響採購決策。

監管機構對二異氰酸酯產品提出了更嚴格的工人培訓和標籤要求,而原始設備製造商 (OEM) 則要求提供符合規定的替代品。為了應對這些要求,混煉商正在擴展其丙烯酸分散體和非異氰酸酯聚氨酯 (NIPU) 的化學配方,以滿足黏合性、柔韌性和耐熱循環性能方面的需求,同時確保二異氰酸酯含量不超過 0.1% 的閾值。能夠平衡合規性、性能和成本的供應商,隨著傳統產品面臨日益嚴格的限制,很可能會要求更高的利潤率。

區域分析

亞太地區預計到2024年將佔據全球植絨膠黏劑市場51.84%的佔有率,並在2030年之前以6.19%的複合年成長率成長。中國是該地區需求的核心,國內品牌和出口型組裝紛紛採用植絨內部裝潢建材,以提升產品感知品質並滿足低VOC排放法規的要求。西卡在遼寧和新加坡新建的工廠體現了其在本地產能方面的投資,旨在縮短前置作業時間並滿足新興的電池散熱需求。日本和韓國正在擴大其用於電子和汽車應用的低甲醛環氧基體系,並在材料科學領域保持領先地位,從而提升了產能。

北美市場緊隨其後,其消費市場成熟但對技術要求更高。原始設備製造商 (OEM) 正在實施嚴格的採購標準,以確保永續性和供應鏈透明度,從而推動水性分散液和生物基材料的快速普及。公共基礎設施和軍事採購管道為鐵路內飾和航太艙室配件等小眾植絨應用領域提供了支持,即使汽車產量低迷,也能維持基準需求。

歐洲兼具嚴格的監管和創新領先地位。歐洲的循環經濟行動計畫規定,到2027年,所有設備必須配備可拆卸電池,這為新型可剝離黏合劑創造了市場空間,這類黏合劑的絨毛在報廢後必須能夠徹底分離。例如,Power Adhesives公司最近推出了一種經認證的可生物分解熱熔膠系統,其生物基含量高達44%。南美洲和中東/非洲地區的市場規模總體上不大,但隨著供應鏈多元化,其重要性日益凸顯。巴西正在擴大其汽車組裝能,而這依賴於在地採購的植絨裝飾材料;海灣地區的石化產業整合也提供了具有競爭力的樹脂原料。儘管非洲市場仍處於起步階段,但其毗鄰高成長城市的消費性電子包裝製造商正積極投資非洲市場。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 對塗層織物和高檔成品的需求激增

- 汽車內裝零件重量更輕、碳排放量更低,正在推動其應用。

- 監管方向轉向水性/無揮發性有機化合物化學品

- 電動車電池組中的溫度控管襯裡

- 消費性電子產品包裝中的高級開箱美學

- 市場限制

- 揮發性異氰酸酯和丙烯酸酯原料價格

- 加強對溶劑排放的監管

- 來自雷射紋理和替代表面處理的競爭

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 依樹脂類型

- 丙烯酸纖維

- 聚氨酯

- 環氧樹脂

- 其他樹脂種類(醇酸樹脂、氰基丙烯酸酯樹脂等)

- 透過使用

- 車

- 紡織品

- 紙張/包裝

- 其他用途(印刷、圖形等)

- 按地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 東南亞國協

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- 3M

- Argent International

- Arkema

- Dow

- HB Fuller Company

- Henkel AG and Co. KGaA

- International Coatings

- Kissel+Wolf GmbH

- Nyatex

- Parker Hannifin

- Sika AG

- Stahl Holdings BV

- SwissFlock AG

- Toyochem Co. Ltd.

第7章 市場機會與未來展望

The Flock Adhesives Market size is estimated at USD 2.94 billion in 2025, and is expected to reach USD 3.85 billion by 2030, at a CAGR of 5.54% during the forecast period (2025-2030).

Growth is anchored in automotive interior demand, accelerated by rising electric-vehicle (EV) production, and reinforced by premium packaging requirements that emphasize soft-touch aesthetics and thermal functionality. Regulatory shifts toward water-based and VOC-free chemistries are prompting rapid product reformulation, especially as the European Union restricts diisocyanates and China tightens interior-emission limits. Automotive applications command the largest slice of the flock adhesives market at 42.56% in 2024 and also expand the fastest at 6.42% CAGR, underscoring the segment's dual role as volume base and innovation engine. Asia-Pacific retains geographic leadership with 51.84% share in 2024 and a 6.19% CAGR outlook through 2030, benefiting from concentrated automotive manufacturing footprints and expanding EV battery capacity. Meanwhile, polyurethane resin systems dominate with 38.19% share, yet "other" chemistries display the strongest 6.65% CAGR as formulators pivot toward acrylic, epoxy and non-isocyanate alternatives to stay ahead of incoming regulation.

Global Flock Adhesives Market Trends and Insights

Surging Demand for Coated Fabrics and Luxury Finish Products

Automotive and luxury-goods producers are stepping up use of flocked materials to signal elevated quality. Cabin parts such as dashboards, pillars and storage trays gain a plush feel that improves grip and cuts rattling noise. Premium packaging makers adopt the same technology so that jewelry boxes or smartphone cases feel exclusive from first touch. The tactile upgrade supports higher retail prices and strengthens brand differentiation. Together these factors translate into a wider, more stable demand base for flock adhesives.

Lightweight, Low-Carbon Vehicle Interior Parts Push Adoption

Car makers are substituting heavy fasteners with adhesive-bonded composite panels to shave grams from every model. Flock adhesives secure thin plastics and fabric laminates while meeting crash, vibration and durability tests. Mass reductions directly extend EV driving range, a metric closely watched by consumers and regulators. Assembly lines also benefit because fewer clips and screws cut cycle times and simplify recycling. As electrification spreads, the weight-saving argument keeps flock solutions on engineering shortlists.

Volatile Isocyanate and Acrylate Feedstock Prices

Adhesive makers rely on petrochemical derivatives whose costs whipsaw with oil and supply-chain shocks. Recent methacrylic-acid oversupply drove a 12% price drop, only for resin producers to impose sharp increases weeks later. Long fixed-price contracts with automotive OEMs limit the ability to pass surcharges through. Smaller formulators are especially exposed because they lack hedging scale and diversified portfolios. Margin uncertainty discourages bold capacity investments during turbulent periods.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Shift Toward Water-Based / VOC-Free Chemistries

- Flocked Thermal-Management Liners in Electric Vehicles Battery Packs

- Tightening Solvent-Emission Regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polyurethane captured 38.19% of flock adhesives market share in 2024, buoyed by broad compatibility with automotive substrates and strong thermal resilience. Yet regulatory scrutiny of isocyanates is shifting demand, evidenced by the 6.65% CAGR projected for "other" resin types. The flock adhesives market size for non-isocyanate chemistries is expected to outpace incumbents as acrylic and epoxy alternatives gain traction, driven by inherently lower VOCs and simplified handling. Henkel's bio-based polyurethane containing 71% renewable content demonstrates a 60% CO2 reduction versus standard formulas, signaling how sustainability narratives translate into purchasing criteria.

Regulators require worker training and stricter labelling for diisocyanate products, prompting OEMs to request compliant substitutes. Formulators respond by scaling acrylic dispersions and non-isocyanate polyurethane (NIPU) chemistries that meet adhesion, flexibility and heat-cycling needs without surpassing 0.1% diisocyanate thresholds. Suppliers able to balance compliance, performance and cost will command premium margins as legacy options face phased restriction.

The Flock Adhesives Market Report is Segmented by Resin Type (Acrylic, Polyurethane, Epoxy, Other Resin Types), Application (Automotive, Textiles, Paper and Packaging, Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 51.84% flock adhesives market share in 2024 and is set to grow at 6.19% CAGR through 2030. China anchors regional demand as domestic brands and export-oriented assemblers adopt flocked interiors to elevate perceived quality and meet low-VOC mandates. Sika's new Liaoning and Singapore plants illustrate local capacity investments aimed at shortening lead times and tailoring chemistries for emerging battery-thermal needs. Japan and South Korea complement volume with materials science leadership, scaling epoxy-based and low-formal-emission systems for electronics as well as autos.

North America follows with mature but technologically demanding consumption. OEMs enforce strict sourcing criteria on sustainability and supply-chain transparency, incentivizing rapid adoption of water dispersions and bio-based content. Public infrastructure and military procurement channels support niche flocked applications in rail interiors and aerospace cabin fittings, keeping baseline demand intact despite plateaued vehicle output.

Europe blends tight regulation with innovation leadership. The continent's Circular Economy Action Plan requires removable batteries in devices by 2027, spawning new debondable-adhesive niches where flock must cleanly separate at end-of-life. Companies like Power Adhesives recently introduced certified biodegradable hot-melt systems containing 44% bio-based content, a template likely to spread into flock formulations. South America, the Middle East and Africa collectively represent modest volumes but rising importance as supply chains diversify. Brazil expands automotive assembly capacity that relies on locally sourced flocked trims, while petrochemical integration in the Gulf provides competitive resin feedstock. African markets remain early-stage yet draw investment from consumer-electronics packagers seeking proximity to high-growth urban centers.

- 3M

- Argent International

- Arkema

- Dow

- H.B. Fuller Company

- Henkel AG and Co. KGaA

- International Coatings

- Kissel + Wolf GmbH

- Nyatex

- Parker Hannifin

- Sika AG

- Stahl Holdings B.V.

- SwissFlock AG

- Toyochem Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging demand for coated fabrics and luxury finish products

- 4.2.2 Lightweight, low-carbon vehicle interior parts push adoption

- 4.2.3 Regulatory shift toward water-based / VOC-free chemistries

- 4.2.4 Flocked thermal-management liners in electric vehicles battery packs

- 4.2.5 Premium unboxing aesthetics in consumer-electronics packaging

- 4.3 Market Restraints

- 4.3.1 Volatile isocyanate and acrylate feedstock prices

- 4.3.2 Tightening solvent-emission regulations

- 4.3.3 Competition from laser-texturing and alternative finishes

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Resin Type

- 5.1.1 Acrylic

- 5.1.2 Polyurethane

- 5.1.3 Epoxy

- 5.1.4 Other Resin Types (Alkyd, Cyanoacrylate, etc.)

- 5.2 By Application

- 5.2.1 Automotive

- 5.2.2 Textiles

- 5.2.3 Paper and Packaging

- 5.2.4 Other Applications (Printing and Graphics, etc.)

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 India

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 NORDIC Countries

- 5.3.3.8 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Argent International

- 6.4.3 Arkema

- 6.4.4 Dow

- 6.4.5 H.B. Fuller Company

- 6.4.6 Henkel AG and Co. KGaA

- 6.4.7 International Coatings

- 6.4.8 Kissel + Wolf GmbH

- 6.4.9 Nyatex

- 6.4.10 Parker Hannifin

- 6.4.11 Sika AG

- 6.4.12 Stahl Holdings B.V.

- 6.4.13 SwissFlock AG

- 6.4.14 Toyochem Co. Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment