|

市場調查報告書

商品編碼

1851562

可再生能源:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)Renewable Energy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

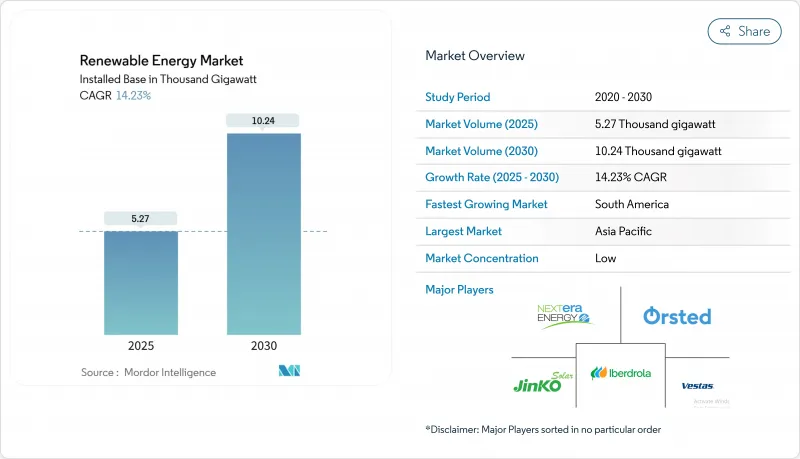

預計可再生能源市場規模將從 2025 年的 5,080 吉瓦擴大到 2030 年的 7,040 吉瓦,在預測期(2025-2030 年)內實現 8.94% 的複合年成長率。

技術成本暴跌、政府扶持政策以及企業需求不斷成長,共同推動了這項擴張。 2024年,太陽能光電發電將引領可再生能源市場,佔總裝置容量的42%,預計到2030年將以13%的複合年成長率成長。儘管公共產業事業規模的計劃仍然是成長的支柱,但隨著企業對沖石化燃料價格波動風險並加強永續性目標,工商業(C&I)光電發電專案也正在加速發展。亞太地區佔最大佔有率,但南美洲的成長速度最快,這得益於有利於投資的改革以及豐富的風能和太陽能資源。

全球可再生能源市場趨勢與洞察

在北美和歐洲,根據購電協議建造的大型發電廠正在加速。

企業購電協議 (CPPA) 如今已成為可再生能源採購的核心,科技公司和製造商需要為其人工智慧、雲端運算和重工業營運獲取綠能。例如,ENGIE 已簽署 85 份 CPPA,涵蓋 4.3 吉瓦的裝置容量,有效期至 2024 年,相當於 136 太瓦時的電力供應。自願性企業購電協議已為美國近一半的新建電力項目提供支持,為開發商提供可觀的收入並降低資本成本。靈活的「虛擬」購電協議允許買家在無需實際交割的情況下對沖價格風險,但不斷上漲的電網電價和複雜的合約仍然是中小企業面臨的障礙。

對超大規模資料中心的需求推動了北歐和愛爾蘭的太陽能和風能採購。

預計資料中心用電需求將從2024年的415太瓦時成長到2030年的945太瓦時。業者選擇北歐國家和愛爾蘭,是因為這些地區氣候涼爽且再生能源豐富。 2024年5月,微軟簽署了一項長期電力採購協議(CPPA),將從愛爾蘭的萊納利亞風電場採購30兆瓦的風力發電。工作負載轉移使資料中心能夠作為靈活負載吸收多餘的風力發電,從而減少棄風棄光,並提高可再生能源市場的併網容量。

美國ERCOT和中國內蒙古的電網擁塞和限流風險

到2024年,ERCOT的太陽能和風能棄光量將增加29%,達到340萬兆瓦時。德克薩斯州的資源匱乏和輸電線路不暢是限制因素,這與中國內蒙古的情況類似,後者也面臨類似的限制,阻礙了可再生能源市場的發展。電池儲能和電網增強裝置是可行的解決方案,但部署速度落後於新增裝置容量,損害了開發商的利潤,並阻礙了未來的計劃。

細分市場分析

到2024年,太陽能光電發電將佔總發電量的42%,到2030年將以13%的複合年成長率成長。在許多國家,公用事業規模的太陽能光電發電目前是最經濟的新型發電方式。隨著鈣鈦礦-矽串聯電池的實驗室效率達到31.6%,預計2030年,可再生能源市場將成長80%。然而,組件供應過剩正在擠壓生產商的淨利率,促使他們轉向在美國和歐洲等地進行國內生產,以減少對中國進口的依賴。

中國的沙漠太陽能發電廠和印度的超大型太陽能發電園區等大型計畫展現了規模經濟效應,使其成本與傳統電力持平。隨著第三方所有權和虛擬淨計量技術的引入,住宅屋頂太陽能發電的部署也在不斷改進,降低了家庭用戶的前期成本。這些趨勢正在鞏固太陽能作為可再生能源市場容量重要貢獻者的地位。

陸上和離岸風電使可再生能源市場更加多元化,並以每年約8%的速度成長。離岸風力發電渦輪機的額定功率現已超過18兆瓦,提高了單位面積的能源捕獲量。然而,通膨和供應鏈壓力導致成本高於競標水平,迫使購電協議重新談判甚至終止。預計到2025年,離岸風力發電可再生能源市場規模將翻倍,但營運商正在尋求更可預測的政策來降低資本配置風險。

歐洲強制回收舊葉片和印度限制本地化含量的政策表明,如果供應鏈放緩,這些政策會如何推高成本。來自亞洲低成本風力渦輪機的競爭正迫使西方製造商專注於服務合約、數位最佳化和模組化設計,以保持市場競爭力。

可再生能源市場報告按技術(太陽能、風力發電、水力發電、生質能源、地熱能和海洋能)、終端用戶(公共產業、商業和工業以及住宅用戶)以及地區(北美、亞太、歐洲、南美以及中東和非洲)進行細分。市場規模和預測以裝置容量(吉瓦)為單位。

區域分析

亞太地區將佔全球可再生能源市場裝置容量的55%,其中中國在2024年將佔全球新增裝置容量的64%。由於獎勵,印度的可再生能源市場規模到2030年將成長四倍,達到62吉瓦,而東南亞國家則致力於解決儲能和電網瓶頸問題。 2024年,外國直接投資將超過580億美元,凸顯了投資者對再生能源市場的信心,儘管各國政策不盡相同。

南美洲將迎來最快成長,複合年成長率將達16%。巴西預計2024年太陽能和風能裝置容量將有所成長,但不斷上漲的輸電成本和授權延誤令投資人望而卻步。智利和哥倫比亞也在擴大商業太陽能發電工程,這得益於現貨市場流動性的增加。

北美正受惠於美國《通膨降低法案》中的稅額扣抵。到2025年,太陽能發電裝置容量將成長35%,但電網擁塞正在運作計劃的併網進程。在德克薩斯州和中西部地區,企業購電協議(PPA)正成為將資料中心需求與豐富的風能和太陽能資源相匹配的主要採購方式。

歐洲透過「再生能源電力計畫」(REPowerEU)設定目標,到2030年實現12吉瓦的再生能源裝置容量。儘管面臨電網瓶頸,西班牙仍在努力將其可再生能源裝置容量翻番;義大利則在試行推行容量市場改革,以獎勵電力彈性。歐洲風電產業面臨中國低成本製造商的供應鏈競爭,但授權規則的調整正在縮短前置作業時間。

中東和北非地區在開發以廉價太陽能為動力的綠色氫能方面取得了進展。沙烏地阿拉伯已將3.7吉瓦的太陽能發電計畫列入2024年競標的候選名單,其中包括2吉瓦的薩達維(Al Saadawi)計劃。埃及的本班(Benban)綜合設施和阿拉伯聯合大公國的達夫拉(Al Dhafra)工廠是重要的建設項目,旨在為國家電網供氫,並成為未來的氫氣出口中心。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 2024年可再生能源結構

- 市場促進因素

- 企業購電協議加速了北美和歐洲的電力擴張。

- 超大規模資料中心的需求推動了北歐和愛爾蘭的太陽能和風能採購。

- 吉瓦級綠色氫能管道將推動中東、北非和澳洲的產能成長

- 歐盟的「REPowerEU」快速核准系統將南歐陸上風電計畫的前置作業時間縮短至12個月以內。

- 市場限制

- 美國ERCOT和中國內蒙古的電網擁塞和停電風險

- 德國和法國在處理廢棄風力發電機葉片方面面臨日益上漲的廢棄物成本。

- 長期儲存設施不足減緩了東南亞再生能源的推廣。

- 在地採購政策推動印度和巴西離岸風力發電投資

- 供應鏈分析

- 監理展望

- 技術展望

- 最新進展

- 波特五力模型

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 透過技術

- 太陽能(光伏和聚光太陽能)

- 風力發電(陸上和海上)

- 水力發電(小型、大型、抽水蓄能)

- 生質能源

- 地熱

- 海洋能源(潮汐和波浪)

- 最終用戶

- 公用事業

- 商業和工業

- 住房

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 德國

- 法國

- 西班牙

- 北歐國家

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 馬來西亞

- 泰國

- 印尼

- 越南

- 澳洲

- 亞太其他地區

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 南美洲其他地區

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 埃及

- 其他中東和非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略性措施(併購、合資、資金籌措、購電協議)

- 市場佔有率分析(主要企業的市場排名/佔有率)

- 公司簡介

- EPC開發商/營運商/業主

- NextEra Energy, Inc.

- Orsted A/S

- Iberdrola, SA

- EDF Renewables(EDF SA)

- Duke Energy Corporation

- Berkshire Hathaway Energy

- Acciona Energia SA

- Engie SA

- China Three Gorges Corporation

- Enel Green Power SpA

- Statkraft AS

- Pattern Energy Group

- Invenergy LLC

- RWE Renewables GmbH

- ACWA Power

- EDP Renovaveis SA

- Brookfield Renewable Partners LP

- ReNew Energy Global PLC

- Scatec ASA

- 設備供應商

- First Solar, Inc.

- Vestas Wind Systems A/S

- Siemens Gamesa Renewable Energy SA

- GE Vernova(General Electric)

- JinkoSolar Holding Co. Ltd.

- Canadian Solar Inc.

- Longi Green Energy Technology Co., Ltd.

- Goldwind Science & Technology Co., Ltd.

- Trina Solar Co., Ltd.

- Enphase Energy, Inc.

- Sungrow Power Supply Co., Ltd.

- Mitsubishi Power, Ltd.

- Nordex SE

- MHI Vestas Offshore Wind A/S

- Shanghai Electric Group Co., Ltd.

- Hitachi Energy Ltd.

- ABB Ltd.

- Climeon AB

- Pelamis Wave Power Ltd.(in Administration)

- Ocean Power Technologies, Inc.

- EPC開發商/營運商/業主

第7章 市場機會與未來展望

The Renewable Energy Market size in terms of installed base is expected to grow from 5.08 Thousand gigawatt in 2025 to 7.04 Thousand gigawatt by 2030, at a CAGR of 8.94% during the forecast period (2025-2030).

A sharp fall in technology costs, supportive government policies, and rising corporate demand underpin this expansion. Solar power led the renewable energy market in 2024 with 42% of capacity and is forecast to grow at a 13% CAGR through 2030. Utility-scale projects remain the backbone of growth, but commercial and industrial (C&I) installations are gaining momentum as companies hedge against volatile fossil-fuel prices and tighten sustainability targets. Asia-Pacific holds the largest regional share, while South America is advancing the fastest on the back of pro-investment reforms and plentiful wind and solar resources.

Global Renewable Energy Market Trends and Insights

Corporate power-purchase agreements accelerating utility-scale builds in North America & Europe

Corporate power-purchase agreements (CPPAs) are now central to renewable energy procurement as tech firms and manufacturers lock in clean electricity for AI, cloud, and heavy-industry operations. An example is ENGIE's 85 CPPAs covering 4.3 GW signed in 2024, equal to 136 TWh of supply. Voluntary corporate offtake deals already support around half of new US utility-scale projects, providing developers with bankable revenue and lowering the cost of capital. Flexible "virtual" PPAs let buyers hedge price risk without physical delivery, although rising grid tariffs and complex contracting still deter smaller firms.

Hyperscale data-centre demand boosting solar-wind procurement in the Nordics & Ireland

Data-centre electricity demand is projected to reach 945 TWh by 2030, up from 415 TWh in 2024. Operators gravitate to the Nordics and Ireland for cool climates and abundant renewables. In May 2024 Microsoft signed a long-term CPPA that adds 30 MW of wind power from Lenalea Wind Farm in Ireland sse.com. Workload-shifting lets data centres act as flexible loads that absorb surplus wind power, reducing curtailment and increasing the renewable energy market's integration capability.

Grid congestion & curtailment risks in ERCOT (US) and Inner Mongolia (CN)

Solar and wind curtailment in ERCOT rose 29% in 2024 to 3.4 million MWh. West Texas resources and sparse transmission create bottlenecks that mirror China's Inner Mongolia, where similar constraints slow the renewable energy market. Battery storage and grid-enhancing devices are viable fixes, but deployment lags capacity additions, eroding developer revenue and deterring future projects.

Other drivers and restraints analyzed in the detailed report include:

- Green-hydrogen gigawatt pipelines driving capacity additions in MENA & Australia

- EU 'REPowerEU' fast-track permitting cutting onshore-wind lead times (<12 months) in Southern Europe

- End-of-life blade-waste regulations raising costs in Germany & France

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solar commanded 42% of capacity in 2024 and will rise at 13% CAGR to 2030. Utility-scale solar is now the cheapest new generation option in many countries. The renewable energy market size for solar installations is forecast to expand by 80% by 2030, aided by perovskite-silicon tandem cells achieving 31.6% lab efficiencies. Module oversupply, however, is squeezing producer margins, prompting diversification into domestic manufacturing in the United States and Europe to trim reliance on Chinese imports.

Massive installations such as China's desert solar bases and India's ultramega parks illustrate economies of scale that drive cost parity with conventional power. Residential rooftop uptake is also improving through third-party ownership and virtual net metering, easing upfront costs for households. These trends cement solar's role as the leading contributor to renewable energy market capacity.

Onshore and offshore wind add diversity to the renewable energy market, growing at roughly 8% annually. Turbine ratings now exceed 18 MW offshore, lifting energy capture per foundation. Yet inflation and supply-chain stress lifted costs above bid levels, forcing renegotiation and, in some cases, cancellation of power-purchase agreements. The renewable energy market size for offshore wind is forecast to double by 2025, but developers seek greater policy predictability to de-risk capital allocation.

End-of-life blade recycling mandates in Europe and local-content rules in India illustrate how policy can inflate costs if supply chains lag. Competition from low-cost Asian turbines is pushing Western manufacturers to focus on service contracts, digital optimisation, and modular designs to retain market presence.

The Renewable Energy Market Report is Segmented by Technology (Solar Energy, Wind Energy, Hydropower, Bioenergy, Geothermal, and Ocean Energy), End-User (Utility, Commercial and Industrial, and Residential), and Geography (North America, Asia-Pacific, Europe, South America, and Middle East and Africa). The Market Sizes and Forecasts are Provided in Terms of Installed Capacity (GW).

Geography Analysis

Asia-Pacific owns 55% of the renewable energy market capacity, led by China's 64% share of new global additions in 2024. India's renewable energy market size is set to quadruple to 62 GW by 2030 under incentive schemes, while Southeast Asian nations tackle storage and grid constraints. Foreign direct investment topped USD 58 billion in 2024, underlining investor confidence despite policy variability.

South America posts the fastest growth at 16% CAGR. Brazil recorded solar and wind additions in 2024, though rising transmission charges and permitting delays temper investor enthusiasm. Chile and Colombia are also scaling up merchant solar projects, helped by growing spot-market liquidity.

North America benefits from US tax credits within the Inflation Reduction Act. Solar capacity will climb 35% by 2025, though grid congestion slows project energisation. Corporate PPAs now dominate procurement in Texas and the Midwest, aligning data-centre needs with abundant wind and solar resources.

Europe is targeting 1,200 GW of renewables by 2030 through REPowerEU. Spain doubled its renewable capacity despite grid bottlenecks, and Italy is piloting capacity-market reforms that reward flexibility. Supply-chain competition with low-cost Chinese manufacturers challenges the European wind sector, though revamped permitting rules are shortening lead times.

MENA leverages cheap solar irradiation for green hydrogen. Saudi Arabia shortlisted 3.7 GW of solar in its 2024 tender round, including the 2 GW Al Sadawi project. Egypt's Benban complex and the UAE's Al Dhafra plant showcase large-scale builds that feed domestic grids and future hydrogen export hubs.

- EPC Developers / Operators / Owners

- Equipment Suppliers

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Renewable Energy Mix, 2024

- 4.3 Market Drivers

- 4.3.1 Corporate Power-Purchase Agreements Accelerating Utility-scale Builds in North America & Europe

- 4.3.2 Hyperscale Data-Centre Demand Boosting Solar-Wind Procurement in the Nordics & Ireland

- 4.3.3 Green-Hydrogen Gigawatt Pipelines Driving Capacity Additions in MENA & Australia

- 4.3.4 EU 'REPowerEU' Fast-Track Permitting Cutting Onshore-Wind Lead-Times (<12 Months) in Southern Europe

- 4.4 Market Restraints

- 4.4.1 Grid Congestion & Curtailment Risks in ERCOT (US) and Inner Mongolia (CN)

- 4.4.2 End-of-Life Blade Waste Regulations Raising Costs in Germany & France

- 4.4.3 Lack of Long-Duration Storage Slowing High VRE Penetration in SE-Asia

- 4.4.4 Local-Content Mandates Inflating Offshore-Wind CAPEX in India & Brazil

- 4.5 Supply-Chain Analysis

- 4.6 Regulatory Outlook

- 4.7 Technological Outlook

- 4.8 Recent Trends & Developments

- 4.9 Porter's Five Forces

- 4.9.1 Bargaining Power of Suppliers

- 4.9.2 Bargaining Power of Consumers

- 4.9.3 Threat of New Entrants

- 4.9.4 Threat of Substitute Products & Services

- 4.9.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Technology

- 5.1.1 Solar Energy (PV and CSP)

- 5.1.2 Wind Energy (Onshore and Offshore)

- 5.1.3 Hydropower (Small, Large, PSH)

- 5.1.4 Bioenergy

- 5.1.5 Geothermal

- 5.1.6 Ocean Energy (Tidal and Wave)

- 5.2 By End-User

- 5.2.1 Utility

- 5.2.2 Commercial and Industrial

- 5.2.3 Residential

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 Germany

- 5.3.2.3 France

- 5.3.2.4 Spain

- 5.3.2.5 Nordic Countries

- 5.3.2.6 Russia

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Malaysia

- 5.3.3.6 Thailand

- 5.3.3.7 Indonesia

- 5.3.3.8 Vietnam

- 5.3.3.9 Australia

- 5.3.3.10 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 South Africa

- 5.3.5.4 Egypt

- 5.3.5.5 Rest of Middle East and Africa

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, JVs, Funding, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Products & Services, Recent Developments)

- 6.4.1 EPC Developers / Operators / Owners

- 6.4.1.1 NextEra Energy, Inc.

- 6.4.1.2 Orsted A/S

- 6.4.1.3 Iberdrola, S.A.

- 6.4.1.4 EDF Renewables (EDF S.A.)

- 6.4.1.5 Duke Energy Corporation

- 6.4.1.6 Berkshire Hathaway Energy

- 6.4.1.7 Acciona Energia S.A.

- 6.4.1.8 Engie S.A.

- 6.4.1.9 China Three Gorges Corporation

- 6.4.1.10 Enel Green Power S.p.A.

- 6.4.1.11 Statkraft A.S.

- 6.4.1.12 Pattern Energy Group

- 6.4.1.13 Invenergy LLC

- 6.4.1.14 RWE Renewables GmbH

- 6.4.1.15 ACWA Power

- 6.4.1.16 EDP Renovaveis S.A.

- 6.4.1.17 Brookfield Renewable Partners L.P.

- 6.4.1.18 ReNew Energy Global PLC

- 6.4.1.19 Scatec ASA

- 6.4.2 Equipment Suppliers

- 6.4.2.1 First Solar, Inc.

- 6.4.2.2 Vestas Wind Systems A/S

- 6.4.2.3 Siemens Gamesa Renewable Energy S.A.

- 6.4.2.4 GE Vernova (General Electric)

- 6.4.2.5 JinkoSolar Holding Co. Ltd.

- 6.4.2.6 Canadian Solar Inc.

- 6.4.2.7 Longi Green Energy Technology Co., Ltd.

- 6.4.2.8 Goldwind Science & Technology Co., Ltd.

- 6.4.2.9 Trina Solar Co., Ltd.

- 6.4.2.10 Enphase Energy, Inc.

- 6.4.2.11 Sungrow Power Supply Co., Ltd.

- 6.4.2.12 Mitsubishi Power, Ltd.

- 6.4.2.13 Nordex SE

- 6.4.2.14 MHI Vestas Offshore Wind A/S

- 6.4.2.15 Shanghai Electric Group Co., Ltd.

- 6.4.2.16 Hitachi Energy Ltd.

- 6.4.2.17 ABB Ltd.

- 6.4.2.18 Climeon AB

- 6.4.2.19 Pelamis Wave Power Ltd. (in Administration)

- 6.4.2.20 Ocean Power Technologies, Inc.

- 6.4.1 EPC Developers / Operators / Owners

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

農業可再生能源:生質燃料、太陽能發電廠和永續農業實踐的全球市場—按應用、產品和地區分類的分析和預測(2025-2035 年)

農業可再生能源:生質燃料、太陽能發電廠和永續農業實踐的全球市場—按應用、產品和地區分類的分析和預測(2025-2035 年) 2026年全球可再生能源市場報告2026年全球多元能源系統市場報告2026年全球太陽能燃料市場報告

2026年全球可再生能源市場報告2026年全球多元能源系統市場報告2026年全球太陽能燃料市場報告 風電場變電站市場按組件類型、配置類型、連接類型、電壓等級、最終用戶和安裝類型分類,全球預測(2026-2032年)全球節能設備市場:機會與策略展望(至2034年)

風電場變電站市場按組件類型、配置類型、連接類型、電壓等級、最終用戶和安裝類型分類,全球預測(2026-2032年)全球節能設備市場:機會與策略展望(至2034年) 節能微控制器市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、最終用戶、功能、安裝類型、解決方案分類

節能微控制器市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、最終用戶、功能、安裝類型、解決方案分類 中國可再生能源:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)新加坡可再生能源:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)美國可再生能源:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

中國可再生能源:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)新加坡可再生能源:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)美國可再生能源:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)