|

市場調查報告書

商品編碼

1851526

增稠劑:市佔率分析、產業趨勢、統計、成長預測(2025-2030)Tackifier - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

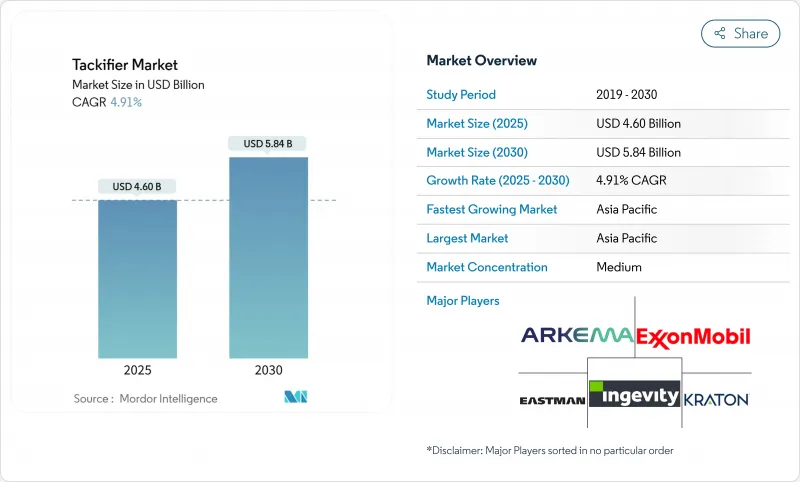

2025 年增黏劑市場規模預估為 46 億美元,預計到 2030 年將達到 58.4 億美元,預測期(2025-2030 年)複合年成長率為 4.91%。

包裝和衛生用品領域對壓敏黏著劑和熱熔膠的持續需求支撐著當前的收入,而電動車電池組裝、特殊建築和低VOC食品包裝等領域的日益廣泛應用則開闢了未來的成長途徑。亞太地區基礎設施的快速投資、北美和歐洲日益嚴格的排放法規以及品牌所有者對生物基材料的承諾,都在推動市場發展。超低VOC等級、耐高溫烴類樹脂和松香衍生分散體等創新技術,使供應商能夠在不犧牲黏合性能的前提下,滿足日益嚴格的食品接觸和環境法規要求。技術朝向無增黏劑反應型熱熔膠和動態聚氨酯化學的轉變,以及原油價格的波動,仍然是可能降低盈利但同時也促進研發多元化的主要風險。

全球增粘劑市場趨勢與洞察

包裝和衛生用品行業對熱熔膠和壓敏膠的需求不斷成長

電子商務小包裹量和高階衛生用品的需求持續成長,推動了熱熔膠和壓敏黏著劑的消費量增加。增粘樹脂為這些高速生產線提供了至關重要的初始黏合力和持久剝離強度。 HB Fuller 的 Full-Care 6217 表明,透過配方調整,可以在提高脫模性能的同時,減少 20% 的膠合劑用量。可生物分解的松香樹脂在紙基膠帶中越來越受歡迎,這與品牌的永續性承諾相契合。女性墊片的吸濕排汗性能促使供應商尋求能夠耐受高濕度並減少異味的膠合劑。埃克森美孚的 Escorez 產品組合表明,透明包裝薄膜需要淺色、耐熱的膠粘劑,因為透明度至關重要。這些需求共同表明,到 2030 年,增黏劑市場將與消費品產業的成長緊密相連。

亞太地區城市基礎建設熱潮帶動建築黏合劑需求

中國、印度和東南亞國協的公共交通線、機場和經濟適用房計畫支撐著對地板材料、屋頂和板材黏合劑的長期需求。濕固化系統在熱帶潮濕環境下表現優異,其對增粘樹脂早期潤濕的依賴推動了銷售量。憑藉這些產品,Master Builders Solutions的目標是到2028年在印度實現50億印度盧比的銷售額。建築規範鼓勵使用輕質複合材料建築幕牆和夾芯板,這拓寬了具有熱穩定性的合成烴基黏合劑的性能範圍。中國膠帶協會報告稱,建築膠帶的銷售成長顯著,凸顯了基礎設施和耐用消費品產業的交叉作用。這些投資鞏固了公司在亞太地區增黏劑市場成長的領先地位。

石油和原料價格的波動對烴類樹脂利潤率帶來壓力。

烴類增黏劑生產線受原油價格波動的影響,因為C5和C9餾分是石腦油裂解產物。價格上漲會損害利潤率,抑制資本投資,並限制研發預算。 2021年歐洲物流危機期間,黏合劑需求下降了5%,凸顯了其對供應中斷的脆弱性。特種化學品規劃人員目前正專注於避險和靈活的定價措施,但小型獨立樹脂生產商仍面臨風險。石油基樹脂佔市場佔有率的65.45%,價格波動加劇可能重塑競爭格局,並促使買家轉向生物基樹脂。

細分市場分析

2024年,石油樹脂將佔銷售額的65.45%,憑藉其可靠的品質和性價比,為增黏劑市場提供支撐。 C5-C9混合樹脂可確保汽車內裝和工業膠帶的黏性和耐熱性。同時,隨著加工商為獲得環保標章和認證可堆肥包裝袋而追求可再生成分,松香樹脂的年複合成長率將達到5.15%。由於生質燃料精煉商也使用相同的原料,妥爾油松香的供應緊張,預計到2030年將出現8%的供不應求。成功的供應商正在烴類和松香體系之間進行多元化配置,以對沖價格波動風險,同時實現品牌永續性目標。萜烯樹脂雖然應用範圍較小,但其極性優勢可提高對天然橡膠和彈性體基材的黏合力。增粘劑市場受益於此混合原料策略,使配方師能夠平衡成本、性能和環保成分。

石油生產商尋求長期合約以維持穩定,但當客戶強調生物基含量時,此類合約會降低靈活性。另一方面,松香創新者正利用氫化改質來滿足透明包裝薄膜所需的顏色和氣味標準。成本波動與永續性法規之間的相互作用將決定未來十年的原料策略。

2024年,固態切片和顆粒佔總銷售額的81.56%,這主要歸功於加工商對其易於供應、粉塵含量低以及與現有熱熔設備的兼容性的青睞。它們對於紙箱封口和木工生產線至關重要,因為它們能夠承受超過150°C的熔化峰值而不會發生氧化劣化。樹脂分散體將以5.32%的複合年成長率 (CAGR) 實現成長,推動水性黏合劑在標籤和軟性複合材料領域的應用。這些分散體能夠減少VOC排放並簡化生產線清潔。液體型產品用於需要常溫黏度的色帶塗層和溶劑體系,但由於溶劑成本的降低,其市場佔有率已停滯不前。對於製造商而言,提供多種形式的產品組合可以提高轉換門檻,並確保在需要客製化黏度特性的專業終端應用領域佔據市場佔有率。

區域分析

亞太地區預計到2024年將佔全球收入的36.25%,複合年成長率達5.50%,這主要得益於基礎設施投資、商業的蓬勃發展以及一次性尿布使用量的增加。中國膠帶產量將實現強勁的個位數成長,這與建築和電子產業對差異化黏合劑的需求相符。印度建築化學品市場預計到2025年將達到2,000億盧比,凸顯了該地區對能夠加速建築週期的黏合劑的需求。政府鼓勵可生物分解包裝的政策將提振對松香基材料的需求,而不穩定的妥爾油供應則給當地複合材料生產商帶來了確保原料穩定供應的挑戰。

北美在創新方面保持主導,嚴格的揮發性有機化合物 (VOC) 法規和美國食品藥物管理局 (FDA) 的食品接觸規則推動了超低氣味等級產品的採購。美國和墨西哥汽車電氣化程度的不斷提高,推動了對耐高溫合成樹脂的需求,以保護電池組。歐洲專注於循環經濟目標和 REACH 法規合規,儘管成本不斷上升,但仍在轉向生物基增黏劑。歐洲建築黏合劑市場預計在 2025 年復甦,這表明監管方面的阻力可以與永續的替代機會並存。

南美洲和中東及非洲地區雖然規模較小,但憑藉著物流走廊、消費品成長以及製造業領域的外國直接投資,蘊藏著巨大的發展潛力。聖戈班斥資10.25億美元收購福斯羅克,鞏固了其在海灣合作理事會國家和印度的建築膠粘劑配銷通路,這正是全球企業對新興需求中心進行戰略性押注的例證。儘管外匯波動和當地樹脂產能有限會限制短期成長,但逐步推進的工業化將為未來十年增黏劑的市場滲透奠定基礎。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 包裝和衛生用品行業對熱熔膠和壓敏膠的需求不斷成長。

- 亞太地區城市基礎建設熱潮帶動建築黏合劑需求

- 電子商務的成長將加速膠帶和標籤的消耗。

- 超低VOC、食品接觸相容的樹脂等級將成為首選。

- 電動車電池和輕量化汽車組件需要高耐熱黏合劑

- 市場限制

- 石油原料價格波動會損害烴類樹脂的利潤率。

- 無增黏劑反應型熱熔體系的出現。

- 永續性認證限制了妥爾油和松香的供應。

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 按原料

- 松香樹脂

- 石油樹脂

- 萜烯樹脂

- 按形式

- 固體的

- 液體

- 樹脂分散體

- 按類型

- 合成

- 自然的

- 透過使用

- 膠帶和標籤

- 組裝

- 書籍裝訂

- 鞋類、皮革、橡膠

- 其他用途

- 按最終用戶行業分類

- 包裹

- 建築/施工

- 車

- 不織布

- 鞋類

- 其他終端用戶產業

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Arakawa Chemical Industries, Ltd.

- Arkema

- Eastman Chemical Company

- Exxon Mobil Corporation

- Henkel AG & Co. KGaA

- Ingevity Corporation

- Kolon Industries, Inc.

- Kraton Corporation

- Lawter, a Harima Chemicals, Inc. Company

- Natrochem, Inc.

- SI Group, Inc.

- Teckrez, Inc.

- TWC Group

- Yasuhara Chemical Co., Ltd.

第7章 市場機會與未來展望

The Tackifier Market size is estimated at USD 4.60 billion in 2025, and is expected to reach USD 5.84 billion by 2030, at a CAGR of 4.91% during the forecast period (2025-2030).

Sustained demand for pressure-sensitive and hot-melt adhesives in packaging and hygiene products anchors current revenue, while widening use in electric vehicle battery assembly, specialty construction, and low-VOC food packaging broadens future growth pathways. Rapid infrastructure spending across Asia Pacific, stringent emission norms in North America and Europe, and brand owner commitments to bio-based materials collectively reinforce market momentum. Innovation in ultra-low-VOC grades, high-heat hydrocarbon resins, and rosin-derived dispersions allows suppliers to address tightening food-contact and environmental regulations without sacrificing bond performance. Technology shifts toward tackifier-free reactive hot melts and dynamic polyurethane chemistries, alongside crude-oil price swings, remain overarching risks that could temper profitability yet also spur R&D diversification.

Global Tackifier Market Trends and Insights

Rising Demand for Hot-Melt & PSA Adhesives in Packaging and Hygiene

E-commerce parcel volume, combined with premium hygiene products, continues to lift hot-melt and pressure-sensitive adhesive consumption. Tackifier resins provide the critical early-grab and sustained peel strength these fast-running production lines require. H.B. Fuller's Full-Care 6217 shows how formulation tweaks can cut adhesive usage by 20% while improving peel, a direct cost-and-performance benefit to diaper makers. Biodegradable rosin resins gain traction in paper-backed tapes, aligning with brand sustainability pledges. Moisture-management features in feminine care pads push suppliers toward tackifiers that tolerate high humidity yet keep odor low. ExxonMobil's Escorez portfolio illustrates the push for light-color, thermally stable grades serving transparent packaging films where clarity is paramount. These combined needs ensure that the tackifier market remains firmly linked to consumer goods growth through 2030.

Urban Infrastructure Boom in APAC Spurring Construction Adhesives

Mass transit lines, airports, and affordable housing programs across China, India, and ASEAN nations underpin long-run demand for flooring, roofing, and panel bonding adhesives. Moisture-cure systems excel in tropical humidity, and their reliance on tackifier resins for initial wet-out drives incremental volumes. Master Builders Solutions targets INR 500 crore turnover in India by 2028 on the strength of such products. Building codes pushing lightweight composite facades and sandwich panels widen the performance window for synthetic hydrocarbon tackifiers that deliver thermal stability. The China Adhesive Tape Council reports volume gains in building tapes, highlighting how infrastructure and consumer durables intersect. These investments sustain APAC's leadership in tackifier market growth.

Petroleum-Feedstock Price Volatility Hurting Hydrocarbon Resin Margins

Hydrocarbon tackifier lines mirror crude-oil price swings because C5 and C9 streams are co-products of naphtha crackers. Spikes erode margins, stall expansion CAPEX, and constrain R&D budgets. During the 2021 European logistics crunch, adhesive demand slipped 5%, underscoring vulnerability to supply disruptions. Specialty chemical planners now emphasize hedging and agile pricing tools, yet smaller independent resin houses remain exposed. With petroleum resins occupying 65.45% share, extended volatility could redirect buyers toward bio-based grades, reshaping the competitive landscape.

Other drivers and restraints analyzed in the detailed report include:

- E-commerce Growth Accelerating Tape & Label Consumption

- Ultra-Low-VOC, Food-Contact Compliant Resin Grades Gain Preference

- Emergence of Tackifier-Free Reactive Hot-Melt Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Petroleum resins delivered 65.45% of 2024 revenue, anchoring the tackifier market with a reliable quality and price-performance balance. C5-C9 hybrids secure tack and heat resistance for automotive interiors and industrial tapes. Meanwhile, rosin grades expand at a 5.15% CAGR as converters pursue renewable content for eco-labels and certified compostable pouches. Tall-oil rosin supply tightens because biofuel refiners draw from the same feed pool, leading to a projected 8% deficit by 2030. Successful suppliers diversify between hydrocarbon and rosin lines, hedging price swings while meeting brand sustainability targets. Terpene resins, though niche, add polarity advantages that improve adhesion to natural rubber and elastic substrates. The tackifier market benefits from this blended feedstock approach, ensuring formulators can balance cost, performance, and green content.

Petroleum producers aim to lock in long-term contracts to preserve stability, but such commitments reduce flexibility when customers pivot to bio-content mandates. Conversely, rosin innovators exploit hydrogenated modifications to match color and odor standards demanded in transparent packaging films. The interplay between cost volatility and sustainability legislation defines feedstock strategy for the decade ahead.

Solid chips and pellets held 81.56% of 2024 sales because converters prefer easy feeding, low dust, and compatibility with established hot-melt equipment. They withstand melting peaks above 150 °C without oxidative degradation, making them indispensable for carton-sealing and woodworking lines. Resin dispersions outpace with 5.32% CAGR, meeting waterborne adhesive growth in labels and flexible laminations. These dispersions reduce VOC output and simplify line cleanup, critical under tighter plant-emission audits. Liquid forms serve ribbon-coating and solvent systems where room-temperature viscosity is needed, yet their market share lags amid solvent abatement costs. For manufacturers, offering multi-form portfolios elevates switching barriers and secures share in specialty end uses that demand customized viscosity profiles.

The Tackifier Market Report is Segmented by Feedstock (Rosin Resins, Petroleum Resins, Terpene Resins), Form (Solid, Liquid, Resin Dispersion), Type (Synthetic, Natural), Application (Tapes and Labels, Assembly, Bookbinding, and More), End-User Industry (Packaging, Building and Construction, and More), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific commanded 36.25% of 2024 revenue and rises at 5.50% CAGR, underpinned by infrastructure investment, surging e-commerce, and expanding diaper penetration. China's adhesive tape production grew at high single digits, aligned with construction and electronics verticals that specify differentiated tackifiers. India's construction chemicals market, sized at INR 20,000 crore in 2025, underscores regional appetite for adhesives that accelerate build cycles. Government policies favoring biodegradable packaging boost rosin-based demand, while volatile tall-oil supply challenges local formulators to secure consistent feedstock.

North America retains innovation leadership through tight VOC caps and FDA food-contact rules steering purchases toward ultra-low-odor grades. Automotive electrification in the United States and Mexico triggers demand for high-heat synthetic resins that secure battery cell stacks. Europe emphasizes circular economy targets and REACH compliance, prompting a pivot to bio-content tackifiers despite higher costs. The 2025 rebound in European construction adhesives signals that regulatory headwinds can coexist with sustainable substitution opportunities.

South America and Middle East & Africa, though smaller, offer upside tied to logistics corridors, consumer goods growth, and foreign direct investment in manufacturing. Saint-Gobain's USD 1.025 billion purchase of FOSROC bolsters distribution of construction adhesives in GCC states and India, an example of global firms placing strategic bets on emerging demand centers. Exchange-rate swings and limited local resin capacity temper immediate growth, but gradual industrialization sets a foundation for tackifier uptake over the next decade.

- Arakawa Chemical Industries, Ltd.

- Arkema

- Eastman Chemical Company

- Exxon Mobil Corporation

- Henkel AG & Co. KGaA

- Ingevity Corporation

- Kolon Industries, Inc.

- Kraton Corporation

- Lawter, a Harima Chemicals, Inc. Company

- Natrochem, Inc.

- SI Group, Inc.

- Teckrez, Inc.

- TWC Group

- Yasuhara Chemical Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for hot-melt and PSA adhesives in packaging and hygiene

- 4.2.2 Urban infrastructure boom in APAC spurring construction adhesives

- 4.2.3 E-commerce growth accelerating tape and label consumption

- 4.2.4 Ultra-low-VOC, food-contact compliant resin grades gain preference

- 4.2.5 EV battery and lightweight automotive assembly needing high-heat tackifiers

- 4.3 Market Restraints

- 4.3.1 Petroleum-feedstock price volatility hurting hydrocarbon resin margins

- 4.3.2 Emergence of tackifier-free reactive hot-melt systems

- 4.3.3 Sustainability certifications constraining tall-oil and gum-rosin supply

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products and Services

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 Feedstock

- 5.1.1 Rosin Resins

- 5.1.2 Petroleum Resins

- 5.1.3 Terpene Resins

- 5.2 Form

- 5.2.1 Solid

- 5.2.2 Liquid

- 5.2.3 Resin Dispersion

- 5.3 Type

- 5.3.1 Synthetic

- 5.3.2 Natural

- 5.4 Application

- 5.4.1 Tapes and Labels

- 5.4.2 Assembly

- 5.4.3 Bookbinding

- 5.4.4 Footwear, Leather and Rubber

- 5.4.5 Other Applications

- 5.5 End-user Industry

- 5.5.1 Packaging

- 5.5.2 Building and Construction

- 5.5.3 Automotive

- 5.5.4 Non-wovens

- 5.5.5 Footwear

- 5.5.6 Other End-user Industries

- 5.6 Geography

- 5.6.1 Asia-Pacific

- 5.6.1.1 China

- 5.6.1.2 India

- 5.6.1.3 Japan

- 5.6.1.4 South Korea

- 5.6.1.5 Rest of Asia-Pacific

- 5.6.2 North America

- 5.6.2.1 United States

- 5.6.2.2 Canada

- 5.6.2.3 Mexico

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Rest of Europe

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 South Africa

- 5.6.5.3 Rest of Middle East and Africa

- 5.6.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Arakawa Chemical Industries, Ltd.

- 6.4.2 Arkema

- 6.4.3 Eastman Chemical Company

- 6.4.4 Exxon Mobil Corporation

- 6.4.5 Henkel AG & Co. KGaA

- 6.4.6 Ingevity Corporation

- 6.4.7 Kolon Industries, Inc.

- 6.4.8 Kraton Corporation

- 6.4.9 Lawter, a Harima Chemicals, Inc. Company

- 6.4.10 Natrochem, Inc.

- 6.4.11 SI Group, Inc.

- 6.4.12 Teckrez, Inc.

- 6.4.13 TWC Group

- 6.4.14 Yasuhara Chemical Co., Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

增粘劑市場:按類型、形式、分銷管道和應用分類-2026-2032年全球市場預測

增粘劑市場:按類型、形式、分銷管道和應用分類-2026-2032年全球市場預測 毛氈纖維市場機會、成長要素、產業趨勢分析及2026-2035年預測

毛氈纖維市場機會、成長要素、產業趨勢分析及2026-2035年預測 全球增稠劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年)PTOP橡膠增粘劑市場按類型、形態、等級和應用分類,全球預測(2026-2032年)生物基 Tacklyzer 市場按原料來源、產品類型、應用、終端用戶產業和分銷管道分類,全球預測(2026-2032 年)增黏劑市場 - 全球預測 2025-2030

全球增稠劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年)PTOP橡膠增粘劑市場按類型、形態、等級和應用分類,全球預測(2026-2032年)生物基 Tacklyzer 市場按原料來源、產品類型、應用、終端用戶產業和分銷管道分類,全球預測(2026-2032 年)增黏劑市場 - 全球預測 2025-2030 增黏劑市場-全球產業規模、佔有率、趨勢、機會與預測,依產品、形式、應用、地區及競爭細分,2020-2030 年預測

增黏劑市場-全球產業規模、佔有率、趨勢、機會與預測,依產品、形式、應用、地區及競爭細分,2020-2030 年預測 增黏劑市場報告:2031 年趨勢、預測與競爭分析

增黏劑市場報告:2031 年趨勢、預測與競爭分析 增粘劑市場規模、佔有率、趨勢分析報告:按產品、形式、應用、地區、細分市場預測,2024-2030

增粘劑市場規模、佔有率、趨勢分析報告:按產品、形式、應用、地區、細分市場預測,2024-2030