|

市場調查報告書

商品編碼

1851506

嬰兒食品包裝:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)Baby Food Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

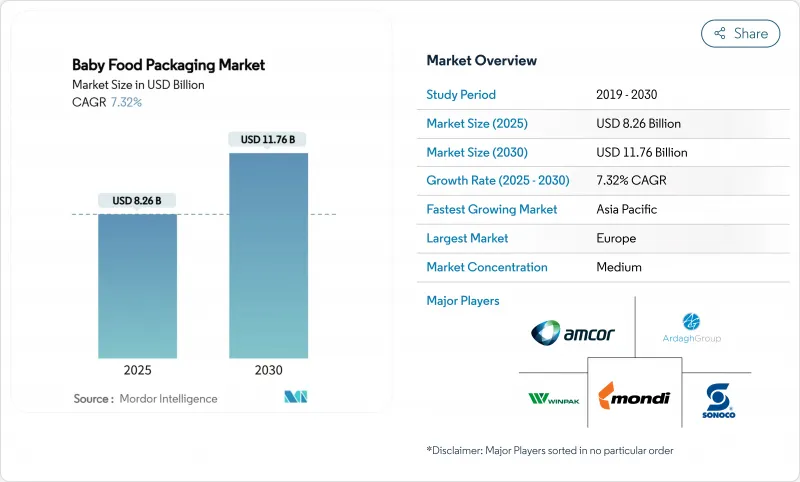

預計到 2025 年,嬰兒食品包裝市場規模將達到 82.6 億美元,到 2030 年將達到 117.6 億美元,年複合成長率為 7.32%。

隨著都市區家庭對即食包裝的需求不斷成長,監管機構對嬰幼兒食品安全制定了更為嚴格的規定,以及加工商採用能夠延長保存期限並促進消費者溝通的智慧材料,嬰幼兒食品包裝行業的成長速度超過了整個食品包裝行業。嬰幼兒樹脂的高價位保持穩定,使供應商能夠將合規成本轉嫁給消費者,而生產者延伸責任制(EPR)計劃正在推動對可回收和生物基複合材料的需求。從2025年到2030年,吸嘴袋、無菌填充線和人工智慧驅動的可追溯性預計將繼續引領嬰幼兒食品包裝市場的關鍵創新,從而將業績卓越的供應商與普通商品競爭者區分開來。由於全球樹脂價格波動和DIY食物泥潮流抑制了該行業的成長勢頭,加強醫藥級吸嘴和阻隔膜的供應鏈管理仍然至關重要。

全球嬰幼兒食品包裝市場趨勢與洞察

嬰兒食品袋裝產品的受歡迎程度主要歸功於其便利性。

由於輕巧、易攜帶且方便取用,吸嘴袋已取代玻璃瓶,佔據了嬰兒食品包裝市場超過30%的佔有率。千禧世代的父母認為可重複密封和降低破損風險是至關重要的優勢,這支撐了其價格溢價和重複購買率。耐熱複合材料可實現熱填充、蒸餾高壓滅菌和高壓巴氏殺菌,並確保產品無需添加防腐劑即可保持良好的貨架穩定性。品牌案例研究表明,改用吸嘴袋包裝後,尤其是有機食物泥,銷量實現了兩位數的成長。這些因素共同證實,吸嘴袋是嬰兒食品包裝市場中規模最大、成長最快的細分市場。

都市區雙薪家庭需要節省時間的模式

在人口密集的都市,上班族父母紛紛轉向即食包裝,以省去準備食物和清洗的麻煩。為了滿足這項需求,Once Upon a Farm 將其自動化生產線擴建至每週 120 萬包,是 2020 年產能的三倍。電子商務的興起進一步加劇了這一趨勢,因為與玻璃包裝相比,軟包裝袋和加固紙盒更能承受小包裹運輸過程中的衝擊。儘管價格溢價可能高達 20-30%,但市場韌性依然良好,為嬰幼兒食品包裝市場提供了持續的利好,因為家庭已經將包裝的便利性與節省時間劃上了等號。

針對塑膠永續性的強烈反對和立法

加州、緬因州、奧勒岡州和科羅拉多的生產者責任延伸制度(EPR)要求生產商為回收系統提供資金,並符合可回收的設計標準。歐盟的《包裝和包裝廢棄物條例》進一步規定,到2030年,包裝回收率必須達到30%。食品級再生聚丙烯(PP)的產能僅佔再生聚合物總產量的近10%,導致供應緊張和成本上升。能夠證明產品可回收性和可堆肥性的品牌贏得了消費者的信任,但傳統的多層包裝形式正面臨加速淘汰的局面,這將擠壓嬰兒食品包裝市場近期的淨利率。

細分市場分析

預計到2024年,塑膠仍將佔據26.7%的收入佔有率,這反映了其完善的加工基礎設施。但隨著監管機構和品牌商收緊碳減排目標,生質塑膠將以9.7%的複合年成長率成為成長最快的領域。 Braskem公司利用廢棄食用油製成的生物循環聚丙烯可直接取代傳統塑膠,以便於生產線改造。 ADBioplastics公司已將一種適用於嬰兒食物泥的100%可堆肥樹脂商業化。生物聚合物的早期採用者正在獲得生產者責任延伸(EPR)積分和市場優勢,將生物聚合物定位為策略對沖工具,而傳統塑膠則繼續保持其規模和成本優勢。

加工商正與生物聚合物供應商洽談長期回收協議,消費品公司也重新設計標籤,以強調產品在消費前的用途。隨著銷售量的成長,規模經濟將縮小成本差距,預計生質塑膠將在嬰幼兒食品包裝市場佔據更有利的地位。

區域分析

2024年,歐洲在銷售額方面維持25.8%的領先優勢,主要得益於鼓勵可回收設計、懲罰化學危害的先進法規。 2025年1月生效的BPA禁令將促使相關產業加快改進,並將業務導向擁有合格材料和合規文件的供應商。德國和法國擁有永續包裝研發中心,而英國對採用整合可追溯晶片的智慧包裝袋包裝的高階有機食物泥的需求持續旺盛。

亞太地區到2030年將以7.8%的複合年成長率成為全球成長最快的地區。中階收入的成長和都市區生活方式的普及將推動便利型產品(SKU)的需求,使該地區成為嬰幼兒食品包裝市場銷售成長的最大來源。中國嬰幼兒奶粉奶粉市場反彈:H&H集團2025年第一季營收成長44.3%,顯示消費者在經歷了先前的安全疑慮後,對品牌營養品的信任度有所回升。印度無BPA)的包裝,適逢安姆科(Amcor)以2,000萬美元收購鳳凰軟包裝(Phoenix Flexibles)。日本和韓國將率先推行雙重2D碼溯源,反映出消費者對安全保障的需求。

北美仍然是一個高價值市場,擁有嚴格的FDA監管和廣泛的電子商務。四個州已頒布生產者責任延伸(EPR)法,要求品牌商為回收提供資金,並推動了單一材料複合材料的快速普及。 2022年的奶粉短缺刺激了國內產能投資:Bobby's位於俄亥俄州的工廠目前在9萬平方英尺的廠房內,採用嚴格的微生物控制措施生產罐裝和奶粉。加拿大的省級EPR網路鼓勵在軟包裝和硬包裝產品中採用可回收設計,從而支持持續創新。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 方便主導嬰兒食品袋

- 省時省力的格式,受到雙薪都市區的青睞

- 更嚴格的嬰兒安全法規擴大了奢侈品包裝的適用範圍。

- 無菌吸嘴袋填充線的興起

- 生產者延伸責任制獎勵促進可回收性

- 人工智慧驅動的個人化營養套件設計創新

- 市場限制

- 針對塑膠永續性的強烈反對和立法

- BPA/化學品合規成本壓力

- 醫藥級噴嘴樹脂供應瓶頸

- DIY嬰兒食品趨勢降低了包裝需求

- 供應鏈分析

- 監管環境

- 技術展望

- 波特五力模型

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

- 評估市場的宏觀經濟因素

第5章 市場規模與成長預測

- 材料

- 塑膠

- 紙板

- 金屬

- 玻璃

- 生質塑膠

- 按包裝類型

- 瓶子

- 紙盒

- 瓶子

- 小袋

- 襯袋紙盒

- 依產品

- 液體配方

- 嬰兒乾糧

- 粉狀配方

- 已烹調的嬰兒輔食

- 嬰兒零食

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 東南亞

- 亞太其他地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 埃及

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Amcor PLC

- Tetra Laval Group

- Mondi Group

- Berry Global Inc.(incl. former RPC)

- Silgan Holdings Inc.

- Sonoco Products Company

- Ardagh Group

- Winpak Ltd

- DS Smith PLC

- SIG Combibloc Group

- Cheer Pack North America

- Gualapack Group

- Scholle IPN

- UFlex Ltd

- ProAmpac LLC

- Huhtamaki Oyj

- AptarGroup Inc.

- Plastipak Packaging Inc.

- Crown Holdings Inc.

- Sealed Air Corp.

第7章 市場機會與未來展望

The baby food packaging market size stands at USD 8.26 billion in 2025 and is forecast to reach USD 11.76 billion by 2030, advancing at a 7.32% CAGR.

This growth rate exceeds the broader food-packaging category as urban families seek ready-to-serve formats, regulators impose strict infant-safety rules, and converters deploy smart materials that lengthen shelf life while enabling consumer interaction. Steady premium-price tolerance for infant-grade resins allows suppliers to pass through compliance costs, while extended-producer-responsibility (EPR) programs propel demand for recyclable or bio-based laminates. During 2025-2030, spouted pouches, aseptic filling lines, and AI-enabled traceability are expected to remain the pivotal innovation fronts that separate high-performing vendors from commodity competitors in the baby food packaging market. Heightened supply-chain discipline around pharmaceutical-grade spouts and barrier films will remain essential as global resin volatility and DIY puree trends periodically temper category momentum.

Global Baby Food Packaging Market Trends and Insights

Convenience-Driven Adoption of Baby Food Pouches

Spouted pouches have secured more than 30% share of the baby food packaging market by displacing glass jars through lighter weight, portability, and mess-free dispensing. Millennial parents view resealability and reduced breakage risk as decisive benefits, supporting price premiums and repeat purchases. Heat-resistant laminates enable hot-fill, retort, and high-pressure pasteurization, delivering preservative-free shelf stability. Brand case studies show double-digit sales lifts after switching to pouch formats, particularly in organic purees. Together, these factors underpin the segment's dual status as both largest and fastest growth engine of the baby food packaging market.

Urban Dual-Income Households Demanding Time-Saving Formats

In dense metros, working parents trade up to ready-to-consume packages that cut prep time and washing. Once Upon a Farm scaled automated lines to 1.2 million packs per week triple 2020 throughput-to meet this demand.Asia Pacific megacities show the sharpest volume increases as extended-family childcare support wanes. E-commerce penetration amplifies the trend because pouches and reinforced cartons tolerate parcel-handling shocks better than glass. Despite 20-30% price premiums, elasticity remains favorable as households equate packaging convenience with intangible time savings, providing sustained tailwinds for the baby food packaging market.

Plastics Sustainability Backlash & Legislation

EPR statutes in California, Maine, Oregon, and Colorado obligate producers to bankroll recycling systems and meet design-for-recovery criteria.The EU's Packaging and Packaging Waste Regulation further mandates 30% recycled content by 2030. Food-grade recycled PP capacity sits near 10% of total recycled polymer output, tightening supply and inflating costs. Brands able to validate recyclability or compostability gain consumer trust, whereas legacy multilayer formats face accelerating obsolescence, weighing on near-term margins across the baby food packaging market.

Other drivers and restraints analyzed in the detailed report include:

- Stricter Infant-Safety Regulations Expanding Premium Packaging

- Aseptic Spouted-Pouch Filling Lines Gaining Ground

- Supply Bottlenecks of Pharma-Grade Spout Resins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Plastic maintained 26.7% revenue share in 2024, reflecting extensive processing infrastructure, but bioplastics now post the quickest 9.7% CAGR as regulators and brands escalate carbon-reduction targets. Braskem's bio-circular polypropylene derived from used cooking oil offers a drop-in alternative that eases line changeovers. ADBioplastics commercialized a 100% compostable resin tailored for wet baby purees. Early adopters secure EPR credits and marketing lift, positioning biopolymers as a strategic hedge even while traditional plastics keep scale and cost advantages.

The material shift galvanizes supply-chain reengineering: converters negotiate long-term offtake with bio-polymer suppliers, and CPGs redesign labels to highlight end-of-life credentials. As volumes rise, economies of scale are expected to narrow the cost delta, further embedding bioplastics within the baby food packaging market.

Baby Food Packaging Market Report is Segmented by Material (Plastic, Paperboard, Metal, Glass, Bioplastics), Package Type (Bottles, Cartons, Jars, Pouches, Bag-In-Box), Product (Liquid Milk Formula, Dried Baby Food, Powder Milk Formula, Prepared Baby Food, Baby Snacks), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Europe maintained a 25.8% revenue lead in 2024, propelled by progressive regulation that rewards recyclable designs and punishes chemical hazards. The January 2025 BPA prohibition forces immediate reformulations, channeling business toward suppliers with qualifying materials and compliance documentation. Germany and France house active clusters of sustainable-packaging R&D, while the UK displays sustained demand for premium organic purees sold in smart pouches that embed traceability chips.

Asia Pacific shows the fastest 7.8% CAGR through 2030. Rising middle-class incomes and urban lifestyles accelerate convenience-focused SKUs, positioning the region as the largest incremental volume source for the baby food packaging market. China's infant-formula rebound H&H Group recorded 44.3% Q1 2025 revenue growth signals renewed confidence in branded nutrition after earlier safety scares. India's BPA-free mandate aligns with Amcor's USD 20 million purchase of Phoenix Flexibles, which boosts local flexible-film capacity in Gujarat. Japan and South Korea pioneer dual-QR traceability, reflecting consumer penchant for safety verification.

North America remains a high-value arena given stringent FDA rules and wide e-commerce penetration. EPR laws in four states obligate brands to finance recycling, pushing quick adoption of mono-material laminates. The 2022 formula shortage catalyzed domestic capacity investments: Bobbie's 90,000 sq ft Ohio plant now produces canned and powdered formula under strict microbiological controls. Canada's harmonized provincial EPR network incentivizes design-for-recycling across flexible and rigid formats alike, sustaining steady innovation.

- Amcor PLC

- Tetra Laval Group

- Mondi Group

- Berry Global Inc. (incl. former RPC)

- Silgan Holdings Inc.

- Sonoco Products Company

- Ardagh Group

- Winpak Ltd

- DS Smith PLC

- SIG Combibloc Group

- Cheer Pack North America

- Gualapack Group

- Scholle IPN

- UFlex Ltd

- ProAmpac LLC

- Huhtamaki Oyj

- AptarGroup Inc.

- Plastipak Packaging Inc.

- Crown Holdings Inc.

- Sealed Air Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Convenience-driven adoption of baby food pouches

- 4.2.2 Urban dual-income households demanding time-saving formats

- 4.2.3 Stricter infant-safety regulations expanding premium packaging

- 4.2.4 Aseptic spouted-pouch filling lines gaining ground

- 4.2.5 Extended-producer-responsibility incentives for recyclability

- 4.2.6 AI-led personalised-nutrition pack design innovations

- 4.3 Market Restraints

- 4.3.1 Plastics sustainability backlash and legislation

- 4.3.2 BPA/chemicals compliance cost pressures

- 4.3.3 Supply bottlenecks of pharma-grade spout resins

- 4.3.4 DIY baby-food trend reducing packaged demand

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assesment of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Plastic

- 5.1.2 Paperboard

- 5.1.3 Metal

- 5.1.4 Glass

- 5.1.5 Bioplastics

- 5.2 By Package Type

- 5.2.1 Bottles

- 5.2.2 Cartons

- 5.2.3 Jars

- 5.2.4 Pouches

- 5.2.5 Bag-in-Box

- 5.3 By Product

- 5.3.1 Liquid Milk Formula

- 5.3.2 Dried Baby Food

- 5.3.3 Powder Milk Formula

- 5.3.4 Prepared Baby Food

- 5.3.5 Baby Snacks

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 India

- 5.4.4.4 South Korea

- 5.4.4.5 Southeast Asia

- 5.4.4.6 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 Middle East

- 5.4.5.1.1 Saudi Arabia

- 5.4.5.1.2 United Arab Emirates

- 5.4.5.1.3 Turkey

- 5.4.5.1.4 Rest of Middle East

- 5.4.5.2 Africa

- 5.4.5.2.1 South Africa

- 5.4.5.2.2 Nigeria

- 5.4.5.2.3 Egypt

- 5.4.5.2.4 Rest of Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Amcor PLC

- 6.4.2 Tetra Laval Group

- 6.4.3 Mondi Group

- 6.4.4 Berry Global Inc. (incl. former RPC)

- 6.4.5 Silgan Holdings Inc.

- 6.4.6 Sonoco Products Company

- 6.4.7 Ardagh Group

- 6.4.8 Winpak Ltd

- 6.4.9 DS Smith PLC

- 6.4.10 SIG Combibloc Group

- 6.4.11 Cheer Pack North America

- 6.4.12 Gualapack Group

- 6.4.13 Scholle IPN

- 6.4.14 UFlex Ltd

- 6.4.15 ProAmpac LLC

- 6.4.16 Huhtamaki Oyj

- 6.4.17 AptarGroup Inc.

- 6.4.18 Plastipak Packaging Inc.

- 6.4.19 Crown Holdings Inc.

- 6.4.20 Sealed Air Corp.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

嬰兒食品包裝市場規模、佔有率和成長分析(按材料、包裝類型、食品類型、分銷管道和地區分類)-2026-2033年產業預測

嬰兒食品包裝市場規模、佔有率和成長分析(按材料、包裝類型、食品類型、分銷管道和地區分類)-2026-2033年產業預測 嬰兒食品包裝市場按包裝材料、包裝形式、封蓋類型和類別分類-2025-2032年全球預測

嬰兒食品包裝市場按包裝材料、包裝形式、封蓋類型和類別分類-2025-2032年全球預測 嬰兒食品包裝市場 - 預測 2025-2030

嬰兒食品包裝市場 - 預測 2025-2030 亞太地區嬰幼兒食品包裝:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)

亞太地區嬰幼兒食品包裝:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年) 嬰兒食品包裝市場規模、佔有率、趨勢分析報告:按材料、產品、地區、細分市場、預測,2025-2030 年嬰兒食品玻璃包裝:市場佔有率分析、產業趨勢與成長預測(2025-2030)

嬰兒食品包裝市場規模、佔有率、趨勢分析報告:按材料、產品、地區、細分市場、預測,2025-2030 年嬰兒食品玻璃包裝:市場佔有率分析、產業趨勢與成長預測(2025-2030) 2025 年至 2033 年嬰兒食品包裝市場報告(按產品、材料、包裝類型和地區)中東和非洲嬰兒食品包裝:市場佔有率分析、產業趨勢、成長預測(2025-2030)北美嬰兒食品包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030)拉丁美洲嬰兒食品包裝:市場佔有率分析、產業趨勢與成長預測(2025-2030)

2025 年至 2033 年嬰兒食品包裝市場報告(按產品、材料、包裝類型和地區)中東和非洲嬰兒食品包裝:市場佔有率分析、產業趨勢、成長預測(2025-2030)北美嬰兒食品包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030)拉丁美洲嬰兒食品包裝:市場佔有率分析、產業趨勢與成長預測(2025-2030)