|

市場調查報告書

商品編碼

1851465

商業分析:市場佔有率分析、產業趨勢、統計數據、成長預測(2025-2030 年)Business Analytics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

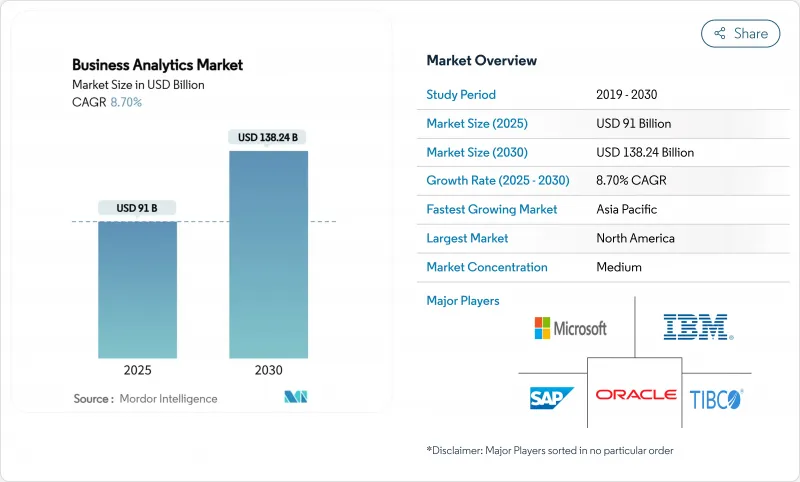

預計到 2025 年,商業分析市場規模將達到 910 億美元,到 2030 年將達到 1,382.4 億美元,複合年成長率為 8.70%。

雲端原生平台、人工智慧驅動的自動化以及數位轉型的廣泛推動正在推動這一擴張。各行各業的組織機構如今都將分析融入日常工作流程,以發現低效環節、提升客戶參與並縮短決策週期。人工智慧與現有分析技術的融合正將分析領域從回顧性報告轉向即時預測智慧,而雲端運算的普及則降低了各種規模企業的准入門檻。隨著現有企業軟體供應商不斷調整產品組合以跟上雲端專家和人工智慧優先型新興企業的步伐,競爭依然激烈,這些公司承諾提供更快的部署速度和更簡單的用戶體驗。人才短缺、資料主權法規以及高昂的前期成本仍然限制著成長,但尚未阻止向以資料為中心的營運模式的系統性轉變。

全球商業分析市場趨勢與洞察

將人工智慧和機器學習整合到您的分析平台中

人工智慧正從附加功能轉變為商業分析平台的核心能力。諸如 Snowflake Cortex 和 Microsoft 365 Copilot 的 Analyst 代理等新版本能夠解讀自然語言、自動生成 SQL 語句,並提供以往需要資料科學家才能實現的預測性洞察。採用這些功能的公司報告稱,其行銷、供應鏈和財務團隊的生產力提高了 30% 到 50%。隨著模型訓練成本的下降,平台供應商正在整合生成式人工智慧,以擴大存取權限、自動化資料準備,並開啟「代理分析」時代——在這個時代,自主代理無需人工編碼編配複雜的分析流程。

巨量資料和雲端運算的興起

資料量、傳輸速度和資料種類都在持續成長。每週有超過 6000 家機構向 BigQuery 傳輸超過 275 Petabyte的資料傳輸,這凸顯了彈性雲端儲存和運算正逐漸成為分析的預設基礎。諸如 ClickHouse 與 AWS 簽署的五年合作協議等聯合創新項目,正在加速開發金融和電子商務工作負載的客製化解決方案。雲端框架還支援將本地化的物聯網資料處理與集中式儀表板相結合,從而使工業環境中的設備效率提高 10%,計劃外停機時間減少 30%。

數據主權限制

GDPR、《雲端法案》和新興國家法律之間的衝突規則迫使跨國公司建立特定區域的資料堆疊。雖然超大規模資料中心業者和區域性雲端服務供應商提供的自主雲可以解決這個問題,但企業仍需要在多個供應商和控制措施之間周旋,才能在不損害分析一致性的前提下滿足監管機構的要求。

細分市場分析

2024年,雲端運算業務將佔總營收的65.4%,年複合成長率達10.7%,到2030年,其在商業分析市場規模中的佔比將進一步擴大。資本支出減少、彈性擴展以及與資料湖和人工智慧服務的快速整合,進一步增強了雲端運算的吸引力。安全認證和自動化合規功能現已涵蓋金融、醫療保健和政府等行業的業務,進一步削弱了本地部署支持者的最後堡壘。

儘管在面臨嚴格的延遲要求、傳統系統整合或監管義務時,本地部署仍然可行,但其市場佔有率近年來已逐漸萎縮。混合雲方案提供了一條過渡路徑,將敏感工作負載保留在防火牆後,並將突發處理遷移到雲端。服務供應商正在將遷移套件、託管服務和按需付費模式捆綁在一起,以吸引猶豫不決的客戶遷移到雲端,從而鞏固雲端作為市場領導者和成長引擎的地位。

說明分析將佔據商業分析市場最大佔有率,到2024年將佔總收入的32.7%,而預測技術將以8.8%的複合年成長率超越所有其他類別。企業將從「發生了什麼事」的儀錶板轉向前瞻性模型,這些模型能夠識別客戶流失風險、最佳化庫存,並在故障發生前安排維修人員。生成式人工智慧將透過自動產生複雜的時間序列模型並為非技術使用者展示場景模擬,來增強預測工作流程。

診斷分析充當橋樑,解釋根本原因並為預測演算法提供見解。指導性工具則形成閉迴路,在預算和人員配置等限制條件下推薦最佳行動方案。早期成功案例,例如消費品製造商透過最佳化生產計劃每週節省高達 20 萬美元,正在推動該技術的更廣泛應用。隨著套件的不斷完善,預測層和指導層將協同工作,將歷史資料轉化為跨職能部門的自動化、情境感知決策。

商業分析市場按部署模式(本地部署、雲端部署)、分析類型(說明分析、診斷性分析及其他)、組織規模(大型企業、中小企業)、最終用戶行業(銀行、金融服務和保險、醫療保健和生命科學及其他)以及地區進行細分。市場預測以美元計價。

區域分析

北美地區預計到2024年將佔全球收入的27.4%,這主要得益於其成熟的技術生態系統、豐富的人才儲備以及早期對雲端技術的採用。各公司正在對現有平台進行改造,整合人工智慧加速器、串流管道和自動化管治,並從現有的資料資產中提高效率。美國在雲端支出方面處於領先地位,加拿大則在自然資源和金融服務領域大力應用分析技術。墨西哥正在採用雲端平台來支援出口導向製造業和跨境物流。

亞太地區以10.3%的複合年成長率 (CAGR) 實現最快成長,這主要得益於政府人工智慧策略、行動應用普及以及待開發區雲端平台的快速部署。中國佔該地區商業分析市場37.5%的佔有率,這得益於其龐大的數位支付生態系統和產業升級計畫。越南和菲律賓等高成長國家的年成長率超過19%,中小企業 (SME) 正積極採用SaaS分析來顯著改善其舊有系統。印度、日本、韓國和泰國正將公共部門津貼用於勞動力技能提升和數據生態系統建設,這為平台供應商創造了肥沃的土壤。

在強而有力的隱私保護條例和產業數位化資金的支持下,歐洲正穩步推進。德國、法國和英國正在利用分析技術來提高製造業效率和財務合規性,而南歐國家則在旅遊和零售業拓展分析技術的應用情境。主權雲端框架和隱私增強技術正在滿足GDPR主導的需求。中東和非洲正受益於智慧城市計劃,尤其是在海灣地區;南美洲的巴西和阿根廷也在積極採用雲端運算,儘管基礎設施差異和貨幣波動正在減緩其普及速度。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 巨量資料和雲端運算的興起

- 即時決策的必要性

- 將人工智慧/機器學習引入分析平台

- 監管壓力日益加大,數據主導合規性面臨越來越大壓力

- 面向物聯網密集型產業的邊緣分析

- 一個保護隱私的資料潔淨室

- 市場限制

- 前期成本高,投資報酬率不確定性

- 高級分析人才短缺

- 數據主權限制

- ESG數據品質差距

- 供應鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 評估市場的宏觀經濟因素

第5章 市場規模與成長預測

- 按部署模式

- 本地部署

- 雲

- 按分析類型

- 說明的

- 診斷

- 預言

- 規範

- 按公司規模

- 主要企業

- 中小企業

- 按最終用戶行業分類

- 銀行、金融服務和保險(BFSI)

- 醫療保健和生命科學

- 製造業

- 零售與電子商務

- 電訊和資訊技術

- 政府/公共部門

- 能源與公共產業

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 東南亞

- 亞太其他地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 埃及

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略性措施與資金籌措活動

- 市佔率分析

- 公司簡介

- Microsoft Corp.

- SAP SE

- Oracle Corp.

- IBM Corp.

- Salesforce Inc.(Tableau)

- SAS Institute Inc.

- TIBCO Software Inc.

- Qlik Tech Intl.

- MicroStrategy Inc.

- Infor Inc.

- Google LLC(Looker)

- Amazon Web Services(QuickSight)

- Domo Inc.

- Sisense Ltd.

- ThoughtSpot Inc.

- Alteryx Inc.

- Zoho Corp.(Zoho Analytics)

- Board International

- GoodData Corp.

- Yellowfin BI

- Pyramid Analytics

- Logi Analytics(InsightSoftware)

- Teradata Corp.

- Informatica Inc.

- Palantir Technologies

- Snowflake Inc.

- Databricks Inc.

第7章 市場機會與未來展望

The business analytics market is valued at USD 91 billion in 2025 and is forecast to reach USD 138.24 billion by 2030, reflecting an 8.70% CAGR over the period.

Cloud-native platforms, AI-driven automation, and a widespread push for digital transformation underpin this expansion. Organizations across industries now embed analytics into day-to-day workflows to uncover inefficiencies, sharpen customer engagement, and shorten decision cycles. The convergence of artificial intelligence with established analytics stacks is shifting the discipline from retrospective reporting toward real-time predictive intelligence, while pervasive cloud adoption lowers entry barriers for firms of every size. Competitive intensity remains lively as incumbent enterprise software vendors revamp portfolios to match the pace set by cloud specialists and AI-first start-ups that promise faster deployment and simpler user experiences. Talent shortages, data-sovereignty rules, and high initial costs continue to temper growth yet have not derailed the structural migration toward data-centric operations.

Global Business Analytics Market Trends and Insights

AI and ML infusion into analytics platforms

Artificial intelligence has shifted from a bolt-on feature to a core capability within business analytics platforms. New releases such as Snowflake Cortex and Microsoft 365 Copilot's Analyst agent interpret natural language, auto-generate SQL, and surface predictive insights that once required a data scientist. Companies adopting these capabilities report 30-50% productivity lifts in marketing, supply-chain, and finance teams. As model training costs fall, platform vendors embed generative AI to widen access and automate data preparation, ushering in an era of "agentic analytics" where autonomous agents orchestrate complex analysis pipelines without human coding.

Proliferation of big data and cloud adoption

Volume, velocity, and variety of data keep rising. More than 6,000 organizations exchange upward of 275 petabytes each week on BigQuery, highlighting how elastic cloud storage and compute have become the default substrate for analytics. Joint innovation programs, such as the five-year agreement between ClickHouse and AWS, accelerate purpose-built solutions for finance and e-commerce workloads. Cloud frameworks also let firms pair localized IoT data processing with centralized dashboards, delivering 10% gains in equipment efficiency and 30% reductions in unplanned downtime in industrial settings.

Data-sovereignty restrictions

Conflicting rules among GDPR, the CLOUD Act, and emerging national laws force multinationals to architect region-specific data stacks. Deployments must ensure local processing, encrypted transfers, and auditable consent, adding cost and complexity.Sovereign-cloud offerings from hyperscalers and regional providers address the issue, yet organizations still juggle multiple vendors and controls to satisfy regulators without fracturing analytical coherence.

Other drivers and restraints analyzed in the detailed report include:

- Need for real-time decision-making

- Edge analytics for IoT-heavy industries

- Talent shortage in advanced analytics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The cloud segment accounts for 65.4% of 2024 revenue, and its 10.7% CAGR means it will command an even larger slice of the business analytics market size by 2030. Lower capital expenditure, elastic scaling, and rapid integration with data lakes and AI services cement its appeal. Security certifications and automated compliance features now cover finance, healthcare, and government workloads, eroding the last strongholds of on-premise advocates.

On-premise deployments persist where strict latency, legacy integration, or regulatory mandates prevail, but their share recedes every year. Hybrid blueprints, in which sensitive workloads stay behind the firewall while burst processing moves to the cloud, offer a transitional path. Providers bundle migration toolkits, managed services, and consumption-based pricing to nudge hesitant customers toward the cloud, reinforcing its position as both market leader and growth engine.

Descriptive analytics retained 32.7% of 2024 revenue, the largest slice of the business analytics market, yet predictive techniques outpace all categories with an 8.8% CAGR. Organizations evolve from "what happened" dashboards to forward-looking models that flag churn risk, optimize inventory, and route maintenance crews before breakdowns occur. Generative AI enhances predictive workflows by auto-coding complex time-series models and surfacing scenario simulations for non-technical users.

Diagnostic analytics serves as a bridge, explaining root causes and feeding features into forecasting algorithms. Prescriptive tools close the loop by recommending the best action under constraints such as budget or staffing. Early success stories like a consumer-products maker saving up to USD 200,000 weekly through optimized production schedules fuel wider adoption. As toolkits mature, predictive and prescriptive layers will jointly convert historical data into automated, context-aware decisions across functions.

Business Analytics Market is Segmented by Deployment Model (On-Premises, Cloud), Analytics Type (Descriptive, Diagnostic, and More), Organization Size (Large Enterprises, Smes), End-User Industry (BFSI, Healthcare and Life Sciences, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America holds 27.4% of 2024 revenue thanks to a mature technology ecosystem, abundant talent, and early cloud adoption. Enterprises refine existing platforms with AI accelerators, streaming pipelines, and automated governance, squeezing incremental efficiency from established data assets. The United States leads spending, and Canada leverages analytics in natural-resources and financial-services verticals. Mexico adopts cloud platforms to support export-oriented manufacturing and cross-border logistics.

Asia Pacific is the fastest-growing region at a 10.3% CAGR, fueled by government AI strategies, widespread mobile adoption, and greenfield cloud deployments. China commands 37.5% of the regional business analytics market, backed by large-scale digital payment ecosystems and industrial upgrade programs. High-growth economies such as Vietnam and the Philippines exceed 19% annual expansion as SMEs embrace SaaS analytics to leapfrog legacy systems. India, Japan, South Korea, and Thailand channel public-sector grants into workforce upskilling and data-ecosystem development, creating fertile ground for platform vendors.

Europe advances steadily underpinned by strong privacy regulations and industry digitization funding. Germany, France, and the United Kingdom deploy analytics for manufacturing efficiency and financial compliance, while southern nations expand tourism and retail analytics use cases. Sovereign-cloud frameworks and privacy-enhancing technologies address GDPR-driven demands. The Middle East and Africa benefit from smart-city agendas, especially in the Gulf states, whereas South America gains traction through cloud uptake in Brazil and Argentina, although infrastructure gaps and currency volatility temper the slope of adoption

- Microsoft Corp.

- SAP SE

- Oracle Corp.

- IBM Corp.

- Salesforce Inc. (Tableau)

- SAS Institute Inc.

- TIBCO Software Inc.

- Qlik Tech Intl.

- MicroStrategy Inc.

- Infor Inc.

- Google LLC (Looker)

- Amazon Web Services (QuickSight)

- Domo Inc.

- Sisense Ltd.

- ThoughtSpot Inc.

- Alteryx Inc.

- Zoho Corp. (Zoho Analytics)

- Board International

- GoodData Corp.

- Yellowfin BI

- Pyramid Analytics

- Logi Analytics (InsightSoftware)

- Teradata Corp.

- Informatica Inc.

- Palantir Technologies

- Snowflake Inc.

- Databricks Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of big data and cloud adoption

- 4.2.2 Need for real-time decision-making

- 4.2.3 AI/ML infusion into analytics platforms

- 4.2.4 Regulatory push for data-driven compliance

- 4.2.5 Edge analytics for IoT-heavy industries

- 4.2.6 Privacy-preserving data clean rooms

- 4.3 Market Restraints

- 4.3.1 High upfront cost and ROI uncertainty

- 4.3.2 Talent shortage in advanced analytics

- 4.3.3 Data-sovereignty restrictions

- 4.3.4 ESG-data quality gaps

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assesment of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Model

- 5.1.1 On-Premise

- 5.1.2 Cloud

- 5.2 By Analytics Type

- 5.2.1 Descriptive

- 5.2.2 Diagnostic

- 5.2.3 Predictive

- 5.2.4 Prescriptive

- 5.3 By Organisation Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Mid-sized Enterprises (SMEs)

- 5.4 By End-user Industry

- 5.4.1 Banking, Financial Services and Insurance (BFSI)

- 5.4.2 Healthcare and Life Sciences

- 5.4.3 Manufacturing

- 5.4.4 Retail and E-commerce

- 5.4.5 Telecom and IT

- 5.4.6 Government and Public Sector

- 5.4.7 Energy and Utilities

- 5.4.8 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Southeast Asia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Egypt

- 5.5.5.2.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves and Funding Activity

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Microsoft Corp.

- 6.4.2 SAP SE

- 6.4.3 Oracle Corp.

- 6.4.4 IBM Corp.

- 6.4.5 Salesforce Inc. (Tableau)

- 6.4.6 SAS Institute Inc.

- 6.4.7 TIBCO Software Inc.

- 6.4.8 Qlik Tech Intl.

- 6.4.9 MicroStrategy Inc.

- 6.4.10 Infor Inc.

- 6.4.11 Google LLC (Looker)

- 6.4.12 Amazon Web Services (QuickSight)

- 6.4.13 Domo Inc.

- 6.4.14 Sisense Ltd.

- 6.4.15 ThoughtSpot Inc.

- 6.4.16 Alteryx Inc.

- 6.4.17 Zoho Corp. (Zoho Analytics)

- 6.4.18 Board International

- 6.4.19 GoodData Corp.

- 6.4.20 Yellowfin BI

- 6.4.21 Pyramid Analytics

- 6.4.22 Logi Analytics (InsightSoftware)

- 6.4.23 Teradata Corp.

- 6.4.24 Informatica Inc.

- 6.4.25 Palantir Technologies

- 6.4.26 Snowflake Inc.

- 6.4.27 Databricks Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

雲端商業分析市場:按組件、最終用戶、應用、部署模式和組織規模分類-2026-2032年全球市場預測基於SaaS的商業分析市場:依架構類型、部署模式、組織規模、分析類型和產業分類-2026年至2032年全球市場預測商業分析市場:按類型、部署模式、應用程式和最終用戶分類-2026-2032年全球市場預測

雲端商業分析市場:按組件、最終用戶、應用、部署模式和組織規模分類-2026-2032年全球市場預測基於SaaS的商業分析市場:依架構類型、部署模式、組織規模、分析類型和產業分類-2026年至2032年全球市場預測商業分析市場:按類型、部署模式、應用程式和最終用戶分類-2026-2032年全球市場預測 2026年全球商業分析與企業軟體市場報告2026年全球360度回饋軟體市場報告

2026年全球商業分析與企業軟體市場報告2026年全球360度回饋軟體市場報告 全球資料提取市場規模、佔有率、趨勢和成長分析報告(2026-2034年)按部署模式、定價模式、應用領域和客戶類型分類的簡報撰寫和分析軟體市場,全球預測(2026-2032 年)

全球資料提取市場規模、佔有率、趨勢和成長分析報告(2026-2034年)按部署模式、定價模式、應用領域和客戶類型分類的簡報撰寫和分析軟體市場,全球預測(2026-2032 年) 全球個人化腦功能分析市場預測(至2032年),按組件、分析類型、認知功能、部署類型、最終用戶和地區分類

全球個人化腦功能分析市場預測(至2032年),按組件、分析類型、認知功能、部署類型、最終用戶和地區分類 基於 SaaS 的商業分析市場規模、佔有率和成長分析(按交付類型、部署模式、分析類型和地區分類)—產業預測(2026-2033 年)

基於 SaaS 的商業分析市場規模、佔有率和成長分析(按交付類型、部署模式、分析類型和地區分類)—產業預測(2026-2033 年) 商業分析軟體市場規模、佔有率和成長分析(按部署模式、組織規模、功能領域、解決方案類型、垂直產業和地區分類)-2026-2033年產業預測

商業分析軟體市場規模、佔有率和成長分析(按部署模式、組織規模、功能領域、解決方案類型、垂直產業和地區分類)-2026-2033年產業預測