|

市場調查報告書

商品編碼

1851414

能源管理系統:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)Energy Management Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

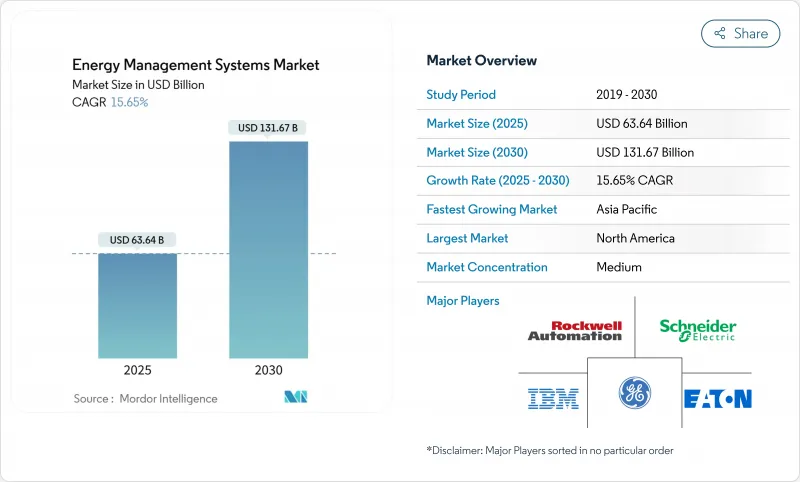

預計到 2025 年,能源管理系統市場規模將達到 636.4 億美元,到 2030 年將達到 1,316.7 億美元,複合年成長率為 15.65%。

這種快速成長反映了更嚴格的脫碳法規、智慧電網的快速部署以及企業日益成長的淨零排放目標,這些因素使得即時能源最佳化成為必需而非可選項。公共產業正在大規模部署高級計量基礎設施 (AMI),為營運商提供實現電網自癒能力和人工智慧主導分析所需的精細數據,從而降低營運成本。商業房地產所有者將面臨從 2026 年開始實施的強制性淨零建築規範,這將推動對互聯的暖通空調、照明和控制平台的需求激增。同時,簽訂大規模可再生能源購電協議的公司需要能夠進行小時追蹤、證書管理和碳計量的整合系統。氣候政策、大宗商品價格波動以及不斷上漲的碳成本,都凸顯了能源管理系統市場的經濟價值,因為企業都在尋求兩位數的節能效果和應對供應面衝擊的能力。

全球能源管理系統市場趨勢與洞察

快速普及先進計量基礎設施將變革電網智慧

成熟經濟體的公共產業正在加速推進其高級計量基礎設施(AMI)項目,目標是在2024年之前完成,屆時將安裝數百萬個智慧電錶,並將間隔數據傳輸到雲端分析引擎。 Eversource公司在麻薩諸塞州和康乃狄克州完成了一個涵蓋130萬個電錶的計劃,而National Grid公司則在東北地區連接了340萬個終端。這些資料饋送自動需量反應、故障自癒和預測性負載預測等功能提供支援——這些都是現代能源管理系統市場平台的核心模組。人工智慧演算法能夠在幾秒鐘內重新分配電力,從而縮短恢復時間並減少配電損耗。隨著配電公司實現電網服務的商業化並整合可再生能源,AMI正在成為連接現場資產和雲端基礎最佳化系統的關鍵環節。

強制性淨零排放建築規範加速商業環境管理系統的採用

紐約市、華盛頓州和加州等地區已頒布相關法規,旨在推動大型建築最快於2026年開始實現淨零排放營運。第97號地方法律要求面積超過25,000平方英尺的設施到2030年將排放減少40%,並對不合規者處以嚴厲處罰。加州第24號法規的更新強制要求採用先進的控制和計量技術,使能源管理系統市場從自願升級轉變為合規要求。類似的強制規定正在加拿大和歐盟蔓延,推動了對整合式暖通空調、照明和可再生能源平台的需求。

系統整合的高昂初始成本阻礙了中小企業的市場滲透。

全面部署的成本仍然在 5 萬至 50 萬美元之間,這對資金緊張的企業來說是一道障礙。硬體、整合和培訓的投資回收期長達 18 至 36 個月,減緩了中小企業採用該技術的步伐。 Iris Ohyama 於 2025 年發布的 ENEverse 雲端套件就是一個很好的例子,它將感測器、分析和遠端控制功能整合到一個無需硬體的模型中。

細分市場分析

到2024年,建築能源管理系統將佔據能源管理系統市場最大的佔有率,達到46.0%。在監管要求日益嚴格、租戶永續性報告要求不斷提高以及對健康室內環境日益重視的推動下,商業房地產持續投資於先進的控制系統,以降低25%至40%的公用事業成本。家庭解決方案將以17.2%的複合年成長率快速成長,能源價格上漲、智慧家電普及以及公用事業需量反應獎勵促使家庭用戶轉向語音控制恆溫器和電動車自動充電調度系統。整合平台正在融合居住感應器、光伏逆變器和電池調度功能,以建構自平衡微電網。儘管供應商提供邊緣中心或雲端優先架構,但兩者都會將資料路由至人工智慧引擎進行即時最佳化,從而擴大了能源管理系統市場的潛在用戶群。

近期進展表明,自動化方式正從基於規則的自動化轉向預測性編配。 C3.ai 模型將基於物理的設備庫與機器學習相結合,預測負載峰值並主動調節暖通空調系統,從而最大限度地降低能耗。開利 BluEdge 控制中心將冷水機組層級的資料傳輸給遠端工程師,工程師只需幾分鐘即可微調設定值,無需現場人員即可實現冷卻器的節能效果。由此產生的回饋循環使得已確認的節能成果可用於資助進一步的維修,並建立長期服務協議,從而保障供應商的收入。

至2024年,製造業將佔據能源管理系統31.4%的市場。水泥、鋼鐵和化學等產業正利用高速感測器和數位孿生技術來控制熔爐、壓縮機和生產線,力求最大限度地提高每一千瓦時的生產力。同時,醫療保健產業正以16.25%的複合年成長率快速成長。醫院全天候運作,對濕度和溫度有嚴格的控制要求,因此是利用人工智慧控制空調和鍋爐的理想場所。阿波羅醫院在實施了一套整合醫療設備調度和熱電汽電共生控制的雲端能源管理系統後,公用事業成本降低了30%。

電力公司作為第二大終端用戶,正在利用能源管理系統(EMS)模組進行需求預測和可再生能源併網。 IT和電訊也在資料中心應用類似的邏輯,因為資料中心的冷卻負荷接近總消費量的40%。隨著人工智慧工作負載的激增,伺服器密度也隨之飆升,先進的氣流建模和液冷最佳化正成為設施藍圖中的主流方案。住宅和商業綜合體的需求也在不斷成長,這主要得益於淨計量政策和屋頂太陽能貨幣化的推動。

能源管理系統市場報告按 EMS 類型(BEMS、IEMS、HEMS)、最終用戶(製造業、電力能源、IT 和通訊、醫療保健、住宅和商業)、應用(能源產出、能源傳輸、能源監控)、組件(硬體、軟體、服務)和地區進行細分。

區域分析

北美將繼續保持領先地位,預計到2024年將佔能源管理系統市場收入的35.6% 。 《稅額扣抵計量、電動車充電和建築維修計劃。像Eversource和National Grid這樣的公共產業將在2024年新增數百萬個智慧終端,從而建立支援進階分析的資料基礎。Schneider Electric積極響應,投資7億美元擴建美國的工廠,用於本地生產開關設備、微電網控制器以及進行軟體研發,體現了其對政策穩定性和客戶需求的信心。

在「歐洲綠色新政」和「Fit-for-55」一攬子計畫的推動下,歐洲正積極效仿。 「Fit-for-55」計畫的目標是到2030年將排放量比1990年水準降低55%。成員國正在將數位化建築要求納入當地立法,從而推動了對整合建築分析的強勁需求。德國P2P交易沙盒的推出以及荷蘭大力推行的熱泵獎勵,都反映了監管的廣泛性。 TPG斥資67億歐元收購Techem,也顯示了其投資意願。公共產業正在加速電網邊緣數位化,以應對可再生能源的波動,這進一步擴大了能源管理系統市場。

亞太地區是經濟成長引擎,預計將以16.05%的複合年成長率成長。中國正在投資建造超高壓輸電和人工智慧增強型發電配電中心,以平衡計畫在2030年新增的120萬千瓦風能和太陽能發電裝置容量。日本計劃在2025年向住宅和建築能源管理系統(EMS)提供40億日圓的補貼,將增強供應商儲備。印度的智慧城市計畫已將EMS要求納入公共設施和路燈網路的競標中,東南亞國家正在尋求電網穩定解決方案,以支援屋頂太陽能的快速部署。跨國公司在建立區域製造地之初就指定採用EMS,加速了待開發區的需求。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 快速部署先進測量基礎設施(AMI)

- 從2026年起,主要國家將強制執行淨零能耗建築標準。

- 人工智慧驅動的預測性維護可降低電力公司的營運成本

- 越來越多的企業購電協議(PPA)需要精細的能源數據。

- 基於區塊鏈的P2P(P2P)能源交易試點項目

- 市場限制

- 系統整合初期成本較高

- 棕地專案中遺留的OT/IT互通性差距

- 在不斷發展的關鍵基礎設施法律下的網路安全責任

- 經合組織地區以外熟練的急救醫療服務技術人員短缺

- 價值鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 按EMS類型

- 建築能源管理系統(BEMS)

- 工業電子管理系統(IEMS)

- 家庭急救服務 (HEMS)

- 最終用戶

- 製造業

- 電力和能源

- 資訊科技/通訊

- 衛生保健

- 住宅及商業地產

- 透過使用

- 能源產出

- 能源運輸

- 能源監控與最佳化

- 按組件

- 硬體

- 軟體

- 服務

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 智利

- 其他南美洲

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- ASEAN

- 亞太其他地區

- 中東和非洲

- 中東

- 海灣合作理事會(沙烏地阿拉伯、阿拉伯聯合大公國、卡達等)

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 肯亞

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Schneider Electric

- Siemens AG

- Honeywell International Inc.

- ABB Ltd.

- General Electric

- Eaton Corporation

- Rockwell Automation Inc.

- Johnson Controls

- IBM Corporation

- Oracle Corporation

- SAP SE

- Cisco Systems

- Enel X

- Autogrid Systems

- Itron Inc.

- Honeywell Smart Energy

- Mitsubishi Electric

- Yokogawa Electric

- Tendril(Uplight)

- WAGO Kontakttechnik

第7章 市場機會與未來展望

The Energy Management Systems market size reaches USD 63.64 billion in 2025 and is forecast to climb to USD 131.67 billion by 2030, advancing at a 15.65% CAGR.

The surge reflects stricter decarbonization rules, rapid smart-grid deployment, and mounting corporate net-zero targets that elevate real-time energy optimization from optional to indispensable. Utilities are rolling out advanced metering infrastructure (AMI) at scale, giving operators the granular data they need to pair with AI-driven analytics for self-healing grid functions and lower operating costs. Commercial real-estate owners face mandatory net-zero building codes starting in 2026, driving a jump in demand for connected HVAC, lighting, and controls platforms. Meanwhile, firms signing large renewable power-purchase agreements require integrated systems capable of hourly tracking, certificate management, and carbon accounting. Beyond climate policy, volatile commodity prices and growing carbon costs sharpen the economic case for the Energy Management Systems market, as enterprises chase double-digit savings and resilience against supply-side shocks.

Global Energy Management Systems Market Trends and Insights

Rapid Roll-out of Advanced Metering Infrastructure Transforms Grid Intelligence

Utilities across mature economies accelerated AMI programs in 2024, installing millions of smart meters that stream interval data to cloud analytics engines. Eversource finished a 1.3 million-meter project spanning Massachusetts and Connecticut, while National Grid connected 3.4 million endpoints in the Northeast. The data feed underpins automated demand response, outage self-healing, and predictive load forecasting, all core modules in modern Energy Management Systems market platforms. AI algorithms re-route power within seconds, cutting restoration times and trimming distribution losses. As distribution operators monetize grid services and accommodate renewables, AMI forms the essential layer linking field assets with cloud-based optimization.

Mandatory Net-Zero Building Codes Accelerate Commercial EMS Adoption

Jurisdictions such as New York City, Washington State, and California enacted rules that push large buildings toward net-zero operations, starting as early as 2026. Local Law 97 requires facilities over 25,000 ft2 to cut emissions 40% by 2030, with steep fines for non-compliance. California's Title 24 updates stipulate advanced controls and measurement, turning Energy Management Systems market deployments from voluntary upgrades into compliance necessities. Similar mandates ripple across Canada and the EU, expanding addressable demand for integrated HVAC, lighting, and renewable-ready platforms.

High Up-Front System Integration Costs Constrain SME Market Penetration

Comprehensive deployments still command USD 50,000-500,000, a hurdle for cash-constrained facilities. Hardware, integration, and training extend payback to 18-36 months, delaying adoption in small enterprises. Energy-as-a-Service subscriptions now re-cast capex as opex, lowering entry barriers; Iris Ohyama's 2025 launch of the ENEverse cloud suite typifies that pivot, bundling sensors, analytics, and remote operations into a no-hardware model.

Other drivers and restraints analyzed in the detailed report include:

- AI-Powered Predictive Maintenance Revolutionizes Utility Operations

- Corporate Power Purchase Agreements Drive Granular Energy Data Requirements

- Legacy OT/IT Interoperability Gaps Complicate Brownfield Deployments

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Building Energy Management Systems capture the largest slice of the Energy Management Systems market at 46.0% in 2024. Tighter codes, tenant sustainability reporting, and the premium on healthy indoor environments keep commercial campuses investing in advanced controls that trim 25-40% of utility spend. Home solutions post the fastest trajectory, rising at a 17.2% CAGR as rising electricity tariffs, smart-appliance penetration, and utility demand-response incentives nudge households toward voice-controlled thermostats and automated EV-charger scheduling. Integrated platforms now fuse occupancy sensors, PV inverters, and battery dispatch to create self-balancing nanogrids. Suppliers differ on architecture-edge hubs versus cloud-first-but all route data into AI engines for real-time optimization, broadening the Energy Management Systems market addressable base.

Recent advancements illustrate the shift from rule-based automation to predictive orchestration. C3.ai models combine physics-based equipment libraries with machine learning to anticipate load peaks and pre-condition HVAC for minimal energy intensity. Carrier's BluEdge Command Center streams chiller-level data to remote engineers who tweak set points in minutes, achieving double-digit savings without on-site staff. The result is a feedback loop: verified savings fund further retrofits, cementing long-term service contracts that anchor vendor revenue.

Manufacturing facilities accounted for 31.4% of Energy Management Systems market share in 2024 owing to energy bills that routinely reach 20% of operating costs. Sectors such as cement, steel, and chemicals leverage high-speed sensors and digital twins to orchestrate furnaces, compressors, and process lines, seeking every kilowatt of productivity. Nevertheless, the healthcare vertical is expanding at a 16.25% CAGR. Hospitals run 24/7, with stringent humidity and temperature thresholds, making them ideal candidates for AI-guided HVAC and boiler sequencing. Apollo Hospitals reports 30% utility savings after deploying a cloud EMS that integrates medical equipment scheduling and cogeneration controls.

Power utilities, the second-largest end-user, rely on EMS modules for demand forecasting and renewables integration. IT and telecom operators apply similar logic inside data centers where cooling loads approach 40% of total consumption. As server densities jump with AI workloads, advanced airflow modeling and liquid-cooling optimization enter mainstream facility roadmaps. Residential and commercial mixed-use complexes round out demand, driven by net-metering policies and the urge to monetize rooftop solar.

The Energy Management System Market Report is Segmented by Type of EMS (BEMS, IEMS, and HEMS), End-User (Manufacturing, Power and Energy, IT and Telecommunication, Healthcare, and Residential and Commercial), Application (Energy Generation, Energy Transmission, and Energy Monitoring), Component (Hardware, Software, and Services), and Geography.

Geography Analysis

North America retains its pole position with 35.6% of Energy Management Systems market revenue in 2024. Federal funding through the Inflation Reduction Act and state tax credits catalyze metering, EV-charging, and building-retrofit projects. Utilities such as Eversource and National Grid added millions of smart endpoints in 2024, laying the data fabric that underpins advanced analytics. Schneider Electric responded with a USD 700 million expansion across U.S. plants to localize production of switchgear, microgrid controllers, and software R&D, signalling confidence in policy stability and customer demand.

Europe follows closely, propelled by the European Green Deal and Fit-for-55 package that stipulate 55% emission cuts versus 1990 by 2030. Member states embed digital-building requirements in local codes, fostering robust demand for integrated building analytics. Germany's roll-out of P2P trading sandboxes and the Netherlands' aggressive heat-pump incentives showcase regulatory breadth. Investment appetite surfaced when TPG paid EUR 6.7 billion for Techem, attracted by recurring revenues from sub-metering and efficiency services. Utilities accelerate grid-edge digitization to handle variable renewable flows, further enlarging the Energy Management Systems market.

Asia-Pacific is the growth engine with a projected 16.05% CAGR. China invests in ultra-high-voltage transmission and AI-enhanced dispatch centers to balance its 1,200 GW of wind-solar capacity planned by 2030. Japan's subsidies for Home EMS and Building EMS, backed by JPY 4 billion earmarked in 2025, bolster vendor pipelines. India's Smart Cities Mission embeds EMS requirements in tenders for public buildings and street-lighting networks, while Southeast Asian economies seek grid-stability solutions to cope with rapid rooftop-solar adoption. Multinationals setting up regional manufacturing hubs specify EMS from day one, accelerating greenfield demand.

- Schneider Electric

- Siemens AG

- Honeywell International Inc.

- ABB Ltd.

- General Electric

- Eaton Corporation

- Rockwell Automation Inc.

- Johnson Controls

- IBM Corporation

- Oracle Corporation

- SAP SE

- Cisco Systems

- Enel X

- Autogrid Systems

- Itron Inc.

- Honeywell Smart Energy

- Mitsubishi Electric

- Yokogawa Electric

- Tendril (Uplight)

- WAGO Kontakttechnik

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid roll-out of advanced metering infrastructure (AMI)

- 4.2.2 Mandatory net-zero building codes in major economies from 2026

- 4.2.3 AI-powered predictive maintenance lowering OPEX for utilities

- 4.2.4 Growing corporate PPAs demanding granular energy data

- 4.2.5 Blockchain-enabled peer-to-peer (P2P) energy trading pilots

- 4.3 Market Restraints

- 4.3.1 High up-front system integration costs

- 4.3.2 Legacy OT/IT interoperability gaps in brownfield sites

- 4.3.3 Cyber-security liability under evolving critical-infrastructure laws

- 4.3.4 Shortage of EMS-skilled technicians outside OECD

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type of EMS

- 5.1.1 Building EMS (BEMS)

- 5.1.2 Industrial EMS (IEMS)

- 5.1.3 Home EMS (HEMS)

- 5.2 By End-User

- 5.2.1 Manufacturing

- 5.2.2 Power and Energy

- 5.2.3 IT and Telecommunication

- 5.2.4 Healthcare

- 5.2.5 Residential and Commercial

- 5.3 By Application

- 5.3.1 Energy Generation

- 5.3.2 Energy Transmission

- 5.3.3 Energy Monitoring and Optimization

- 5.4 By Component

- 5.4.1 Hardware

- 5.4.2 Software

- 5.4.3 Services

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Netherlands

- 5.5.3.7 Russia

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 ASEAN

- 5.5.4.6 Rest of Asia Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 GCC (Saudi Arabia, UAE, Qatar, etc.)

- 5.5.5.1.2 Turkey

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Kenya

- 5.5.5.2.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Schneider Electric

- 6.4.2 Siemens AG

- 6.4.3 Honeywell International Inc.

- 6.4.4 ABB Ltd.

- 6.4.5 General Electric

- 6.4.6 Eaton Corporation

- 6.4.7 Rockwell Automation Inc.

- 6.4.8 Johnson Controls

- 6.4.9 IBM Corporation

- 6.4.10 Oracle Corporation

- 6.4.11 SAP SE

- 6.4.12 Cisco Systems

- 6.4.13 Enel X

- 6.4.14 Autogrid Systems

- 6.4.15 Itron Inc.

- 6.4.16 Honeywell Smart Energy

- 6.4.17 Mitsubishi Electric

- 6.4.18 Yokogawa Electric

- 6.4.19 Tendril (Uplight)

- 6.4.20 WAGO Kontakttechnik

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

2025年全球充電站能源管理系統市場報告

2025年全球充電站能源管理系統市場報告 能源管理系統 (EMS) 市場預測(至 2032 年):按組件、解決方案、部署、應用、最終用戶和地區進行的全球分析

能源管理系統 (EMS) 市場預測(至 2032 年):按組件、解決方案、部署、應用、最終用戶和地區進行的全球分析 能源管理系統市場(按服務提供、通訊技術、能源來源整合、組織規模、部署模式和最終用途)—全球預測 2025-20322025年全球能源管理系統市場報告

能源管理系統市場(按服務提供、通訊技術、能源來源整合、組織規模、部署模式和最終用途)—全球預測 2025-20322025年全球能源管理系統市場報告 北美能源管理系統:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)

北美能源管理系統:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年) 能源管理系統 (EMS) 市場 2025-2029歐洲能源管理系統:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)

能源管理系統 (EMS) 市場 2025-2029歐洲能源管理系統:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年) 能源管理系統 (EMS) 市場 - 全球市場規模(按系統類型、應用、地區分類)預測(至 2025 年)

能源管理系統 (EMS) 市場 - 全球市場規模(按系統類型、應用、地區分類)預測(至 2025 年) 2025 年至 2033 年能源管理系統市場報告,按組件、產品(工業能源管理系統、建築能源管理系統、家庭能源管理系統)、解決方案、行業垂直、最終用途和地區分類

2025 年至 2033 年能源管理系統市場報告,按組件、產品(工業能源管理系統、建築能源管理系統、家庭能源管理系統)、解決方案、行業垂直、最終用途和地區分類 能源管理系統市場規模和預測 2021 - 2031 年,全球和區域佔有率、趨勢和成長機會分析報告範圍:按組件、系統類型、最終用途行業和地理分類

能源管理系統市場規模和預測 2021 - 2031 年,全球和區域佔有率、趨勢和成長機會分析報告範圍:按組件、系統類型、最終用途行業和地理分類