|

市場調查報告書

商品編碼

1851370

美國振動感測器市場:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)US Vibration Sensors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

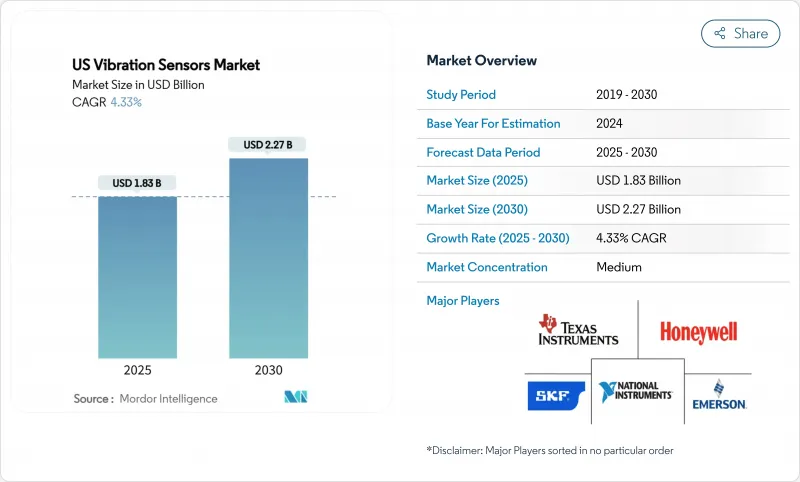

美國振動感測器市場規模預計到 2025 年將達到 18.3 億美元,到 2030 年將達到 22.7 億美元,複合年成長率為 4.33%。

隨著終端用戶採用邊緣人工智慧、無線連接和工業4.0技術,美國振動感測器市場正從銷售擴張轉向技術主導的價值創造。預測分析的普及、來自美國職業安全與健康管理局 (OSHA) 和美國石油學會 (API) 標準的合規壓力,以及減少非計劃性停機時間的需求,都支撐著市場需求的穩定成長。無線節點、能源採集設計和基於微機電系統 (MEMS) 的加速計,為老舊工業設備提供了更多部署選擇。供應商正透過提供將硬體與雲端分析相結合的整合解決方案,並建立生態系統夥伴關係關係來應對網路安全和傳統系統整合方面的挑戰,從而實現差異化競爭。

美國振動感測器市場趨勢與洞察

對預測性維護計劃的需求日益成長

美國製造業每年因計畫外停機造成的損失超過500億美元,促使企業從基於時間的維護策略轉向基於狀態的維護策略。許多工廠現在採用連續振動監測來及早發現軸承磨損和不對中,從而將設備壽命延長多達30%,同時減少備件庫存。將機器學習應用於頻譜數據,可以識別出人工分析人員可能忽略的異常情況,尤其是在存在交互機械的工廠中。風電場營運商利用這些工具預測變速箱故障,避免了400萬至500萬歐元(430萬至540萬美元)的生產損失。早期應用的成功推動了該技術在汽車、金屬和食品加工行業的廣泛部署。

工業物聯網(IIoT)賦能的無線振動節點日益普及

無線監測無需佈線,並將覆蓋範圍擴展到以往難以觸及的資產。 LoRaWAN 網路的資料傳輸距離超過 15 公里,已被證明適用於遠端環境感測。動力來源環境振動和熱量供電的能源採集裝置無需更換電池,從而節省了傳統電池成本。貝克休斯公司的 Ranger Pro 感測器已核准在全球危險區域使用,並為石油和天然氣營運商提供企業級狀態監測的典範。其部署週期短,可輕鬆納入計畫維護窗口,並支援快速計算投資報酬率。

與舊機器的整合問題

許多設施仍然依賴幾十年前生產的設備,這些設備缺乏標準化的感測器安裝座和通訊連接埠。改裝是為新設備安裝感測器的三到五倍。老舊機架的共振效應會影響訊號保真度,並且需要客製化夾具,從而增加工時。多代專有通訊協定需要閘道器,這會增加資本投入和網路安全風險。 Analog Devices 的 Voyager4 平台提供自適應安裝座和節點上 AI,可以克服這些障礙,但價格敏感性正在減緩其普及速度。

細分市場分析

2024年,加速計貨量將佔總出貨量的45.1%,這充分展現了其在各個頻寬的通用性。速度感測器由於能夠及早偵測大型旋轉設備的低頻故障,其複合年成長率將達到7.81%,成為市場成長最快的產品。多參數裝置整合了加速度、速度和溫度訊息,簡化了安裝流程並降低了整體擁有成本。 Analog Devices公司正在將邊緣人工智慧整合到這些裝置中,實現節點內故障分類,從而降低網路頻寬。水力發電廠和紙漿造紙廠對速度感測技術的日益廣泛應用,也推動了美國振動感測器市場的多元化發展。

第二個成長要素是輪胎和變速箱測試的擴展,其中三軸加速計用於追蹤複雜的動態負荷。接近式探頭雖然仍處於小眾市場,但對於非接觸式渦輪機應用至關重要。轉速表作為變速驅動器階次分析的參考儀器,仍具有重要價值。隨著工廠數位化,資產健康平台正在整合所有產品類型的數據,這不僅擴大了美國振動感測器市場的硬體利潤空間,還產生了服務費,從而加強了供應商與客戶之間的聯繫。

由於有線數位系統可靠性久經考驗且現有電纜配線架可用,預計到 2024 年,有線數位系統將佔總收入的 61.3%。然而,無線節點將因電池壽命的提升和無線穩定性的增強而以每年 9.23% 的速度成長。 LoRaWAN 將透過單一閘道器實現公里級覆蓋範圍,並支援分散式太陽能發電廠。混合電源加無線架構將在製藥無塵室中應用,因為在這些場所,執行時間和污染控制至關重要。能源採集技術將消除維護難題,並拓展應用場景,例如在迴轉窯中,滑環會增加成本和複雜性。

資料二極體功能和 AES-256 加密技術緩解了以往有線配置所面臨的網路安全隱患。無線韌體更新允許操作人員在無需實體存取的情況下修復漏洞。 ISA100 和 IEC 62938 標準化促進了不同廠商之間的互通性,從而拓展了美國振動感測器市場的生態系統。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 對預測性維護計劃的需求日益成長

- 相容於工業物聯網的無線振動節點正變得越來越普及。

- 採用基於EMS的低成本加速感應器

- 危險產業面臨的 OSHA 和 API 合規壓力

- 邊緣人工智慧分析釋放新的價值池

- 汽車電氣化推動高頻振動感測技術的發展

- 市場限制

- 遺留整合問題

- I類/II區本質安全型感測器短缺

- 連網感測器帶來的網路安全風險

- 壓電陶瓷材料供應鏈的波動

- 價值鏈分析

- 監管現狀和標準

- 技術展望

- 波特五力分析

- 新進入者的威脅

- 替代品的威脅

- 供應商的議價能力

- 買方的議價能力

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 依產品類型

- 加速計

- 近距離探針

- 轉速表

- 速度感測器

- 其他

- 透過感測器技術

- 有線(類比/數位)

- 無線(BLE、LoRa、Wi-Fi)

- 感測材料/原理

- 壓電

- MEMS(電容式/壓阻式)

- 磁致伸縮

- 光纖

- 按最終用戶行業分類

- 車

- 航太/國防

- 石油和天然氣

- 金屬和採礦

- 發電

- 衛生保健

- 消費性電子產品

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Analog Devices Inc.

- Texas Instruments Incorporated

- Honeywell International Inc.

- Emerson Electric Co.

- Rockwell Automation Inc.

- SKF USA Inc.

- PCB Piezotronics(MTS Systems)

- TE Connectivity Ltd.

- Wilcoxon Sensing Technologies(Amphenol)

- Siemens Digital Industries USA

- STMicroelectronics Inc.

- Bosch Sensortec GmbH

- KCF Technologies Inc.

- Banner Engineering Corp.

- Fluke Corporation

- Baker Hughes(Bently Nevada)

- Meggitt PLC(Endevco)

- Omron Corporation

- National Instruments Corp.

- Hansford Sensors Ltd.

第7章 市場機會與未來展望

The United States vibration sensors market size reached USD 1.83 billion in 2025 and is forecast to reach USD 2.27 billion by 2030, reflecting a 4.33% CAGR.

The United States vibration sensors market is moving from volume expansion toward technology-driven value creation as end users adopt edge AI, wireless connectivity, and Industry 4.0 practices. Uptake of predictive analytics, compliance pressures from OSHA and API standards, and the need to limit unplanned downtime underpin steady demand growth. Wireless nodes, energy-harvesting designs, and MEMS-based accelerometers broaden deployment options across aging industrial assets. Suppliers differentiate through integrated solutions that bundle hardware with cloud analytics while forming ecosystem partnerships to address cybersecurity and legacy-system integration challenges.

US Vibration Sensors Market Trends and Insights

Rising Demand for Predictive-Maintenance Programs

Unplanned downtime costs exceed USD 50 billion each year across U.S. manufacturing, prompting a shift from time-based to condition-based maintenance strategies. Many plants now deploy continuous vibration monitoring that detects bearing wear and misalignment early, extending asset life by as much as 30% while cutting spare-parts inventory. Machine learning applied to spectral data identifies anomalies that human analysts can miss, especially in facilities with interacting machines. Wind-farm operators using these tools have avoided lost production valued at EUR 4-5 million (USD 4.3-5.4 million) by predicting gearbox failures. Early adoption success is accelerating broader rollouts across automotive, metals, and food-processing sites.

IIoT-Enabled Wireless Vibration Nodes Gaining Traction

Wireless monitoring eliminates cable routing and allows coverage of assets once considered unreachable. LoRaWAN networks transmit data more than 15 kilometers, proven in remote environmental sensing. Energy-harvesting devices powered by ambient vibration or heat remove battery-change labor, addressing previous cost barriers. Baker Hughes' Ranger Pro sensor, approved for global hazardous areas, provides a template for oil and gas operators pursuing enterprise-wide condition monitoring. Short deployment times fit scheduled maintenance windows, supporting rapid ROI calculations.

Integration Issues with Legacy Machinery

Many facilities rely on equipment built decades ago without standardized sensor mounts or communication ports. Retrofitting can cost three to five times more than installing sensors on new assets. Resonance effects in older frames complicate signal fidelity and demand custom fixtures that add labor hours. Multiple generations of proprietary protocols require gateways that increase capex and cybersecurity exposure. Analog Devices' Voyager4 platform offers adaptive mounting and on-node AI to counter these hurdles, though price sensitivity slows adoption.

Other drivers and restraints analyzed in the detailed report include:

- Accelerating Adoption of MEMS-Based Low-Cost Accelerometers

- OSHA and API Compliance Pressures in Hazardous Industries

- Shortage of Intrinsically Safe Sensors for Class I/Div II Zones

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Accelerometers represented 45.1% of 2024 shipments, underlining their versatility across frequency ranges. Velocity sensors post the highest 7.81% CAGR as they capture low-frequency faults earlier in large rotating equipment. Multi-parameter devices combine acceleration, velocity, and temperature to simplify installation and reduce total cost of ownership. Analog Devices integrates edge AI in such packages, allowing on-node fault classification that trims network bandwidth. Growing use of velocity sensing in hydropower and pulp-and-paper plants supports revenue diversity within the United States vibration sensors market.

The second growth driver lies in expanding tire and gearbox testing where triaxial accelerometers track compound dynamic loads. Proximity probes, though niche, remain indispensable in non-contact turbine applications. Tachometers retain value as reference instruments for order analysis in variable-speed drives. As plants digitize, asset-health platforms ingest data from all product types, creating service fees that augment hardware margins and strengthen supplier-customer ties within the United States vibration sensors market.

Wired digital systems delivered 61.3% of 2024 revenue thanks to proven reliability and existing cable trays. However, wireless nodes grow 9.23% annually as battery life and radio resilience improve. LoRaWAN achieves kilometer-scale reach on single gateways, supporting distributed solar farms. Hybrid power-plus-wireless architectures appear in pharmaceutical cleanrooms where uptime and contamination control are paramount. Energy harvesting addresses maintenance pain points and expands use cases such as rotating kilns where slip rings add cost and complexity.

Data-diode features and AES-256 encryption mitigate cybersecurity concerns that once favored wired setups. Firmware-over-air updates let operators patch vulnerabilities without physical access. Standardization under ISA100 and IEC 62938 promotes interoperability across vendors, broadening the ecosystem for the United States vibration sensors market.

The United States Vibration Sensors Market Report is Segmented by Product Type (Accelerometers, Proximity Probes, Tachometers, Velocity Sensors, Others), Sensor Technology (Wired, Wireless), Sensing Material/Principle (Piezoelectric, MEMS, Magnetostrictive, Fiber-Optic), End-User Industry (Automotive, Aerospace and Defense, Oil and Gas, Metals and Mining, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Analog Devices Inc.

- Texas Instruments Incorporated

- Honeywell International Inc.

- Emerson Electric Co.

- Rockwell Automation Inc.

- SKF USA Inc.

- PCB Piezotronics (MTS Systems)

- TE Connectivity Ltd.

- Wilcoxon Sensing Technologies (Amphenol)

- Siemens Digital Industries USA

- STMicroelectronics Inc.

- Bosch Sensortec GmbH

- KCF Technologies Inc.

- Banner Engineering Corp.

- Fluke Corporation

- Baker Hughes (Bently Nevada)

- Meggitt PLC (Endevco)

- Omron Corporation

- National Instruments Corp.

- Hansford Sensors Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for predictive-maintenance programs

- 4.2.2 IIoT-enabled wireless vibration nodes gaining traction

- 4.2.3 Accelerating adoption of MEMS-based low-cost accelerometers

- 4.2.4 OSHA and API compliance pressures in hazardous industries

- 4.2.5 Edge-AI analytics unlocking new value pools (under-reported)

- 4.2.6 Vehicle electrification driving high-frequency vibration sensing (under-reported)

- 4.3 Market Restraints

- 4.3.1 Integration issues with legacy machinery

- 4.3.2 Shortage of intrinsically safe sensors for Class I/Div II zones

- 4.3.3 Cyber-security risks from connected sensors (under-reported)

- 4.3.4 Supply-chain volatility in piezo-ceramic materials (under-reported)

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape and Standards

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Threat of Substitutes

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Bargaining Power of Buyers

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Product Type

- 5.1.1 Accelerometers

- 5.1.2 Proximity Probes

- 5.1.3 Tachometers

- 5.1.4 Velocity Sensors

- 5.1.5 Others

- 5.2 By Sensor Technology

- 5.2.1 Wired (Analog/Digital)

- 5.2.2 Wireless (BLE, LoRa, Wi-Fi)

- 5.3 By Sensing Material / Principle

- 5.3.1 Piezoelectric

- 5.3.2 MEMS (Capacitive/Piezoresistive)

- 5.3.3 Magnetostrictive

- 5.3.4 Fiber-Optic

- 5.4 By End-user Industry

- 5.4.1 Automotive

- 5.4.2 Aerospace and Defense

- 5.4.3 Oil and Gas

- 5.4.4 Metals and Mining

- 5.4.5 Power Generation

- 5.4.6 Healthcare

- 5.4.7 Consumer Electronics

- 5.4.8 Other End-user Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Analog Devices Inc.

- 6.4.2 Texas Instruments Incorporated

- 6.4.3 Honeywell International Inc.

- 6.4.4 Emerson Electric Co.

- 6.4.5 Rockwell Automation Inc.

- 6.4.6 SKF USA Inc.

- 6.4.7 PCB Piezotronics (MTS Systems)

- 6.4.8 TE Connectivity Ltd.

- 6.4.9 Wilcoxon Sensing Technologies (Amphenol)

- 6.4.10 Siemens Digital Industries USA

- 6.4.11 STMicroelectronics Inc.

- 6.4.12 Bosch Sensortec GmbH

- 6.4.13 KCF Technologies Inc.

- 6.4.14 Banner Engineering Corp.

- 6.4.15 Fluke Corporation

- 6.4.16 Baker Hughes (Bently Nevada)

- 6.4.17 Meggitt PLC (Endevco)

- 6.4.18 Omron Corporation

- 6.4.19 National Instruments Corp.

- 6.4.20 Hansford Sensors Ltd.

7 MARKET OPPORTUNITIES and FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

振動感測器市場:按類型、頻率範圍、安裝配置、軸配置、輸出方式、應用和最終用戶產業分類-2026-2032年全球市場預測

振動感測器市場:按類型、頻率範圍、安裝配置、軸配置、輸出方式、應用和最終用戶產業分類-2026-2032年全球市場預測 全球振動感測器市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球振動感測器市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年全球振動感測器市場報告超音波振動感測器市場按技術、產品類型、頻率範圍、應用、最終用戶和銷售管道,全球預測(2026-2032年)

2026年全球振動感測器市場報告超音波振動感測器市場按技術、產品類型、頻率範圍、應用、最終用戶和銷售管道,全球預測(2026-2032年) 2025-2033年振動感測器市場報告(按產品、技術、材料、最終用途產業和地區)

2025-2033年振動感測器市場報告(按產品、技術、材料、最終用途產業和地區) 振動感測器:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)

振動感測器:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年) 2032 年振動感測器市場預測:按類型、監測流程、設備、材料、網路、技術、最終用戶和地區進行的全球分析2032 年無線振動感測器市場預測:按感測器類型、應用和地區進行的全球分析

2032 年振動感測器市場預測:按類型、監測流程、設備、材料、網路、技術、最終用戶和地區進行的全球分析2032 年無線振動感測器市場預測:按感測器類型、應用和地區進行的全球分析 振動感測器市場規模、佔有率和成長分析(按類型、監測過程、訊號、設備、技術、材料、垂直產業和地區)- 2025-2032 年產業預測中東和非洲的振動感測器:市場佔有率分析、產業趨勢和成長預測(2025-2030)

振動感測器市場規模、佔有率和成長分析(按類型、監測過程、訊號、設備、技術、材料、垂直產業和地區)- 2025-2032 年產業預測中東和非洲的振動感測器:市場佔有率分析、產業趨勢和成長預測(2025-2030)