|

市場調查報告書

商品編碼

1939073

超級電容:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Supercapacitors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

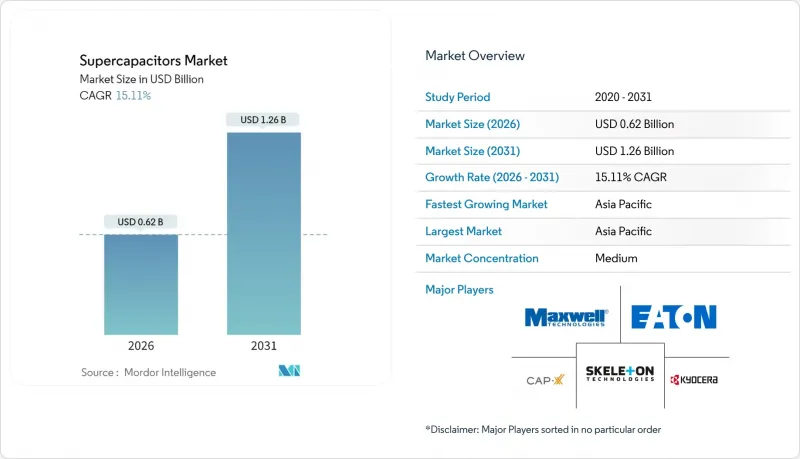

超級電容市場預計將從 2025 年的 5.4 億美元成長到 2026 年的 6.2 億美元,到 2031 年將達到 12.6 億美元,2026 年至 2031 年的複合年成長率為 15.11%。

這項成長主要受以下因素驅動:電氣化法規,例如歐盟的48伏輕度混合動力汽車強制令;人工智慧(AI)需求成長帶動資料中心對不斷電系統(UPS)的需求不斷成長;以及將電池和超級電容相結合以實現快速頻率響應的電網現代化計劃。中國繼續保持其作為生產和研發中心的地位,而隨著鋰離子電池市場佔有率的下降,韓國製造商正將重心轉向能源儲存系統。產品創新主要集中在將能量密度提升至接近電池等級的混合動力設計,以及用於製造超薄穿戴裝置的石墨烯電極。活性碳價格和離子液體電解質相關的供應鏈風險限制了短期利潤率,但也推動了地域多角化。

全球超級電容市場趨勢與洞察

電動公車隊快速採用超級電容模組進行再生煞車

城市交通系統正日益普及結合電池和超級電容的再生煞車系統,與純電池系統相比,動能可提高高達85%。賓士的Inturo混合動力公車採用48伏特超級電容組,可承受數百萬次充放電循環而不劣化,進而降低5%的油耗。中國城市率先採用這項技術,目前正將混合動力汽車停車場連接到電網,用於車輛充電和電網穩定服務。系統供應商正在整合演算法,以控制超級電容和電池之間的功率轉換,使其與線路地形相匹配,從而降低整體擁有成本。隨著電動公車採購量的成長,這項特性增強了超級電容在公共運輸電氣化領域的市場競爭力。

電網級電池-超級電容混合儲能系統

電力公司看重超級電容的瞬時頻率調節能力。示範測試表明,與獨立的鋰離子電池組相比,超級電容器可將頻率下降降低17.43%,經濟效益是純電池方案的3.2倍。美國能源局預測,隨著電池生產自動化程度的提高,到2030年,儲能的平準化成本將達到每度電0.337美元。此外,電力公司也重視超級電容的環境優勢,因為它們不含鈷或鎳。這些因素正推動超級電容市場發展成為電網的關鍵資源,在可再生能源佔比高的場景中,超級電容器可與長時電池儲能形成互補。

認證差距(IEC 62391)限制了住宅應用

IEC 62391 測試程序延長了認證時間並增加了成本,尤其對中小企業而言更是如此。對比研究表明,該標準比 Maxwell 和 QC/T 741-2014通訊協定耗時更長,導致產品上市延遲長達 12 個月。此外,該標準過度強調高電流測試,這與典型的住宅用電模式不符。這一行政障礙阻礙了超級電容在住宅儲能領域的市場滲透,而簡化的合格評定流程本來可以創造新的市場需求。

細分市場分析

鑑於其成熟的生產線和在工業功率緩衝領域久經考驗的耐用性,電動超級電容器將在2025年保持54.62%的超級電容市場佔有率。混合型超級電容融合了類似電池的儲能特性和傳統電容器的功率輸出特性,預計到2031年將達到17.62%的複合年成長率。這種混合型方案滿足了原始設備製造商(OEM)對能夠承受數秒電壓驟降並保持更長放電曲線的設備的需求。

鋰離子電容器技術的快速研發正在縮小能量密度差距,並擴大動作溫度範圍。在汽車逆變器和併網系統中的先導計畫已證明,混合型超級電容器的循環壽命超過一百萬次。這些特性使混合型超級電容器成為超級電容行業的下一個性能標竿。

模組化組件,得益於整合的平衡電路以及與公車、起重機和風力發電機的即插即用相容性,將在2025年佔據超級電容市場57.12%的佔有率。然而,在電網營運商和電動車製造商向更高電壓堆(超過800V)發展趨勢的推動下,電池組配置預計將以每年16.95%的速度成長。到2031年,受電力公司採用亞秒頻率響應技術的推動,電池組級超級電容的市場規模可能會翻倍。

在穿戴式裝置和工業控制器領域,電池產品仍然具有重要意義,因為基板級整合和成本仍然是關鍵因素。供應商現在提供模組化架構,可以以 50 伏特為增量擴展能量容量,從而縮短計劃設計週期。先進的溫度控管功能進一步拓展了其在嚴苛環境下的應用。

區域分析

到2025年,中國將佔全球超級電容器市場收入的27.88%,這主要得益於其在活性碳加工領域的規模優勢和深厚的研究基礎,中國發表了65.4%的高影響力論文。國內電動車製造商和國家支持的電網計劃帶來的需求正在支撐市場規模的成長。國家優先發展國內儲能技術的政策也進一步強化了超級電容市場的供應鏈生態系統。

預計到2031年,韓國及全部區域的複合年成長率將達到15.96%,主要得益於LG能源解決方案、三星SDI和SK安等公司超過200億美元的新增產能投資。韓國企業正利用電極塗層技術為北美公用事業公司開發組件級儲能系統。日本為高可靠性汽車模組提供精密製造技術,而東南亞國家則吸引尋求供應鏈多元化的組裝廠。

美國正利用《通膨控制法案》的激勵措施,促進生產在地化,並推動超大規模資料中心採用基於超級電容的UPS設備。歐洲仍以監管主導,歐7法規結構刺激了汽車需求,電網現代化基金則支持混合儲能先導工廠。拉丁美洲和中東等新興地區正在試用超級電容組來穩定微電網,預示著超級電容市場具有長期成長潛力。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 電動公車隊快速採用超級電容模組進行再生煞車

- 電網級電池-超級電容混合儲能系統

- 石墨烯電極技術的創新使超薄穿戴裝置成為可能

- 歐盟48V輕混動力系統強制令推動了對12-48V模組的需求。

- 資料中心超大規模資料中心業者採用基於超級電容的UPS來實現ESG目標

- 市場限制

- 活性碳前驅體的價格波動推高了組件成本。

- 認證差距(IEC 62391)限制了其在住宅領域的應用。

- 能量密度平台期(約 10 Wh/kg)限制了長續航力電動車的普及。

- 離子液體電解質供應鏈中的瓶頸導致前置作業時間延長

- 監管與技術展望(電極材料、容量額定值、電解液、電壓範圍)

- 宏觀經濟因素和貿易關稅的影響

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 投資與資金籌措分析

第5章 市場規模與成長預測

- 依成分(類型)

- 雙電層電容器(EDLC)

- 贗電容器

- 混合型超級電容

- 按外形規格

- 細胞

- 模組

- 包裹

- 依安裝類型(分立元件)

- 表面黏著技術

- 徑向引線

- 卡扣式

- 螺絲端子

- 按最終用戶行業分類

- 家用電子電器

- 穿戴式裝置

- 智慧型手機和平板電腦

- SSD 和記憶體備份

- 能源與公共產業

- 電網頻率調整

- 可再生能源併網(風能、太陽能)

- 微電網和不斷電系統(UPS)

- 工業設備

- 機器人與自動化

- 電動工具

- 重型機械和起重機

- 汽車和運輸設備

- 搭乘用車

- 48V輕混

- 啟停式微混合動力

- 商用車輛

- 公車

- 追蹤

- 鐵路和路面電車

- 航空航太太空產業

- 搭乘用車

- 資料中心和通訊

- 國防與航太

- 其他(醫療設備、農業無人機)

- 家用電子電器

- 按地區

- 美國

- 歐洲

- 中國

- 日本

- 韓國及其他亞太地區

- 世界其他地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Maxwell Technologies Inc.(Tesla)

- Skeleton Technologies SA

- CAP-XX Ltd.

- Eaton Corporation plc

- Panasonic Holdings Corp.

- LS Mtron Ltd.

- Kyocera Corp.

- Nippon Chemi-Con Corp.

- Supreme Power Solutions Co.

- Shanghai Aowei Technology Development Co.

- Samwha capacitor Group

- Nanoramic Laboratories(FastCAP)

- Nawa Technologies SAS

- Cornell Dubilier Electronics Inc.

- Toyo capacitor Co.

- Shenzhen Topmay Electronic Co.

- Liaoning Brother Electronics Technology Co.

- Chengdu ZT-Energy Tech Co.

- Loxus Inc.

- Nantong Jianghai capacitor Co. Ltd

- Beijing HCC Energy

- Jinzhou Kaimei Power Co. Ltd(KAM)

- Shanghai Green Tech Co. Ltd(GTCAP)

- Shenzhen Topmay Electronic Co. Ltd

- SEMG(Seattle Electronics Manufacturing Group(HK)Co. Ltd)

- Shanghai Pluspark Electronics Co. Ltd

第7章 市場機會與未來展望

The supercapacitors market is expected to grow from USD 0.54 billion in 2025 to USD 0.62 billion in 2026 and is forecast to reach USD 1.26 billion by 2031 at 15.11% CAGR over 2026-2031.

Growth is supported by electrification rules such as the European Union's 48-volt mild-hybrid mandate, datacenter demand for uninterruptible power during artificial-intelligence (AI) surges, and grid-modernization projects that blend batteries with supercapacitors for rapid frequency response. China continues to anchor production and research, while Korean manufacturers pivot toward energy-storage systems as their lithium-ion share slips. Product innovation centres on hybrid designs that lift energy density toward battery-like levels and graphene electrodes that enable ultra-thin wearables. Supply-chain risks around activated-carbon prices and ionic-liquid electrolytes temper near-term margins but also encourage regional diversification.

Global Supercapacitors Market Trends and Insights

Rapid adoption of regenerative-braking supercapacitor modules in e-bus fleets

Urban transit agencies are scaling regenerative-braking systems that pair batteries with supercapacitors, recovering up to 85% more kinetic energy than battery-only setups. Mercedes-Benz's Intouro hybrid bus cut fuel use by 5% using a 48-volt supercapacitor pack that endures millions of charge cycles without degradation. Chinese cities were first movers and now link hybrid depots to the grid for both vehicle charging and grid-stability services. System suppliers integrate algorithms that shift power between supercapacitors and batteries to match route topography, which lowers total cost of ownership. As electric-bus procurements rise, this capability strengthens the competitive position of the supercapacitors market in mass-transit electrification.

Grid-scale battery-supercapacitor hybrid storage

Utilities value supercapacitors for instant frequency regulation. Demonstrations showed a 17.43% reduction in frequency-drop rates versus standalone lithium-ion arrays, delivering economic benefits 3.2-times greater than battery-only solutions. The U.S. Department of Energy projects levelized storage costs of USD 0.337 per kWh by 2030 as automated cell production scales. Operators also cite environmental advantages because supercapacitors avoid cobalt and nickel. These factors position the supercapacitors market as an essential grid-forming resource that complements long-duration batteries under high-renewable penetration scenarios.

Certification gaps (IEC 62391) limiting residential adoption

IEC 62391 testing procedures prolong qualification timelines and raise costs, especially for smaller firms. Comparative studies show the standard takes longer than Maxwell and QC/T 741-2014 protocols, stretching product launches by up to 12 months. The heavy focus on high-current testing is mismatched with typical household power profiles. This administrative hurdle slows the supercapacitors market from penetrating residential energy-storage segments where simplified compliance would unlock new demand.

Other drivers and restraints analyzed in the detailed report include:

- Graphene-based electrode breakthroughs enabling ultra-thin wearables

- EU 48 V mild-hybrid mandate accelerating demand for 12-48 V modules

- Energy-density plateau (~10 Wh/kg) restricting long-range EV penetration

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Electric Double-Layer Capacitors maintained a 54.62% share of the supercapacitors market in 2025, reflecting established production lines and proven durability in industrial power buffering. Hybrid Supercapacitors are on track for an 17.62% CAGR to 2031 as they merge battery-like energy storage with classic capacitor power delivery. The hybrid approach answers OEM calls for devices that can ride through seconds-long voltage dips and also sustain longer discharge profiles.

Rapid R&D advances, including lithium-ion capacitor variants, narrow the energy-density gap and extend operating temperatures. Pilot projects in automotive inverters and grid-forming systems showcase cycle lifetimes beyond one million cycles. These traits position hybrids as the next performance benchmark within the supercapacitors industry.

Module assemblies captured 57.12% of the supercapacitors market in 2025 thanks to integrated balancing circuitry and drop-in compatibility for buses, cranes, and wind turbines. Pack configurations, however, are projected to grow 16.95% annually as grid operators and EV makers opt for higher-voltage stacks that exceed 800 V. The supercapacitors market size for pack-level products could double by 2031 as utilities deploy them for sub-second frequency response.

Cell products retain relevance in wearables and industrial controllers where board-level integration and cost sensitivity remain critical. Vendors now offer modular architectures that let customers scale energy in 50-volt increments, shortening project design cycles. Advanced thermal-management features further widen adoption across harsh-duty environments.

The Supercapacitors Market Report is Segmented by Configuration (Type) (Electric Double-Layer Capacitors (EDLC), Pseudo Capacitors, and Hybrid Supercapacitors), Form Factor (Cell, Module, and Pack), Mounting Type (Discrete Components) (Surface-Mount, Radial Leaded, Snap-In, and More), End-User Industry (Consumer Electronics, Energy and Utilities, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

China controlled 27.88% of global revenue in 2025 due to scale in activated-carbon processing and a deep research base that publishes 65.4% of high-impact papers. Domestic demand from electric-vehicle makers and state-backed grid projects underpins volume growth. State policies that prioritise local energy-storage content further entrench supply-chain ecosystems for the supercapacitors market.

Korea and the broader Asia region are set for a 15.96% CAGR through 2031, propelled by LG Energy Solution, Samsung SDI, and SK On investments that exceed USD 20 billion in new capacity. Korean firms channel expertise in electrode coatings toward pack-level storage systems aimed at North American utilities. Japan contributes precision manufacturing for high-reliability automotive modules, while Southeast Asian nations attract assembly plants seeking diversified supply bases.

The United States leverages Inflation Reduction Act incentives to localise production and deploy supercapacitor-based UPS units in hyperscale datacenters. Europe remains regulation-driven, with the Euro 7 framework spurring automotive demand and grid-modernization funds supporting hybrid storage pilot plants. Emerging regions in Latin America and the Middle East trial supercapacitor packs for microgrid stability, signalling long-term addressable growth for the supercapacitors market.

List of Companies Covered in this Report:

- Maxwell Technologies Inc. (Tesla)

- Skeleton Technologies SA

- CAP-XX Ltd.

- Eaton Corporation plc

- Panasonic Holdings Corp.

- LS Mtron Ltd.

- Kyocera Corp.

- Nippon Chemi-Con Corp.

- Supreme Power Solutions Co.

- Shanghai Aowei Technology Development Co.

- Samwha capacitor Group

- Nanoramic Laboratories (FastCAP)

- Nawa Technologies SAS

- Cornell Dubilier Electronics Inc.

- Toyo capacitor Co.

- Shenzhen Topmay Electronic Co.

- Liaoning Brother Electronics Technology Co.

- Chengdu ZT-Energy Tech Co.

- Loxus Inc.

- Nantong Jianghai capacitor Co. Ltd

- Beijing HCC Energy

- Jinzhou Kaimei Power Co. Ltd (KAM)

- Shanghai Green Tech Co. Ltd (GTCAP)

- Shenzhen Topmay Electronic Co. Ltd

- SEMG (Seattle Electronics Manufacturing Group (HK) Co. Ltd)

- Shanghai Pluspark Electronics Co. Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid adoption of regenerative-braking supercapacitor modules in e-bus fleets

- 4.2.2 Grid-scale battery-supercapacitor hybrid storage

- 4.2.3 Graphene-based electrode breakthroughs enabling ultra-thin wearables

- 4.2.4 EU 48 V mild-hybrid mandate accelerating demand for 12-48 V modules

- 4.2.5 Supercapacitor-based UPS deployment by Datacenter hyperscalers to meet ESG targets

- 4.3 Market Restraints

- 4.3.1 Activated-carbon precursor price volatility inflating BOM costs

- 4.3.2 Certification gaps (IEC 62391) limiting the residential adoption

- 4.3.3 Energy-density plateau (~10 Wh/kg) restricting long-range EV penetration

- 4.3.4 Ionic-liquid electrolyte supply-chain bottlenecks elongating lead-times

- 4.4 Regulatory and Technological Outlook (Electrode Material, CAsia-Pacificitance Ratings, Electrolyte, Voltage Range)

- 4.5 Impact of Macroeconomic Factors and Trade Tarrifs

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Investment and Funding Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Configuration (Type)

- 5.1.1 Electric Double-Layer Capacitors (EDLC)

- 5.1.2 Pseudocapacitors

- 5.1.3 Hybrid Supercapacitors

- 5.2 By Form Factor

- 5.2.1 Cell

- 5.2.2 Module

- 5.2.3 Pack

- 5.3 By Mounting Type (Discrete Components)

- 5.3.1 Surface-Mount

- 5.3.2 Radial Leaded

- 5.3.3 Snap-in

- 5.3.4 Screw Terminal

- 5.4 By End-User Industry

- 5.4.1 Consumer Electronics

- 5.4.1.1 Wearables

- 5.4.1.2 Smartphones and Tablets

- 5.4.1.3 SSD and Memory Backup

- 5.4.2 Energy and Utilities

- 5.4.2.1 Grid Frequency Regulation

- 5.4.2.2 Renewable Integration (Wind, Solar)

- 5.4.2.3 Microgrid and UPS

- 5.4.3 Industrial Equipment

- 5.4.3.1 Robotics and Automation

- 5.4.3.2 Power Tools

- 5.4.3.3 Heavy Machinery and Cranes

- 5.4.4 Automotive and Transportation

- 5.4.4.1 Passenger Cars

- 5.4.4.1.1 48 V Mild Hybrid

- 5.4.4.1.2 Start-Stop Micro Hybrid

- 5.4.4.2 Commercial Vehicles

- 5.4.4.2.1 Buses

- 5.4.4.2.2 Trucks

- 5.4.4.3 Rail and Tram

- 5.4.4.4 Aviation and Aerospace

- 5.4.4.1 Passenger Cars

- 5.4.5 Data Centers and Telecom

- 5.4.6 Defense and Space

- 5.4.7 Others (Medical Devices, Agri-drones)

- 5.4.1 Consumer Electronics

- 5.5 By Geography

- 5.5.1 United States

- 5.5.2 Europe

- 5.5.3 China

- 5.5.4 Japan

- 5.5.5 Korea and Rest of Asia-Pacific

- 5.5.6 Rest of the World

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Maxwell Technologies Inc. (Tesla)

- 6.4.2 Skeleton Technologies SA

- 6.4.3 CAP-XX Ltd.

- 6.4.4 Eaton Corporation plc

- 6.4.5 Panasonic Holdings Corp.

- 6.4.6 LS Mtron Ltd.

- 6.4.7 Kyocera Corp.

- 6.4.8 Nippon Chemi-Con Corp.

- 6.4.9 Supreme Power Solutions Co.

- 6.4.10 Shanghai Aowei Technology Development Co.

- 6.4.11 Samwha capacitor Group

- 6.4.12 Nanoramic Laboratories (FastCAP)

- 6.4.13 Nawa Technologies SAS

- 6.4.14 Cornell Dubilier Electronics Inc.

- 6.4.15 Toyo capacitor Co.

- 6.4.16 Shenzhen Topmay Electronic Co.

- 6.4.17 Liaoning Brother Electronics Technology Co.

- 6.4.18 Chengdu ZT-Energy Tech Co.

- 6.4.19 Loxus Inc.

- 6.4.20 Nantong Jianghai capacitor Co. Ltd

- 6.4.21 Beijing HCC Energy

- 6.4.22 Jinzhou Kaimei Power Co. Ltd (KAM)

- 6.4.23 Shanghai Green Tech Co. Ltd (GTCAP)

- 6.4.24 Shenzhen Topmay Electronic Co. Ltd

- 6.4.25 SEMG (Seattle Electronics Manufacturing Group (HK) Co. Ltd)

- 6.4.26 Shanghai Pluspark Electronics Co. Ltd

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

SMD超級電容市場按電壓範圍、產品類型、電解液類型、銷售管道、應用和終端用戶產業分類-全球預測(2026-2032年)超級電容材料市場(按電極材料類型、電解質類型、結構類型、封裝類型和最終用途分類)-2026-2032年全球預測

SMD超級電容市場按電壓範圍、產品類型、電解液類型、銷售管道、應用和終端用戶產業分類-全球預測(2026-2032年)超級電容材料市場(按電極材料類型、電解質類型、結構類型、封裝類型和最終用途分類)-2026-2032年全球預測 全球超級電容材料市場預測(至2032年):依材料類型、裝置配置、最終用戶和地區分類

全球超級電容材料市場預測(至2032年):依材料類型、裝置配置、最終用戶和地區分類 日本超級電容器市場報告(按產品類型、模組類型、材料類型、最終用途產業和地區分類,2026-2034年)

日本超級電容器市場報告(按產品類型、模組類型、材料類型、最終用途產業和地區分類,2026-2034年) 全球超級電容器市場:按類型、電極材料、電容、產業和地區劃分 - 產業動態、市場規模、機會分析和預測(2026-2035 年)

全球超級電容器市場:按類型、電極材料、電容、產業和地區劃分 - 產業動態、市場規模、機會分析和預測(2026-2035 年) 超級電容電池市場規模、佔有率和成長分析(按產品類型、材料類型、容量、應用、最終用戶和地區分類)-2026-2033年產業預測

超級電容電池市場規模、佔有率和成長分析(按產品類型、材料類型、容量、應用、最終用戶和地區分類)-2026-2033年產業預測 超級電容市場規模、佔有率和成長分析(按類型、應用、額定電壓和地區分類)-2026-2033年產業預測

超級電容市場規模、佔有率和成長分析(按類型、應用、額定電壓和地區分類)-2026-2033年產業預測 超級電容器材料市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)

超級電容器材料市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年) 超級電容器市場-全球產業規模、佔有率、趨勢、機會和預測(按最終用戶、類型、地區和競爭格局分類,2020-2030 年)超級電容器市場:按類型、電容、材料、安裝方式、終端用戶產業、國家及地區分類-全球產業分析、市場規模、市場佔有率及2025-2032年預測

超級電容器市場-全球產業規模、佔有率、趨勢、機會和預測(按最終用戶、類型、地區和競爭格局分類,2020-2030 年)超級電容器市場:按類型、電容、材料、安裝方式、終端用戶產業、國家及地區分類-全球產業分析、市場規模、市場佔有率及2025-2032年預測