|

市場調查報告書

商品編碼

1851248

溫度感測器:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)Temperature Sensors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

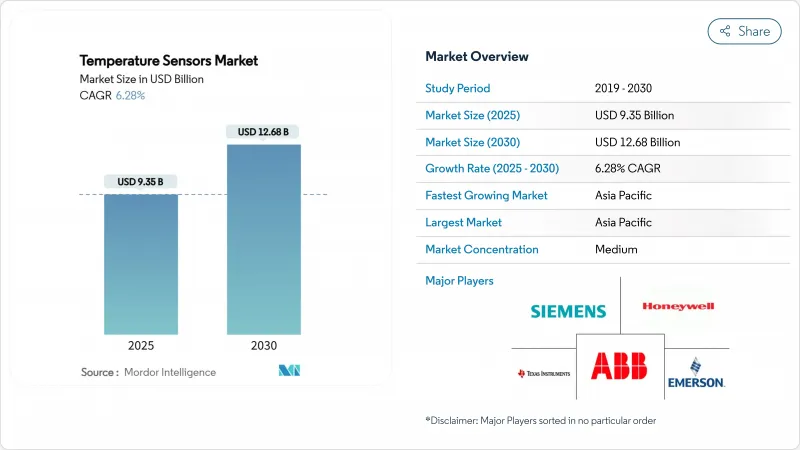

預計到 2025 年,溫度感測器市場規模將達到 93.5 億美元,到 2030 年將達到 126.8 億美元,複合年成長率為 6.28%。

隨著工業設施數位化、電動車的普及以及生命科學供應鏈對即時熱溯源的要求日益嚴格,市場對感測器的需求正在成長。生技藥品的低溫運輸法規、超大規模資料中心建設對光纖分散式感測技術的青睞,以及工業物聯網在歐洲加工廠的廣泛應用,共同推動了感測器市場規模的成長。 GaN/SiC功率電子元件的普及將進一步增強市場成長,因為其對精密冷卻的要求更高;此外,5G基地台的部署也需要板載溫度監控以確保運作。在供應方面,垂直整合的現有企業將透過專注於高精度產品和無線改造解決方案來降低總資本成本,從而應對來自亞洲低成本供應商的價格壓力。

全球溫度感測器市場趨勢與洞察

在歐洲製程工業擴展智慧工業物聯網溫度網路

歐洲製造商正將無線溫度節點整合到現有的控制架構中,以實現工業5.0在能源效率和工人安全方面的目標。這種免維護的感測器設計降低了生命週期成本,並簡化了化纖工廠和暖通空調升級改造中極具改裝的部署方案。人工智慧控制迴路利用更豐富的資料流來穩定氣壓和溫度條件,從而提高產品產量比率並減少停機時間。一項在美國小型工廠進行的投資回報率研究表明,營運成本的節省超過了初始工業物聯網硬體支出,檢驗了類似資本預算的可行性。因此,即使在可靠性要求極高的應用中,無線節點也越來越受歡迎,加速了溫度感測器市場轉型為互聯架構。

GaN/SiC功率電子技術的應用推動了對精密冷卻感知器的需求。

氮化鎵和碳化矽元件在高功率密度下運行,會產生局部高溫區域,因此需要亞攝氏度級的監測精度。半導體供應商預測,氮化鎵將在快速充電器、人工智慧伺服器和電動車轉換器等領域達到商業性化臨界點。汽車製造商指定使用即使在強電磁場下也能保持校準的感測器,而資料中心營運商則採用多點熱感映射來降低熱點風險。對氮化鋁薄膜感測器的研究表明,它們可以在高達 900 度C 的溫度下可靠運行,從而擴展了其在極端電力電子環境中的應用。能夠以具有競爭力的價格提供高精度和抗電磁干擾性能的供應商,將更有可能在溫度感測器市場佔據佔有率。

來自低成本中國供應商的降低平均售價壓力

國家支持的規模經濟使中國供應商能夠在通用熱電偶和基礎型熱電阻(RTD)領域以低於全球同行的價格銷售產品,從而擠壓了整個溫度感測器市場的利潤空間。歐洲公司則透過推出具成本效益、高精度的產品來應對這項挑戰,例如Sensirion的STS4L,產品功耗僅為微瓦級,卻能保持±0.4 度C的精度,使它們能夠在不直接參與價格競爭的情況下維持市場佔有率。

細分市場分析

到2024年,有線感測器將佔總收入的84.7%,為必須承受電磁干擾和延遲風險的關鍵生產迴路提供支援。隨著工廠對傳統生產線維修,以及建築管理公司引入無需佈線即可安裝的電池供電發射器,無線節點將填補這一空白,到2030年將以11.8%的複合年成長率成長。隨著每次無線維修增加冗餘通道,溫度感測器市場的銷售和業務收益都將增加。應用場景涵蓋化學反應器、暖通空調平衡和遠端油井口監測,這些都需要安全的通訊協定堆疊和多年的電池壽命。

快速成熟的通訊協定降低了無線傳輸相對於銅纜的可靠性Delta,使多節點部署的平均計劃投資回收期縮短至兩年以內。Honeywell符合 ISA100 標準的 SmartLine 發射器證明,其加密網狀架構能夠以亞秒級的速度更新數據,同時將封包遺失控制在 0.01% 以下 [honeywell.com]。營運商也在評估無線韌體升級,該升級允許在不中斷線路的情況下部署網路安全補丁,這項韌體目前已成為溫度感測器市場的標配。因此,整個溫度感測器產業普遍認為無線傳輸是現有設施棕地專案的長期預設方案,而非小眾技術。

到2024年,模擬元件的收入將維持71.2%的成長,因為4-20 mA迴路仍然是煉油廠和鋼鐵廠分散式控制系統(DCS)輸入的主要供電介質。然而,隨著工業乙太網、I2C和1-Wire匯流排在邊緣到雲端架構中日益普及,數位感測器市場到2030年將以9.4%的複合年成長率成長。由於數位節點嵌入了基於EEPROM的校準功能,安裝人員不再需要在工廠進行微調,從而降低了試運行成本和停機時間。受此加速轉變的影響,預計2030年,數位溫度感測器市場規模將達到51億美元。

德克薩斯(TI) 的 TMP117(精度為 ±0.08 度C)展示了其內建的 CRC 保護暫存器如何提升製藥廠的可追溯性,這些製藥廠必須儲存校準資料以備 FDA審核[ti.com]。資料豐富的套件還支援資產性能管理演算法,該演算法能夠預測故障的發生,從而延長泵浦和馬達的使用壽命並降低責任風險。供應商正在將分析儀表板作為增值訂閱服務捆綁銷售,從而平滑溫度感測器市場的收入週期。

溫度感測器市場報告按類型(有線、無線)、輸出(類比、數位)、技術(接觸式熱電偶、其他)、終端用戶產業(化學及石化、石油天然氣、其他)和地區進行細分。市場預測以美元計價。

區域分析

亞太地區將佔2024年總收入的44.9%,年複合成長率達7.2%,這主要得益於中國5G大型基地台的部署和印度符合GMP標準的疫苗工廠的建設。政府對電動車電池生產線的補貼將提高單車感測器密度,而國內半導體工廠將採用對溫度控制要求為±0.2°C的無塵室迴路。日本和韓國將進一步增強對精密製造的需求,特別是對需要在1400 度C高溫下運作的碳化矽晶圓爐的需求。

在北美,緊隨其後的是醫藥低溫運輸支援和超大規模雲園區,這些園區通常每個站點部署超過150公里的光纖分散式傳輸系統(DTS)。美國食品藥物管理局(FDA)對某些臨床體溫計的2025年豁免正在加速設備認證週期,而美國能源部(DOE)資助的能源效率目標正推動資料中心營運商將進氣溫度控制在1攝氏度以下。汽車一級供應商(Tier-1)的設計週期正在延長,但新型電動車平台仍在擴展熱感節點,溫度感測器市場與底特律的電氣化進程保持一致。

歐洲正優先推動工業5.0維修,歐盟層級提供補貼,用於升級整合無線感測器數位雙胞胎的智慧工廠。電動車的普及也將增加每輛車所需的電池溫度控管單元數量。該地區的能源轉型將刺激對氫電解和離岸風力發電機組耐腐蝕探頭的需求。總體而言,歐洲溫度感測器產業的特點是平均售價高昂,且測量標準嚴格,以保護淨利率免受全球價格競爭的影響。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 在歐洲製程工業擴展智慧工業物聯網溫度網路

- GaN/SiC功率電子技術的應用將推動對精密冷卻感知器的需求(亞洲)

- 強制要求生技藥品和mRNA疫苗低溫運輸可追溯性(北美)

- 亞洲地區5G基地台部署需要機載熱監測

- 歐洲電動車溫度控管模組的採用情況

- 超大規模資料中心建置推動光纖分散式感測(全球)

- 市場限制

- 來自低成本中國供應商的降低平均售價壓力

- 用於熱電阻的高純度鉑絲的供應風險

- 製藥生產中的校準漂移責任索賠(美國/歐盟)

- 汽車一級供應商的長期設計凍結週期

- 價值/供應鏈分析

- 監管和技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 競爭對手之間的競爭

- 替代品的威脅

第5章 市場規模與成長預測

- 按類型

- 有線

- 無線的

- 透過輸出

- 模擬

- 數位的

- 透過技術

- 接觸式熱電偶

- 電阻溫度檢測器(RTD)

- 熱敏電阻器(NTC/PTC)

- 溫度積體電路

- 非接觸式紅外線

- 光纖

- 終端用戶產業

- 化工/石油化工

- 石油和天然氣

- 金屬和採礦

- 發電

- 飲食

- 汽車和電動交通

- 醫療保健

- 航太/國防

- 消費性電子產品和穿戴式裝置

- 其他行業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 亞太其他地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Honeywell International Inc.

- Siemens AG

- Texas Instruments Inc.

- STMicroelectronics NV

- TE Connectivity Ltd.

- Panasonic Corporation

- ABB Ltd

- Emerson Electric Co.

- Analog Devices Inc.

- Denso Corporation

- Microchip Technology Inc.

- Amphenol Advanced Sensors

- Sensirion AG

- Endress+Hauser AG

- Robert Bosch GmbH

- Fluke Process Instruments

- FLIR Systems(Teledyne)

- Gnther GmbH Temperaturmesstechnik

- Kongsberg Gruppen

- Maxim Integrated Products

- Thermometris

第7章 市場機會與未來展望

The temperature sensor market size has reached USD 9.35 billion in 2025 and is forecast to climb to USD 12.68 billion by 2030, registering a 6.28% CAGR.

Demand is rising as industrial facilities digitize, electric vehicles proliferate, and life-science supply chains enforce real-time thermal traceability. Regulatory cold-chain mandates for biologics, hyperscale data-center buildouts that favor fiber-optic distributed sensing, and widespread IIoT adoption across European process plants jointly elevate sensor volumes. Growth is further strengthened by GaN/SiC power-electronics adoption, which raises precision-cooling requirements, and by 5G base-station deployments that need on-board thermal monitoring to protect uptime. On the supply side, vertically integrated incumbents counter price pressure from low-cost Asian suppliers by focusing on high-accuracy products and wireless retrofit solutions that reduce total installed cost.

Global Temperature Sensors Market Trends and Insights

Expansion of Smart IIoT Temperature Networks in European Process Industries

European manufacturers are integrating wireless temperature nodes into existing control architectures to meet Industry 5.0 goals for energy efficiency and worker safety. Maintenance-free sensor designs lower lifecycle cost and simplify retrofit deployment, which is attractive in chemical-fiber plants and HVAC upgrades. AI-enabled control loops use the richer data stream to stabilize air-pressure and thermal conditions, improving product yield and reducing downtime. Return-on-investment studies in small US factories show operating savings that outweigh initial IIoT hardware spend, validating capital budgets for similar. As a result, wireless nodes gain momentum even in reliability-critical applications, accelerating the temperature sensor market toward connected architectures.

GaN/SiC Power Electronics Adoption Elevating Precision-Cooling Sensor Demand

Gallium-nitride and silicon-carbide devices operate at higher power densities, creating localized heat zones that require sub-degree monitoring accuracy. Semiconductor suppliers forecast GaN reaching commercial tipping points in fast chargers, AI servers, and electric-vehicle converters. Automotive OEMs specify sensors that maintain calibration under strong electromagnetic fields, while data-center operators adopt multi-point thermal maps to contain hotspot risk. Research into aluminum-nitride thin-film sensors shows reliable operation up to 900 °C, extending sensor use into extreme power-electronics environments . Suppliers that deliver precision and EMI immunity at competitive cost are well-positioned to gain share in the temperature sensor market.

Downward ASP Pressure from Chinese Low-Cost Suppliers

State-supported economies of scale allow Chinese vendors to undercut global peers on commodity thermocouples and basic RTDs, eroding margins across the temperature sensor market. European firms are countering by releasing cost-efficient yet accurate models such as Sensirion's STS4L, which draws micro-watts of power while holding +-0.4 °C accuracy, thereby defending share without direct price wars

Other drivers and restraints analyzed in the detailed report include:

- Mandatory Cold-Chain Traceability for Biologics & mRNA Vaccines

- 5G Base-Station Roll-outs Requiring On-Board Thermal Monitoring

- Supply Risk of High-Purity Platinum Wire for RTDs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Wired sensors continued to dominate with 84.7 % revenue in 2024, anchoring production-critical loops that must resist electromagnetic interference and latency risks. Wireless nodes are closing the gap, expanding at 11.8 % CAGR to 2030 as factories retrofit legacy lines and building-management firms deploy battery-powered transmitters that install without conduit work. The temperature sensor market benefits because every wireless retrofit typically adds extra redundancy channels, lifting unit volumes and service revenues. Use cases span chemical reactors, HVAC balancing and remote well-head monitoring, each demanding secure protocol stacks and multi-year battery life.

Rapid protocol maturation is reducing the reliability delta versus copper cabling and bringing average project payback below two years for multi-node deployments. Honeywell's ISA100-compliant SmartLine transmitter illustrates how encrypted mesh architectures keep packet loss below 0.01 % while reporting sub-second updates [honeywell.com]. Operators also value firmware-over-the-air upgrades that let them roll out cyber-security patches without line shutdowns, a feature now common across the temperature sensor market. The overall temperature sensor industry therefore sees wireless not as a niche but as the long-term default for brown-field sites.

Analog devices retained 71.2 % revenue in 2024 because 4-20 mA loops still anchor distributed-control-system (DCS) inputs in refineries and steel mills. Digital sensors, however, are expanding 9.4 % CAGR to 2030 as industrial Ethernet, I2C and 1-Wire buses proliferate in edge-to-cloud architectures. When digital nodes embed EEPROM-based calibration, installers no longer need plant-floor trim, cutting commissioning cost and shortening downtime. The temperature sensor market size for digital devices is projected to reach USD 5.1 billion by 2030, reflecting this accelerating conversion.

Texas Instruments' +-0.08 °C TMP117 exemplifies how embedded CRC-protected registers improve traceability in pharmaceutical plants that must archive calibration data for FDA audits [ti.com]. Data-rich packets also enable asset-performance-management algorithms that predict failure before excursions occur, extending pump and motor life and lowering indemnity exposure. Vendors consequently bundle analytics dashboards as value-added subscriptions that smooth revenue cyclicality across the temperature sensor market.

The Temperature Sensors Market Report is Segmented Into Type (Wired, Wireless), Output (Analog, Digital), Technology (Contact Thermocouple, and More), End-User Industry (Chemical and Petrochemical, Oil and Gas and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific generated 44.9 % of 2024 revenue and is advancing at a 7.2 % CAGR, supported by China's 5G macro-cell rollout and India's build-out of GMP-compliant vaccine plants. Government subsidies for EV battery lines amplify sensor density per vehicle, while domestic semiconductor fabs adopt clean-room loops that demand +-0.2 °C RTDs. Japan and South Korea add precision-manufacturing pull, especially for SiC wafer furnaces requiring 1,400 °C sensors.

North America follows with pharmaceutical cold-chain compliance and hyperscale cloud campuses that often deploy >150 km of fiber DTS per site. The FDA's 2025 waiver on certain clinical thermometers accelerates device qualification cycles, while DOE-funded efficiency targets push data-center operators to sub-1 °C inlet-air control. Automotive Tier-1 design cycles are longer, yet every new EV platform still expands thermal nodes, tying the temperature sensor market to Detroit's electrification timetable.

Europe prioritizes Industry 5.0 retrofits, leveraging EU-level grants for smart-factory upgrades that merge wireless sensor networks with digital twins. EV adoption likewise lifts battery thermal-management units per vehicle. The region's energy transition stimulates demand for corrosion-resistant probes in hydrogen electrolyzers and offshore wind converters. Overall the temperature sensor industry in Europe is characterised by premium ASPs and stringent metrology standards that shield margins against global price competition.

- Honeywell International Inc.

- Siemens AG

- Texas Instruments Inc.

- STMicroelectronics N.V.

- TE Connectivity Ltd.

- Panasonic Corporation

- ABB Ltd

- Emerson Electric Co.

- Analog Devices Inc.

- Denso Corporation

- Microchip Technology Inc.

- Amphenol Advanced Sensors

- Sensirion AG

- Endress+Hauser AG

- Robert Bosch GmbH

- Fluke Process Instruments

- FLIR Systems (Teledyne)

- Gnther GmbH Temperaturmesstechnik

- Kongsberg Gruppen

- Maxim Integrated Products

- Thermometris

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of Smart IIoT Temperature Networks in European Process Industries

- 4.2.2 GaN/SiC Power Electronics Adoption Elevating Precision-Cooling Sensor Demand (Asia)

- 4.2.3 Mandatory Cold-Chain Traceability for Biologics and mRNA Vaccines (North America)

- 4.2.4 5G Base-Station Roll-outs Requiring On-Board Thermal Monitoring (Asia)

- 4.2.5 Electrified-Mobility Thermal-Management Modules Adoption (Europe)

- 4.2.6 Hyperscale Data-Center Build-out Driving Fiber-Optic Distributed Sensing (Global)

- 4.3 Market Restraints

- 4.3.1 Downward ASP Pressure from Chinese Low-Cost Suppliers

- 4.3.2 Supply Risk of High-Purity Platinum Wire for RTDs

- 4.3.3 Calibration-Drift Liability Claims in Pharma Manufacturing (US/EU)

- 4.3.4 Long Design-in Freeze Cycles in Automotive Tier-1s

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory or Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Intensity of Competitive Rivalry

- 4.6.5 Threat of Substitute Products

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 Type

- 5.1.1 Wired

- 5.1.2 Wireless

- 5.2 Output

- 5.2.1 Analog

- 5.2.2 Digital

- 5.3 Technology

- 5.3.1 Contact Thermocouple

- 5.3.2 Resistance Temperature Detector (RTD)

- 5.3.3 Thermistor (NTC/PTC)

- 5.3.4 Temperature IC

- 5.3.5 Non-Contact Infrared

- 5.3.6 Fiber-Optic

- 5.4 End-User Industry

- 5.4.1 Chemical and Petrochemical

- 5.4.2 Oil and Gas

- 5.4.3 Metals and Mining

- 5.4.4 Power Generation

- 5.4.5 Food and Beverage

- 5.4.6 Automotive and E-Mobility

- 5.4.7 Medical and Healthcare

- 5.4.8 Aerospace and Defense

- 5.4.9 Consumer Electronics and Wearables

- 5.4.10 Other Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Honeywell International Inc.

- 6.4.2 Siemens AG

- 6.4.3 Texas Instruments Inc.

- 6.4.4 STMicroelectronics N.V.

- 6.4.5 TE Connectivity Ltd.

- 6.4.6 Panasonic Corporation

- 6.4.7 ABB Ltd

- 6.4.8 Emerson Electric Co.

- 6.4.9 Analog Devices Inc.

- 6.4.10 Denso Corporation

- 6.4.11 Microchip Technology Inc.

- 6.4.12 Amphenol Advanced Sensors

- 6.4.13 Sensirion AG

- 6.4.14 Endress+Hauser AG

- 6.4.15 Robert Bosch GmbH

- 6.4.16 Fluke Process Instruments

- 6.4.17 FLIR Systems (Teledyne)

- 6.4.18 Gnther GmbH Temperaturmesstechnik

- 6.4.19 Kongsberg Gruppen

- 6.4.20 Maxim Integrated Products

- 6.4.21 Thermometris

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

城市氣候監測系統市場預測至2034年—按組件、部署模式、技術、應用、最終用戶和地區分類的全球分析

城市氣候監測系統市場預測至2034年—按組件、部署模式、技術、應用、最終用戶和地區分類的全球分析 溫度感測器市場:2026-2032年全球市場預測(依感測器類型、安裝方式、輸出方式、連接方式、精度等級、測量範圍、應用、最終用戶和分銷管道分類)雙感測器模組市場:按模組類型、感測器類型、技術、應用、終端用戶產業和分銷管道分類,全球預測,2026-2032年

溫度感測器市場:2026-2032年全球市場預測(依感測器類型、安裝方式、輸出方式、連接方式、精度等級、測量範圍、應用、最終用戶和分銷管道分類)雙感測器模組市場:按模組類型、感測器類型、技術、應用、終端用戶產業和分銷管道分類,全球預測,2026-2032年 體溫篩檢系統市場規模、佔有率和成長分析:按產品類型、技術、最終用戶和地區分類-2026-2033年產業預測

體溫篩檢系統市場規模、佔有率和成長分析:按產品類型、技術、最終用戶和地區分類-2026-2033年產業預測 溫度感測器市場分析及預測(至2035年):按類型、產品、技術、組件、應用、材質、最終用戶、功能、安裝類型和解決方案分類

溫度感測器市場分析及預測(至2035年):按類型、產品、技術、組件、應用、材質、最終用戶、功能、安裝類型和解決方案分類 2026-2034年全球衛生級溫度感測器市場規模、佔有率、趨勢及成長分析報告全球溫度感測器市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

2026-2034年全球衛生級溫度感測器市場規模、佔有率、趨勢及成長分析報告全球溫度感測器市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年全球溫度感測器市場報告

2026年全球溫度感測器市場報告 溫度感測器市場 - 全球產業規模、佔有率、趨勢、機會及預測(按類型、功率、垂直產業、地區和競爭格局分類,2021-2031年)熱電偶溫度感測器市場 - 全球產業規模、佔有率、趨勢、機會及預測(按類型、應用、結構類型、地區和競爭格局分類,2021-2031年)

溫度感測器市場 - 全球產業規模、佔有率、趨勢、機會及預測(按類型、功率、垂直產業、地區和競爭格局分類,2021-2031年)熱電偶溫度感測器市場 - 全球產業規模、佔有率、趨勢、機會及預測(按類型、應用、結構類型、地區和競爭格局分類,2021-2031年)