|

市場調查報告書

商品編碼

1851208

智慧顯示器:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)Smart Display - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

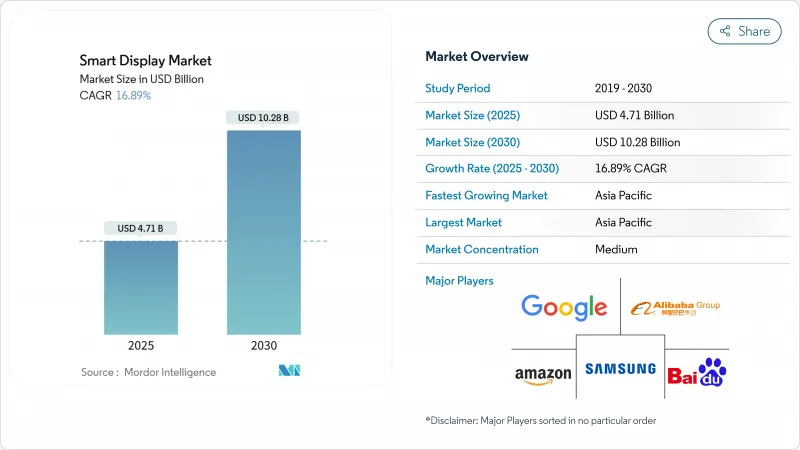

預計到 2025 年,智慧顯示器市場規模將達到 47.1 億美元,到 2030 年將達到 102.8 億美元,複合年成長率為 16.89%。

從純語音螢幕到人工智慧主導的多模態中心的升級週期正在擴大裝置量,同時也推高平均售價。 Matter 通訊協定 的普及正在消除平台鎖定,使競爭重心從生態系統獨佔轉向硬體創新。汽車駕駛座、OLED 的普及以及人工智慧增強的 10 吋及以上尺寸機型正在推動收入成長。儘管 8-10 吋液晶面板短缺,垂直整合的面板製造商仍能維持利潤率。另一方面,由於擔心麥克風始終開啟的風險,企業買家正在延長採購週期,這抑制了近期的出貨動能。

全球智慧顯示市場趨勢與洞察

北美地區多模態語音優先智慧家庭中心的普及率不斷提高

智慧顯示器正朝著視覺和語音混合型設備的方向發展,可透過單一介面控制照明、安防和娛樂系統。預計到2026年,美國語音助理用戶將達到1.571億,這將推動設備升級,以處理更豐富的指令並提供情境化的視覺效果。生成式人工智慧(AI)能夠提供主動式提案,例如根據通勤資料預熱恆溫器,進而提升使用者體驗價值。三星的Vision AI顯示器在2024年佔據了高階產品28.3%的出貨量佔有率。零售商將顯示器與訂閱服務捆綁銷售,從而提高經常性收入和用戶黏性。隨著蘋果即將推出首款智慧家庭顯示器,競爭日益激烈,促使生態系統參與者每年更新產品線。

Matter相容設備的普及將加速平台互通性。

Matter 1.4 引進了整合 Wi-Fi 和 Thread 的認證家用路由器,減少了部署失敗率,節省了安裝人員的時間。預計到 2025 年中,將有超過 1000 款 Matter 認證產品上市,消費者可以放心混用不同品牌的產品,無需擔心被廠商鎖定。企業將該通訊協定的安全性能驗證視為滿足零信任要求的重要一步,從而促進了更廣泛的商業部署。公共產業正在探索基於 Matter 的能源儀表板,以支援需量反應計劃。該標準也為酒店業帶來了維修機遇,現有的 Wi-Fi 基礎設施無需重新佈線即可承載 Thread 邊界路由器。

始終開啟的麥克風的安全漏洞導致B2B採購延遲。

金融機構和醫院暫停部署,直到供應商提供資料路徑文件並證明設備端處理能力足夠。由於首席資訊安全長 (CISO) 要求按照 ISO 27001 標準進行滲透測試,採購週期最多延長了 45 天。 Matter 的可選離線模式緩解了一些擔憂,但也使中央設備管理更加複雜,並促使人們需要混合架構,從而增加了成本和整合複雜性。擁有 FedRAMP 同等授權的供應商更早贏得了契約,從而獲得了先發優勢。

細分市場分析

預計到2025年,智慧語音助理設備的市場規模將達到42億美元。亞馬遜Alexa憑藉著Fire TV和Ring的交叉銷售勢頭,在2024年佔據了33.7%的市場佔有率。谷歌助理隨後推出了Nest Hub,而阿里巴巴旗下的天貓精靈則以18.7%的複合年成長率成長,這主要得益於其整合的AI聊天機器人,能夠將內容本地化以適應中文方言。預計到2025年,智慧語音助理設備的市場規模將達到42億美元,這主要得益於生成式模型能夠記憶過往對話,從而帶動了設備的更換需求。蘋果將於2025年3月發布一款6吋的Home Display,這預示著新的競爭即將到來,並可能將iOS用戶引入HomeKit的世界。

在中國,儘管市佔率下降了10.3個百分點,百度DuerOS仍佔了41.1%的行動智慧螢幕市場。各大品牌透過視覺搜尋、兒童安全模式以及與2D碼結帳相連的多模態購物車來區分彼此。這些舉措凸顯了智慧顯示市場在區域體驗層級上的分散程度,儘管Matter公司一直在努力實現連結性的統一。

5-10吋的螢幕尺寸預計將在2024年佔據52.7%的銷售佔有率,因為它既能節省檯面空間,又能提供舒適的觀看體驗。廚房食譜、臥室鬧鐘和辦公桌視訊通話等應用大多採用此尺寸,從而降低了組件成本。然而,隨著零售、醫院和汽車儀錶板對更豐富視覺效果的需求,10吋以上尺寸的螢幕正以19.3%的複合年成長率快速成長。更大的螢幕尺寸支援智慧家庭儀錶板的同步視訊聊天和分割螢幕模式,從而提升用戶參與度。

對角線尺寸超過10吋的智慧顯示器,平均售價大幅上漲,提高了製造商的利潤率。 OLED螢幕在該尺寸區間滲透率很高,助力智慧顯示器市場佔據高階價格分佈。面板製造商正將產能轉向8.6代玻璃基板,以滿足大尺寸尺寸螢幕的需求。同時,5吋以下的智慧顯示器仍屬於低成本小眾市場或床頭伴侶,但由於穿戴式裝置的競爭,它們在智慧顯示器市場的佔有率正在萎縮,穿戴式設備已經佔據了小螢幕通知功能。

憑藉成熟的供應鏈和具有競爭力的價格,LCD預計在2024年仍將保持81.8%的市場佔有率。汽車儀錶板通常採用LTPS LCD,因為其具有良好的熱穩定性和亮度。然而,OLED的複合年成長率高達21.8%,這主要得益於供應商利用其深邃的黑色和柔韌性,實現了曲面和旋轉性外形規格。豪華飯店的智慧鏡子採用OLED層壓板,將非工作顯示器隱藏在反射玻璃後,從而獲得更高的每位用戶平均收入(ARPU)。

預計到2030年,基於OLED的智慧顯示器市場規模將超過30億美元,這主要得益於韓國和中國第六代軟性製造廠的蓬勃發展。隨著印刷轉移技術成本的逐步降低,MicroLED技術有望帶來更高的亮度和更長的使用壽命。製造商正透過交叉授權專利和建構面板產品組合來規避單一技術帶來的風險。

區域分析

預計亞太地區將在2024年以37.6%的市佔率引領智慧顯示器市場,並在2030年之前維持17.3%的複合年成長率。為因應2024年智慧音箱出貨量25.6%的下滑,百度和阿里巴巴等中國廠商已透過將大型語言模型整合到顯示器中來重塑其提案主張。政府支持的人工智慧晶片計畫將降低物料清單成本,從而推動售價低於100美元的大螢幕顯示器上市,並擴大其在農村地區的滲透率。韓國品牌將專注於OLED創新,並利用本土面板生態系統向全部區域出口高階產品。

由於近乎普及的寬頻和語音助理的高普及率,北美繼續引領科技潮流。隨著家庭用戶將第一代螢幕設備更換為配備更高級麥克風和邊緣人工智慧的智慧型設備,更換週期成為成長的主要驅動力。亞馬遜佔據美國智慧音箱市場29%的佔有率,並正在為Alexa推出生成式人工智慧升級,從而促進用戶提升銷售更大尺寸的Echo Show機型。蘋果計劃於2025年推出新產品,可能會重塑廠商格局,並吸引一部分富裕的iOS用戶。

在歐洲,對隱私和永續性的日益重視推動了對設備端處理和採用回收材料製成的設備的需求。預計到2024年,歐洲智慧家庭市場規模將達到221.1億美元,即將推出的生態設計法規強制要求具備能源管理功能,這將促使企業採購經Matter認證的、能夠監控消費量維修補貼有望釋放潛在需求。在南美和中東/非洲等新興地區,隨著智慧型手機廠商為促進生態系統融合而推出小螢幕產品,智慧型手機的普及率預計將逐步提高,但價格敏感度和網路連線的不穩定性限制了其普及。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 北美地區多模態語音優先智慧家庭中心的普及率不斷提高

- Matter技術的普及將加速平台互通性。

- 汽車OEM廠商整合智慧後視鏡與貫穿式駕駛座顯示器

- 人工智慧驅動的上下文使用者介面推動了10英寸以上螢幕產品的高階定價,亞洲地區主導

- 零售商需要便捷的結帳流程和動態貨架指示牌

- 智慧床邊設備可提高病人參與和HCAHPS評分

- 市場限制

- 始終開啟的麥克風的安全漏洞導致B2B採購延遲。

- 8-10吋液晶面板工廠持續面臨面板短缺問題,限制了供應彈性。

- 區域資料隱私碎片化推高了在地化成本。

- 語音助理語言支援方面的不足阻礙了北歐和加勒比地區的普及。

第5章:生態系分析

第6章:技術展望

第7章 波特五力分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第8章 市場規模與成長預測

- 透過語音助手

- Amazon Alexa

- Google Assistant

- Baidu DuerOS

- Alibaba TmallGenie

- Apple Siri

- 其他

- 按螢幕尺寸

- 小於5英寸

- 5到10英寸

- 10吋或以上

- 透過顯示技術

- 液晶顯示器

- 有機發光二極體

- 其他(微型LED、電子紙)

- 通過決議

- HD(720p)

- 全高清 (1080p)

- 4K 或更高

- 按安裝類型

- 獨立式智慧顯示器

- 整合智慧顯示器(智慧鏡子、自助服務終端、貨架邊緣)

- 連結性別

- 僅限 Wi-Fi

- Wi-Fi + 蜂窩網路

- Wi-Fi+Zigbee/Thread/Matter

- 按最終用戶行業分類

- 住宅智慧家居

- 車

- 零售與飯店

- 衛生保健

- 企業和教育機構

- 其他(交通樞紐、公共部門)

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐國家(丹麥、瑞典、挪威、芬蘭)

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 東南亞

- 澳洲

- 亞太其他地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中東

- GCC

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 其他非洲地區

- 北美洲

第9章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Amazon.com Inc.

- Google LLC

- Baidu Inc.

- Alibaba Group Holding Ltd.

- Xiaomi Corp.

- Lenovo Group Ltd.

- LG Electronics Inc.

- Samsung Electronics Co., Ltd.

- Meta Platforms Inc.(Portal)

- Sony Corp.

- TCL Tech. Group

- Hisense Group

- Sharp Corp.

- Koninklijke Philips NV

- Panasonic Holdings Corp.

- Huawei Tech. Co. Ltd.

- BOE Technology Group Co. Ltd.

- Vizio Inc.

- JBL(Harman Int'l)

- Apple Inc.

第10章:市場機會與未來展望

- 閒置頻段與未滿足需求評估

The smart display market stood at USD 4.71 billion in 2025 and is projected to reach USD 10.28 billion by 2030, reflecting a 16.89% CAGR.

The upgrade cycle from voice-only screens to AI-driven multimodal hubs is widening average selling prices while enlarging the installed base. Matter protocol adoption is dismantling platform lock-in, shifting competition toward hardware innovation rather than ecosystem exclusivity. Automotive cockpits, OLED diffusion, and AI-enhanced above 10-inch models are intensifying revenue upside. Vertically integrated panel makers have preserved margins despite 8-10-inch LCD shortages. Conversely, enterprise buyers have prolonged procurement cycles because of always-on-microphone risks, tempering short-term shipment momentum.

Global Smart Display Market Trends and Insights

Rising adoption of multimodal voice-first smart-home hubs in North America

Smart displays are evolving into visual-voice hybrids that orchestrate lighting, security, and entertainment systems from a single interface. Voice-assistant penetration is expected to reach 157.1 million U.S. users by 2026, underpinning device upgrades that handle richer commands and provide contextual visuals. Generative AI is enabling proactive suggestions-such as pre-warming thermostats based on commute data-raising perceived value. Samsung's Vision AI-equipped displays helped the company capture 28.3% of premium category shipments in 2024. Retailers are bundling displays with subscription services, driving recurring revenue and stickiness. Competitive intensity is heightening as Apple prepares its first smart home display, prompting ecosystem players to refresh line-ups annually.

Proliferation of Matter-compliant devices accelerating platform interoperability

Matter 1.4 introduced certified home routers that unify Wi-Fi and Thread, slashing onboarding failures and cutting installer time. By mid-2025 more than 1,000 Matter-certified products are expected, giving consumers confidence to mix brands without fearing lock-in. Enterprises view the protocol's secure commissioning as a step toward meeting zero-trust mandates, encouraging broader commercial rollouts. Utilities are exploring Matter-based energy dashboards to support demand-response programs. The standard also unlocks retrofit opportunities in hospitality, where existing Wi-Fi infrastructure can host Thread border routers without rewiring.

Security vulnerabilities in always-on microphones causing B2B procurement delays

Financial institutions and hospitals are pausing deployments until vendors document data pathways and prove on-device processing sufficiency. Procurement cycles have stretched by up to 45 days as CISOs demand penetration tests aligned with ISO 27001 requirements. Matter's optional offline mode eases some concerns but complicates central device management, prompting requests for hybrid architectures that add cost and integration complexity. Vendors that achieve FedRAMP-equivalent attestations are winning contracts faster, creating early-mover advantages.

Other drivers and restraints analyzed in the detailed report include:

- Automotive OEM integration of smart mirrors and pillar-to-pillar cockpit displays

- AI-powered contextual UI driving premium price mix in more than 10-inch category

- Persistent panel shortage in 8-10-inch LCD fabs limiting supply elasticity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The smart display market size for voice-assistant devices reached USD 4.2 billion in 2025. Amazon Alexa held 33.7% market share in 2024, riding cross-sell momentum from Fire TV and Ring. Google Assistant followed through Nest hubs, while Alibaba's TmallGenie grew at 18.7% CAGR, buoyed by AI chatbot integration that localizes content for Chinese dialects. The smart display market size for voice-assistant devices reached USD 4.2 billion in 2025, and replacement demand is strengthening as generative models enable memory of prior conversations. Apple's March 2025 six-inch Home Display announcement signals fresh competition that may draw iOS households into its HomeKit universe.

Continued expansion of Mandarin-optimized large language models is eroding Alexa's edge in China, where Baidu DuerOS controlled 41.1% of mobile smart screens despite a 10.3 percentage-point decline. Brands are differentiating via visual search, kid-safe modes, and multimodal shopping carts that link QR-based checkout. These moves illustrate how the smart display market is fragmenting into region-specific experience layers even as Matter attempts to harmonize connectivity.

The 5-10-inch category dominated with 52.7% revenue in 2024 because it balances countertop space and viewing comfort. Kitchen recipes, bedroom alarms, and desk video calls mostly fit this diagonal, keeping BOM costs low. Yet the >10-inch cohort is expanding at a 19.3% CAGR as retailers, hospitals, and vehicle dashboards demand richer visuals. Wider panels invite split-screen modes for simultaneous video chats and smart-home dashboards, elevating user engagement metrics.

Average selling prices jump when diagonal exceeds 10 inches, improving manufacturer margins. OLED penetration is higher in this tier, helping the smart display market command premium price points. Panel makers are shifting capacity toward Gen 8.6 glass substrates to serve the large-format rush. Meanwhile, <5-inch devices remain in budget niches and as bedside companions, but their slice of the smart display market is shrinking under competition from wearables that already occupy the small-screen notification role.

LCD retained 81.8% share in 2024, thanks to mature supply chains and competitive pricing. Automotive instrument clusters often favor LTPS LCD for thermal stability and brightness. However, OLED's 21.8% CAGR is accelerating as vendors exploit its deep blacks and flexibility to fashion curved or rollable form factors. Smart mirrors in luxury hotels use OLED laminates to hide inactive displays behind reflective glass, commanding higher ARPU.

The smart display market size for OLED-based units is forecast to exceed USD 3 billion by 2030, aided by Gen 6 flexible fabs in South Korea and China. MicroLED research promises even higher luminance and lifespan, with printed transfer techniques edging closer to cost targets. Manufacturers are hedging by cross-licensing patents and mixing panel portfolios to avoid single-technology risk.

The Smart Display Market Report is Segmented by Voice Assistant (Amazon Alexa, and More), Screen Size (5 - 10 Inches, and More), Display Technology (LCD, and More), Resolution (Full HD, and More), Installation Type (Stand-Alone, and More), Connectivity (Wi-Fi Only, and More), End-User Industry (Automotive, and More), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific led the smart display market with 37.6% revenue share in 2024 and is set to compound at 17.3% CAGR through 2030. Chinese vendors such as Baidu and Alibaba responded to a 25.6% slump in 2024 smart-speaker shipments by layering large language models onto displays, resetting value propositions. Government-backed AI chip initiatives are lowering BOM costs, enabling sub-USD 100 large-screen models that widen rural penetration. South Korean brands focus on OLED innovation, leveraging local panel ecosystems to export premium units across the region.

North America remains a technology trendsetter with near-ubiquitous broadband and high voice-assistant uptake. Replacement cycles dominate growth as households swap first-generation screens for Matter-capable variants with superior microphones and edge AI. Amazon retained 29% of U.S. smart-speaker units, rolling out generative AI upgrades to Alexa that encourage upsells to larger Echo Show models. Apple's 2025 entry could lure a slice of the affluent iOS base, reshuffling vendor rankings.

Europe emphasizes privacy and sustainability, stimulating demand for devices with on-device processing and recycled materials. The European Smart Home market reached USD 22.11 billion in 2024, and energy-management features mandated by upcoming Ecodesign rules are steering procurement toward Matter-certified hubs that monitor consumption. Nordic adoption lags owing to voice-assistant language gaps, but regulatory clarity and subsidies for energy retrofits are expected to unlock latent demand. Emerging regions in South America, the Middle East, and Africa witness gradual uptake as smartphone OEMs bundle smaller screens to drive ecosystem stickiness, although price sensitivity and patchy connectivity temper volumes.

- Amazon.com Inc.

- Google LLC

- Baidu Inc.

- Alibaba Group Holding Ltd.

- Xiaomi Corp.

- Lenovo Group Ltd.

- LG Electronics Inc.

- Samsung Electronics Co., Ltd.

- Meta Platforms Inc. (Portal)

- Sony Corp.

- TCL Tech. Group

- Hisense Group

- Sharp Corp.

- Koninklijke Philips N.V.

- Panasonic Holdings Corp.

- Huawei Tech. Co. Ltd.

- BOE Technology Group Co. Ltd.

- Vizio Inc.

- JBL (Harman Int'l)

- Apple Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising adoption of multimodal voice-first smart-home hubs in North America

- 4.2.2 Proliferation of Matter-compliant devices accelerating platform interoperability

- 4.2.3 Automotive OEM integration of smart mirrors and pillar-to-pillar cockpit displays

- 4.2.4 AI-powered contextual UI driving premium price mix in Above 10-inch category, Asia-led

- 4.2.5 Retail demand for frictionless checkout and dynamic shelf-edge signage

- 4.2.6 Hospital bedside smart terminals improving patient engagement and HCAHPS scores

- 4.3 Market Restraints

- 4.3.1 Security vulnerabilities in always-on microphones causing B2B procurement delays

- 4.3.2 Persistent panel shortage in 8-10-inch LCD fabs limiting supply elasticity

- 4.3.3 Fragmented regional data-privacy mandates raising localisation costs

- 4.3.4 Voice-assistant language support gaps curbing uptake across Nordics and Caribbeans

5 INDUSTRY ECOSYSTEM ANALYSIS

6 TECHNOLOGICAL OUTLOOK

7 PORTER'S FIVE FORCES ANALYSIS

- 7.1 Porter's Five Forces

- 7.1.1 Bargaining Power of Suppliers

- 7.1.2 Bargaining Power of Buyers

- 7.1.3 Threat of New Entrants

- 7.1.4 Threat of Substitutes

- 7.1.5 Intensity of Competitive Rivalry

8 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 8.1 By Voice Assistant

- 8.1.1 Amazon Alexa

- 8.1.2 Google Assistant

- 8.1.3 Baidu DuerOS

- 8.1.4 Alibaba TmallGenie

- 8.1.5 Apple Siri

- 8.1.6 Others

- 8.2 By Screen Size

- 8.2.1 Less than 5 Inches

- 8.2.2 5 - 10 Inches

- 8.2.3 Above 10 Inches

- 8.3 By Display Technology

- 8.3.1 LCD

- 8.3.2 OLED

- 8.3.3 Others (Micro-LED, E-Paper)

- 8.4 By Resolution

- 8.4.1 HD (= 720p)

- 8.4.2 Full HD (1080p)

- 8.4.3 4K and Above

- 8.5 By Installation Type

- 8.5.1 Stand-alone Smart Displays

- 8.5.2 Integrated Smart Displays (smart mirrors, kiosk, shelf-edge)

- 8.6 By Connectivity

- 8.6.1 Wi-Fi Only

- 8.6.2 Wi-Fi + Cellular

- 8.6.3 Wi-Fi + Zigbee/Thread/Matter

- 8.7 By End-user Industry

- 8.7.1 Residential Smart Home

- 8.7.2 Automotive

- 8.7.3 Retail and Hospitality

- 8.7.4 Healthcare

- 8.7.5 Corporate and Education

- 8.7.6 Others (Transportation Hubs, Public Sector)

- 8.8 By Geography

- 8.8.1 North America

- 8.8.1.1 United States

- 8.8.1.2 Canada

- 8.8.1.3 Mexico

- 8.8.2 Europe

- 8.8.2.1 Germany

- 8.8.2.2 United Kingdom

- 8.8.2.3 France

- 8.8.2.4 Italy

- 8.8.2.5 Spain

- 8.8.2.6 Nordics (Denmark, Sweden, Norway, Finland)

- 8.8.2.7 Rest of Europe

- 8.8.3 Asia-Pacific

- 8.8.3.1 China

- 8.8.3.2 Japan

- 8.8.3.3 South Korea

- 8.8.3.4 India

- 8.8.3.5 Southeast Asia

- 8.8.3.6 Australia

- 8.8.3.7 Rest of Asia-Pacific

- 8.8.4 South America

- 8.8.4.1 Brazil

- 8.8.4.2 Argentina

- 8.8.4.3 Rest of South America

- 8.8.5 Middle East

- 8.8.5.1 Gulf Cooperation Council Countries

- 8.8.5.2 Turkey

- 8.8.5.3 Rest of Middle East

- 8.8.6 Africa

- 8.8.6.1 South Africa

- 8.8.6.2 Nigeria

- 8.8.6.3 Rest of Africa

- 8.8.1 North America

9 COMPETITIVE LANDSCAPE

- 9.1 Market Concentration

- 9.2 Strategic Moves

- 9.3 Market Share Analysis

- 9.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 9.4.1 Amazon.com Inc.

- 9.4.2 Google LLC

- 9.4.3 Baidu Inc.

- 9.4.4 Alibaba Group Holding Ltd.

- 9.4.5 Xiaomi Corp.

- 9.4.6 Lenovo Group Ltd.

- 9.4.7 LG Electronics Inc.

- 9.4.8 Samsung Electronics Co., Ltd.

- 9.4.9 Meta Platforms Inc. (Portal)

- 9.4.10 Sony Corp.

- 9.4.11 TCL Tech. Group

- 9.4.12 Hisense Group

- 9.4.13 Sharp Corp.

- 9.4.14 Koninklijke Philips N.V.

- 9.4.15 Panasonic Holdings Corp.

- 9.4.16 Huawei Tech. Co. Ltd.

- 9.4.17 BOE Technology Group Co. Ltd.

- 9.4.18 Vizio Inc.

- 9.4.19 JBL (Harman Int'l)

- 9.4.20 Apple Inc.

10 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 10.1 White-space and Unmet-Need Assessment

智慧顯示器市場-2026-2032年全球市場預測

智慧顯示器市場-2026-2032年全球市場預測 全球智慧顯示器市場

全球智慧顯示器市場 智慧顯示器市場報告:按類型、顯示尺寸、解析度、最終用戶和地區分類(2026-2034 年)

智慧顯示器市場報告:按類型、顯示尺寸、解析度、最終用戶和地區分類(2026-2034 年) 2026-2034年全球教育智慧顯示器市場規模、佔有率、趨勢和成長分析報告教育智慧顯示器市場:2026-2032年全球市場預測(依產品類型、定價模式、應用、最終用戶及通路分類)

2026-2034年全球教育智慧顯示器市場規模、佔有率、趨勢和成長分析報告教育智慧顯示器市場:2026-2032年全球市場預測(依產品類型、定價模式、應用、最終用戶及通路分類) 智慧顯示器市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、外形、最終用戶及功能分類日本智慧顯示器市場規模、佔有率、趨勢及預測(按類型、顯示器尺寸、解析度、最終用戶和地區分類),2026-2034年

智慧顯示器市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、外形、最終用戶及功能分類日本智慧顯示器市場規模、佔有率、趨勢及預測(按類型、顯示器尺寸、解析度、最終用戶和地區分類),2026-2034年 2026年全球感溫變色智慧窗戶顯示市場報告2026年全球智慧顯示器市場報告

2026年全球感溫變色智慧窗戶顯示市場報告2026年全球智慧顯示器市場報告 智慧顯示器市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、技術、最終用戶、地區和競爭格局分類,2021-2031年

智慧顯示器市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、技術、最終用戶、地區和競爭格局分類,2021-2031年