|

市場調查報告書

商品編碼

1851151

商業印刷:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)Commercial Printing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

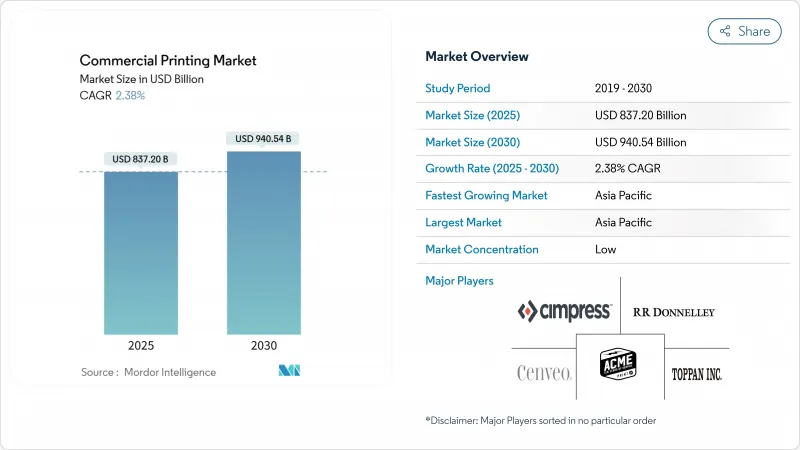

商業印刷市場預計到 2025 年將達到 8,372 億美元,到 2030 年將達到 9,405.4 億美元,年複合成長率為 2.38%。

這項業績表明,商業印刷市場正在適應數位化變革,同時充分利用包裝、可變資訊服務和永續基材的成長。電子商務對印刷包裝的持續需求、向植物油墨的穩步轉型以及按需數位工作流程的廣泛應用,正在緩解傳統出版業務仍然面臨的收入壓力。對用於印刷工作流程自動化的人工智慧投資以及在消費者附近部署微型工廠的舉措,預計將提高商業印刷市場眾多參與企業的產量和盈利。同時,大型企業正與軟體供應商合作,整合即時數據分析,而本地專業公司則在桌面促銷應用領域開闢利基市場。

全球商業印刷市場趨勢與洞察

按需包裝印刷業務爆炸性成長

為了支持快速的產品上市和區域促銷活動,電商企業越來越傾向於採用更短、更頻繁的包裝。這一趨勢在亞太地區發展最為迅速,因為當地的履約中心需要更靠近消費者印刷包裝,從而降低庫存成本並減少產品過時。

可變數據印刷在個人化行銷的應用日益廣泛

北美和歐洲的廣告商要求提供基於第一方資料的個人化郵件和包裹。大日本印刷株式會社於2025年推出了「Persona Insights」人工智慧工具,將政府人口統計與印刷工作流程相結合,可在一次生產過程中產生獨特的設計變體。將數據分析與數位印刷相結合的印刷公司正在贏得優質、服務豐富的契約,並彌補傳統商業印刷作業週轉時間長的不足。

廣告支出持續向數位媒體管道轉移

品牌所有者正將預算分配給線上影片和社交媒體,這限制了雜誌和報紙印刷訂單的成長。印刷商則透過專注於包裝和直郵形式來彌補這一下滑,這些包裝和直郵形式整合了QR碼,以實現線上線下無縫銜接。

細分市場分析

2024年,柔印平台維持了41.07%的收入佔有率,這主要得益於長幅面軟質包裝印刷的良好經濟效益。隨著品牌對快速修改設計稿和個人化宣傳活動的需求不斷成長,預計到2030年,數位噴墨解決方案的商業印刷市場規模將以3.45%的複合年成長率成長。區域印刷商正擴大採用混合生產線,將柔印白層與可變噴墨顏色結合,以減少設定時間和浪費。預計到2028年,數位印刷在中幅幅面印刷方面的成本將與傳統印刷持平,這將削弱柔印在飲料標籤等高SKU細分市場的優勢。

人工智慧引導的套準和自動作業切換技術的進步正在減少人工投入並最大限度地提高運作。例如,Multi-Label Tech-Print 公司的 Domino N610i 等設備展示了中型印刷商如何利用六色、600 dpi 的引擎,一次性完成金屬色和高密度白的印刷。水性噴墨墨水比溶劑型柔印墨水產生的 VOC排放更低,使印刷商能夠滿足日益嚴格的空氣品質法規要求。

到2024年,包裝將佔商業印刷市場佔有率的44.08%,年複合成長率達3.07%,這主要得益於電子商務小包裹量的成長和品牌優質化趨勢。折疊式紙盒和軟包裝袋廣泛應用於依賴清晰貨架展示的行業,例如化妝品、營養補充劑和已調理食品。報紙、雜誌和平裝書等出版品的銷售量持續下滑,尤其是在北美和西歐。然而,採用再生紙印刷的漫畫和小批量文學作品在具有環保意識的消費者群體中呈現出成長動能。

商業印刷供應商正透過提供包含瓦楞紙箱、商店展示架和個人化插頁卡的「宣傳活動套件」來實現業務多元化。嵌入包裝的印刷電子元件能夠實現溫度監控和防偽功能,深受亞太地區製藥公司和奢侈品牌的青睞。包裝的韌性抵消了其他行業廣告支出週期性波動的影響,為印刷商提供了穩定的收入來源。

商業印刷市場報告按印刷類型(平張膠印噴墨、柔版印刷、網版印刷等)、應用(包裝、廣告、出版等)、印刷基材(紙張和紙板、織物和紡織品等)、幅面(大尺寸印刷等)和地區(北美、歐洲、亞太、南美、中東和非洲)進行細分。

區域分析

預計到2024年,亞太地區將佔全球印刷收入的45.64%,並在2030年之前以3.28%的複合年成長率成長。消費品包裝生產、國內電子商務交易量以及政府對基礎設施計劃的獎勵策略推動了印刷需求的成長。僅中國每年就新增數百條瓦楞紙板加工生產線,而印度的標籤行業將受益於商品及服務稅(GST)的推行,該稅種強制要求在物流管道中使用標準化的條碼進行識別。區域品牌正積極採用帶有QR碼的智慧包裝,以提高行動優先消費者的忠誠度。

北美在全球印刷業中仍佔據重要佔有率,儘管成長速度有所放緩。隨著需求轉向數據主導的直郵、藥品說明書和高階包裝,美國商業印刷市場規模趨於穩定。受教育出版業優先採用國內印刷內容的政策推動,加拿大印刷商正專注於小批量圖書生產。

在歐洲,一般商業印刷量保持平穩,但C2C可回收基材和植物油墨的投資正在加速成長。德國正在試行紙質咖啡杯的押金返還制度,加工商也積極測試經認證可堆肥的阻隔塗佈紙板。歐盟關於一次性塑膠包裝形式的法規可能會在中期內推動纖維板的銷售成長。

拉丁美洲和中東及非洲地區在商業印刷市場中所佔佔有率雖小,但成長潛力巨大。巴西的PET回收率將在2025年達到56.4%,這將使食品品牌能夠轉向使用PCR含量較高的標籤和軟包裝袋,從而提升印刷量。波灣合作理事會成員國正在建造新的工業園區,其中的包裝廠服務於乳製品、飲料和個人護理叢集,這將支撐近期對膠印機和凹版印刷機的需求。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 按需包裝印刷業務爆炸性成長

- 可變數據印刷在個人化行銷的應用日益廣泛

- 零售和消費品品牌對促銷印刷品的需求持續成長

- 轉向環保基材和植物油墨

- 將印刷電子技術(RFID、NFC)整合到包裝和標籤中

- 靠近客戶的微型工廠「列印即服務」中心的出現

- 市場限制

- 廣告支出正在向數位媒體管道轉移

- 紙張、油墨和能源投入價格的波動;

- 對傳統油墨的VOC和化學品使用量有嚴格的限制

- 新型數位印刷機所需的半導體元件短缺

- 供應鏈分析

- 監管環境

- 技術展望

- 投資分析

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 按列印類型

- 平張膠印

- 數位噴墨

- 柔版印刷

- 螢幕

- 凹版印刷

- 其他列印類型

- 透過使用

- 包裹

- 廣告

- 發布

- 圖書

- 雜誌

- 報紙

- 其他出版品

- 企業及貿易印刷

- 其他應用

- 透過印刷材料

- 紙張和紙板

- 塑膠和合成基材

- 織物和紡織品

- 金屬和箔材

- 其他材料

- 按格式

- 大尺寸列印

- 小幅面印刷

- 直接物件印刷

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲、紐西蘭

- 亞太其他地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 肯亞

- 其他非洲地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Toppan Inc.

- Dai Nippon Printing Co., Ltd.

- RR Donnelley & Sons Company

- Quad/Graphics Inc.

- Transcontinental Inc.

- Cenveo Worldwide Limited

- Cimpress plc

- Deluxe Corporation

- Shutterfly LLC

- LSC Communications LLC

- Mondi Group

- Printpack Inc.

- Multi-Color Corporation

- ACME Printing

- O'Neil Printing

- Xerox Corporation(Print Services)

- Smurfit Westrock(Print and Packaging)

- Berry Global Group(Graphics Services)

- Seiko Epson Corporation(Commercial Inkjet Systems)

- HP Inc.(PageWide Industrial)

第7章 市場機會與未來展望

The commercial printing market size is valued at USD 837.20 billion in 2025 and is forecast to reach USD 940.54 billion by 2030, advancing at a 2.38% CAGR.

This performance indicates that the commercial printing market is adapting to digital disruption while capitalizing on growth in packaging, variable-data services, and sustainable substrates. Ongoing demand for printed packaging in e-commerce, a steady shift toward vegetable-based inks, and wider use of on-demand digital workflows are cushioning revenue pressures that still affect traditional publishing work. Investments in artificial intelligence for print workflow automation, together with micro-factory concepts located near consumer hubs, are expected to raise throughput and improve profitability for many participants in the commercial printing market. At the same time, larger firms are pursuing alliances with software vendors to integrate real-time data analytics, while regional specialists are carving out niche positions in direct-to-object and short-run promotional applications.

Global Commercial Printing Market Trends and Insights

Explosive Growth in On-Demand Packaging Print Runs

E-commerce brands increasingly favor shorter, more frequent packaging runs to support fast product launches and regional promotions. A 2024 installation of a Domino N610i digital label press by Multi-Label Tech-Print in Ahmedabad underscores the migration toward high-throughput digital lines able to process hundreds of SKUs with minimal changeover time.The trend is advancing most rapidly in Asia-Pacific, where localized fulfillment centers require packaging that is printed close to consumers, limiting inventory costs and reducing obsolescence.

Rising Adoption of Variable-Data Printing for Personalized Marketing

Advertisers in North America and Europe are demanding individualized mailers and packaging tied to first-party data. Dai Nippon Printing introduced its "Persona Insight" AI tool in 2025, combining government demographic statistics with print workflows that generate unique design variants in one production pass. Printers that integrate data analytics and digital presses are securing premium, service-rich contracts that offset slower run lengths in traditional commercial jobs.

Ongoing Shift of Advertising Spend to Digital Media Channels

Brand owners allocate budget toward online video and social media, curbing growth in magazine and newspaper print orders. Printers offset the decline by emphasizing packaging and direct mail formats that integrate QR codes for seamless offline-to-online engagement.

Other drivers and restraints analyzed in the detailed report include:

- Sustained Demand for Promotional Print from Retail and CPG Brands

- Transition Toward Eco-Friendly Substrates and Vegetable-Based Inks

- Volatile Prices of Paper, Ink and Energy Inputs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Flexographic platforms retained 41.07% revenue in 2024, underpinned by favorable economics for long runs on flexible packaging. The commercial printing market size for digital inkjet solutions is projected to widen by 3.45% CAGR to 2030 as brands demand quicker artwork changes and individualized campaigns. Regional converters increasingly deploy hybrid lines, marrying flexo white layers with variable inkjet color to cut setup times and waste. Digital cost parity at mid-length runs is expected before 2028, eroding flexo's historical edge in SKU-rich sectors such as beverage labels.

Advances in AI-guided registration and automated job changeovers are shrinking labor input and maximizing uptime. Investments like Multi-Label Tech-Print's Domino N610i show how medium-sized converters leverage six-color, 600 dpi engines to print metallics and high-opacity whites in one pass. Environmental compliance is another driver: water-borne inkjet fluids emit lower VOCs than solvent-based flexo blends, helping printers satisfy tightening air-quality rules.

Packaging held 44.08% of commercial printing market share in 2024 and will rise at a 3.07% CAGR on the back of e-commerce parcel volumes and brand premiumization. Folding cartons and flexible pouches serve cosmetics, nutraceuticals, and ready-to-eat meals, sectors that rely on vivid shelf appeal. Publishing work-newspapers, magazines, softcover books-experiences ongoing volume erosion, especially in North America and Western Europe. Yet manga and small-batch literary titles printed on recycled paper are registering niche growth among environmentally conscious consumers.

Commercial printing industry vendors diversify by offering "campaign kits" that bundle corrugated shipper boxes, point-of-sale displays, and personalized insert cards. Printed electronics embedded in packages enable temperature monitoring and anti-counterfeiting, features valued by pharmaceutical and luxury brands in Asia-Pacific. Packaging's resilience gives printers an anchor revenue stream, offsetting cyclical ad-spend patterns in other segments.

The Commercial Printing Market Report is Segmented by Printing Type (Offset Lithography, Digital Inkjet, Flexographic, Screen, and More), Application (Packaging, Advertising, Publishing, and More), Print Material (Paper and Cardboard, Fabric and Textiles, and More), Format (Large-Format Printing, and More) and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa).

Geography Analysis

Asia-Pacific dominated revenue with 45.64% in 2024 and is projected to post a 3.28% CAGR through 2030 as consumer packaged goods output, domestic e-commerce volumes, and government stimulus for infrastructure projects expand print demand. China alone adds hundreds of corrugated converting lines annually, while India's label sector benefits from GST roll-out mandating standardized barcode identification across logistics channels. Regional brands actively specify QR-code smart packaging to build loyalty among mobile-first consumers.

North America maintains a sizeable slice of global output, although growth is modest. The commercial printing market size in the United States is steady as demand migrates toward data-driven direct mail, pharmaceutical inserts, and luxury packaging. Canada's printers focus on short-run book production fueled by educational publishing mandates favoring domestically printed content.

Europe shows flat volume in general commercial work but accelerating investment in C2C recyclable substrates and vegetable-oil inks. Germany is piloting deposit-return systems for paper-based coffee cups, spurring converters to test barrier-coated boards certified for compostability. EU regulations on single-use plastic pack formats will likely channel incremental volume to fiberboard over the medium term.

Latin America and the Middle East & Africa together account for a smaller proportion of the commercial printing market but represent meaningful upside. Brazil's PET recycling rate reached 56.4% in 2025, allowing food brands to switch to PCR-rich labels and flexible pouches, which in turn creates print volume. Gulf Cooperation Council states are building new industrial zones that house packaging plants serving dairy, beverage, and personal-care clusters, underpinning near-term demand for offset and gravure equipment.

- Toppan Inc.

- Dai Nippon Printing Co., Ltd.

- R.R. Donnelley & Sons Company

- Quad/Graphics Inc.

- Transcontinental Inc.

- Cenveo Worldwide Limited

- Cimpress plc

- Deluxe Corporation

- Shutterfly LLC

- LSC Communications LLC

- Mondi Group

- Printpack Inc.

- Multi-Color Corporation

- ACME Printing

- O'Neil Printing

- Xerox Corporation (Print Services)

- Smurfit Westrock (Print and Packaging)

- Berry Global Group (Graphics Services)

- Seiko Epson Corporation (Commercial Inkjet Systems)

- HP Inc. (PageWide Industrial)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Explosive growth in on-demand packaging print runs

- 4.2.2 Rising adoption of variable-data printing for personalized marketing

- 4.2.3 Sustained demand for promotional print from retail and CPG brands

- 4.2.4 Transition toward eco-friendly substrates and vegetable-based inks

- 4.2.5 Integration of printed electronics (RFID, NFC) into packaging and labels

- 4.2.6 Emergence of micro-factory "print-as-a-service" hubs close to customers

- 4.3 Market Restraints

- 4.3.1 Ongoing shift of advertising spend to digital media channels

- 4.3.2 Volatile prices of paper, ink and energy inputs

- 4.3.3 Stringent VOC and chemical-use regulations on conventional inks

- 4.3.4 Shortage of semiconductor components for new digital presses

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Investment Analysis

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Printing Type

- 5.1.1 Offset Lithography

- 5.1.2 Digital Inkjet

- 5.1.3 Flexographic

- 5.1.4 Screen

- 5.1.5 Gravure

- 5.1.6 Other Printing Types

- 5.2 By Application

- 5.2.1 Packaging

- 5.2.2 Advertising

- 5.2.3 Publishing

- 5.2.3.1 Books

- 5.2.3.2 Magazines

- 5.2.3.3 Newspapers

- 5.2.3.4 Other Publishing

- 5.2.4 Corporate and Transactional Printing

- 5.2.5 Other Application

- 5.3 By Print Material

- 5.3.1 Paper and Cardboard

- 5.3.2 Plastic and Synthetic Substrates

- 5.3.3 Fabric and Textiles

- 5.3.4 Metal and Foils

- 5.3.5 Other Materials

- 5.4 By Format

- 5.4.1 Large-Format Printing

- 5.4.2 Small-Format Printing

- 5.4.3 Direct-to-Object Printing

- 5.5 By Geography (Value)

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia and New Zealand

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 Middle East

- 5.5.4.1.1 Saudi Arabia

- 5.5.4.1.2 United Arab Emirates

- 5.5.4.1.3 Turkey

- 5.5.4.1.4 Rest of Middle East

- 5.5.4.2 Africa

- 5.5.4.2.1 South Africa

- 5.5.4.2.2 Nigeria

- 5.5.4.2.3 Kenya

- 5.5.4.2.4 Rest of Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Toppan Inc.

- 6.4.2 Dai Nippon Printing Co., Ltd.

- 6.4.3 R.R. Donnelley & Sons Company

- 6.4.4 Quad/Graphics Inc.

- 6.4.5 Transcontinental Inc.

- 6.4.6 Cenveo Worldwide Limited

- 6.4.7 Cimpress plc

- 6.4.8 Deluxe Corporation

- 6.4.9 Shutterfly LLC

- 6.4.10 LSC Communications LLC

- 6.4.11 Mondi Group

- 6.4.12 Printpack Inc.

- 6.4.13 Multi-Color Corporation

- 6.4.14 ACME Printing

- 6.4.15 O'Neil Printing

- 6.4.16 Xerox Corporation (Print Services)

- 6.4.17 Smurfit Westrock (Print and Packaging)

- 6.4.18 Berry Global Group (Graphics Services)

- 6.4.19 Seiko Epson Corporation (Commercial Inkjet Systems)

- 6.4.20 HP Inc. (PageWide Industrial)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

商業印刷市場規模、佔有率、趨勢和預測:按技術、印刷類型、應用和地區分類,2026-2034年

商業印刷市場規模、佔有率、趨勢和預測:按技術、印刷類型、應用和地區分類,2026-2034年 商業印刷市場:按印刷製程、產品、材料和最終用戶分類的全球市場預測,2026-2032年

商業印刷市場:按印刷製程、產品、材料和最終用戶分類的全球市場預測,2026-2032年 全球商業印刷市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球商業印刷市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年全球商業印刷服務市場報告商用網路攝影機市場按產品類型、解析度、連接方式、性別、應用、分銷管道和最終用戶分類-2026年至2032年全球預測日本商業印刷市場規模、佔有率、趨勢及預測(按技術、印刷類型、應用和地區分類,2026-2034年)

2026年全球商業印刷服務市場報告商用網路攝影機市場按產品類型、解析度、連接方式、性別、應用、分銷管道和最終用戶分類-2026年至2032年全球預測日本商業印刷市場規模、佔有率、趨勢及預測(按技術、印刷類型、應用和地區分類,2026-2034年) 商業印刷外包市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、應用、地區和競爭格局分類,2020-2030年預測

商業印刷外包市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、應用、地區和競爭格局分類,2020-2030年預測 全球商業印刷市場全球商業印刷市場

全球商業印刷市場全球商業印刷市場 商業印刷市場:按印刷類型、應用和地區分類

商業印刷市場:按印刷類型、應用和地區分類