|

市場調查報告書

商品編碼

1851119

電子競技:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)E-Sports - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

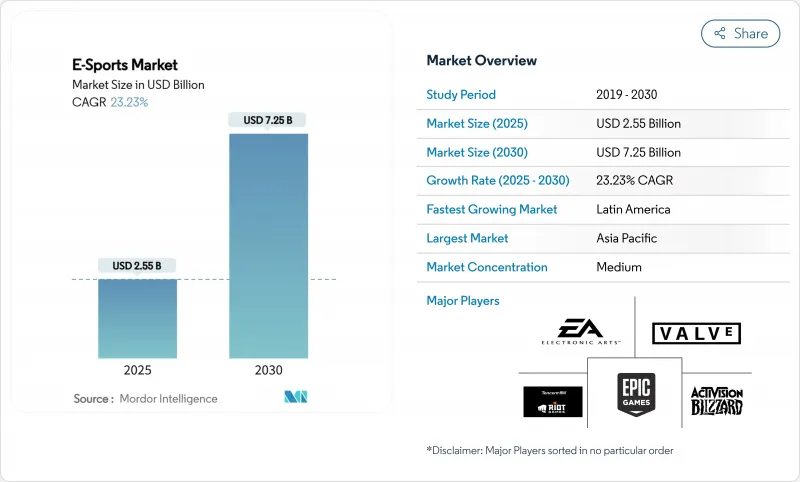

根據估計和預測,電子競技市場規模將在 2025 年達到 25.5 億美元,在 2030 年達到 72.5 億美元,年複合成長率為 23.23%。

亞太地區強大的數位基礎設施、日趨成熟的發行商經營的特許經營聯賽以及不斷成長的遊戲內貨幣化正在推動營收成長。獨家串流媒體版權協議正穩步將觀眾規模轉化為可預測的媒體版權收入,同時對贊助的依賴也開始降低。行動端的普及、區塊鏈賦能的資產所有權以及政府的資助計劃正在擴大參與度並實現收入多元化,而遊戲類型的創新,尤其是大逃殺模式,持續吸引主流玩家。隨著獨立賽事營運商要求更公平的智慧財產權條款並對行銷人員主導的聯賽結構施加壓力,競爭動態正在改變。

全球電競市場趨勢與洞察

5G和光纖部署協助亞洲行動電競商業化

5G的廣泛部署有望顯著提升連線速度並降低延遲,使行動遊戲能夠提供媲美錦標賽級別的競技體驗。 Airtel等通訊業者報告稱,平均吞吐量顯著提高,從而改善了觀眾的視訊品質和遊戲內的響應速度。行動網路普及率的不斷提高正推動以往服務不足的區域和二線城市參與到有組織的電競活動中,使電競市場遠遠超出傳統都市區中心的範圍。區域通訊集團正透過遊戲積分的直接營運商收費、數據流量包贊助和聯合品牌賽事等方式獲取增量價值。由此形成了一個良性循環:更高的服務品質提升了用戶參與度,用戶參與度提升了遊戲內消費,而消費的增加又吸引了發行商和贊助商的注意。因此,行動生態系統的規模經濟正成為電競市場成長的關鍵支柱。

基於區塊鏈的數位資產所有權提升了出版商的收入

透過驗證與電競精彩瞬間、皮膚和成就相關的非同質化代幣(NFT) 的所有權,玩家可以安心交易,而發行商則可以透過次市場交易獲得持續的版稅收入。一些主流遊戲正在試驗計畫計畫中將可收集物品直接整合到直播中,從而強化觀看和消費的循環。各大開發人員正在探討的互通性標準可望使資產跨越多個遊戲,加深用戶投入並延長產品生命週期。早期市場已呈現流動性增強的趨勢,顯示市場對稀有、具有聲望的數位物品的需求日益成長。對於賽事主辦單位而言,區塊鏈基礎設施可自動分配獎金池和出場費,從而降低營運成本和糾紛。隨著技術的成熟,區塊鏈有望開闢新的收入來源,這些收入來源在結構上對廣告週期的依賴程度較低。

歐洲數位廣告成長放緩,贊助支出隨之減少。

隨著數位廣告成長放緩,歐洲品牌負責人正在收緊預算。 2024年,贊助收入將佔總收入的60.27%,因此,戰隊和賽事主辦單位對行銷支出的變化高度敏感。投資回報率正受到越來越多的關注,尤其是在快餐、酒類和博彩等行業,這些行業監管的加強使得宣傳活動更加複雜。因此,版權所有者正透過媒體版權競標和遊戲內物品銷售等方式實現收入多元化,以降低波動性。然而,獲取其他收入來源需要更強大的數據分析來證明受眾價值,這給規模較小的營業單位帶來了壓力。因此,在贊助比例重新平衡之前,歐洲電競市場的短期成長可能低於全球平均。

細分市場分析

到2024年,電競市場60.27%的收入將來自贊助,但隨著平台為獨家內容支付溢價,媒體版權的擴張正在加速。預計到2030年,媒體版權帶來的電競市場規模將以19.8%的複合年成長率成長,逐漸縮小與贊助收入的差距。賽事組織者受益於多年轉播協議,這些協議能夠穩定現金流並降低賽事預算風險。同時,發行商正在將直播視窗整合到遊戲用戶端中,並啟用將觀看與微交易關聯的即時購買提示。與發行商簽訂收入分成協議的戰隊可以獲得這些收入,從而減少對外部品牌合約的依賴。同時,觀眾收益代幣和即時投注疊加層等實驗性收入來源也正在獲得認可。收入來源的多元化表明,電子競技市場正朝著成熟運動賽事典型的平衡結構發展。

媒體版權的崛起也對製作品質提出了更高的要求。高清畫面、多語種說明和即時資料疊加提高了觀看體驗,並促使主辦單位加大對攝影棚和虛擬實境舞台的投入。此類投資增強了主辦單位在未來版權週期中的議價能力。對於規模較小的組織者而言,聯合製作中心和特許經營賽事體系提供了成本分攤的途徑,以保持競爭力。總而言之,這些變化可能會在預測期結束時重塑電競市場的收入結構。

到2024年,Twitch將佔據電競市場74.89%的觀看時間佔有率,這主要得益於其先行推出的社群工具以及與創作者的深度合作關係。然而,YouTube Gaming將憑藉其與搜尋和精彩片段重播功能的緊密整合,在觀看時長方面縮小與Twitch的差距,預計到2030年將以24.38%的複合年成長率成長。虎牙和鬥魚等區域性服務在中國吸引了大量用戶,而Nimo TV則在東南亞地區獲得了發展勢頭,其本地化的語言支援顯著提升了觀看時長。平台間的競爭主要集中在降低延遲、簡化影片剪輯製作流程以及提高創作者的變現率等方面。與頂級體育賽事類似,大型賽事的獨家轉播協議能夠有效推動用戶成長。隨著內容版權在各平台間日益分散,觀眾越來越依賴社群媒體上的精彩片段和匯總的賽事結果,這使得流量預測變得更加複雜。

從商業性角度來看,各大平台正採用混合模式來吸引前 1% 以外的網紅。他們透過整合原生電商Widgets來拓展收入來源,使用戶能夠在直播期間購買周邊商品和門票。隨著亞馬遜和米高梅影業等傳統媒體公司加入戰局,製作大型紀錄片系列,各大平台也增加了獲取主流贊助商的管道。因此,多平台環境為賽事組織者提供了談判的靈活性,但也需要完善的版權管理來防止內容蠶食。總而言之,這些動態強化了平台多樣性作為電競市場結構性特徵的重要性。

電子競技市場按收入模式(例如媒體版權、廣告和贊助)、直播平台(例如 Twitch、YouTube Gaming)、設備類型(PC、行動/掌機、主機)、遊戲類型(例如 MOBA、FPS)和地區進行細分。市場預測以美元計價。

區域分析

亞太地區預計2024年將貢獻57.3%的電競收入,成為電競市場的核心。通訊業者主導的5G投資、政府對場館建設的補貼以及遊戲作為主流娛樂方式在文化上的普及,都鞏固了亞太地區的主導。韓國等國家已將大學電競聯賽制度化,確保了人才的穩定輸送;而中國的地方政府津貼則鼓勵企業在專門的數位運動園區內聚集。該地區以行動端為主的消費群體推動了休閒遊戲向電子競技觀看的轉變,並透過數位道具銷售和賽事門票銷售增強了生態系統的自給自足資金籌措。這些結構性優勢正在推動人均參與度的持續成長,使亞太地區成為發行商全球內容策略中不可或缺的一部分。

北美擁有電競市場中最成熟的特許經營聯賽體系。高額的特許經營費確保了球隊的長期發展和收入分成,吸引了來自NBA和NFL的財團進駐。雖然這種模式促進了強大的商品行銷和贊助,但某些聯賽高達4億美元的遞延費用負債卻讓人對低階球隊的償付能力產生擔憂。儘管發行商的收入多元化降低了媒體曝光率,但對獎金分配機制的監管卻增加了複雜性。雖然主客場賽制等營運創新尚處於試驗階段,且依賴本地粉絲群體,但成本控制對於球隊保持獲利至關重要。

預計到2030年,拉丁美洲將成為主要地區中成長最快的地區,年複合成長率將達到19.2%,這主要得益於寬頻普及率的提高以及年輕且以行動裝置為中心的用戶群。巴西在該地區獎金池和觀眾人數方面佔據主導地位,這得益於品牌對葡萄牙語轉播的投資以及本地贊助商的強大陣容。經濟和外匯波動導致用戶平均消費下降,促使全球發行商調整其價格敏感的微交易套餐和靈活的訂閱等級。此類調整將在不降低單位利潤率的情況下擴大用戶轉換管道,從而保持整個拉丁美洲電競市場的成長勢頭。

歐洲監理格局正在塑造一條獨特的發展軌跡。儘管法國等國家政府為賽事舉辦提供津貼和獎勵,但各國在廣告和博彩方面的法律差異卻阻礙了跨國賽事的協調統一。威爾斯的發展計畫概述了一項旨在透過電子競技創新中心實現經濟多元化的國家策略。強制性最低工資和醫療保險等選手福利標準正日益受到關注,並對成本結構產生影響。歐洲觀眾使用多種語言,因此對於尋求市場滲透的廣播公司而言,本地化投資勢在必行。從長遠來看,結構性的歐洲方案可能會略微減緩商業性試驗的步伐,但有望加強對運動員的保護,並提升廣播的專業化水平。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 5G和光纖部署協助亞洲行動電競貨幣化

- 基於區塊鏈的數位資產所有權提升出版商收入

- 特許經營聯盟模式吸引了傳統運動投資者

- 歐洲和中國政府對電子競技的認可和資助

- 市場限制

- 歐洲數位廣告成長放緩,贊助支出隨之減少。

- 知識產權所有權分散阻礙了聯賽結構的標準化。

- 監理展望

- 波特五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 按收入模式

- 贊助

- 媒體版權

- 廣告

- 發行商費用和遊戲內收費

- 門票和商品

- 其他

- 透過串流媒體平台

- 抽搐

- YouTube Games

- Facebook遊戲

- 富亞

- DouYu

- 其他平台

- 依設備類型

- PC

- 移動/手持設備

- 主機

- 按遊戲類型

- MOBA

- 第一人稱射擊遊戲(FPS)

- 生存遊戲

- 運動與賽車

- 鬥爭

- 戰略及其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 亞太其他地區

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 北美洲

第6章 競爭情勢

- Strategic Developments

- Vendor Positioning Analysis

- 公司簡介

- Tencent Holdings Ltd(Riot Games)

- Activision Blizzard Inc

- Electronic Arts Inc

- Epic Games Inc

- Valve Corporation

- Modern Times Group(ESL FACEIT Group)

- Gfinity PLC

- Capcom Co Ltd

- Ubisoft Entertainment SA

- Take-Two Interactive Software Inc

- Krafton Inc

- Garena Online(Sea Ltd)

- Nintendo Co Ltd

- Bandai Namco Holdings Inc

- NetEase Inc

- Sony Interactive Entertainment LLC

- Cloud9 Esports Inc

- Team Liquid Enterprises BV

- 100 Thieves LLC

- Fnatic Ltd

- OG Esports A/S

第7章 市場機會與未來展望

The E-Sports market size is estimated at USD 2.55 billion in 2025 and is forecast to reach USD 7.25 billion by 2030, expanding at a 23.23% CAGR.

Robust digital infrastructure in Asia-Pacific, the maturation of publisher-run franchise leagues, and rising in-game monetization are accelerating top-line growth. Exclusive streaming-rights deals are steadily converting audience scale into predictable media-rights income, even as sponsorship dependence begins to ease. Mobile accessibility, blockchain-enabled asset ownership, and government funding initiatives are widening participation and revenue diversity, while genre innovation, especially battle-royale formats, continues to draw mainstream viewers. Competitive dynamics are shifting as independent tournament operators demand fairer intellectual-property terms, placing pressure on publisher-controlled league structures.

Global E-Sports Market Trends and Insights

5G & Fiber Roll-outs Enabling Mobile Esports Monetization in Asia

Widespread 5G deployment is materially raising connection speeds and lowering latency, allowing mobile titles to deliver tournament-grade competitive experiences. Large operators such as Airtel report meaningful uplifts in average throughput, which improves spectator video quality and in-game responsiveness . As handset penetration climbs, previously under-served rural and tier-two cities gain entry to organized play, expanding the esports market well beyond traditional urban hubs. Regional telecommunications groups are capturing incremental value through direct-carrier billing for game credits, data-bundle sponsorship, and co-branded tournaments. The result is a virtuous cycle: higher service-quality drives engagement, engagement boosts in-game spend, and elevated spend draws more publisher and sponsor attention. The mobile ecosystem's scale advantage is therefore becoming a decisive growth pillar for the esports market.

Blockchain-based Digital Asset Ownership Boosting Publisher Revenues

Verifiable ownership of non-fungible tokens (NFTs) tied to esports moments, skins, and achievements gives players the confidence to trade securely while rewarding publishers with perpetual royalties on secondary-market transactions. Pilot programs inside major titles now embed collectible drops directly into live broadcasts, tightening the loop between viewing and spending. Interoperability standards under discussion among leading developers could allow assets to traverse multiple games, deepening user investment and extending product life cycles. Early-stage marketplaces already show robust liquidity, signaling pent-up demand for scarce, prestige-oriented digital items. For tournament organizers, blockchain infrastructure automates distribution of prize pools and appearance fees, cutting operational overhead and reducing disputes. As the technology matures, blockchain promises to anchor an additional revenue stream that is structurally less exposed to advertising cycles.

Sponsorship Spend Compression Amid Digital-Ad Slow-down in Europe

European brand marketers are tightening budgets as broader digital advertising growth decelerates. Because sponsorship still represents 60.27% of 2024 revenue, teams and tournament operators remain highly sensitive to shifts in marketing outlay. Return-on-investment scrutiny is rising, especially in categories such as fast food, alcohol, and gambling where tightening regulations complicate activation campaigns. Rights holders are therefore diversifying income through media-rights auctions and in-game item sales to buffer volatility. However, capturing alternative sources requires stronger data analytics to demonstrate audience value, pressuring smaller entities that lack scale. Near-term growth of the esports market in Europe may therefore trail global averages until sponsorship ratios rebalance.

Other drivers and restraints analyzed in the detailed report include:

- Franchise League Models Attracting Traditional Sports Investors

- Government Recognition & Funding of Esports in Europe & China

- Fragmented IP Ownership Restricting Standardized League Structures

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The esports market generated 60.27% of its 2024 revenue from sponsorship, but the media-rights line is scaling faster as platforms pay premiums for exclusive content. The esports market size attributable to media rights is forecast to expand at a 19.8% CAGR through 2030, gradually narrowing the gap with sponsorship. Tournament organizers benefit from multi-year broadcast deals that stabilize cash flow and de-risk event budgeting. Meanwhile publishers integrate live-stream windows within game clients, enabling instant purchase prompts that link viewing to micro-transactions. Teams aligned with publishers through revenue-share agreements gain exposure to these sales, easing dependence on external brand deals. At the same time, experimental revenue formats, such as view-and-earn tokens or live-betting overlays, are under evaluation. The growing diversity of income sources signals an esports market migrating toward the balanced mixes typical of mature sports properties.

Media-rights growth also exerts upward pressure on production quality. High-definition feeds, multi-language commentary, and real-time statistics overlays elevate viewing standards, prompting capital expenditure on studios and virtual-reality stages. These investments strengthen negotiation leverage in future rights cycles. For smaller organizers, pooled production hubs and franchised event circuits offer a cost-sharing route to remain competitive. Collectively, these shifts are likely to recalibrate the revenue hierarchy within the esports market by the end of the forecast window.

Twitch dominated 2024 with a 74.89% slice of the esports market share in viewing hours, underpinned by first-mover community tools and deep creator relationships. Yet YouTube Gaming's tighter integration with search and highlight-repeat functions positions it for a 24.38% CAGR through 2030, closing the volume gap. Region-specific services such as Huya and DouYu aggregate large domestic audiences in China, while Nimo TV gains traction in Southeast Asia where localized language support wins incremental watch-time. Platform competition centers on latency reduction, clip-creation ease, and monetization rates for creators. Exclusive deals for marquee tournaments swing subscriber sign-ups, echoing competition in premium sports. As content rights fragment across services, viewers increasingly rely on social snippets and aggregated results dashboards, complicating traffic forecasts.

From a commercial standpoint, platforms are adopting hybrid ad-share and tip-economy models to attract influencers outside the top 1% percentile. Implementation of native e-commerce widgets, allowing merchandise or ticket purchase during streams, broadens revenue capture. Traditional media firms entering the fray illustrated by Amazon MGM Studios' production of documentary series around majors-inject additional distribution lanes that can unlock mainstream sponsors. The resulting multi-platform environment provides organizers with negotiation flexibility but demands sophisticated rights-management to prevent cannibalization. Overall, these dynamics reinforce platform diversity as a structural feature of the esports market.

E-Sports Market is Segmented by Revenue Model (Media Rights, Advertising and Sponsorship, and More), Streaming Platform (Twitch, Youtube Gaming, and More), by Device Type (PC, Mobile/Handheld, Console), Game Genre (MOBA, First-Person Shooter (FPS) and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific generated 57.3% of 2024 revenue, positioning it as the cornerstone of the esports market. Carrier-led 5G investment, government subsidies for arena construction, and cultural acceptance of gaming as mainstream entertainment sustain this leadership. Countries such as South Korea institutionalize scholastic esports leagues, ensuring a steady talent pipeline, while China's municipal grants encourage corporate clustering around dedicated digital-sports parks. The region's mobile-first demographics underpin above-average conversion from casual play to esports viewership, reinforcing ecosystem self-finance through digital item sales and tournament ticketing. These structural advantages support persistently high per-capita engagement, making the region indispensable for publishers' global content strategies.

North America showcases the most mature franchise-league infrastructure inside the esports market. High franchise fees buy permanency and revenue-share participation, drawing ownership groups from NBA and NFL backgrounds. While this configuration fosters robust merchandising and sponsorship packages, deferred fee obligations estimated at USD 400 million across certain circuits raise solvency questions for lower-ranked teams. Regulatory oversight around loot-box mechanics adds complexity, though diversified publisher revenue mitigates headline exposure. Operational innovations such as home-and-away formats are experimenting with localized fan bases, but cost-control remains pivotal to returning teams to profitability.

Latin America is projected to deliver a 19.2% CAGR through 2030, the fastest among major regions, buoyed by improving broadband coverage and a youthful, mobile-centric audience. Brazil dominates regional prize pools and viewership, validating brand investment in Portuguese-language broadcasts and locally-sponsored rosters. Economic volatility and currency swings temper average spend per user, yet global publishers increasingly tailor price-sensitive micro-transaction bundles and flexible subscription tiers. These adaptations widen funnel reach without compromising per-unit margins, sustaining momentum for the esports market across the continent.

Europe's regulatory mosaic shapes a distinct trajectory. National governments such as France allocate grants and event-hosting incentives, but cross-border tournament harmonization lags due to divergent advertising and gambling laws. The Welsh development plan illustrates sub-national strategies aimed at economic diversification through esports innovation hubs. Player-welfare standards, including minimum-salary mandates and health coverage, gain prominence, influencing cost structures. Because European audiences consume multiple languages, localization investment is non-negotiable for broadcasters seeking market penetration. Over time, Europe's structured approach is likely to strengthen athlete protections and broadcasting professionalism, though it may marginally slow commercial experimentation.

- Tencent Holdings Ltd (Riot Games)

- Activision Blizzard Inc

- Electronic Arts Inc

- Epic Games Inc

- Valve Corporation

- Modern Times Group (ESL FACEIT Group)

- Gfinity PLC

- Capcom Co Ltd

- Ubisoft Entertainment SA

- Take-Two Interactive Software Inc

- Krafton Inc

- Garena Online (Sea Ltd)

- Nintendo Co Ltd

- Bandai Namco Holdings Inc

- NetEase Inc

- Sony Interactive Entertainment LLC

- Cloud9 Esports Inc

- Team Liquid Enterprises BV

- 100 Thieves LLC

- Fnatic Ltd

- OG Esports A/S

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 5G and Fiber Roll-outs Enabling Mobile Esports Monetization in Asia

- 4.2.2 Blockchain-based Digital Asset Ownership Boosting Publisher Revenues

- 4.2.3 Franchise League Models Attracting Traditional Sports Investors

- 4.2.4 Government Recognition and Funding of Esports in Europe and China

- 4.3 Market Restraints

- 4.3.1 Sponsorship Spend Compression Amid Digital-Ad Slow-down in Europe

- 4.3.2 Fragmented IP Ownership Restricting Standardized League Structures

- 4.4 Regulatory Outlook

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Revenue Model

- 5.1.1 Sponsorship

- 5.1.2 Media Rights

- 5.1.3 Advertising

- 5.1.4 Publisher Fees and In-Game Purchases

- 5.1.5 Tickets and Merchandise

- 5.1.6 Others

- 5.2 By Streaming Platform

- 5.2.1 Twitch

- 5.2.2 YouTube Gaming

- 5.2.3 Facebook Gaming

- 5.2.4 Huya

- 5.2.5 DouYu

- 5.2.6 Other Platforms

- 5.3 By Device Type

- 5.3.1 PC

- 5.3.2 Mobile/Handheld

- 5.3.3 Console

- 5.4 By Game Genre

- 5.4.1 MOBA

- 5.4.2 First-Person Shooter (FPS)

- 5.4.3 Battle-Royale

- 5.4.4 Sports and Racing

- 5.4.5 Fighting

- 5.4.6 Strategy and Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Strategic Developments

- 6.2 Vendor Positioning Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.3.1 Tencent Holdings Ltd (Riot Games)

- 6.3.2 Activision Blizzard Inc

- 6.3.3 Electronic Arts Inc

- 6.3.4 Epic Games Inc

- 6.3.5 Valve Corporation

- 6.3.6 Modern Times Group (ESL FACEIT Group)

- 6.3.7 Gfinity PLC

- 6.3.8 Capcom Co Ltd

- 6.3.9 Ubisoft Entertainment SA

- 6.3.10 Take-Two Interactive Software Inc

- 6.3.11 Krafton Inc

- 6.3.12 Garena Online (Sea Ltd)

- 6.3.13 Nintendo Co Ltd

- 6.3.14 Bandai Namco Holdings Inc

- 6.3.15 NetEase Inc

- 6.3.16 Sony Interactive Entertainment LLC

- 6.3.17 Cloud9 Esports Inc

- 6.3.18 Team Liquid Enterprises BV

- 6.3.19 100 Thieves LLC

- 6.3.20 Fnatic Ltd

- 6.3.21 OG Esports A/S

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

2026年全球電競市場報告

2026年全球電競市場報告 電子競技市場:2026-2032年全球市場預測(以交付方式、遊戲類型、發行方式及收入模式分類)

電子競技市場:2026-2032年全球市場預測(以交付方式、遊戲類型、發行方式及收入模式分類) 電子競技市場分析及至2035年預測:類型、產品類型、服務、技術、組件、應用、最終用戶、解決方案、形式2026年全球電競內容製作市場報告

電子競技市場分析及至2035年預測:類型、產品類型、服務、技術、組件、應用、最終用戶、解決方案、形式2026年全球電競內容製作市場報告 電子競技市場規模、佔有率、趨勢和預測:收入模式、平台、遊戲和地區,2026-2034 年

電子競技市場規模、佔有率、趨勢和預測:收入模式、平台、遊戲和地區,2026-2034 年 2026-2034年全球電子競技市場規模、佔有率、趨勢和成長分析報告日本電子競技市場規模、佔有率、趨勢和預測:按收入模式、平台、遊戲和地區分類,2026-2034年

2026-2034年全球電子競技市場規模、佔有率、趨勢和成長分析報告日本電子競技市場規模、佔有率、趨勢和預測:按收入模式、平台、遊戲和地區分類,2026-2034年 電子競技市場規模、佔有率和成長分析(按收入、直播類型、遊戲類型和地區分類)-2026-2033年產業預測

電子競技市場規模、佔有率和成長分析(按收入、直播類型、遊戲類型和地區分類)-2026-2033年產業預測 電競的全球市場:種類·收益來源·各地區 (~2032年)

電競的全球市場:種類·收益來源·各地區 (~2032年) 電子競技市場 (~2035年):串流類型·遊戲種類·設備類型·串流平台·收益源·各地區的產業趨勢與全球預測

電子競技市場 (~2035年):串流類型·遊戲種類·設備類型·串流平台·收益源·各地區的產業趨勢與全球預測