|

市場調查報告書

商品編碼

1851060

即時支付:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)Real-Time Payments - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

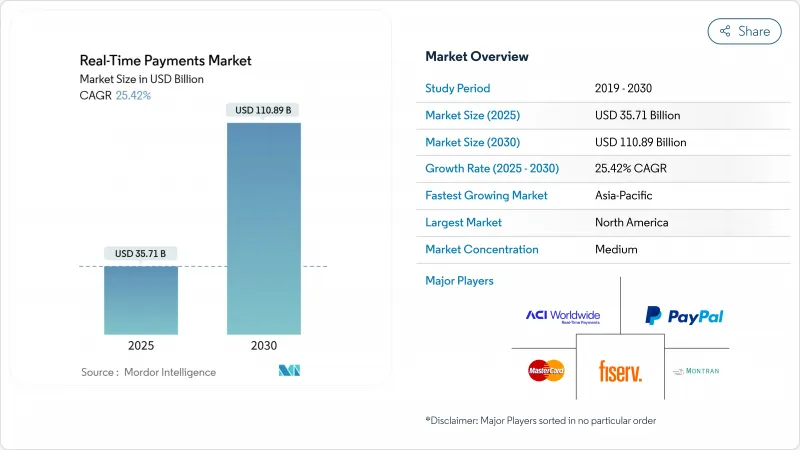

預計到 2025 年,即時支付市場規模將達到 357.1 億美元,到 2030 年將達到 1,108.9 億美元,年複合成長率為 25.42%。

監管要求、2025年11月ISO 20022標準的最後期限以及消費者對零售、薪資和帳單支付等工作流程中即時支付的需求,共同推動了即時支付的普及。在北美,FedNow Rails截至2025年4月已接入1300家金融機構,並在2025年第一季處理了131萬筆交易,總額達486億美元,展現出強大的網路效應。歐洲的即時支付監管條例將於2025年1月生效,該條例要求歐元區全天候24小時服務,這將加速銀行的技術投資。亞太地區的成長勢頭得益於印度UPI擴展到更多支付通道以及新加坡的Project Nexus項目,而巴西的PIX預計將在2023年處理420億筆交易,總額達17.2兆美元(3.44兆美元),凸顯了政府主導方案的規模經濟效益。

全球即時支付市場趨勢與洞察

向 ISO 20022 過渡加速基礎設施現代化

2025年11月ISO 20022標準的最後期限迫使銀行同時更新其通訊和處理引擎,因此採用即時支付軌道成為最具成本效益的合規途徑。 SWIFT指出,目前已有32.9%的跨國訊息符合ISO 20022標準,預計2024年第四季,這一比例將增加6個百分點。更豐富的數據有效載荷有助於改善製裁篩選,德意志銀行強調了即時合規對企業的益處。隨著共存期即將結束,金融機構必須避免雙系統帶來的額外開銷。社區銀行正透過將ISO 20022轉換和即時支付連接外包給捆綁式第三方處理商來彌補能力差距。

FedNow業務擴張推動其在美洲市場佔據領先地位。

FedNow的網路效應顯而易見,2025年第一季以季度為基礎交易量較上季成長43.1%,交易額較上季成長140.8%,預示著其商業性應用前景廣闊。美國聯邦儲備委員會的目標是在8,000家機構部署該系統,力求實現全國的普及。同時,巴西的PIX 2.0計畫於2025年9月推出定期和分期付款功能,標誌著一個成熟的系統正在向多功能平台演進。這些舉措將為其他市場樹立跨洲際的績效標竿。

詐欺監控的複雜性限制了實施速度。

銀行被迫為 FedNow、PIX 和 SEPA Instant 分別投資開發不同的規則集。 ACI Worldwide 與 Banfico 合作的歐洲概念驗證計畫展示了夥伴關係,以滿足歐盟 2025 年 10 月的合規期限。 Visa 收購 Featurespace 凸顯了基於人工智慧的即時詐欺偵測技術對資本的密集需求。小型金融機構面臨平行系統帶來的營運負擔,以及存取多個網路耗時的流程。

細分市場分析

到2024年,點對點支付將佔即時支付市場收入的55.1%,這印證了消費者對點支付的接受度。企業主導的支付流程如今已超過個人轉賬,隨著即時薪水支付和商家支付的普及,企業對點交易正以每年28.61%的速度成長。 FedNow早期針對薪水支付和供應商支付的企業試點計畫凸顯了這一轉變,表明營運資金的益處已引起財務主管的共鳴。雖然企業對企業支付的普及仍處於早期階段,但考慮到ACH結算需要數天時間,它代表最大的潛在用戶群體。隨著「先買後付」(BNPL)服務提供者整合帳戶間支付,以極低的交換成本實現的消費者對企業支付流程正在加速發展。巴西的PIX系統體現了這種轉變,預計到2025年,電子商務商家將透過即時支付創造300億美元的累計。在海灣合作理事會成員國中,政府對個人的強制規定催生了人們對全天候取款的新基本期望,鞏固了即時基礎設施作為公共服務標準的地位。

即時薪資發放的趨勢重塑了薪資核算經濟格局,推動交易頻率而非單筆金額成長,並提升了鐵路貨運總量。企業同步財務和應付帳款流程,從每週支付轉向按需推送。跨國企業利用UPI-PayNow等雙邊支付方式縮短東南亞供應商的付款週期。市場平台引入分期付款模式,同時處理手續費和本金,消除對帳延遲。這些應用場景使得即時支付市場成為最佳化流動性的關鍵。

到2024年,平台和解決方案支出將佔總收入的75.6%,這顯示銀行更傾向於整體性改革而非戰術性附加功能。訊息轉換、詐欺分析和API編配在整合架構上效率最高,這也是ISO 20022標準的實施成為推動這一趨勢的催化劑。然而,服務收入年增率為29.23%,反映出銀行在分階段推廣方面高度依賴專業整合商。諮詢服務包括準備評估、藍圖設計和監管差距分析。金融機構正在將需要全天候執行時間服務等級協定(SLA)的託管服務外包,以確保合規性並減少人員配置。像ACI Worldwide這樣的整合合作夥伴在2025年第一季軟體業務成長了42%,證明平台和專業服務在中型金融機構中越來越受歡迎。

在預測期內,能夠編配即時和批量流程的中間件將至關重要。採用容器化微服務的混合雲編排器將實現與傳統核心系統的逐步解耦。這種架構將使銀行能夠透過即時支付 API 為客戶提供前端服務,同時逐步淘汰大型主機模組。培訓計畫將著重於推動營運文化向持續結算和即時流動性監控的轉變。

區域分析

預計到2024年,北美地區的收入佔有率將達到38.1%,這主要得益於FedNow和清算所即時支付網路(RTP)的成熟。隨著區域性銀行攜手合作,並在打包雲端連接器的支持下,交易量成長將加速。關於即時簽帳金融卡交換費處理的監管政策的明確性將推動商戶採用該技術。加拿大計劃於2026年推出即時鐵路服務,預計開闢一條與美國之間以美元計價的跨國通道。

亞太地區到2030年將維持最高的複合年成長率,達到29.33%。印度的統一支付介面(UPI)在2024會計年度將處理1,310億筆交易,交易額達200兆印度盧比(約2.4兆美元),展現了政府支持的開放API模式的規模經濟效益。新加坡的「Nexus計劃」提出了多邊支付的模板,澳洲的「新支付平台」(NPP)最終確定了「PayTo」授權,並擴展了企業收費功能。日本各地區銀行正在加速現代化進程,以實現無現金支付比例目標。

自2025年1月起,歐洲將強制實施全天候(24/7)收款,德意志銀行當月即時支付業務量激增27%。預計到2025年10月,隨著全面發送功能的推出,即時支付的普及率將進一步提高,但監管機構設定的價格上限可能會對續費利潤率造成壓力。北歐地區暫停實施P27協議意味著SEPA即時支付將成為歐洲事實上的跨境支付標準,各銀行正尋求與英國的聯邦支付系統(FPS)建立雙邊連結。

PIX在南美洲處於領先地位,目前正拓展至分期付款及線下支付模式,徹底消除現金的使用場景。哥倫比亞、智利和阿根廷正在考慮複製PIX的官民合作關係模式。中東地區正經歷政策主導的成長,沙烏地阿拉伯的Sarie Rail和阿拉伯聯合大公國的IPP都強制要求公務員即時領取薪水。在非洲,行動支付企業正在整合開放回路式即時支付系統,將錢包的普及性與銀行級清算結合。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 在歐洲和亞太地區推廣符合 ISO 20022 標準的國內鐵路

- FedNow 的擴展和即將推出的 PIX 2.0 將加速美洲地區的普及應用

- 美國零工勞動者對即時薪資核算和已賺工資獲取(EWA)的需求

- 歐洲的「先買後付」(BNPL)企業正在轉向RTP(即時支付)以實現商家即時支付。

- 海灣合作理事會國家政府強制要求即時支付工資和社會福利

- RippleNet 和 Visa Direct 推動跨境 RTP 通道激增

- 市場限制

- RTP計畫中詐欺監控標準分散

- 亞洲二線銀行傳統核心銀行體系現代化改造積壓問題

- 卡片標記化和帳戶間鐵路互通性差距

- 美國商家額外費用法規的不確定性

- 價值鏈分析

- 監理與標準展望

- 波特五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

- 評估市場宏觀經濟趨勢

- 案例研究和應用案例

- RTP交易佔總交易量的百分比 - 按地區和主要國家/地區分類的百分比

- 非現金交易中即時支付交易的百分比 - 按地區和主要國家/地區細分

第5章 市場規模與成長預測

- 按交易類型

- P2P(P2P)

- 點對點(P2B)

- 按組件

- 平台/解決方案

- 服務

- 透過部署模式

- 雲

- 本地部署

- 按公司規模

- 主要企業

- 小型企業

- 按最終用戶行業分類

- 零售與電子商務

- BFSI

- 公共產業和電訊

- 衛生保健

- 政府和公共部門

- 其他終端用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 德國

- 法國

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 亞太其他地區

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 其他南美洲

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- ACI Worldwide Inc.

- Fiserv Inc.

- PayPal Holdings Inc.

- Mastercard Inc.

- Montran Corporation

- FIS Global

- Temenos AG

- Volante Technologies Inc.

- Finastra Inc.

- Ant Group(Alipay)

- Tencent Holdings Ltd.(WeChat Pay)

- The Clearing House Payments Co.

- Visa Inc.

- SWIFT SCRL

- Worldline SA

- Nets Group

- Nexi SpA

- Ripple Labs Inc.

- Wise PLC

- Pay.UK

- GoCardless Ltd.

- Jack Henry and Associates Inc.

- Infosys Finacle

- VSoft Corporation

- OpenPayd Holdings Ltd.

第7章 市場機會與未來展望

The Real Time Payments market size stands at USD 35.71 billion in 2025 and is forecast to achieve USD 110.89 billion by 2030, reflecting a compelling 25.42% CAGR.

Surging adoption originates from regulatory mandates, the November 2025 ISO 20022 deadline, and customer demand for instantaneous settlement across retail, payroll, and bill-payment workflows. In North America, the FedNow rail welcomed 1,300 institutions by April 2025 and processed 1.31 million transactions worth USD 48.6 billion during Q1 2025, underscoring strong network effects. Europe's Instant Payments Regulation, effective January 2025, requires 24/7 euro-zone coverage, accelerating bank technology investment. Asia-Pacific's momentum is reinforced by India's UPI expansion into additional corridors and Singapore's Project Nexus, while Brazil's PIX processed 42 billion transactions worth BRL 17.2 trillion (USD 3.44 trillion) in 2023, highlighting the scale benefits of government-sponsored schemes.

Global Real-Time Payments Market Trends and Insights

ISO 20022 migration accelerates infrastructure modernization

The November 2025 ISO 20022 deadline compels banks to update messaging and processing engines simultaneously, making real-time payment rail adoption the most cost-efficient compliance path. SWIFT notes that 32.9% of cross-border messages already ride ISO 20022, up six percentage points in Q4 2024. Richer data payloads improve sanctions screening, and Deutsche Bank showcases real-time compliance benefits for corporates. The looming end of the coexistence period forces institutions to avoid dual-system overhead. Community banks mitigate capability gaps by outsourcing to third-party processors that bundle ISO 20022 translation with instant-payment connectivity.

FedNow expansion drives Americas market leadership

FedNow's network effects were evident with a 43.1% quarterly volume spike in Q1 2025 and a 140.8% value leap, signalling widening commercial use cases. The Federal Reserve's ambition to onboard 8,000 institutions positions the rail for nationwide ubiquity. In parallel, Brazil's PIX 2.0 will introduce recurring and instalment capabilities in September 2025, showing how mature systems evolve into multifunction platforms. Combined, these initiatives set cross-continental performance benchmarks that other markets emulate.

Fraud monitoring complexity constrains adoption velocity

Verification-of-Payee frameworks differ across schemes, obliging banks to invest in separate rule sets for FedNow, PIX, and SEPA Instant. ACI Worldwide's European PoC with Banfico illustrates workaround partnerships to meet the EU's October 2025 compliance deadline. Visa's Featurespace acquisition underscores the capital-intensive nature of AI-based instant fraud detection. Smaller institutions face operational strain from parallel systems, slowing onboarding to multiple networks.

Other drivers and restraints analyzed in the detailed report include:

- Earned-wage access transforms payroll economics

- Cross-border RTP corridors reshape international payments

- Legacy infrastructure modernization challenges

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Peer-to-peer transfers accounted for 55.1% of Real Time Payments market revenue in 2024, underscoring widespread consumer adoption. Business-driven flows now outpace personal transfers, with peer-to-business transactions growing 28.61% annually as instant payroll disbursements and merchant settlement take hold. FedNow's early corporate pilots in payroll and supplier payments highlight this pivot, signalling that working-capital benefits resonate with finance executives. Business-to-business adoption remains in early stages but promises the largest addressable pool, given ACH's multi-day settlement drag. Consumer-to-business flows gain momentum where buy-now-pay-later (BNPL) providers embed account-to-account settlement to minimise interchange costs. Brazil's PIX demonstrates this migration, with e-commerce merchants projected to book USD 30 billion in instant-payment turnover during 2025. Government-to-person mandates across GCC economies create a new baseline expectation for 24/7 disbursement, cementing instant infrastructure as a public-service standard.

Real-time salary advances reshape payroll economics, enlarging transaction frequency rather than ticket size, thus increasing absolute rail volume. Corporates synchronise treasury and AP processes, shifting from weekly payment runs to on-demand pushes. Cross-border organisations leverage bilateral links such as UPI-PayNow to shorten supplier settlement cycles in Southeast Asia. Market platforms introduce split-payment models that route commission and principal amounts simultaneously, removing reconciliation delays. These combined use cases reinforce the Real Time Payments market as indispensable for liquidity optimisation.

Platform & solution spending captured 75.6% of 2024 revenue, signalling that banks favour holistic overhauls versus tactical bolt-ons. ISO 20022 migration serves as the triggering event, since message translation, fraud analysis, and API orchestration are most efficient on unified stacks. Yet service revenue rises 29.23% annually, reflecting heavy reliance on specialist integrators for phased rollout. Consulting engagements cover readiness assessments, roadmap design, and regulatory gap analysis. Institutions outsource managed services for SLAs covering 24/7 uptime, ensuring compliance while containing headcount. Integration partners such as ACI Worldwide logged 42% software-segment growth in Q1 2025, proving that combinational platform-plus-professional-services deals resonate with mid-tier institutions.

Over the forecast period, middleware capable of orchestrating real-time and batch flows side-by-side becomes critical. Hybrid-cloud orchestrators with containerised microservices enable progressive decoupling from legacy cores. This architecture allows banks to retire mainframe modules gradually while front-ending customers with instant-payment APIs. Training programmes address the operational culture shift to continuous settlement and real-time liquidity monitoring.

The Global Real-Time Payments Market is Segmented by Transaction Type (Peer-To-Peer (P2P), Peer-To-Business (P2B)), Component (Platform / Solution, Services), Deployment (Cloud, On-Premise), Enterprise Size (Large Enterprises, Small and Medium Enterprises), End-User Industry (Retail and E-Commerce, BFSI, Utilities & Telecom, Healthcare, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America posted 38.1% revenue share in 2024, anchored by FedNow and The Clearing House RTP network maturity. Volume growth accelerates as regional banks join en masse, aided by packaged cloud connectors. Regulatory clarity on interchange treatment for instant debit pushes merchant adoption. Canada plans Real-Time Rail launch in 2026, which could open a USD-denominated cross-border corridor with the United States.

Asia-Pacific delivers the highest CAGR at 29.33% to 2030. India's UPI handled 131 billion transactions worth INR 200 trillion (USD 2.4 trillion) in FY24, illustrating scale benefits of a government-backed open API model. Singapore's Project Nexus presents a template for multi-country clearing, while Australia's NPP finalises PayTo mandates, expanding business billing capabilities. Japan's regional banks accelerate modernization to meet the national cashless-ratio target.

Europe's mandatory 24/7 receiving requirement effective January 2025 induced a 27% instant-payment jump at Deutsche Bank that same month. Full send capability by October 2025 will drive further adoption yet may squeeze fee margins given regulation-imposed price caps. Nordic P27's pause leaves SEPA Instant as the de-facto cross-border option inside Europe, pushing banks toward bilateral links with the UK's FPS.

South America's trajectory centres on PIX, now extending to instalment and offline modes that remove the last cash use-cases. Colombia, Chile, and Argentina examine replicating PIX's public-private partnership structure. The Middle East experiences policy-driven growth where Saudi Arabia's Sarie rail and the UAE's IPP mandate instant salary credits for government workers. Africa witnesses mobile-money players integrating open-loop instant rails, blending wallet ubiquity with bank-grade clearing.

- ACI Worldwide Inc.

- Fiserv Inc.

- PayPal Holdings Inc.

- Mastercard Inc.

- Montran Corporation

- FIS Global

- Temenos AG

- Volante Technologies Inc.

- Finastra Inc.

- Ant Group (Alipay)

- Tencent Holdings Ltd. (WeChat Pay)

- The Clearing House Payments Co.

- Visa Inc.

- SWIFT SCRL

- Worldline SA

- Nets Group

- Nexi SpA

- Ripple Labs Inc.

- Wise PLC

- Pay.UK

- GoCardless Ltd.

- Jack Henry and Associates Inc.

- Infosys Finacle

- VSoft Corporation

- OpenPayd Holdings Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of ISO 20022-enabled domestic rails in Europe and Asia-Pacific

- 4.2.2 Expansion of FedNow and upcoming PIX 2.0 accelerating adoption in the Americas

- 4.2.3 Real-time payroll and earned-wage access (EWA) demand among U.S. gig workers

- 4.2.4 BNPL players shifting to RTP for instant merchant settlement in Europe

- 4.2.5 Government mandates for instant salary and welfare disbursement in GCC countries

- 4.2.6 Surging cross-border RTP corridors via RippleNet and Visa Direct

- 4.3 Market Restraints

- 4.3.1 Fragmented fraud-monitoring standards across RTP schemes

- 4.3.2 Legacy core-bank modernisation backlog in Tier-2 Asian banks

- 4.3.3 Interoperability gaps between card tokenisation and account-to-account rails

- 4.3.4 Merchant surcharge regulation uncertainty in the U.S.

- 4.4 Value Chain Analysis

- 4.5 Regulatory and Standards Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Assessment of Macro Economic Trends on the Market

- 4.8 Case Studies and Use-cases

- 4.9 RTP Transactions as % of All Transactions - Regional and Key-Country Split

- 4.10 RTP Transactions as % of Non-Cash Transactions - Regional and Key-Country Split

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Transaction Type

- 5.1.1 Peer-to-Peer (P2P)

- 5.1.2 Peer-to-Business (P2B)

- 5.2 By Component

- 5.2.1 Platform / Solution

- 5.2.2 Services

- 5.3 By Deployment Mode

- 5.3.1 Cloud

- 5.3.2 On-Premise

- 5.4 By Enterprise Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises

- 5.5 By End-User Industry

- 5.5.1 Retail and E-Commerce

- 5.5.2 BFSI

- 5.5.3 Utilities and Telecom

- 5.5.4 Healthcare

- 5.5.5 Government and Public Sector

- 5.5.6 Other End-user Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 United Kingdom

- 5.6.2.2 Germany

- 5.6.2.3 France

- 5.6.2.4 Spain

- 5.6.2.5 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Colombia

- 5.6.4.4 Rest of South America

- 5.6.5 Middle East

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)}

- 6.4.1 ACI Worldwide Inc.

- 6.4.2 Fiserv Inc.

- 6.4.3 PayPal Holdings Inc.

- 6.4.4 Mastercard Inc.

- 6.4.5 Montran Corporation

- 6.4.6 FIS Global

- 6.4.7 Temenos AG

- 6.4.8 Volante Technologies Inc.

- 6.4.9 Finastra Inc.

- 6.4.10 Ant Group (Alipay)

- 6.4.11 Tencent Holdings Ltd. (WeChat Pay)

- 6.4.12 The Clearing House Payments Co.

- 6.4.13 Visa Inc.

- 6.4.14 SWIFT SCRL

- 6.4.15 Worldline SA

- 6.4.16 Nets Group

- 6.4.17 Nexi SpA

- 6.4.18 Ripple Labs Inc.

- 6.4.19 Wise PLC

- 6.4.20 Pay.UK

- 6.4.21 GoCardless Ltd.

- 6.4.22 Jack Henry and Associates Inc.

- 6.4.23 Infosys Finacle

- 6.4.24 VSoft Corporation

- 6.4.25 OpenPayd Holdings Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

2026年全球即時支付市場報告

2026年全球即時支付市場報告 即時支付市場規模、佔有率、成長和全球行業分析:按類型、應用和地區分類的洞察,以及對 2026-2034 年的預測。

即時支付市場規模、佔有率、成長和全球行業分析:按類型、應用和地區分類的洞察,以及對 2026-2034 年的預測。 即時支付市場規模、佔有率和成長分析(按組件、類型、部署類型、公司規模、最終用戶產業和地區分類)-2026-2033年產業預測

即時支付市場規模、佔有率和成長分析(按組件、類型、部署類型、公司規模、最終用戶產業和地區分類)-2026-2033年產業預測 即時支付市場-全球產業規模、佔有率、趨勢、機會及預測(按組件、組織規模(中小企業和大型企業)、最終用戶、地區和競爭格局分類,2020-2030 年預測)

即時支付市場-全球產業規模、佔有率、趨勢、機會及預測(按組件、組織規模(中小企業和大型企業)、最終用戶、地區和競爭格局分類,2020-2030 年預測) 按組件、部署模式、組織規模、交易類型、應用程式和最終用戶分類的即時支付市場 - 全球預測 2025-2032 年

按組件、部署模式、組織規模、交易類型、應用程式和最終用戶分類的即時支付市場 - 全球預測 2025-2032 年 日本即時支付市場報告(按支付類型(P2P、P2B)和地區)2025-2033 年

日本即時支付市場報告(按支付類型(P2P、P2B)和地區)2025-2033 年 即時付款:2025-2029 年全球市場

即時付款:2025-2029 年全球市場 即時付款市場:按組件、按付款類型、按部署模式、按地區

即時付款市場:按組件、按付款類型、按部署模式、按地區 印度的即時付款市場的評估:各類型,各認證方法,各終端用戶,各地區,機會,預測,2018年~2032年

印度的即時付款市場的評估:各類型,各認證方法,各終端用戶,各地區,機會,預測,2018年~2032年 中國即時付款市場:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

中國即時付款市場:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)