|

市場調查報告書

商品編碼

1851021

工業感測器:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)Industrial Sensors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

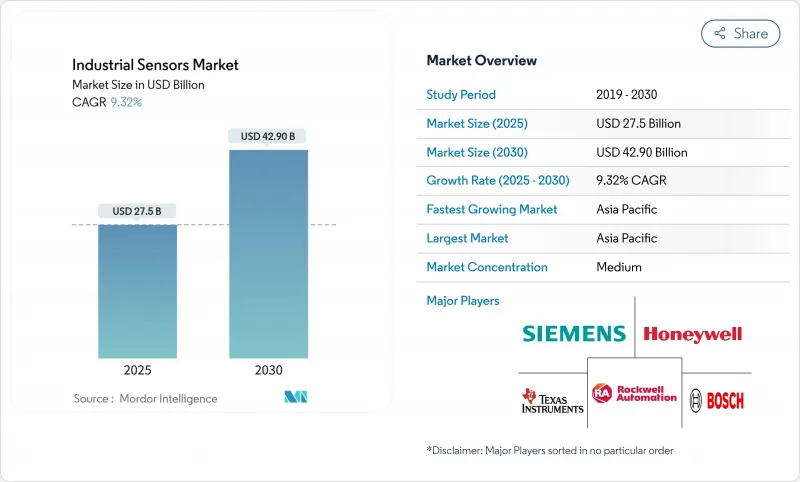

預計到 2025 年,工業感測器市場規模將達到 275 億美元,到 2030 年將擴大到 429 億美元,複合年成長率為 9.3%。

強勁的需求源自於工廠數位化程度的提高、邊緣設備的普及以及簡化系統整合的開放通訊協定的廣泛應用。製造商將密集型感測器網路視為自動駕駛的“耳目”,無需將所有數據上傳至雲端即可實現現場快速決策。能源密集型產業正在部署精細化感測技術以滿足日益嚴格的脫碳要求,而棕地工廠則正在加速進行IO-Link維修,以獲取資產健康數據。在技術方面,感測器內建人工智慧和多重通訊協定連接正在重塑工業感測器市場,增強關鍵任務環境中的反應速度和韌性。

全球工業感測器市場趨勢與洞察

工業4.0/工業物聯網應用激增

面臨數位化挑戰的製造商正推動工業感測器市場蓬勃發展。密集的感測器網路是工業物聯網 (IIoT) 架構的基礎,能夠即時擷取溫度、壓力和流量等數據,將以往各自獨立的機械設備轉變為智慧資產。隨著工廠將分析環節更靠近生產流程,降低延遲並緩解對雲端頻寬的需求,預計邊緣運算領域的支出將大幅成長。亞太地區尤其如此,中國的智慧工廠政策和日本的自動化主導正在加速感測器的應用。

對預測性維護和遠端監控的需求

數據主導的維護策略正日益普及,因為及早發現故障可以減少代價高昂的停機時間。透過部署結合振動、溫度和聲波感測器以及邊緣人工智慧模型的設備,可以在降低網路流量的同時,實現超過 90% 的預測準確率。流程工業由於其嚴格的安全要求而重視這些功能,但投資回報率的計算必須考慮整合工作和組織變革。

高額資本支出和複雜的整合

對於中小企業而言,如果將網路升級、中介軟體和整合服務等費用納入考量,計劃總成本通常會是材料清單的三到四倍。維修原有的MES和ERP平台以適應異質感測器輸出,可能會導致漫長的實施過程,並且需要專門的資源。

細分市場分析

液位感測器預計在2024年佔銷售額的18.4%,為化學、石油和水處理等行業的工業感測器市場提供至關重要的庫存管理功能。同時,受線上機器視覺系統在自動化缺陷檢測領域日益普及的推動,影像/視覺設備預計將以11.2%的複合年成長率成長。儘管有線類比感測器仍受到工廠的青睞,因為它們可靠性久經考驗,但具備自我診斷功能的數位感測器也在快速發展。供應商正在根據ESG(環境、社會和治理)要求,將用於能源監測的MEMS(微機電系統)壓力和流量感測器小型化。

次要趨勢包括:結合光學和超音波技術的混合感測平台,旨在提高對複雜固體材料測量的精度;以及嵌入輕便型相機的邊緣人工智慧技術,可在不佔用過多頻寬的情況下實現設備端異常檢測。這些動態可能會推動工業液位測量感測器市場保持其主導地位,即便新興成像技術正在吸引更多投資。

到2024年,離散製造將佔據工業感測器市場31%的佔有率。在對連續設備監測的強勁需求推動下,工廠不斷升級到可同時擷取振動、溫度和位置資料的多功能感測器。生命科學和製藥產業預計到2030年將以9.8%的複合年成長率成長,這主要得益於無菌生產環境更嚴格的驗證通訊協定以及連續生產線的日益普及。

化學和石化企業在旨在最佳化產量比率的數位雙胞胎框架內部署了強大的排放氣體監測解決方案。礦業公司正在試驗利用密集環境感測技術來導航危險區域的集群機器人系統。電力公共產業在電網現代化改造過程中,正在整合光纖和壓電感測器,以改善可再生能源發電預測和資產管理,從而將工業感測器產業拓展到新的能源領域。

工業感測器市場按感測器類型(流量、壓力及其他)、終端用戶產業(化工及石化、礦業及冶金、電力及能源、食品及飲料及其他)、技術(有線/模擬、邊緣AI/虛擬感測器及其他)、通訊協定(現場匯流排及其他)及地區進行細分。所有細分市場的市場規模和預測均以美元計價。

區域分析

亞太地區將在2024年佔全球支出的44%,這反映了持續的政策獎勵和強大的機器人生態系統。中國在「中國製造2025」計畫的推動下,將佔全球工業機器人出貨量的52%,並且作為汽車和家電中心,其感測器訂單量強勁。日本提供尖端的自動化技術,而韓國則在政府聯合投資的推動下,加速智慧工廠的普及。

北美在多元化、小批量生產和能源基礎設施升級方面仍然至關重要。工廠正在整合邊緣人工智慧感測器,以推動預測性維護並提高工人安全。歐洲市場的成長與強制持續排放氣體監測的脫碳法規一致,刺激了對高精度流量和氣體分析感測器的需求。中東、非洲和南美洲的新興經濟體正在加速基礎建設,推動採礦、金屬和發電工程對相關技術的應用日益廣泛。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 工業4.0/工業物聯網主流應用激增

- 對預測性維護和遠端監控的主流需求

- 以機器人為中心的智慧工廠發展已成為主流

- 隱蔽的邊緣AI感測器節點降低雲延遲

- 棕地工廠IO-Link改裝浪潮

- 淨零排放指令能夠實現精細化的能源檢測

- 市場限制

- 主流方案:資本投入高,整合難度高

- 網路感測器中的網路安全漏洞

- 幕後資料主權規則限制了跨境分析

- OT-IT技能的隱性短缺減緩了技術的採用。

- 價值/供應鏈分析

- 監管環境

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 依感測器類型

- 流動

- 壓力

- 鄰近/區域

- 等級

- 溫度

- 圖像/視覺

- 光電

- 其他類型

- 按最終用戶行業分類

- 化工/石油化工

- 採礦和金屬

- 電力和能源

- 飲食

- 生命科學與製藥

- 航太/國防

- 用水和污水

- 其他行業

- 透過技術

- 有線/模擬

- 有線/數字(智慧)

- 無線的

- 邊緣人工智慧/虛擬感測器

- 透過通訊協定

- 現場匯流排(例如 PROFIBUS、Modbus)

- 工業乙太網(PROFINET、EtherNet/IP、EtherCAT)

- IO-Link

- 無線ICP(Wi-Sun、6LoWPAN、BLE-Mesh)

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 其他南美洲

- 歐洲

- 德國

- 英國

- 法國

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 韓國

- 越南

- 亞太其他地區

- 中東和非洲

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Siemens AG

- Honeywell International Inc.

- Texas Instruments Inc.

- Rockwell Automation Inc.

- Bosch Sensortec GmbH

- TE Connectivity Ltd.

- ABB Ltd.

- STMicroelectronics NV

- Infineon Technologies AG

- NXP Semiconductors NV

- Omron Corporation

- Sick AG

- Emerson Electric Co.

- Schneider Electric SE

- Balluff GmbH

- Pepperl+Fuchs SE

- Keyence Corporation

- IFM Electronic GmbH

- Yokogawa Electric Corp.

- Endress+Hauser AG

- Analog Devices Inc.

第7章 市場機會與未來展望

The industrial sensors market reached USD 27.5 billion in 2025 and is forecast to advance to USD 42.9 billion by 2030, delivering a 9.3% CAGR.

Strong demand stems from rising factory digitalization, deeper penetration of edge-ready devices, and wider availability of open communications protocols that simplify system integration. Manufacturers view dense sensor networks as the "eyes and ears" of automated operations, enabling faster decisions on the shop floor without routing all data to the cloud. Energy-intensive sectors now deploy granular sensing to comply with tightening decarbonization mandates, while brown-field plants accelerate IO-Link retrofits to unlock asset-health data. On the technology front, in-sensor AI and multi-protocol connectivity are redefining the industrial sensors market, enhancing responsiveness and resilience in mission-critical environments.

Global Industrial Sensors Market Trends and Insights

Industry 4.0 / IIoT Adoption Surge

Manufacturers under competitive pressure to digitize operations keep fueling an upswing in the industrial sensors market. Dense sensor grids underpin IIoT architectures that collect real-time data on temperature, pressure, and flow, transforming previously disconnected machines into intelligent assets. Edge computing spend is projected to rise steeply as plants shift analytics closer to the process, trimming latency and easing cloud bandwidth demands. The trend is pronounced in Asia-Pacific where China's smart-factory mandates and Japan's automation leadership accelerate sensor uptake.

Predictive Maintenance & Remote Monitoring Demand

Data-driven maintenance strategies are gaining traction because early fault detection curbs costly downtime. Facilities deploying vibration, thermal, and acoustic sensors coupled with edge AI models achieve prediction accuracies above 90% while lowering network traffic. Process industries value these capabilities due to stringent safety requirements, yet ROI calculations must account for integration work and organizational change.

High Capex and Integration Complexity

Small and mid-size enterprises often face total project costs three to four times higher than the bill of materials once network upgrades, middleware, and integration services are included. Retrofitting legacy MES and ERP platforms to accommodate heterogeneous sensor outputs prolongs implementation and demands specialist talent.

Other drivers and restraints analyzed in the detailed report include:

- Robot-centric Smart-factory Expansion

- Cyber-security Vulnerabilities of Networked Sensors

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Level sensors accounted for 18.4% of 2024 revenue, anchoring the industrial sensors market with indispensable inventory-control functionality in chemicals, oil, and water-treatment operations. Image/vision devices, meanwhile, are forecast for an 11.2% CAGR as inline machine-vision systems proliferate for automated defect detection. Wired analog versions remain widespread because factories value proven reliability, but digital variants with self-diagnostics are advancing fast. Suppliers are miniaturizing MEMS pressure and flow sensors for energy-monitoring tasks aligned with ESG mandates.

Second-order trends point to hybrid sensing platforms that combine optical and ultrasonic techniques to boost accuracy for challenging solid-material measurements. Edge AI incorporated within compact cameras now enables on-device anomaly detection without bandwidth strain. These dynamics position the industrial sensors market size for level measurement to retain a commanding share even as emerging imaging technologies capture incremental spend.

Discrete manufacturing held 31% of the industrial sensors market share in 2024 due to persistent investments in automotive and electronics lines. Robust demand for continuous equipment monitoring keeps factories upgrading to multifunctional sensors that capture vibration, temperature, and positional data concurrently. Life sciences and pharmaceuticals are projected to achieve a 9.8% CAGR through 2030, benefitting from stricter validation protocols for sterile production environments and wider adoption of continuous-manufacturing lines.

Manufacturers in chemicals and petrochemicals deploy rugged solutions for emissions monitoring within digital-twin frameworks aimed at optimizing yield. Mining operators experiment with swarm-robotics systems that rely on dense environmental sensing to navigate hazardous zones. Utilities modernizing grids integrate fiber-optic and piezoelectric sensors to improve renewable-generation forecasting and equipment asset management, extending the industrial sensors industry into new energy verticals.

The Industrial Sensors Market is Segmented by Sensor Type (Flow, Pressure, and More), End-User Industry (Chemical & Petrochemicals, Mining & Metals, Power & Energy, Food & Beverage and More), Technology (Wired / Analog, Edge-AI / Virtual Sensors and More), Communication Protocol (Fieldbus and More), Geography. The Market Sizes and Forecasts are Provided in Terms of Value (USD) for all the Segments.

Geography Analysis

Asia-Pacific captured 44% of 2024 spending, reflecting ongoing policy incentives and a strong robotics ecosystem. China dominates installations, propelled by the Made in China 2025 program and a 52% share of global industrial-robot shipments, translating into vigorous sensor orders across automotive and consumer-electronics hubs. Japan contributes cutting-edge automation technologies, while South Korea's government co-investment accelerates smart-factory penetration.

North America remains pivotal for high-mix, low-volume production and energy-infrastructure renewal. Plants integrate edge-AI sensors to advance predictive maintenance and enhance workforce safety. Europe's market growth aligns with decarbonization rules that require continuous emissions monitoring, stimulating demand for high-precision flow and gas-analysis sensors. Emerging economies in the Middle East, Africa, and South America increase uptake for mining, metals, and power-generation projects as infrastructure build-outs gather momentum.

- Siemens AG

- Honeywell International Inc.

- Texas Instruments Inc.

- Rockwell Automation Inc.

- Bosch Sensortec GmbH

- TE Connectivity Ltd.

- ABB Ltd.

- STMicroelectronics N.V.

- Infineon Technologies AG

- NXP Semiconductors N.V.

- Omron Corporation

- Sick AG

- Emerson Electric Co.

- Schneider Electric SE

- Balluff GmbH

- Pepperl+Fuchs SE

- Keyence Corporation

- IFM Electronic GmbH

- Yokogawa Electric Corp.

- Endress+Hauser AG

- Analog Devices Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mainstream Industry 4.0 / IIoT adoption surge

- 4.2.2 Mainstream Predictive maintenance & remote monitoring demand

- 4.2.3 Mainstream Robot-centric smart-factory expansion

- 4.2.4 Under-the-radar Edge-AI sensor nodes cut cloud latency

- 4.2.5 Under-the-radar IO-Link retrofit wave in brown-field plants

- 4.2.6 Under-the-radar Net-zero mandates drive granular energy sensing

- 4.3 Market Restraints

- 4.3.1 Mainstream High capex & integration complexity

- 4.3.2 Mainstream Cyber-security vulnerabilities of networked sensors

- 4.3.3 Under-the-radar Data-sovereignty rules limit cross-border analytics

- 4.3.4 Under-the-radar OT-IT skills shortage slows deployments

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porters Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE & GROWTH FORECASTS (VALUE)

- 5.1 By Sensor Type

- 5.1.1 Flow

- 5.1.2 Pressure

- 5.1.3 Proximity / Area

- 5.1.4 Level

- 5.1.5 Temperature

- 5.1.6 Image / Vision

- 5.1.7 Photo-electric

- 5.1.8 Other Types

- 5.2 By End-user Industry

- 5.2.1 Chemical & Petrochemicals

- 5.2.2 Mining & Metals

- 5.2.3 Power & Energy

- 5.2.4 Food & Beverage

- 5.2.5 Life Sciences & Pharmaceuticals

- 5.2.6 Aerospace & Defense

- 5.2.7 Water & Waste-water

- 5.2.8 Other Industries

- 5.3 By Technology

- 5.3.1 Wired / Analog

- 5.3.2 Wired / Digital (Smart)

- 5.3.3 Wireless

- 5.3.4 Edge-AI / Virtual Sensors

- 5.4 By Communication Protocol

- 5.4.1 Fieldbus (e.g., PROFIBUS, Modbus)

- 5.4.2 Industrial Ethernet (PROFINET, EtherNet/IP, EtherCAT)

- 5.4.3 IO-Link

- 5.4.4 Wireless ICPs (Wi-Sun, 6LoWPAN, BLE-Mesh)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Rest of Europe

- 5.5.4 APAC

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 Vietnam

- 5.5.4.5 Rest of APAC

- 5.5.5 Middle East & Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Siemens AG

- 6.4.2 Honeywell International Inc.

- 6.4.3 Texas Instruments Inc.

- 6.4.4 Rockwell Automation Inc.

- 6.4.5 Bosch Sensortec GmbH

- 6.4.6 TE Connectivity Ltd.

- 6.4.7 ABB Ltd.

- 6.4.8 STMicroelectronics N.V.

- 6.4.9 Infineon Technologies AG

- 6.4.10 NXP Semiconductors N.V.

- 6.4.11 Omron Corporation

- 6.4.12 Sick AG

- 6.4.13 Emerson Electric Co.

- 6.4.14 Schneider Electric SE

- 6.4.15 Balluff GmbH

- 6.4.16 Pepperl+Fuchs SE

- 6.4.17 Keyence Corporation

- 6.4.18 IFM Electronic GmbH

- 6.4.19 Yokogawa Electric Corp.

- 6.4.20 Endress+Hauser AG

- 6.4.21 Analog Devices Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

工業感測器市場:2026-2032年全球市場預測(按感測器類型、技術、通訊協定、應用和銷售管道)

工業感測器市場:2026-2032年全球市場預測(按感測器類型、技術、通訊協定、應用和銷售管道) 工業感測器市場機會、成長要素、產業趨勢分析及2026年至2035年預測

工業感測器市場機會、成長要素、產業趨勢分析及2026年至2035年預測 半導體氣體感測器市場分析及預測至 2035 年:按類型、產品、技術、應用、材料類型、最終用戶、功能和安裝類型分類。工業感測器市場分析及預測(至2035年):依類型、產品類型、技術、組件、應用、最終用戶、功能、安裝類型、設備及解決方案分類

半導體氣體感測器市場分析及預測至 2035 年:按類型、產品、技術、應用、材料類型、最終用戶、功能和安裝類型分類。工業感測器市場分析及預測(至2035年):依類型、產品類型、技術、組件、應用、最終用戶、功能、安裝類型、設備及解決方案分類 中國工業感測器市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

中國工業感測器市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 日本工業自動化感測器市場規模、佔有率、趨勢及預測(按感測器類型、類型、自動化模式、最終用戶和地區分類,2026-2034年)

日本工業自動化感測器市場規模、佔有率、趨勢及預測(按感測器類型、類型、自動化模式、最終用戶和地區分類,2026-2034年) 2026年全球工業感測器市場報告

2026年全球工業感測器市場報告 半導體氣體感測器市場-2026-2031年預測單單點感測器市場按技術、性別、功率、安裝方式、應用和最終用戶產業分類-2026-2032年全球預測按感測器類型、技術、應用、最終用戶和分銷管道分類的中風感測器市場—2026-2032年全球預測

半導體氣體感測器市場-2026-2031年預測單單點感測器市場按技術、性別、功率、安裝方式、應用和最終用戶產業分類-2026-2032年全球預測按感測器類型、技術、應用、最終用戶和分銷管道分類的中風感測器市場—2026-2032年全球預測