|

市場調查報告書

商品編碼

1851020

安全資訊和事件管理 (SIEM):市場佔有率分析、行業趨勢、統計數據和成長預測 (2025-2030)Security Information And Event Management (SIEM) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

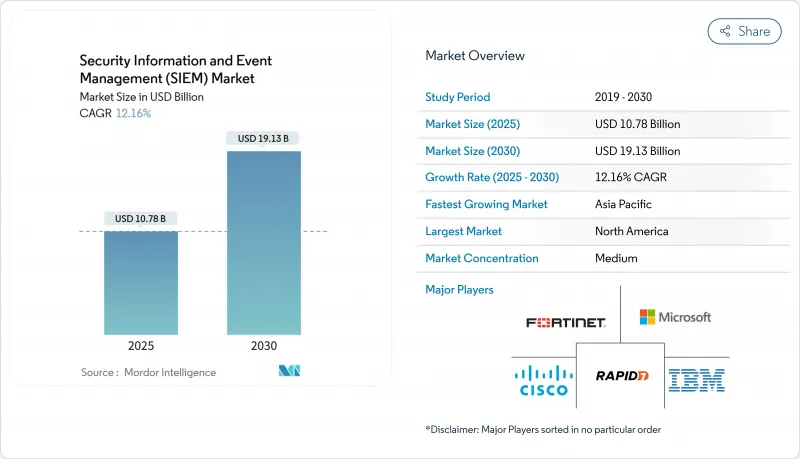

全球 SIEM 市場預計到 2025 年將達到 107.8 億美元,到 2030 年將達到 191.3 億美元,複合年成長率為 12.16%。

雲端工作負載遙測技術的普及、嚴格的監管要求以及供應商的快速整合是推動成長要素。大型企業隨著攻擊面的擴大而持續擴展日誌採集,而中小企業則透過雲端原生消費模式進入市場。北美市場的需求主要受SOX和PCI DSS法規的驅動,而歐洲市場的支出則因NIS2和DORA法規的實施而加速成長。供應商的藍圖目前圍繞著人工智慧驅動的分析、整合資料管道和簡化的授權模式展開——這些主題將在思科於2024年完成對Splunk的里程碑式收購後,推動產品更新換代。

全球安全資訊與事件管理 (SIEM) 市場趨勢與洞察

安全遙測技術的指數級成長

企業每天從終端、雲端服務和操作技術產生Terabyte的日誌。如此龐大的日誌量給傳統的資料收集模型帶來了巨大壓力,同時也為威脅偵測提供了豐富的上下文資訊。 CPFL Energia 透過現代化的安全資訊和事件管理 (SIEM) 系統監控超過5萬台智慧電網設備,該系統將高價值事件路由到資料湖以進行成本控制。雲端原生彈性架構能夠應對突發事件高峰,而選擇性保留機制則確保了儲存費用的可預測性。那些將低成本物件儲存與查詢元資料結合的供應商正受到客戶的青睞,這些客戶需要在覆蓋範圍和成本之間尋求平衡。

加重監管處罰和審核

在歐洲,NIS2 要求關鍵服務提供者記錄、監控並保留事件資料以進行事件重建,這使得安全預算佔 IT 支出的比例上升至 9.0%。在金融業,DORA 強制要求即時檢測和報告。 Reimi 銀行升級了其 SIEM 系統後,誤報率降低了 70%,該系統專注於創建審核證據。醫療保健機構因違反 HIPAA 法規而面臨罰款,平均罰款金額為 488 萬美元。

總擁有成本高

傳統的事件授權模式會造成安全盲點,迫使買家設定資料攝取上限。硬體關稅將在2024年之前使設備成本增加20%,加重預算壓力。儲存、出口流量和進階分析等隱性雲端費用令初次使用者措手不及。供應商目前正在推廣管道卸載層級和固定費率定價模式,以恢復價格的可預測性。

細分市場分析

到2024年,本地部署的SIEM將佔據55.75%的市場。這個細分市場主要由受嚴格資料主權政策約束的行業支撐,但由於硬體成本上升和技能短缺日益嚴重,其成長速度正在放緩。雲端SIEM將以13.40%的複合年成長率成長,透過彈性擴展和計量收費,擴大用戶對高階分析的存取。混合架構則扮演橋樑的角色,將受監管的資料保留在本地節點上,同時將遠端檢測資料串流傳輸到雲端的低成本物件儲存。

雲端技術的採用將升級週期從多年的設備更新轉變為持續的功能交付。西門子採用混合模式,在本地運行OT解析器,同時在雲端豐富事件訊息,以進行威脅情報關聯。隨著授權模式轉向資料使用,買家可以更清楚地了解每種部署方案的SIEM市場規模。供應商整合正在加速從老舊的本地部署架構向由超大規模雲端服務商託管的現代化SaaS產品的轉型。

到 2024 年,傳統平台將佔總收入的 46.20%,但隨著資料規模的擴大,查詢效能和規則調優能力下降,其市場佔有率將會減少。下一代雲端原生引擎將以 18.10% 的複合年成長率 (CAGR) 實現最快成長,在所有架構類型中成長最高。這些系統透過將儲存與計算解耦,並在資料攝取階段整合機器學習,從而縮短平均發現時間。

Palo Alto Networks 將 QRadar SaaS 整合到 Cortex XSI AM 中,收購後的第一個季度就累計了超過 9,000 萬美元的收入。開放原始碼堆疊雖然在預算有限的情況下佔有了一席之地,但需要深厚的工程技術能力。遷移工具和相容層簡化了從傳統規則語法到讀取時模式模型的過渡。 SIEM 市場更傾向於將遙測資料視為巨量資料而非事件流的架構。

SIEM 市場報告按部署方式(本地部署、其他)、SIEM 架構(傳統 SIEM、下一代 SIEM、其他)、組件(平台/軟體、專業服務、託管 SIEM 服務 (MSSP))、組織規模(中小型企業、大型企業)、最終用戶垂直行業(銀行、金融服務、保險 (BFSI)、零售、電子商務、其他)和地區細分行業。

區域分析

2024年,北美將佔據SIEM市場39.20%的收入佔有率,這主要得益於成熟的資料外洩通知法規和高額的網路保險費。由於董事會將安全控制與信託風險掛鉤,預算撥款依然強勁。該地區對雲端運算和人工智慧的早期應用進一步鞏固了其市場領先地位。儘管市場基數已趨於飽和,但由於整合可觀測性解決方案的提升銷售,成長率仍保持在中等個位數水準。

亞太地區預計將以11.80%的複合年成長率實現全球最快成長。中國的多層防護體系和印度的《數位個人資料保護法》正在推動關鍵資訊基礎設施的強制日誌。國內雲端供應商正與全球安全資訊和事件管理(SIEM)廠商合作,以滿足本地化法規要求。日本企業集團在主權和容量之間尋求平衡,傾向於採用混合型SIEM方案,將原始事件儲存在東京地區,並將分析外包給全球雲端。

在GDPR和NIS2的背景下,歐洲面臨巨大的風險。董事會若監管不力,將面臨高達全球營業額2%的罰款,促使企業加大投資。資料主權原則有利於OVHcloud和德國電信等區域雲端服務商。 《數位營運彈性法案》強制要求金融業進行即時威脅偵測,從而推動了對安全資訊和事件管理(SIEM)的需求。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 安全遙測資料的快速成長

- 加強監管處罰力道和增加審核頻率

- 加速企業工作負載的雲端遷移與混合遷移

- 利用基於人工智慧/機器學習的分析提高信噪比

- 隨著安全資料管路層的出現,降低 SIEM 的整體擁有成本

- 供應商的巨額交易(思科-Splunk、Exabeam-LogRhythm)觸發刷新週期

- 市場限制

- 總擁有成本高,授權複雜

- 熟練的SOC分析師短缺

- 資料主權障礙阻礙了集中式日誌聚合

- 與 XDR/SOAR 平台重疊導致預算核准延遲

- 關鍵法規結構評估

- 價值鏈分析

- 技術展望

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 關鍵相關人員影響評估

- 主要用例和案例研究

- 宏觀經濟因素對市場的影響

- 投資分析

第5章 市場區隔

- 透過部署

- 本地部署

- 雲

- 混合

- 按下 SIEM 架構

- 傳統/傳統安全資訊和事件管理 (SIEM)

- 雲端原生/下一代安全資訊和事件管理 (SIEM)

- 開放原始碼和事件管理 (SIEM)

- 按組件

- 平台/軟體

- 專業服務

- 託管安全資訊和事件管理服務 (MSSP)

- 按組織規模

- 小型企業

- 主要企業

- 按最終用戶行業分類

- 銀行、金融服務和保險(BFSI)

- 零售與電子商務

- 政府/國防

- 醫療保健和生命科學

- 製造業

- 能源與公共產業

- 電信和資訊技術

- 其他

- 透過使用

- 威脅偵測與分析

- 合規與審核管理

- 事件回應和取證

- 日誌管理和彙報

- 雲端工作負載安全監控

- 物聯網/OT安全監控

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 北歐國家

- 其他歐洲地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 埃及

- 奈及利亞

- 其他非洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- ASEAN

- 澳洲

- 紐西蘭

- 亞太其他地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Cisco Systems, Inc.(Splunk)

- International Business Machines Corporation

- Microsoft Corporation(Azure Sentinel)

- Google LLC(Chronicle Security Operations)

- Fortinet, Inc.

- LogRhythm, Inc.

- Exabeam, Inc.

- Rapid7, Inc.

- OpenText Corporation(ArcSight)

- RSA Security LLC

- Securonix, Inc.

- CrowdStrike Holdings, Inc.

- Elastic NV

- ATandT Cybersecurity(AlienVault)

- Micro Focus International plc

- SolarWinds Corporation

- Graylog, Inc.

- Logpoint A/S

- ManageEngine(Zoho Corp.)

- Hewlett Packard Enterprise Company

第7章 市場機會與未來展望

The global SIEM market stood at USD 10.78 billion in 2025 and is forecast to climb to USD 19.13 billion by 2030, advancing at a 12.16% CAGR.

A surge in cloud workload telemetry, strict regulatory mandates, and rapid vendor consolidation are the primary growth catalysts. Large enterprises continue to expand log ingestion as attack surfaces widen, while small and medium-sized businesses enter the market through cloud-native consumption models. North American demand is buoyed by SOX and PCI DSS rules, whereas European spending accelerates in response to NIS2 and DORA. Vendor roadmaps now revolve around AI-powered analytics, unified data pipelines, and simplified licensing, themes that spur refresh cycles following Cisco's landmark acquisition of Splunk in 2024.

Global Security Information And Event Management (SIEM) Market Trends and Insights

Exponential growth of security telemetry

Enterprises generate terabytes of logs each day from endpoints, cloud services, and operational technology. The volume strains traditional ingestion models yet unlocks richer context for threat hunting. CPFL Energia monitors more than 50,000 smart-grid devices through a modern SIEM that routes high-value events to a data lake for cost control. Cloud-native elasticity permits burst processing during incident spikes, and selective retention keeps storage fees predictable. Vendors that integrate low-cost object storage with query¬able metadata gain traction as customers balance coverage and cost.

Escalating regulatory penalties and audits

Europe's NIS2 obliges operators of essential services to log, monitor, and retain events for incident reconstruction, pushing security budgets up to 9.0% of IT spending. In finance, DORA compels real-time detection and reporting. Bank Leumi lowered false positives by 70% after a SIEM upgrade tailored to audit evidence generation. Health providers face HIPAA-driven breach fines that now average USD 4.88 million, a cost that underscores the need for continuous monitoring.

High total cost of ownership

Traditional per-event licenses force buyers to cap ingestion, creating security blind spots. Hardware tariffs raised appliance costs by as much as 20% during 2024, adding budget strain. Hidden cloud fees for storage, egress, and premium analytics surprise first-time adopters. Vendors now push pipeline off-load tiers and flat-rate pricing to restore predictability.

Other drivers and restraints analyzed in the detailed report include:

- Accelerated cloud and hybrid adoption

- AI and ML-driven analytics

- Shortage of skilled SOC analysts

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

On-premise deployments held 55.75% of SIEM market share in 2024. The segment remains favored by industries bound to strict data-sovereignty policies, yet growth is subdued as hardware costs rise and skills shortages deepen. The cloud cohort advances at 13.40% CAGR, propelled by elastic scaling and pay-as-you-go fees that widen access to advanced analytics. Hybrid designs act as a bridge, placing regulated data on local nodes while streaming telemetry to low-cost object storage in the cloud.

Cloud adoption shifts upgrade cycles from multi-year appliance refreshes to continuous feature delivery. Siemens uses a hybrid pattern that runs OT parsers on premises while enriching events in the cloud for threat intelligence correlation. As licensing shifts to data usage, buyers gain transparency on the SIEM market size for each deployment choice. Vendor consolidation accelerates moves away from aging on-prem stacks toward modern SaaS offerings hosted by hyperscalers.

Legacy platforms represented 46.20% revenue share in 2024, yet they lose ground as query performance and rule tuning falter under data scale. Next-generation cloud-native engines are forecast to rise at 18.10% CAGR, the fastest among architectural types. These systems decouple storage from compute and embed machine learning at ingestion, reducing mean time to detect.

Palo Alto Networks folded QRadar SaaS into Cortex XSIAM and booked more than USD 90 million in the first post-deal quarter. Open-source stacks carve a budget niche but demand deep engineering skills. Migration utilities and compatibility layers ease the shift from traditional rule syntax to schema-on-read models. The SIEM market aligns behind architectures that treat telemetry as big data rather than event streams.

The SIEM Market Report Segments the Industry by Deployment (On-Premise, and More), SIEM Architecture ( Traditional SIEM, Next-Gen SIEM, and More), Component (Platform / Software, Professional Services, and Managed SIEM Services (MSSP)), Organization Size (Small and Medium Enterprises, and Large Enterprises), End-User Industry (Banking, Financial Services and Insurance (BFSI), Retail and E-Commerce, and More), and Geography.

Geography Analysis

North America accounted for 39.20% of the SIEM market revenue in 2024, underpinned by mature breach notification statutes and high cyber insurance premiums. Budget allocations remain robust as boards tie security controls to fiduciary risk. The region's cloud adoption and early AI experimentation reinforce its leadership. Despite a saturated base, upsell to integrated observability keeps growth in mid-single digits.

Asia-Pacific is projected to post 11.80% CAGR, the fastest globally. China's Multi-Level Protection Scheme and India's Digital Personal Data Protection Act spur mandatory logging for critical information infrastructure. Domestic cloud vendors team with global SIEM players to satisfy localisation rules. Japanese conglomerates favour hybrid SIEM that parks raw events in Tokyo regions while outsourcing analytics to global clouds, balancing sovereignty and capability.

Europe maintains a sizeable stake on the back of GDPR and the incoming NIS2. Boards face fines reaching 2% of global turnover for monitoring lapses, incentivising investment. Data sovereignty drives preference for regional clouds such as OVHcloud and Deutsche Telekom. The Digital Operational Resilience Act imposes real-time threat detection in finance, fuelling premium SIEM demand.

- Cisco Systems, Inc. (Splunk)

- International Business Machines Corporation

- Microsoft Corporation (Azure Sentinel)

- Google LLC (Chronicle Security Operations)

- Fortinet, Inc.

- LogRhythm, Inc.

- Exabeam, Inc.

- Rapid7, Inc.

- OpenText Corporation (ArcSight)

- RSA Security LLC

- Securonix, Inc.

- CrowdStrike Holdings, Inc.

- Elastic N.V.

- ATandT Cybersecurity (AlienVault)

- Micro Focus International plc

- SolarWinds Corporation

- Graylog, Inc.

- Logpoint A/S

- ManageEngine (Zoho Corp.)

- Hewlett Packard Enterprise Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Exponential growth of security telemetry volumes

- 4.2.2 Escalating regulatory penalties and audit frequency

- 4.2.3 Accelerated cloud and hybrid adoption of enterprise workloads

- 4.2.4 AI/ML-infused analytics improve signal-to-noise ratios

- 4.2.5 Emergence of security-data-pipeline layer reduces SIEM TCO

- 4.2.6 Vendor mega-deals (Cisco-Splunk, Exabeam-LogRhythm) trigger refresh cycles

- 4.3 Market Restraints

- 4.3.1 High total cost of ownership and licensing complexity

- 4.3.2 Shortage of skilled SOC analysts

- 4.3.3 Data-sovereignty barriers to central log aggregation

- 4.3.4 Overlap with XDR/SOAR platforms delays budget approval

- 4.4 Evaluation of Critical Regulatory Framework

- 4.5 Value Chain Analysis

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Impact Assessment of Key Stakeholders

- 4.9 Key Use Cases and Case Studies

- 4.10 Impact on Macroeconomic Factors of the Market

- 4.11 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 By Deployment

- 5.1.1 On-premise

- 5.1.2 Cloud

- 5.1.3 Hybrid

- 5.2 By SIEM Architecture

- 5.2.1 Legacy / Traditional SIEM

- 5.2.2 Cloud-native / Next-Gen SIEM

- 5.2.3 Open-source SIEM

- 5.3 By Component

- 5.3.1 Platform / Software

- 5.3.2 Professional Services

- 5.3.3 Managed SIEM Services (MSSP)

- 5.4 By Organization Size

- 5.4.1 Small and Medium Enterprises

- 5.4.2 Large Enterprises

- 5.5 By End-user Industry

- 5.5.1 Banking, Financial Services and Insurance (BFSI)

- 5.5.2 Retail and E-commerce

- 5.5.3 Government and Defense

- 5.5.4 Healthcare and Life Sciences

- 5.5.5 Manufacturing

- 5.5.6 Energy and Utilities

- 5.5.7 Telecom and IT

- 5.5.8 Others

- 5.6 By Application

- 5.6.1 Threat Detection and Analytics

- 5.6.2 Compliance and Audit Management

- 5.6.3 Incident Response and Forensics

- 5.6.4 Log Management and Reporting

- 5.6.5 Cloud-Workload Security Monitoring

- 5.6.6 IoT / OT Security Monitoring

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 United Kingdom

- 5.7.3.2 Germany

- 5.7.3.3 France

- 5.7.3.4 Italy

- 5.7.3.5 Spain

- 5.7.3.6 Nordics

- 5.7.3.7 Rest of Europe

- 5.7.4 Middle East and Africa

- 5.7.4.1 Middle East

- 5.7.4.1.1 Saudi Arabia

- 5.7.4.1.2 United Arab Emirates

- 5.7.4.1.3 Turkey

- 5.7.4.1.4 Rest of Middle East

- 5.7.4.2 Africa

- 5.7.4.2.1 South Africa

- 5.7.4.2.2 Egypt

- 5.7.4.2.3 Nigeria

- 5.7.4.2.4 Rest of Africa

- 5.7.5 Asia-Pacific

- 5.7.5.1 China

- 5.7.5.2 India

- 5.7.5.3 Japan

- 5.7.5.4 South Korea

- 5.7.5.5 ASEAN

- 5.7.5.6 Australia

- 5.7.5.7 New Zealand

- 5.7.5.8 Rest of Asia-Pacific

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Cisco Systems, Inc. (Splunk)

- 6.4.2 International Business Machines Corporation

- 6.4.3 Microsoft Corporation (Azure Sentinel)

- 6.4.4 Google LLC (Chronicle Security Operations)

- 6.4.5 Fortinet, Inc.

- 6.4.6 LogRhythm, Inc.

- 6.4.7 Exabeam, Inc.

- 6.4.8 Rapid7, Inc.

- 6.4.9 OpenText Corporation (ArcSight)

- 6.4.10 RSA Security LLC

- 6.4.11 Securonix, Inc.

- 6.4.12 CrowdStrike Holdings, Inc.

- 6.4.13 Elastic N.V.

- 6.4.14 ATandT Cybersecurity (AlienVault)

- 6.4.15 Micro Focus International plc

- 6.4.16 SolarWinds Corporation

- 6.4.17 Graylog, Inc.

- 6.4.18 Logpoint A/S

- 6.4.19 ManageEngine (Zoho Corp.)

- 6.4.20 Hewlett Packard Enterprise Company

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

安全資訊與事件管理市場:按交付方式、日誌類型、部署方式、組織規模和產業分類-2026年至2032年全球市場預測

安全資訊與事件管理市場:按交付方式、日誌類型、部署方式、組織規模和產業分類-2026年至2032年全球市場預測 2026年全球安全資訊與事件管理市場報告2026年全球託管安全資訊與事件管理 (SIEM) 及日誌管理市場報告

2026年全球安全資訊與事件管理市場報告2026年全球託管安全資訊與事件管理 (SIEM) 及日誌管理市場報告 全球現代 SIEM 市場,2024–2029Frost Radar ™:現代安全資訊與事件管理,2026

全球現代 SIEM 市場,2024–2029Frost Radar ™:現代安全資訊與事件管理,2026 安全資訊與事件管理市場 - 全球產業規模、佔有率、趨勢、機會、預測:按解決方案、部署方式、產業垂直領域、地區和競爭對手分類,2021-2031 年安全資訊和事件管理軟體市場-全球產業規模、佔有率、趨勢、機會和預測(按組件、應用、組織規模、部署模式、垂直產業、地區和競爭格局分類,2020-2030 年預測)

安全資訊與事件管理市場 - 全球產業規模、佔有率、趨勢、機會、預測:按解決方案、部署方式、產業垂直領域、地區和競爭對手分類,2021-2031 年安全資訊和事件管理軟體市場-全球產業規模、佔有率、趨勢、機會和預測(按組件、應用、組織規模、部署模式、垂直產業、地區和競爭格局分類,2020-2030 年預測) 安全資訊和事件管理 (SIEM) 市場規模、佔有率和趨勢分析(按解決方案、部署、企業規模、最終用途、地區和細分市場預測,2025-2033 年)

安全資訊和事件管理 (SIEM) 市場規模、佔有率和趨勢分析(按解決方案、部署、企業規模、最終用途、地區和細分市場預測,2025-2033 年) 保全資訊·活動管理(SIEM)的全球市場:各解決方案,各應用領域,不同企業規模,各終端用戶產業,各地區,機會,預測,2018年~2032年全球安全資訊和事件管理市場規模(按組件、應用、組織規模、部署模式、垂直、地理範圍分類)預測至 2025 年

保全資訊·活動管理(SIEM)的全球市場:各解決方案,各應用領域,不同企業規模,各終端用戶產業,各地區,機會,預測,2018年~2032年全球安全資訊和事件管理市場規模(按組件、應用、組織規模、部署模式、垂直、地理範圍分類)預測至 2025 年