|

市場調查報告書

商品編碼

1850967

AIOps:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)AIOps - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

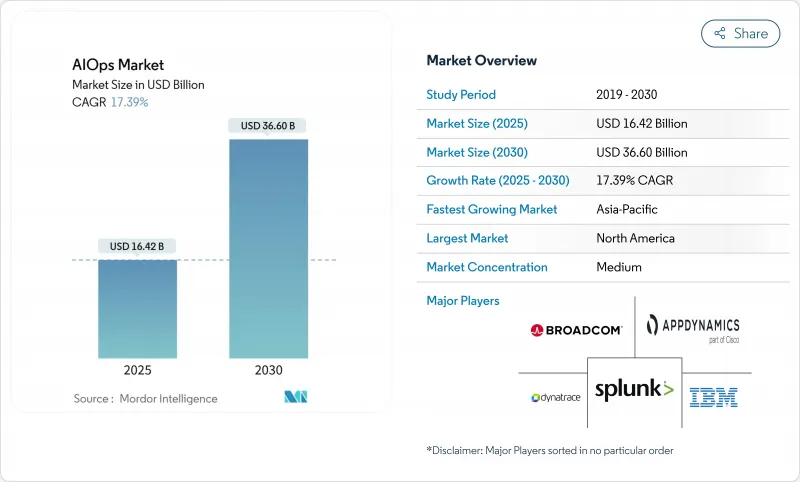

AIOps 市場預計到 2025 年將達到 164.2 億美元,到 2030 年將達到 366 億美元,複合年成長率為 17.39%。

隨著企業面臨混合雲端複雜性、可觀測資料量不斷成長以及在提高服務彈性的同時降低營運成本的壓力,市場需求日益成長。供應商正將大規模語言模型整合到傳統監控中,以減少噪音、加速根本原因發現,並實現自主事件回應,從而最佳化容量規劃。由於買家對分散的工具集感到厭倦,這些工具集不僅推高了許可成本,還拖慢了決策速度,平台整合正在加速進行。基於使用量的定價模式和 OpenTelemetry 等開放標準也降低了進入門檻,吸引中小企業參與採購流程。

全球AIOps市場趨勢與洞察

對人工智慧驅動的可觀測性的需求激增

如今,遙測資料量已達到每天Petabyte,傳統監控方式難以應付。現代AIOps平台將日誌、指標和追蹤資料關聯起來,可將警報噪音降低高達75%。金融服務等關鍵業務產業整合到單一平台後,大型主機任務的自動化率已達99%。隨著雲端原生應用產生的資料量是單體應用的10倍,手動分類變得不切實際,這種能力變得至關重要。供應商將機器學習技術應用於跨資料孤島的異常模式偵測,從而防止使用者可見的故障,並確保運作時間。

向混合/多重雲端架構遷移

約 82% 的公司正在實施混合雲策略,92% 的公司正在使用多個公共雲端,這導致可見性分散且 API 介面多樣化。 45% 的公司已經採用 AIOps 來集中監控,早期採用者報告稱,跨域關聯自動化後,事件解決速度提高了 38%。不斷成長的雲端支出帶來了經濟緊迫性,使得演算法資源最佳化成為董事會層面的優先事項。

工具激增與投資報酬率不確定性

許多公司仍使用五種或更多監控工具,導致資訊脫節,行動遲緩。在AIOps能夠兌現其承諾的價值之前,整合成本就已經不斷攀升,這令經營團隊猶豫不決。這種壓力在北美尤其突出,因為當地預算緊張,採購團隊在核准任何新平台之前,都會要求提供清晰的商業案例。

細分市場分析

平台產品將佔2024年收入的82.4%,這進一步印證了整合遙測資料收集和分析將優於獨立解決方案的觀點。剩餘的17.6%將來自服務,買家尋求配置、模型訓練和變更管理的支援。企業發現,單一主機可以減少頻繁操作帶來的疲勞,並加快決策流程。供應商目前正在整合預訓練模型,這些模型透過聯邦學習不斷演進,從而隨著時間的推移提高檢測精度。諮詢顧問則負責將舊有系統映射到現代管道,並實施最佳實踐管治。

這種以平台為中心的轉變吸取了以往工具氾濫的教訓。核心套件所採用的專有引擎能夠提供精細的異常評分,而這種評分很難透過自訂整合來實現。隨著專家們建構承包儀表板和代理附加元件,合作夥伴生態系統也不斷深化。 RapDev 基於 Datadog 的原生 AI 代理在增值層面展現了獲利潛力,而 IBM 管道正在引入 Instana 以獲取相關業務收益。

到2024年,本地部署仍將維持56.2%的市場佔有率,這主要得益於金融和政府領域嚴格的資料居住規則。然而,隨著用戶轉向基於使用量的合約模式(這種模式可以減輕基礎設施管理的負擔),雲端運算雲端領域到2030年將以18.7%的複合年成長率快速成長。雲端供應商不斷更新人工智慧模型,在無需用戶進行大規模升級的情況下提高準確率。混合配置目前在概念驗證佔據主導地位,敏感資料集保留在本地,而雲端分析引擎則大規模地執行關聯和推理。

雲端運算的發展勢頭預示著向彈性架構的更廣泛轉變。當突發事件激增時,平台可以部署突增的運算資源,並在數秒內完成多方面的根本原因分析。加密和零信任控制措施降低了傳統的安全顧慮,鼓勵即使是受監管的企業也嘗試試用託管可觀測性。成本管治功能會在資料攝取量接近預算閾值時向維運團隊發出警報,從而減少意外帳單。

AIOps市場按元件(平台和服務)、部署類型(本地部署和雲端部署)、組織規模(中小企業和大型企業)、最終用戶產業(IT和通訊、銀行、金融服務和保險等)以及地區進行細分。市場預測以美元計價。

區域分析

北美將在2024年引領AIOps市場,佔據38.2%的市佔率。早期採用者、強大的供應商生態系統以及充足的雲端預算正在推動該地區實現規模經濟。聯邦機構已記錄超過1200個AI用例,其中228個已投入運作,這表明AIOps在關鍵任務環境中已具備成熟的營運能力。併購活動依然活躍,例如ServiceNow收購Logik.ai,旨在增強即時工作流程自動化能力。

亞太地區預計將成為成長最快的地區,複合年成長率將達到19.2%。中國、印度和東南亞各國政府正在資助人工智慧加速器並津貼雲端基礎設施,推動企業實現營運現代化。亞太地區在可觀測性方面的年度投資中位數高達1,008萬美元,超過其他地區,凸顯了數位轉型的規模。電訊正在將AIOps整合到5G核心網路中,以減少網路中斷造成的損失;金融超級應用則正在部署異常檢測技術,以遏制大規模詐欺行為。

在ESG(環境、社會和治理)法規、嚴格的資料主權規則以及對開放標準的偏好等因素的推動下,歐洲市場持續保持穩定成長。該地區高度重視演算法的可解釋性,要求供應商公開模型邏輯並提供本地部署的訓練選項。各公司正將AIOps部署與綠色營運目標結合,並衡量每GB遙測資料的能耗。與NTT DATA和HPE Aruba等公司的夥伴關係,提供了可根據需求自動擴展資源的、針對永續性最佳化的觀測套件。雖然嚴格的監管可能會延緩初始採購,但獲得合規認證最終將增強供應商的信譽。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 對人工智慧主導的可觀測性的需求激增

- 向混合/多重雲端架構遷移

- 需要加快平均修復時間 (MTTR) 和 SRE 部署速度

- 用於營運的 Gen-AI 副駕駛

- 用於邊緣即時推理的FPGA/DPU

- 與ESG相關的「綠色營運」合規性

- 市場限制

- 工具激增與投資報酬率不確定性

- AIOps 人才短缺

- 資料主權/人工智慧管治障礙

- 供應商黑盒演算法與鎖定風險

- 供應鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 對宏觀經濟趨勢的市場評估

第5章 市場規模與成長預測

- 按組件

- 平台

- 服務

- 透過部署模式

- 本地部署

- 雲

- 按組織規模

- 小型企業

- 主要企業

- 按最終用戶行業分類

- 資訊科技和通訊

- BFSI

- 衛生保健

- 零售與電子商務

- 媒體與娛樂

- 製造業

- 政府和公共部門

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 歐洲

- 德國

- 英國

- 法國

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 亞太其他地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- IBM

- Cisco(AppDynamics)

- Splunk

- Dynatrace

- Broadcom(incl. VMware, CA)

- BMC

- BigPanda

- Moogsoft

- Elastic

- New Relic

- Datadog

- PagerDuty

- ServiceNow(Loom Systems)

- ExtraHop

- StackState

- OpsRamp

- Juniper(Mist AI)

- Microsoft Azure Monitor

- Amazon DevOps Guru

- Google Cloud AIOps(Operations Suite)

- SolarWinds

第7章 市場機會與未來展望

The AIOps market stood at USD 16.42 billion in 2025 and is forecast to reach USD 36.60 billion by 2030, advancing at a 17.39% CAGR.

Demand rises as enterprises struggle with complex hybrid clouds, escalating observability data, and the pressure to cut operating costs while raising service resilience. Vendors now embed large language models into traditional monitoring, enabling autonomous incident response that reduces noise, accelerates root-cause discovery, and optimizes capacity planning. Platform consolidation is gathering pace as buyers tire of fragmented tool sets that inflate license spend and slow decision-making. Consumption-based pricing and open standards such as OpenTelemetry also lower entry barriers, pulling small and medium enterprises into the purchasing cycle.

Global AIOps Market Trends and Insights

AI-Driven Observability Demand Surge

Telemetry volume now runs into petabytes per day, overwhelming traditional monitoring. Modern AIOps platforms correlate logs, metrics, and traces to cut alert noise by up to 75%, while mission-critical sectors such as financial services record 99% mainframe task automation after consolidation onto a single platform. The capability becomes pivotal as cloud-native applications generate 10 times more data than monoliths, making manual triage impractical. Vendors embed machine learning that detects anomalous patterns across data silos, preventing user-visible failures and sustaining uptime requirements.

Shift to Hybrid/Multi-Cloud Architectures

About 82% of enterprises run hybrid strategies and 92% use multiple public clouds, creating fragmented visibility and diverse API surfaces.Forty-five percent already deploy AIOps to unify monitoring, and early adopters report 38% faster incident resolution once cross-domain correlation is automated. Economic urgency mounts as cloud expenditure climbs, making algorithmic resource optimization a board-level priority.

Tool Sprawl and ROI Uncertainty

Many organizations still juggle five or more monitoring tools, fragmenting context and delaying action. Integration costs rise before AIOps delivers its promised value, creating executive hesitation. The pressure is most visible in North America, where budgets tighten and procurement teams demand clear business-case evidence before greenlighting new platforms.

Other drivers and restraints analyzed in the detailed report include:

- Need for Faster MTTR and SRE Adoption

- Gen-AI Copilots for Ops

- Shortage of AIOps-Savvy Talent

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Platform offerings captured 82.4% of 2024 revenue, reinforcing the view that unified telemetry ingestion and analytics trump point solutions. Services made up the remaining 17.6% as buyers sought configuration, model training, and change-management assistance. Enterprises confirm that a single console cuts swivel-chair fatigue and accelerates decision loops. Vendors now embed pretrained models that evolve through federated learning, raising detection accuracy over time. Services growth tracks the complexity of hybrid estates, where consultants map legacy systems into modern pipelines and enforce best-practice governance.

The platform-centric shift addresses lessons from earlier tool sprawl. Proprietary engines inside leading suites deliver granular anomaly scoring that is difficult to replicate via custom integration. Partner ecosystems deepen as specialists build turnkey dashboards and agentic add-ons. RapDev's Datadog-native AI agents illustrate the monetization potential in value-added layers, while IBM channels showcase Instana to capture adjacent service revenue.

On-premise deployments retained 56.2% share in 2024, upheld by strict data-residency rules in finance and government. The cloud segment, however, is scaling at an 18.7% CAGR to 2030 as buyers pivot to usage-based contracts that offload infrastructure management. Cloud vendors refresh AI models continuously, meaning subscribers gain incremental accuracy without forklift upgrades. Hybrid configurations now dominate proof-of-concept discussions, letting sensitive datasets stay on site while cloud analytics engines run correlation and inference at scale.

Cloud momentum signals a broader shift toward elasticity. When incidents spike, the platform can burst compute, completing multidimensional causal analysis in seconds. Encryption and zero-trust controls assuage prior security objections, encouraging even regulated entities to pilot managed observability. Cost governance features alert operations teams when ingestion volumes threaten budget thresholds, reducing surprise invoices.

Aiops Market is Segmented by Component (Platform and Services), Deployment Mode (On-Premises and Cloud), Organization Size (Small and Medium Enterprises and Large Enterprises), End-User Industry (IT and Telecom, BFSI, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led the AIOps market with 38.2% revenue in 2024. Early adopter enterprises, a robust vendor ecosystem, and sizable cloud budgets give the region scale advantages. Federal agencies log more than 1,200 AI use cases, 228 of which run in production, proving operational maturity in mission-critical settings. Mergers and acquisitions remain active, typified by ServiceNow's purchase of Logik.ai to enhance real-time workflow automation.

Asia-Pacific is the fastest-growing geography, forecasting a 19.2% CAGR. Governments in China, India, and Southeast Asian nations sponsor AI accelerators and subsidize cloud infrastructure, pushing enterprises to modernize operations. Observability investments deliver a median annual value of USD 10.08 million, exceeding other regions and highlighting the scale of digital transformation. Telecom operators integrate AIOps into 5G core networks to reduce outage penalties, while financial super-apps deploy anomaly detection to curb fraud at scale.

Europe maintains steady expansion propelled by ESG mandates, stringent data-sovereignty rules, and a preference for open standards. The region insists on algorithmic explainability, pressuring vendors to expose model logic and offer on-prem training options. Enterprises align AIOps rollouts with green-ops targets, measuring power consumption per telemetry gigabyte. Partnerships such as NTT DATA and HPE Aruba deliver sustainability-tuned observability suites that auto-scale resources in line with demand. Regulatory rigor slows initial procurement but ultimately cements vendor credibility when compliance certification is achieved.

- IBM

- Cisco (AppDynamics)

- Splunk

- Dynatrace

- Broadcom (incl. VMware, CA)

- BMC

- BigPanda

- Moogsoft

- Elastic

- New Relic

- Datadog

- PagerDuty

- ServiceNow (Loom Systems)

- ExtraHop

- StackState

- OpsRamp

- Juniper (Mist AI)

- Microsoft Azure Monitor

- Amazon DevOps Guru

- Google Cloud AIOps (Operations Suite)

- SolarWinds

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 AI-driven observability demand surge

- 4.2.2 Shift to hybrid / multi-cloud architectures

- 4.2.3 Need for faster MTTR and SRE adoption

- 4.2.4 Gen-AI copilots for ops

- 4.2.5 FPGA/DPUs enabling real-time inference at edge

- 4.2.6 ESG-linked "green ops" compliance

- 4.3 Market Restraints

- 4.3.1 Tool sprawl and ROI uncertainty

- 4.3.2 Shortage of AIOps-savvy talent

- 4.3.3 Data-sovereignty/AI-governance hurdles

- 4.3.4 Vendor black-box algorithms and lock-in risk

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Force Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Assesment of Macroeconomic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS

- 5.1 By Component

- 5.1.1 Platform

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 On-premise

- 5.2.2 Cloud

- 5.3 By Organization Size

- 5.3.1 Small and Medium Enterprises

- 5.3.2 Large Enterprises

- 5.4 By End-User Industry

- 5.4.1 IT and Telecom

- 5.4.2 BFSI

- 5.4.3 Healthcare

- 5.4.4 Retail and E-commerce

- 5.4.5 Media and Entertainment

- 5.4.6 Manufacturing

- 5.4.7 Government and Public Sector

- 5.4.8 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Info, Market Rank, Products and Services, Recent Developments)

- 6.4.1 IBM

- 6.4.2 Cisco (AppDynamics)

- 6.4.3 Splunk

- 6.4.4 Dynatrace

- 6.4.5 Broadcom (incl. VMware, CA)

- 6.4.6 BMC

- 6.4.7 BigPanda

- 6.4.8 Moogsoft

- 6.4.9 Elastic

- 6.4.10 New Relic

- 6.4.11 Datadog

- 6.4.12 PagerDuty

- 6.4.13 ServiceNow (Loom Systems)

- 6.4.14 ExtraHop

- 6.4.15 StackState

- 6.4.16 OpsRamp

- 6.4.17 Juniper (Mist AI)

- 6.4.18 Microsoft Azure Monitor

- 6.4.19 Amazon DevOps Guru

- 6.4.20 Google Cloud AIOps (Operations Suite)

- 6.4.21 SolarWinds

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

IT 營運人工智慧市場(按組件、部署類型、企業規模和最終用戶分類)—全球預測,2025 年至 2032 年

IT 營運人工智慧市場(按組件、部署類型、企業規模和最終用戶分類)—全球預測,2025 年至 2032 年 全球AIOps市場報告,2025年AIOps 平台市場(按組件、組織規模、應用程式、產業和部署)—2025 年至 2030 年全球預測

全球AIOps市場報告,2025年AIOps 平台市場(按組件、組織規模、應用程式、產業和部署)—2025 年至 2030 年全球預測 AIOps 平台市場按組件、組織規模、垂直產業和地區分類

AIOps 平台市場按組件、組織規模、垂直產業和地區分類 演算法IT營運的全球市場AIOps 市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

演算法IT營運的全球市場AIOps 市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測 全球人工智慧 IT 營運平台市場研究報告 - 產業分析、規模、佔有率、成長、趨勢及 2025 年至 2033 年預測

全球人工智慧 IT 營運平台市場研究報告 - 產業分析、規模、佔有率、成長、趨勢及 2025 年至 2033 年預測 AIOps 市場規模、佔有率及成長分析(按產品、部署模式、應用、垂直領域和地區)-2025 年至 2032 年產業預測2025年IT營運平台人工智慧全球市場報告2025年電信營運資訊科技營運人工智慧(AIOps)全球市場報告

AIOps 市場規模、佔有率及成長分析(按產品、部署模式、應用、垂直領域和地區)-2025 年至 2032 年產業預測2025年IT營運平台人工智慧全球市場報告2025年電信營運資訊科技營運人工智慧(AIOps)全球市場報告