|

市場調查報告書

商品編碼

1750598

AIOps 市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測AIOps Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

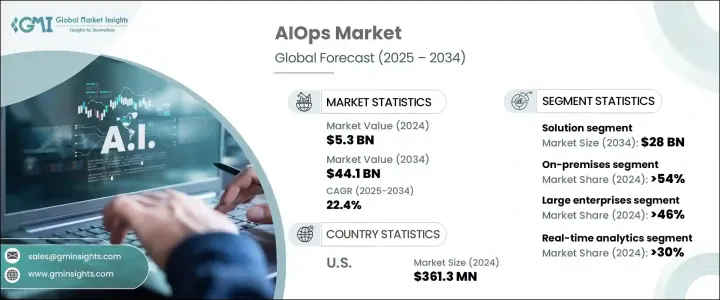

2024年,全球AIOps市場規模達53億美元,預計2034年將以22.4%的複合年成長率成長,達到441億美元。這得益於企業IT生態系統日益複雜的成長,以及對基礎設施效能管理自動化的迫切需求。企業採用人工智慧驅動的平台來減少系統停機時間、加快事件解決速度,並即時洞察營運瓶頸。隨著電信、醫療保健、零售和銀行等產業的數位轉型不斷深入,AIOps平台已成為管理可擴展且敏捷的IT框架的核心。

科技將人工智慧與機器學習和巨量資料功能相結合,以持續監控、分析和改進 IT 營運。部署混合雲和多雲環境的企業會產生大量的遙測和事件資料,而 AIOps 解決方案可以快速處理和解讀這些數據。這使組織能夠預測中斷、追蹤依賴關係並簡化跨分散式系統的效能監控。 AIOps 能夠即時關聯事件、偵測異常並找出根本原因,對於維護正常運作時間和營運連續性至關重要。隨著 IT 堆疊日益分散,對能夠提供預測性洞察和自主回應的智慧平台的需求正在迅速成長。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 53億美元 |

| 預測值 | 441億美元 |

| 複合年成長率 | 22.4% |

解決方案細分市場在2024年佔據了60%的佔有率,預計到2034年將達到280億美元。企業優先考慮可擴展的AIOps平台,以減少人工干預,並支援應用程式管理、事件解決和日誌分析的自動化。這些基於AI的工具擴大部署在混合雲、本地部署和雲端環境中,提供集中式可觀察性和營運透明度。重點在於部署敏捷平台,以適應不斷變化的基礎設施需求,同時最大限度地減少複雜性和人為錯誤。解決方案產品的主導地位源自於其相容性、可擴展性以及即時應對高階效能挑戰的能力。

2024年,本地部署模式佔據市場主導地位,佔54%的佔有率。處理敏感工作負載的企業,尤其是在國防、醫療保健和金融等領域,更傾向於採用內部部署方案來保護資料、確保合規性並與傳統系統整合。本地部署還能降低延遲,並為企業提供對IT基礎架構的全面控制。這些優勢使得本地部署成為那些承擔嚴格監管義務和關鍵任務營運的公司的首選。

美國憑藉其尖端的IT格局和對AI技術的早期應用,在2024年創造了3.613億美元的AIOps市場規模。強大的數位基礎設施,加上Datadog、Elastic、IBM、思科和Dynatrace等科技巨頭的高創新水平,共同打造了一個為高級AIOps部署做好準備的生態系統。敏捷框架、DevOps的採用以及混合IT環境的興起,推動了美國企業對智慧自動化和即時決策的需求。

AIOps 市場主要參與者採用的關鍵策略包括持續的平台創新、策略性收購和 AI 模型最佳化,以確保競爭優勢。 BigPanda、Moogsoft、Digitate、Aisera 和 Broadcom 等公司正在大力投資,擴展與雲端原生和混合系統無縫整合的產品組合。建立強大的合作夥伴生態系統、增強多領域視覺性以及將即時分析嵌入現有 IT 工作流程,有助於這些公司推動企業採用 AIOps,並鞏固其在不斷發展的 AIOps 領域中的領導地位。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 技術提供者

- OEM製造商

- 經銷商

- 最終用途

- 利潤率分析

- 供應商格局

- 川普政府關稅的影響

- 貿易影響

- 貿易量中斷

- 報復措施

- 對產業的影響

- 供應方影響(原料)

- 主要材料價格波動

- 供應鏈重組

- 生產成本影響

- 需求面影響(客戶成本)

- 價格傳導至終端市場

- 市佔率動態

- 消費者反應模式

- 供應方影響(原料)

- 受影響的主要公司

- 策略產業反應

- 供應鏈重組

- 定價和產品策略

- 政策參與

- 展望與未來考慮

- 貿易影響

- 技術與創新格局

- 專利分析

- 重要新聞和舉措

- 監管格局

- 用例

- 衝擊力

- 成長動力

- 雲端基礎設施的激增

- IT營運對基於人工智慧的服務的需求不斷成長

- 現代 IT 基礎架構產生的資料量不斷增加

- 各國政府推動人工智慧應用的舉措

- 產業陷阱與挑戰

- 資料安全和隱私問題

- IT 營運中的變化日益增多

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第5章:市場估計與預測:按組件,2021 - 2034 年

- 主要趨勢

- 解決方案

- 服務

第6章:市場估計與預測:依部署模型,2021 - 2034 年

- 主要趨勢

- 本地

- 雲

第7章:市場估計與預測:依企業規模,2021 - 2034 年

- 主要趨勢

- 大型企業

- 中小企業

第8章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 基礎設施管理

- 即時分析

- 網路和安全管理

- 應用程式效能管理

- 其他

第9章:市場估計與預測:依最終用途,2021 - 2034 年

- 主要趨勢

- 金融服務業

- IT和電信

- 衛生保健

- 零售

- 政府

- 製造業

- 媒體與娛樂

- 其他

第10章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐人

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 東南亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 阿拉伯聯合大公國

- 南非

- 沙烏地阿拉伯

第 11 章:公司簡介

- Aisera

- Amelia (IPsoft)

- Bigpanda

- BMC Software

- Broadcom CA

- Cisco

- Datadog

- Devo

- Digital.ai

- Digitate

- Dynatrace

- Elastic

- Espressive

- Extrahop

- harness

- IBM

- Interlink Software

- kentik

- Logz.io

- Moogsoft

The Global AIOps Market was valued at USD 5.3 billion in 2024 and is estimated to grow at a CAGR of 22.4% to reach USD 44.1 billion by 2034, fueled by the rising complexity of enterprise IT ecosystems and the urgent demand for automation in managing infrastructure performance. Businesses adopt AI-driven platforms to reduce system downtime, accelerate incident resolution, and gain real-time visibility into operational bottlenecks. As digital transformation intensifies across sectors like telecommunications, healthcare, retail, and banking, AIOps platforms become central to managing scalable and agile IT frameworks.

Technology integrates artificial intelligence with machine learning and big data capabilities to continuously monitor, analyze, and improve IT operations. Enterprises deploying hybrid and multi-cloud environments generate vast telemetry and event data, which AIOps solutions can process and interpret quickly. This empowers organizations to forecast disruptions, trace dependencies, and streamline performance monitoring across distributed systems. The ability to correlate events, detect anomalies, and pinpoint root causes in real time has made AIOps indispensable for maintaining uptime and operational continuity. As IT stacks become more decentralized, the need for intelligent platforms that enable predictive insights and autonomous responses is rapidly accelerating.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.3 Billion |

| Forecast Value | $44.1 Billion |

| CAGR | 22.4% |

The solutions segment held a 60% share in 2024 and is projected to reach USD 28 billion by 2034. Businesses prioritize scalable AIOps platforms that reduce manual intervention and support automation across application management, incident resolution, and log analysis. These AI-powered tools are increasingly deployed across hybrid, on-premises, and cloud-based environments, offering centralized observability and operational transparency. The emphasis is on deploying agile platforms that adapt to evolving infrastructure demands while minimizing complexity and human error. The dominance of solution offerings is driven by their compatibility, scalability, and ability to address high-level performance challenges in real time.

The on-premises deployment model led the market with a 54% share in 2024. Enterprises dealing with sensitive workloads, particularly in sectors like defense, healthcare, and finance, prefer in-house setups for data protection, compliance adherence, and integration with legacy systems. On-premises installations also allow lower latency and provide organizations with total control over IT infrastructure. These advantages continue to make local deployments a preferred choice for companies with strict regulatory obligations and mission-critical operations.

U.S. AIOps Market generated USD 361.3 million in 2024, due to its cutting-edge IT landscape and early adoption of AI technologies. Robust digital infrastructure, combined with high innovation levels from tech giants like Datadog, Elastic, IBM, Cisco, and Dynatrace, has created an ecosystem primed for advanced AIOps deployment. The rise of agile frameworks, DevOps adoption, and hybrid IT environments fuels demand for intelligent automation and real-time decision-making across U.S. enterprises.

Key strategies adopted by major players in the AIOps Market include constant platform innovation, strategic acquisitions, and AI model refinement to ensure a competitive edge. Companies like BigPanda, Moogsoft, Digitate, Aisera, and Broadcom are investing heavily in expanding product portfolios that integrate seamlessly with cloud-native and hybrid systems. Building strong partner ecosystems, enhancing multi-domain visibility, and embedding real-time analytics into existing IT workflows help these companies drive enterprise adoption and solidify their leadership in the evolving AIOps landscape.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Technology providers

- 3.1.1.2 OEM Manufacturers

- 3.1.1.3 Distributors

- 3.1.1.4 End use

- 3.1.2 Profit margin analysis

- 3.1.1 Supplier landscape

- 3.2 Impact of Trump administration tariffs

- 3.2.1 Trade impact

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (Cost to customers)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook & future considerations

- 3.2.1 Trade impact

- 3.3 Technology & innovation landscape

- 3.4 Patent analysis

- 3.5 Key news & initiatives

- 3.6 Regulatory landscape

- 3.7 Use cases

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Proliferation of cloud infrastructure

- 3.8.1.2 Growing demand for AI-based services in IT operations

- 3.8.1.3 Increasing volume of data generated by modern IT infrastructures

- 3.8.1.4 Government initiatives for AI adoption in various countries

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 Data security and privacy concerns

- 3.8.2.2 Increasing number of changes in IT operations

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Solution

- 5.3 Service

Chapter 6 Market Estimates & Forecast, By Deployment Model, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 On-premises

- 6.3 Cloud

Chapter 7 Market Estimates & Forecast, By Enterprise Size, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Large enterprises

- 7.3 SME

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Infrastructure management

- 8.3 Real-time analytics

- 8.4 Network & security management

- 8.5 Application performance management

- 8.6 Others

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 BFSI

- 9.3 IT & telecom

- 9.4 Healthcare

- 9.5 Retail

- 9.6 Government

- 9.7 Manufacturing

- 9.8 Media & entertainment

- 9.9 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Aisera

- 11.2 Amelia (IPsoft)

- 11.3 Bigpanda

- 11.4 BMC Software

- 11.5 Broadcom CA

- 11.6 Cisco

- 11.7 Datadog

- 11.8 Devo

- 11.9 Digital.ai

- 11.10 Digitate

- 11.11 Dynatrace

- 11.12 Elastic

- 11.13 Espressive

- 11.14 Extrahop

- 11.15 harness

- 11.16 IBM

- 11.17 Interlink Software

- 11.18 kentik

- 11.19 Logz.io

- 11.20 Moogsoft

面向 IT 維運的人工智慧市場:按組件、部署類型、企業規模和最終用戶分類——2026 年至 2032 年全球市場預測

面向 IT 維運的人工智慧市場:按組件、部署類型、企業規模和最終用戶分類——2026 年至 2032 年全球市場預測 AIOps平台市場預測至2034年-按交付類型、部署類型、組織規模、應用、最終用戶和地區分類的全球分析

AIOps平台市場預測至2034年-按交付類型、部署類型、組織規模、應用、最終用戶和地區分類的全球分析 2026年全球演算法IT運維(AIOps)市場報告AIOps平台市場:按組件、組織規模、應用、產業和部署類型分類 - 2026-2032年全球預測2026年AIOps全球市場報告2026年全球人工智慧在IT運維平台市場報告2026年通訊業資訊科技營運人工智慧(AIOps)全球市場報告

2026年全球演算法IT運維(AIOps)市場報告AIOps平台市場:按組件、組織規模、應用、產業和部署類型分類 - 2026-2032年全球預測2026年AIOps全球市場報告2026年全球人工智慧在IT運維平台市場報告2026年通訊業資訊科技營運人工智慧(AIOps)全球市場報告 AIOps平台市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、功能和解決方案分類

AIOps平台市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、功能和解決方案分類 全球人工智慧市場規模、佔有率、趨勢和成長分析報告(面向 IT 維運平台),2026-2034 年AIOps市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034年預測

全球人工智慧市場規模、佔有率、趨勢和成長分析報告(面向 IT 維運平台),2026-2034 年AIOps市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034年預測