|

市場調查報告書

商品編碼

1850402

智慧電視:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)Smart TV - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

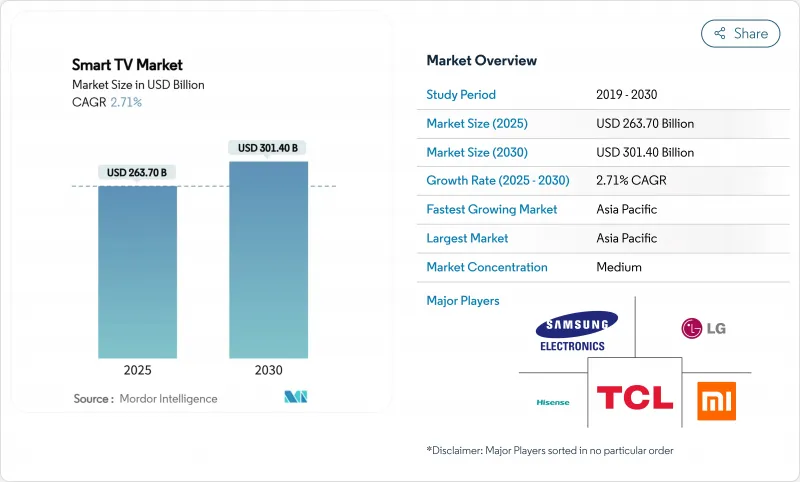

預計到 2025 年,智慧電視市場規模將達到 2,637 億美元,到 2030 年將達到 3,014 億美元,年複合成長率為 2.71%。

如今,推動成長的並非首次購機用戶數量的激增,而是人工智慧影像處理、整合雲端遊戲功能以及價值鏈本地化等漸進式改進,這些改進在降低成本的同時還能保持淨利率。印度擴大生產連結獎勵,越南和墨西哥也推出類似的製造業信貸政策,這些措施正在扶持產地附近的組裝中心,從而縮短前置作業時間並降低平均售價。顯示器製造商正加大研發投入,改進mini-LED背光和量子點技術,以應對OLED的供應限制;通訊業者則將電視與光纖套餐捆綁銷售,以擴大目標用戶群。平台競爭的焦點正轉向廣告支援的內容服務和延長軟體支援的承諾,這即使在成熟市場也促使用戶進行高級更換。

全球智慧電視市場趨勢與洞察

55-65吋4K電視價格的下降將推動印度和巴西的大規模普及。

中國OEM廠商已將55吋4K電視的零售價(曾經的高階閾值)在2024年降至400美元以下。諸如TCL 98吋機型從5999美元降至1999美元等積極的促銷,迫使競爭對手擴大入門級產品線,並透過在地採購來確保利潤。三星印度分公司報告稱,其2024年的電視銷售額將達到1000億盧比,凸顯了品牌主導的AI功能將如何幫助其即使在通縮環境下也能保持價格分佈。

電信主導的光纖部署推動東南亞首家擁有者

印尼、泰國和馬來西亞的全國性光纖網路計畫正在降低寬頻訂閱成本,並實現流暢的4K串流媒體播放。營運商目前將入門級43吋電視捆綁到100Mbps的寬頻套餐中,打造繞過傳統零售通路的一體化提案。隨著觀看方式從行動裝置轉向客廳螢幕,潛在需求將從城市中心轉移到二線城市,預計到2030年,二線城市智慧電視市場將繼續領先全球市場。

用於迷你LED背光燈的半導體供應緊張,限制了高階產品的供應。

Mini-LED電視需要數千個驅動晶片和高密度封裝的二極體,但這些元件的晶圓產能遠遠無法滿足預計在2024年出現的激增需求。 TrendForce預測,2024年Mini-LED電視的出貨量將成長59%,達到640萬台,這將使現有元件供應捉襟見肘。前置作業時間超過30週,導致各大品牌優先生產旗艦產品,延後推出中階機型。供應緩解的關鍵在於一座計畫於2026年下半年投產的12吋晶圓廠。

細分市場分析

預計到2024年,高畫質/全高清電視仍將以37.8%的市佔率領跑,主要得益於新興經濟體消費者對成本的關注。相比之下,8K超高清電視預計將以4.2%的速度成長,並在2030年之前超越整體智慧電視市場的成長速度。三星的Vision AI引擎將於2025年推出,它將把低解析度視訊串流提升至接近原生8K的畫質,從而緩解超高碼率內容短缺的問題。歐盟生態設計法規對峰值亮度的限制將促使廠商採用更有效率的背光設計,從而在高亮度合規性方面轉向mini-LED而非OLED。

入門級4K電視也開始配備可變刷新率遊戲模式等高階功能,模糊了中階市場的界限,並擴大了智慧電視市場的整體規模。內容平台也將其內容庫升級到HDR10+和杜比視界,從而推動了對能夠精確渲染動態元資料的高像素密度面板的需求。

到2024年,主流46-55吋智慧電視將佔智慧電視市場32.1%的佔有率。由於印度和墨西哥本地組裝的減少,該類別電視的平均售價將比去年同期下降9%。 65吋以上尺寸的電視將以3.8%的複合年成長率成長,並帶動高階技術(包括120Hz面板和物件追蹤音效)的普及。

透過共用玻璃基板,製造商正將98吋液晶電視的價格降至2,000美元以下,讓壁掛式電視也能惠及中等收入家庭。疫情期間家庭劇院的升級改造改變了客廳的佈局,而這種空間變化更有利於大螢幕電視的使用。雖然小螢幕電視(32吋以下)在其他房間仍有市場,但收入結構正在向上轉移,即使智慧電視市場整體成長放緩,大螢幕電視也能為利潤池提供支撐。

區域分析

亞太地區預計到2024年將佔全球營收的41.2%,以3.2%的複合年成長率引領成長。新德里的獎勵機制在十年內推動本地生產成長了九倍,由此形成的規模經濟將輻射至東協出口走廊。光纖網路的部署和在地化的OTT內容將協助印尼、越南和菲律賓等國的首次購機者進入智慧電視市場,從而擴大農村地區的普及率。

北美市場日趨成熟,人工智慧驅動的影像增強技術和FAST通道整合推動了電視的更換需求。廣告商資助的服務補貼了高階電視,而雲端遊戲延遲的改善將進一步提升更新率規格。歐洲正努力應對嚴格的節能法規EC 2024/1781,該法規限制了大型8K電視的亮度。遵守該法規將迫使電視峰值亮度降低,從而推動mini-LED技術的應用,並促進微透鏡陣列的研究與開發。

中東和非洲的普及率僅為個位數,但基礎設施投資的增加和可支配收入的成長領先提供了空間。區域廣播公司推出高速阿拉伯語頻道,消除了內容障礙。拉丁美洲的需求呈現兩極化:高階電視機受到富裕的都市區消費者的青睞,而低價串流媒體適配器則延緩了價格敏感型家庭的電視機升級。整體而言,外匯波動迫使製造商採取靈活的採購和避險策略,以保持市場競爭力。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 55-65吋4K電視價格的下降正在推動印度和巴西的普及。

- 電信業者主導的光纖部署推動東南亞首批光纖所有權公司成立

- 快速通路整合推動北美升級需求

- 在印度,政府的生產關聯激勵措施和在地化獎勵正在拉低平均售價。

- 雲端遊戲夥伴關係(Xbox、GeForce Now)推動了120Hz高階電視的銷售

- Matter認證的互通性加快了歐盟的更換週期。

- 市場限制

- 微型LED背光半導體供應緊張限制了高階產品的供應。

- 作業系統生態系統碎片化推高了應用程式開發成本。

- 歐盟第二項能源法規限制了8K電視的亮度和普及率。

- 價格親民的串流媒體加密狗延長了價格敏感型市場中的產品更換週期。

- 產業價值鏈分析

- 監理與技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 通過決議

- 高清/全高清

- 4K UHD

- 8K UHD

- 按螢幕尺寸(英吋)

- 小於 32 英寸

- 33 至 45 英寸

- 46 至 55 英寸

- 56 至 65 英寸

- 65吋或以上

- 按下面板/顯示技術

- LED/LCD

- 有機發光二極體

- QLED

- 迷你LED

- 微型LED

- 按螢幕形狀

- 平坦的

- 曲線

- 按作業系統

- Android TV

- 其他/OEM特定規格

- 透過分銷管道

- 線下零售(大賣場、品牌專賣店)

- 線上(電子商務、D2C)

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 北歐國家

- 其他歐洲地區

- 南美洲

- 巴西

- 其他南美洲

- 亞太地區

- 中國

- 日本

- 印度

- 東南亞

- 亞太其他地區

- 中東和非洲

- 中東

- GCC

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Samsung Electronics Co., Ltd.

- LG Electronics Inc.

- TCL Technology Group Corp.

- Hisense Group Co., Ltd.

- Xiaomi Corporation

- Sony Group Corporation

- Vizio Holding Corp.

- Panasonic Holdings Corporation

- Sharp Corporation

- TPV Technology Limited(Philips)

- Skyworth Group Ltd.

- Konka Group Co., Ltd.

- Haier Smart Home Co., Ltd.

- Changhong Electric Co., Ltd.

- Toshiba Corporation

- OnePlus Technology(Shenzhen)Co., Ltd.

- VU Technologies Pvt. Ltd.

第7章 市場機會與未來展望

The smart TV market size stands at USD 263.7 billion in 2025 and is projected to reach USD 301.4 billion by 2030, expanding at a 2.71% CAGR.

Momentum now comes less from first-time ownership surges and more from incremental improvements such as AI-driven picture processing, integrated cloud-gaming features and value-chain localization that compresses costs while preserving margins. India's expanded production-linked incentives and similar manufacturing credits in Vietnam and Mexico are fostering near-source assembly hubs that shorten lead times and lower average selling prices Ministry of Commerce & Industry. Display makers are steering R&D toward Mini-LED backlighting and quantum-dot enhancements that counter OLED's supply constraints, while telecom operators bundle televisions with fiber plans to widen addressable households. Platform competition is shifting toward ad-supported content services and extended software-support promises, encouraging premium replacements even in mature regions.

Global Smart TV Market Trends and Insights

Price Erosion of 55-65" 4 K Sets Accelerating Mass Adoption in India and Brazil

Chinese OEMs pushed 55-inch 4 K retail pricing below USD 400 in 2024, a threshold that once signaled the premium tier. Aggressive promotions, such as TCL's drop on 98-inch models from USD 5,999 to USD 1,999, compelled rivals to broaden entry-level line-ups while preserving margins through localized sourcing . Samsung's Indian unit still reported INR 10,000 crore television revenue in 2024, underscoring that brand-led AI features can hold price points even amid deflation Lower barriers entice middle-income households into larger-screen categories and compress replacement cycles across value-sensitive markets.

Telecom-Led Fiber Roll-outs Catalyzing First-Time Ownership in Southeast Asia

Nationwide fiber plans in Indonesia, Thailand and Malaysia are shrinking broadband subscription costs and enabling seamless 4 K streaming. Operators now bundle entry-level 43-inch televisions with 100 Mbps contracts, creating integrated service propositions that sidestep traditional retail channels. As viewing shifts from mobile devices to living-room screens, addressable demand moves beyond urban cores into tier-2 cities, sustaining outperformance against the global smart TV market through 2030.

Semiconductor Tightness for Mini-LED Backlights Limiting Premium Supply

Mini-LED sets need thousands of driver ICs and densely packed diodes; wafer-fab capacity for these parts lagged surging demand in 2024. TrendForce estimates Mini-LED television shipments grew 59% to 6.4 million units in 2024, overwhelming available component supply. Lead times stretched beyond 30 weeks, prompting brands to prioritise flagship lines and delay mid-tier adopters. Supply relief hinges on new 12-inch fabs slated to ramp only in late 2026.

Other drivers and restraints analyzed in the detailed report include:

- Government PLI and Localization Incentives Lowering ASPs in India

- Integration of FAST Channels Spurring Upgrade Demand in North America

- Low-Cost Streaming Dongles Extending Replacement Cycles in Price-Sensitive Markets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

HD/Full HD still led revenue with 37.8% in 2024, sustained by cost-sensitive buyers in developing economies. Conversely, 8 K UHD is projected to compound at 4.2% and outsprint overall smart TV market growth through 2030. Samsung's Vision AI engine, rolled out in 2025, enhances lower-resolution streams to near-native 8 K quality and mitigates the shortage of ultra-high-bitrate content . EU ecodesign rules that limit peak brightness add pressure to engineer more efficient backlights, nudging brands toward Mini-LED over OLED for high-nit compliance.

Entry-level 4 K sets inherit premium features such as variable-refresh-rate gaming modes, blurring the mid-tier and expanding the total smart TV market. Content platforms also upscale catalogues to HDR10+ and Dolby Vision, reinforcing demand for higher-pixel-density panels that can render dynamic metadata accurately.

Mainstream 46-55-inch models captured 32.1% of the smart TV market in 2024. Average selling prices in this category fell 9% year on year after local assembly scaled in India and Mexico. Sets above 65 inches are forecast for a 3.8% CAGR and pull most premium technology attach-rates, including 120 Hz panels and object-tracking sound.

Manufacturers leverage shared glass-substrate fabs to push 98-inch LCDs below USD 2,000, making wall-sized viewing accessible to middle-income households. Pandemic-era home-theatre upgrades reconfigured living-room layouts, and those spatial changes now lock in preference for larger screens. Smaller than 32 inch remains viable for secondary rooms, yet the revenue mix shifts upward, underpinning profit pools despite moderate headline growth for the smart TV market.

The Smart TV Market Report is Segmented by Resolution (HD/Full HD, 4K UHD, and 8K UHD), Screen Size (Up To 32 Inch, 33-45 Inch, 46-55 Inch, and More), Panel/Display Technology (LED/LCD, OLED, QLED, Mini-LED, and More), Screen Shape (Flat, and Curved), Operating System (Android TV, and Other/OEM Proprietary), Distribution Channel (Offline Retail, and Online), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific generated 41.2% of 2024 revenue and leads growth at 3.2% CAGR as domestic panel fabs in China and assembly hubs in India lower regional landed costs. New Delhi's incentive ecosystem boosted local output nine-fold over a decade, creating scale that reverberates across ASEAN exporting corridors. Fiber roll-outs and OTT content localisation bring first-time buyers in Indonesia, Vietnam and the Philippines into the smart TV market, expanding rural penetration.

North America is mature; replacement demand hinges on AI-powered upscaling and FAST-channel integration. Advertiser-funded services subsidise premium sets, and cloud-gaming latency improvements elevate refresh-rate specifications. Europe wrestles with stringent energy-efficiency law EC 2024/1781 that caps brightness for large 8 K models. Compliance forces thinner peak-luminance levels, prompting Mini-LED adoption and spurring R&D into micro-lens arrays.

Middle East and Africa trail with low single-digit penetration, yet infrastructure investments and rising disposable incomes signal headroom. Regional broadcasters rolling out Arabic-language FAST channels remove content barriers. Latin America shows bifurcated demand: premium sets sell into affluent urban districts, while low-cost streaming dongles slow panel upgrades in price-sensitive households. Throughout, currency volatility steers manufacturers toward flexible sourcing and hedging strategies to keep the smart TV market competitive.

- Samsung Electronics Co., Ltd.

- LG Electronics Inc.

- TCL Technology Group Corp.

- Hisense Group Co., Ltd.

- Xiaomi Corporation

- Sony Group Corporation

- Vizio Holding Corp.

- Panasonic Holdings Corporation

- Sharp Corporation

- TPV Technology Limited (Philips)

- Skyworth Group Ltd.

- Konka Group Co., Ltd.

- Haier Smart Home Co., Ltd.

- Changhong Electric Co., Ltd.

- Toshiba Corporation

- OnePlus Technology (Shenzhen) Co., Ltd.

- VU Technologies Pvt. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Price Erosion of 55-65" 4K Sets Accelerating Mass Adoption in India and Brazil

- 4.2.2 Telecom-Led Fiber Roll-outs Catalyzing First-Time Ownership in Southeast Asia

- 4.2.3 Integration of FAST Channels Spurring Upgrade Demand in North America

- 4.2.4 Government PLI and Localization Incentives Lowering ASPs in India

- 4.2.5 Cloud-Gaming Partnerships (Xbox, GeForce Now) Driving 120 Hz Premium TV Sales

- 4.2.6 Matter-Certified Interoperability Boosting Replacement Cycles in EU

- 4.3 Market Restraints

- 4.3.1 Semiconductor Tightness for MiniLED Backlights Limiting Premium Supply

- 4.3.2 Fragmented OS Ecosystem Raising App Development Costs

- 4.3.3 EU Tier-2 Energy Rules Curbing 8K TV Brightness and Adoption Rates

- 4.3.4 Low-Cost Streaming Dongles Extending Replacement Cycles in Price-Sensitive Markets

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Resolution

- 5.1.1 HD/Full HD

- 5.1.2 4K UHD

- 5.1.3 8K UHD

- 5.2 By Screen Size (Inches)

- 5.2.1 Upto 32

- 5.2.2 33-45

- 5.2.3 46-55

- 5.2.4 56-65

- 5.2.5 Above 65

- 5.3 By Panel/Display Technology

- 5.3.1 LED/LCD

- 5.3.2 OLED

- 5.3.3 QLED

- 5.3.4 Mini-LED

- 5.3.5 Micro-LED

- 5.4 By Screen Shape

- 5.4.1 Flat

- 5.4.2 Curved

- 5.5 By Operating System

- 5.5.1 Android TV

- 5.5.2 Other/OEM Proprietary

- 5.6 By Distribution Channel

- 5.6.1 Offline Retail (Hypermarket, Brand Stores)

- 5.6.2 Online (E-commerce, D2C)

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 Germany

- 5.7.2.2 United Kingdom

- 5.7.2.3 France

- 5.7.2.4 Nordics

- 5.7.2.5 Rest of Europe

- 5.7.3 South America

- 5.7.3.1 Brazil

- 5.7.3.2 Rest of South America

- 5.7.4 Asia-Pacific

- 5.7.4.1 China

- 5.7.4.2 Japan

- 5.7.4.3 India

- 5.7.4.4 South-East Asia

- 5.7.4.5 Rest of Asia-Pacific

- 5.7.5 Middle East and Africa

- 5.7.5.1 Middle East

- 5.7.5.1.1 Gulf Cooperation Council Countries

- 5.7.5.1.2 Turkey

- 5.7.5.1.3 Rest of Middle East

- 5.7.5.2 Africa

- 5.7.5.2.1 South Africa

- 5.7.5.2.2 Rest of Africa

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Samsung Electronics Co., Ltd.

- 6.4.2 LG Electronics Inc.

- 6.4.3 TCL Technology Group Corp.

- 6.4.4 Hisense Group Co., Ltd.

- 6.4.5 Xiaomi Corporation

- 6.4.6 Sony Group Corporation

- 6.4.7 Vizio Holding Corp.

- 6.4.8 Panasonic Holdings Corporation

- 6.4.9 Sharp Corporation

- 6.4.10 TPV Technology Limited (Philips)

- 6.4.11 Skyworth Group Ltd.

- 6.4.12 Konka Group Co., Ltd.

- 6.4.13 Haier Smart Home Co., Ltd.

- 6.4.14 Changhong Electric Co., Ltd.

- 6.4.15 Toshiba Corporation

- 6.4.16 OnePlus Technology (Shenzhen) Co., Ltd.

- 6.4.17 VU Technologies Pvt. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

智慧電視市場:2026-2032年全球市場預測(按顯示技術、螢幕大小、解析度、銷售管道和應用分類)

智慧電視市場:2026-2032年全球市場預測(按顯示技術、螢幕大小、解析度、銷售管道和應用分類) 智慧電視市場:按螢幕大小、顯示技術、作業系統和地區分類網路電視市場:2026年至2032年全球預測(依顯示技術、解析度、螢幕大小、作業系統和應用程式分類)

智慧電視市場:按螢幕大小、顯示技術、作業系統和地區分類網路電視市場:2026年至2032年全球預測(依顯示技術、解析度、螢幕大小、作業系統和應用程式分類) 2026年全球體育賽事線上影片市場報告智慧電視晶片市場:按類型、解析度、最終用戶和地區分類

2026年全球體育賽事線上影片市場報告智慧電視晶片市場:按類型、解析度、最終用戶和地區分類 智慧電視市場分析及預測(至2035年):依類型、產品類型、技術、組件、應用、功能、安裝類型、最終用戶及模式分類

智慧電視市場分析及預測(至2035年):依類型、產品類型、技術、組件、應用、功能、安裝類型、最終用戶及模式分類 美國智慧電視:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

美國智慧電視:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 全球智慧電視市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球智慧電視市場規模、佔有率、趨勢和成長分析報告(2026-2034) 智慧型電視晶片市場:按類型、解析度、最終用戶、國家和地區分類-全球產業分析、市場規模、市場佔有率及2025年至2032年預測

智慧型電視晶片市場:按類型、解析度、最終用戶、國家和地區分類-全球產業分析、市場規模、市場佔有率及2025年至2032年預測 智慧電視市場規模、佔有率、趨勢和預測(按解析度類型、螢幕大小、螢幕類型、技術、平台、分銷管道、應用和地區分類),2026-2034年

智慧電視市場規模、佔有率、趨勢和預測(按解析度類型、螢幕大小、螢幕類型、技術、平台、分銷管道、應用和地區分類),2026-2034年