|

市場調查報告書

商品編碼

1850351

新加坡海運:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)Singapore Sea Freight Transport - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

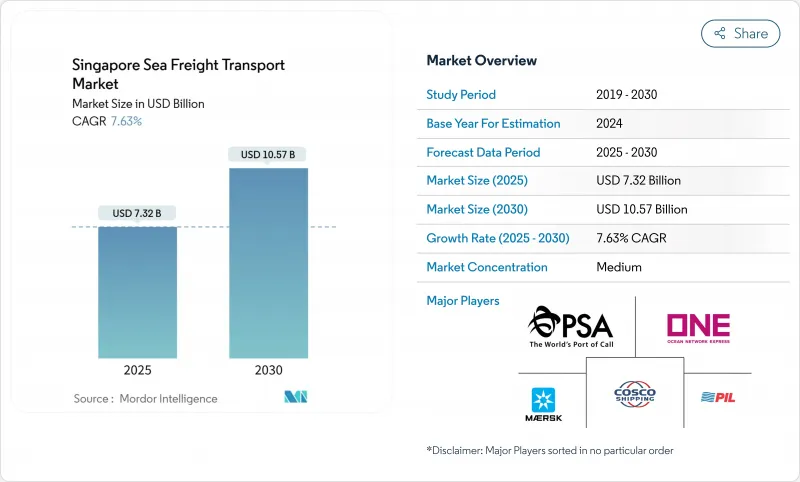

新加坡海運市場規模預計在 2025 年達到 73.2 億美元,預計到 2030 年將達到 105.7 億美元,預測期(2025-2030 年)複合年成長率為 7.63%。

這一成長動能主要得益於所有貨櫃業務逐步轉移至大士港,此舉釋放了泊位容量,並縮短了船舶週轉時間。以電子載貨證券和統一港口社區系統為代表的數位化工具正在減少紙本工作,並為承運商將新加坡置於其航線網路核心提供了新的理由。優惠貿易協定正在擴大出口腹地,加之製造業向東南亞轉移,共同推動了出口貨櫃數量(TEU)的成長。與清潔能源相關的液體散貨運輸量的成長以及溫控藥品運輸方式向海運的轉變,正在進一步推動成長。燃油成本上漲以及與馬來西亞鄰國的價格競爭仍然是主要觀點,但新增船舶運力和貿易航線多元化相結合,確保了成長前景穩步推進。

新加坡海運市場趨勢與洞察

大士港的整合提高了吞吐量

大士港計劃將萊格西城碼頭整合為大士超級港,預計到2040年代吞吐能力將達到6500萬標準箱,幾乎是2021年3750萬標準箱吞吐能力的兩倍。第一期工程計畫於2022年投入使用,目前已配備200多輛自動導引車和一個事件驅動型數位骨幹網,可即時指揮堆場作業。由於該設施位於一條連續的海岸線上,內部轉運次數顯著減少,從而提高了起重機的運轉率和船舶週轉速度。由此帶來的更高可預測性使航運公司能夠合理安排同一航線的兩次靠泊,並將運力保留給額外的航次。透過縮短港口停留時間,航運公司既能節省成本,也能減少溫室氣體排放,進一步鞏固了新加坡作為樞紐港的地位。

東協製造業轉型推動出口貨櫃數量成長

電子產品、精密工程和耐用消費品生產從北亞向東協轉移,正推動新加坡成為出口大戶。聯華電子投資50億美元的半導體晶圓廠以及其他類似投資項目,將吸引晶圓設備、化學品和成品晶片透過出口轉運服務運往深水港。越南的工業擴張也遵循類似的模式,利用新加坡作為貨運中心門戶,並透過YCH集團和越南郵政正在建造的數位貿易走廊進行運輸。供應商佈局的擴大分散了地緣政治風險,提高了網路密度,並確保即使在全球經濟疲軟時期,東協內部的需求也能支撐泊位利用率。

燃油價格波動導致運費上漲

到2024年下半年,部分遠距航線的貨櫃即期運價加倍以上。在新加坡,2023年生質燃料燃料庫量增加了兩倍,為航運公司的燃料成本基礎增加了一個新的價格點。替代燃料有助於實現脫碳目標,但其尚不成熟的供應鏈導致與指數掛鉤的燃料額外費用波動。因此,托運人優先選擇港內延誤較少的港口,以確保燃料消費量的可預測性。新加坡的效率提升將緩解但無法消除這種波動。

細分市場分析

預計到2024年,貨櫃貨物將佔新加坡海運市場佔有率的61%,隨著冷藏貨櫃的普及,其主導地位預計將持續到2030年。疫苗和生技藥品對溫控箱的需求日益成長,促使PSA公司增設插電點和空氣控制監控系統,使貨櫃運輸成為生命科學出口商的策略推動力。液體散貨將以8.1%的複合年成長率實現最快成長,這主要得益於生質燃料摻混和新興綠色氨計劃在裕廊島的專用泊位需求。乾散貨量將受到區域建築需求的推動而實現溫和成長,而普通貨物和滾裝貨物將保持穩定的市場佔有率。自動化、數位雙胞胎和區塊鏈技術在這些領域的應用將提高可預測性,使碼頭營運商能夠針對每種商品類別最佳化堆場作業。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 透過將城市碼頭整合到大士大型港口來提高吞吐量

- 東協製造業轉移推動新加坡出口貨櫃數量增加

- 透過優惠貿易協定(RCEP、CPTPP)降低海運成本

- 透過引入DigitalPORT@SG和電子載貨證券,縮短了貨物停留時間。

- 擴大藥品和生鮮食品低溫運輸貨櫃運輸量

- 綠色與數位化航運走廊舉措

- 市場限制

- 燃油價格波動會導致綜合運費上漲。

- 來自巴生港和丹戎帕拉帕斯港支線關稅的競爭壓力

- 旺季期間40英尺高箱冷藏車短缺

- 裕廊島的「最後一公里」/「首公里」貨車運輸能力緊張。

- 價值/供應鏈分析

- 監理與技術展望

- 波特五力模型

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 按貨物類型

- 貨櫃貨物

- 乾燥

- 冷藏

- 乾散貨

- 液體散貨

- 普通貨物

- 滾裝/滾卸貨物

- 貨櫃貨物

- 按最終用戶行業分類

- 電子和半導體

- 化工/石油化工產品

- 飲食

- 製藥和醫療保健

- 零售與電子商務

- 其他

- 貿易通道

- 亞洲內部

- 北美洲

- 歐洲

- 中東

- 非洲

- 南美洲

- 大洋洲

- 按區域/連接埠叢集

- 西部地區(大士和裕廊)

- 中部地區(巴西班讓和吉寶)

- 北部地區(三巴旺)

- 東部地區(樟宜和洛陽)

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- PSA International

- Ocean Network Express(ONE)

- Pacific International Lines(PIL)

- AP Moller-Maersk Singapore

- CMA CGM & ANL(Singapore)

- Evergreen Marine(Singapore)

- Hapag-Lloyd(Singapore)

- Cosco Shipping Lines(Singapore)

- Yang Ming(Singapore)

- X-Press Feeders(Sea Consortium)

- DHL Global Forwarding Singapore

- Kuehne+Nagel Singapore

- NYK Line(Yusen Logistics)

- DSV Air & Sea Singapore

- Sinotrans Singapore

- Agility Logistics Singapore

- Toll Group Singapore

- OOCL(Singapore)

- FedEx Logistics Singapore

- CEVA Logistics Singapore*

第7章 市場機會與未來展望

The Singapore Sea Freight Transport Market size is estimated at USD 7.32 billion in 2025, and is expected to reach USD 10.57 billion by 2030, at a CAGR of 7.63% during the forecast period (2025-2030).

This momentum rests on the phased shift of all container activity to Tuas Mega-Port, a move that frees berth capacity while cutting vessel turnaround times. Digital tools-most notably electronic bills of lading and a unified port community system-are trimming paperwork and giving carriers fresh reasons to keep Singapore at the centre of their networks. Preferential trade pacts widen the export hinterland and, together with a manufacturing tilt toward Southeast Asia, are lifting outbound TEU counts. A growing stream of liquid bulk linked to cleaner energy and a modal swing toward sea freight for temperature-controlled pharmaceuticals add further lift. Rising bunker costs and price competition from Malaysian neighbours remain watch points, yet the combination of new capacity and more diversified trade lanes keeps the growth outlook firmly on course.

Singapore Sea Freight Transport Market Trends and Insights

Tuas Mega-Port Consolidation Elevating Throughput

The consolidation of legacy city terminals into Tuas Mega-Port is transforming Singapore's competitiveness by pushing planned capacity toward 65 million TEUs in the 2040s-almost double the 37.5 million TEUs handled in 2021 . Phase 1, opened in 2022, already deploys more than 200 Automated Guided Vehicles, while an event-driven digital backbone orchestrates yard moves in real time. Because the facility sits on a single contiguous coastline, internal trans-shifts fall sharply, improving crane utilisation and vessel turnaround. The resulting predictability lets carriers rationalise dual calls on the same loop, freeing vessel days for extra sailings. An immediate inference is that shipping lines gain both cost savings and greenhouse-gas reductions through shorter port dwell, tightening Singapore's hold on hub status.

ASEAN Manufacturing Shift Driving Export TEUs

Relocation of electronics, precision-engineering and consumer-durables production from North Asia into ASEAN is pumping new export volumes through Singapore. United Microelectronics Corp.'s USD 5 billion semiconductor fab and similar investments pull in wafer tools, chemicals and finished chips that ride outbound feeder services before transhipment onto deep-sea loops. Vietnam's industrial expansion follows an identical pattern, using Singapore as its load-centre gateway via digital trade corridors being built by YCH Group and Vietnam Post. The widened supplier footprint spreads geopolitical risk and deepens network density, indicating that intra-ASEAN demand will support berth utilisation even when global cycles soften.

Volatile Bunker Prices Translating into Higher Freight Rates

Container spot rates on several long-haul trades more than doubled through late 2024, propelled by a 256 % spike on the Shanghai-Europe route tied to Red Sea diversions. In Singapore, biofuel bunkering volumes tripled in 2023, adding a fresh price reference to carriers' fuel cost base. Although alternative grades help with decarbonisation targets, their nascent supply chains inject volatility into index-linked fuel surcharges. Shippers therefore prioritise ports with minimal in-harbour delay so that bunker burn remains predictable; Singapore's efficiency gains cushion, but do not eliminate, that volatility.

Other drivers and restraints analyzed in the detailed report include:

- Preferential Trade Agreements Cutting Sea-Freight Costs

- DigitalPORT@SG & Electronic Bill-of-Lading Adoption

- Competitive Pressure from Port Klang & Tanjung Pelepas

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Containerised cargo commands a 61% Singapore Sea Freight market share in 2024, and its prominence is expected to persist through 2030 as reefer adoption widens. Higher uptake of temperature-controlled boxes for vaccines and biologics is pushing PSA to add plug points and controlled-atmosphere monitoring, making container operations a strategic enabler for life-science exporters. Liquid bulk shows the fastest forecast growth at 8.1% CAGR, propelled by biofuel blending and nascent green-ammonia projects that need dedicated berths on Jurong Island. Dry bulk volumes grow modestly on the back of regional construction demand, while general cargo and roll-on/roll-off remain stable niches. The interplay of automation, digital twins, and blockchain within these segments boosts predictability, allowing terminal operators to fine-tune yard staging for each commodity class.

The Singapore Sea Freight Transport Market Report Segments the Industry Into by Cargo Type (Containerized Cargo, Dry Bulk Cargo and More), by End User Industry (Electronics & Semiconductors, Chemicals & Petrochemicals, Food & Beverage and More), by Trade Lane (Intra-Asia, North America, Europe and More) and by Region/Port Cluster(West Region, Central Region and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- PSA International

- Ocean Network Express (ONE)

- Pacific International Lines (PIL)

- A.P. Moller-Maersk Singapore

- CMA CGM & ANL (Singapore)

- Evergreen Marine (Singapore)

- Hapag-Lloyd (Singapore)

- Cosco Shipping Lines (Singapore)

- Yang Ming (Singapore)

- X-Press Feeders (Sea Consortium)

- DHL Global Forwarding Singapore

- Kuehne + Nagel Singapore

- NYK Line (Yusen Logistics)

- DSV Air & Sea Singapore

- Sinotrans Singapore

- Agility Logistics Singapore

- Toll Group Singapore

- OOCL (Singapore)

- FedEx Logistics Singapore

- CEVA Logistics Singapore*

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Consolidation of City Terminals into Tuas Mega-Port Elevating Throughput

- 4.2.2 ASEAN Manufacturing Shift Driving Export TEUs from Singapore

- 4.2.3 Preferential Trade Agreements (RCEP, CPTPP) Cutting Sea-Freight Costs

- 4.2.4 DigitalPORT@SG & Electronic Bill-of-Lading Adoption Shortening Dwell-Time

- 4.2.5 Expansion of Cold-Chain TEUs for Pharma & Perishables

- 4.2.6 Green & Digital Shipping-Corridor Initiatives

- 4.3 Market Restraints

- 4.3.1 Volatile Bunker Prices Translating into Higher All-in Freight Rates

- 4.3.2 Competitive Pressure from Port Klang & Tanjung Pelepas Feeder Rates

- 4.3.3 Shortage of 40-ft High-Cube Reefers During Peak Season

- 4.3.4 Tight Trucking Capacity for First/Last-Mile on Jurong Island

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory & Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Cargo Type

- 5.1.1 Containerized Cargo

- 5.1.1.1 Dry

- 5.1.1.2 Reefer

- 5.1.2 Dry Bulk Cargo

- 5.1.3 Liquid Bulk Cargo

- 5.1.4 General Cargo

- 5.1.5 Roll-On/Roll-Off Cargo

- 5.1.1 Containerized Cargo

- 5.2 By End-User Industry

- 5.2.1 Electronics & Semiconductors

- 5.2.2 Chemicals & Petrochemicals

- 5.2.3 Food & Beverage

- 5.2.4 Pharmaceuticals & Healthcare

- 5.2.5 Retail & E-commerce

- 5.2.6 Others

- 5.3 By Trade Lane

- 5.3.1 Intra-Asia

- 5.3.2 North America

- 5.3.3 Europe

- 5.3.4 Middle East

- 5.3.5 Africa

- 5.3.6 South America

- 5.3.7 Oceania

- 5.4 By Region / Port Cluster

- 5.4.1 West Region (Tuas & Jurong)

- 5.4.2 Central Region (Pasir Panjang & Keppel)

- 5.4.3 North Region (Sembawang)

- 5.4.4 East Region (Changi & Loyang)

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)}

- 6.4.1 PSA International

- 6.4.2 Ocean Network Express (ONE)

- 6.4.3 Pacific International Lines (PIL)

- 6.4.4 A.P. Moller-Maersk Singapore

- 6.4.5 CMA CGM & ANL (Singapore)

- 6.4.6 Evergreen Marine (Singapore)

- 6.4.7 Hapag-Lloyd (Singapore)

- 6.4.8 Cosco Shipping Lines (Singapore)

- 6.4.9 Yang Ming (Singapore)

- 6.4.10 X-Press Feeders (Sea Consortium)

- 6.4.11 DHL Global Forwarding Singapore

- 6.4.12 Kuehne + Nagel Singapore

- 6.4.13 NYK Line (Yusen Logistics)

- 6.4.14 DSV Air & Sea Singapore

- 6.4.15 Sinotrans Singapore

- 6.4.16 Agility Logistics Singapore

- 6.4.17 Toll Group Singapore

- 6.4.18 OOCL (Singapore)

- 6.4.19 FedEx Logistics Singapore

- 6.4.20 CEVA Logistics Singapore*

7 Market Opportunities & Future Outlook

全球海運市場

全球海運市場 2025年全球生鮮產品海運市場報告

2025年全球生鮮產品海運市場報告 海運的全球市場:貨物類別,技術整合,各服務形式,各類服務,各地區,機會,預測,2018年~2032年2025年海運全球市場報告

海運的全球市場:貨物類別,技術整合,各服務形式,各類服務,各地區,機會,預測,2018年~2032年2025年海運全球市場報告 2025-2033 年海運貨運代理市場(按類型(整箱裝載、拼箱裝載等)、服務、垂直領域和地區分類)海運市場評估:類型·服務·產業·各地區的機會及預測 (2018-2032年)全球海運市場

2025-2033 年海運貨運代理市場(按類型(整箱裝載、拼箱裝載等)、服務、垂直領域和地區分類)海運市場評估:類型·服務·產業·各地區的機會及預測 (2018-2032年)全球海運市場 海運:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)海運:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)

海運:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)海運:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029) 2024-2028 年全球海運市場

2024-2028 年全球海運市場