|

市場調查報告書

商品編碼

1850262

暖通空調服務:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)HVAC Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

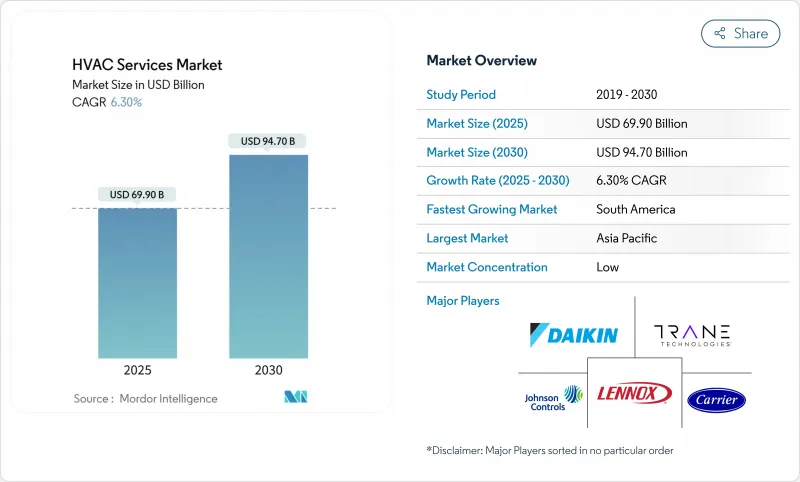

預計到 2025 年,暖通空調服務市場規模將達到 699 億美元,到 2030 年將擴大到 947 億美元,複合年成長率為 6.30%。

需求主要源自於超大規模資料中心的建置、由氫氟碳化合物(HFC)減排政策推動的維修浪潮,以及將被動維修轉變為預測性服務合約的數位化。亞太地區的經濟成長勢頭、快速的都市化以及資料中心的蓬勃發展,鞏固了該地區的收入領先地位。同時,全球各地的超大規模營運商正推動暖通空調(HVAC)服務市場向專業冷卻、液冷溫度控管以及保障正常運作的訂閱定價模式轉型。儘管現有供應商正透過物聯網分析平台實現裝置量客戶群的獲利,並將故障維修服務轉變為持續的最佳化服務,但技術純熟勞工短缺和投入成本上漲正威脅著淨利率。因此,競爭壓力有利於那些能夠將規模化採購與強大的內部培訓相結合,從而抵禦工資上漲並從規模較小的競爭對手手中奪取市場佔有率的公司。

全球暖通空調服務市場趨勢與洞察

新興國家建設活動的擴張

亞太和拉丁美洲加速的都市化推動了新建項目的湧現,進而帶動了暖通空調(HVAC)服務市場的安裝和試運行需求。建築許可中納入的能源效率標準正促使人們將生命週期支出從緊急維修轉向預防性保養和性能合約。在印度和巴西,政府的綠建築獎勵措施鼓勵早期採用高效暖通空調系統,促使開發商在設計階段就簽訂服務合約。能夠在交付時整合數位化監控的供應商,可以在建築物的整個生命週期內獲得類似年金的收入。加州向Lincus公司提供的176萬美元津貼,用於直流供電的商用系統,體現了政策制定者對依賴專業服務技術的下一代系統的承諾。

超大規模資料中心建置的擴展

超大規模資料中心需要複雜的、通常基於液體的冷卻系統,傳統機械承包商若不大幅提升自身技能,則難以滿足需求。冷卻能耗可能佔資料中心電力預算的50%之多,因此,效率是營運商整體擁有成本的核心組成部分,也是選擇服務供應商的關鍵因素。因此,暖通空調服務市場青睞那些擁有先進流體處理技術和人工智慧主導的監控能力的公司,這些能力能夠預測故障發生前的熱點區域。特靈科技與LiquidStack的合作,展現了原始設備製造商(OEM)如何與液體冷卻專家攜手合作,加速自身能力的提升。預計到2024年初,資料中心資本支出將激增185%,達到540億美元,將確保專業服務需求的強勁成長。

技術純熟勞工短缺和工資上漲

全球暖通空調服務市場需要新增11萬名技術人員,但目前從業人員中已有半數超過45歲。服務提供者目前的平均年薪為59,620美元,而資料中心專業的薪資則高得多。隨著物聯網平台融合IT和OT,需要兼具機器和數位技術的混合技能,人才缺口將更加嚴峻。那些投資內部培訓機構的公司能夠維持服務品質和運作的保障,而資金不足的競爭對手則面臨客戶流失的風險。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 新興國家建設活動增加

- 超大規模資料中心擴建

- 強制逐步減少冷媒的使用推動了對維修的需求。

- 經合組織成員國的老舊建築需要維修。

- 利用遠距離診斷和機器人技術降低服務成本

- 暖通空調即服務合約釋放年金收入潛力

- 市場限制

- 技術純熟勞工短缺和工資上漲

- 暖通空調零件供應的不確定性和材料價格上漲

- 互聯建築系統中的網路安全風險

- 訂閱模式的顛覆性變革對利潤率帶來壓力

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 投資與併購格局

第5章 市場規模與成長預測

- 按安裝類型

- 新建工程

- 建築改裝

- 按服務類型

- 安裝和更換服務

- 維護和維修服務

- 能源效率和維修服務

- 暖通空調控制系統升級與整合

- 諮詢及其他服務

- 依系統類型

- 暖氣服務

- 冷凍服務

- 通風和室內空氣品質服務

- 綜合建築管理服務

- 最終用戶

- 住房

- 商業的

- 產業

- 透過使用

- 資料中心

- 醫療機構

- 教育機構

- 飯店及休閒

- 零售空間

- 政府及公共建築

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 墨西哥

- 其他南美洲

- 歐洲

- 英國

- 德國

- 法國

- 比荷盧經濟聯盟

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 亞太其他地區

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Johnson Controls International PLC

- Carrier Global Corporation

- Daikin Industries Ltd.

- Trane Technologies plc

- Lennox International Inc.

- Honeywell International Inc.

- Siemens AG

- LG Electronics Inc.

- Electrolux AB

- Robert Bosch GmbH

- Fujitsu General Ltd.

- Nortek Global HVAC

- Mitsubishi Electric Corporation

- Rheem Manufacturing Company

- Danfoss A/S

- GREE Electric Appliances Inc.

- Midea Group Co. Ltd.

- Johnson Service Group plc

- Comfort Systems USA, Inc.

- EMCOR Group Inc.

第7章 市場機會與未來展望

The HVAC services market size reached USD 69.90 billion in 2025 and is projected to advance to USD 94.70 billion by 2030, translating to a 6.30% CAGR-evidence that the HVAC services market remains resilient despite refrigerant phase-downs, talent shortages, and supply volatility.

Demand stems from hyperscale data-center construction, a wave of retrofits triggered by mandatory HFC reductions, and digitization that converts reactive fixes into predictive service contracts. Asia-Pacific's economic momentum, rapid urbanization, and data-center boom secure the region's leadership in revenue terms, while hyperscale operators everywhere are propelling the HVAC services market toward specialized cooling, liquid-based thermal management, and subscription pricing for uptime assurance. Established providers are monetizing their installed base through IoT-enabled analytics platforms that transform break-fix visits into continuous optimization services, yet skilled-labor scarcity and input-cost inflation threaten margins. Competitive pressure therefore favors companies that combine scale procurement with strong in-house training, allowing them to absorb wage inflation while capturing share from smaller rivals.

Global HVAC Services Market Trends and Insights

Growing Construction Activity in Emerging Economies

Accelerating urbanization across Asia-Pacific and Latin America sustains new building pipelines that automatically translate into installation and commissioning demand for the HVAC services market. Energy-efficiency codes now embedded in building permits shift lifetime spending toward preventive maintenance and performance contracts rather than emergency repairs. Government green-building incentives in India and Brazil reward early adoption of high-efficiency HVAC, nudging developers to lock in service contracts during the design phase. Providers able to embed digital monitoring at handover secure annuity-style revenue across a building's lifecycle. California's USD 1.76 million grant to Lincus for DC-powered commercial HVAC validates policymaker commitment to next-generation systems that depend on specialist service expertise

Expansion of Hyperscale Data-Center Build-Outs

Hyperscale facilities require precise, often liquid-based cooling that traditional mechanical contractors cannot service without significant up-skilling. Cooling can reach 50% of a data center's power budget, making efficiency gains central to operators' total cost of ownership and a decisive service-provider selection factor . The HVAC services market therefore rewards firms with advanced fluid-handling skills and AI-driven monitoring that predict hot-spots before failures occur. Trane Technologies' collaboration with LiquidStack illustrates how OEMs partner with liquid-cooling experts to accelerate capability build-out. Data-center capital outlays surged 185% to USD 54 billion in early 2024, guaranteeing a robust pipeline of specialized service demand.

Skilled-Labor Shortages and Escalating Wage Bills

The HVAC services market needs an additional 110,000 technicians worldwide, while half the current workforce is already older than 45 . Providers now pay USD 59,620 on average, with specialized data-center roles commanding far higher compensation, squeezing smaller contractors that lack tiered pricing power. The talent gap becomes more acute as IoT platforms converge IT and OT, demanding hybrid mechanical-digital skills. Companies funding in-house academies can maintain service quality and uptime guarantees, while less capitalized rivals risk client attrition.

Other drivers and restraints analyzed in the detailed report include:

- Mandatory Refrigerant Phase-Downs Driving Retrofit Demand

- Aging Building Stock in OECD Markets Requiring Upgrades

- Volatile HVAC Component Supply & Material Inflation

For complete list of drivers and restraints, kindly check the Table Of Contents.

List of Companies Covered in this Report:

- Johnson Controls International PLC

- Carrier Global Corporation

- Daikin Industries Ltd.

- Trane Technologies plc

- Lennox International Inc.

- Honeywell International Inc.

- Siemens AG

- LG Electronics Inc.

- Electrolux AB

- Robert Bosch GmbH

- Fujitsu General Ltd.

- Nortek Global HVAC

- Mitsubishi Electric Corporation

- Rheem Manufacturing Company

- Danfoss A/S

- GREE Electric Appliances Inc.

- Midea Group Co. Ltd.

- Johnson Service Group plc

- Comfort Systems USA, Inc.

- EMCOR Group Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing construction activity in emerging economies

- 4.2.2 Expansion of hyperscale data-center build-outs

- 4.2.3 Mandatory refrigerant phase-downs driving retrofit demand

- 4.2.4 Aging building stock in OECD markets requiring upgrades

- 4.2.5 Remote diagnostics and robotics lowering service costs

- 4.2.6 HVAC-as-a-Service contracts unlocking annuity revenues

- 4.3 Market Restraints

- 4.3.1 Skilled-labor shortages and escalating wage bills

- 4.3.2 Volatile HVAC component supply and material inflation

- 4.3.3 Cyber-security risks in connected building systems

- 4.3.4 Subscription-based disruptors compressing margins

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porters Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment and M&A Landscape

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Implementation Type

- 5.1.1 New Construction

- 5.1.2 Retrofit Buildings

- 5.2 By Service Type

- 5.2.1 Installation and Replacement Services

- 5.2.2 Maintenance and Repair Services

- 5.2.3 Energy-Efficiency and Retrofit Services

- 5.2.4 HVAC Controls Upgrade and Integration

- 5.2.5 Consulting and Other Services

- 5.3 By System Type

- 5.3.1 Heating Services

- 5.3.2 Cooling Services

- 5.3.3 Ventilation and IAQ Services

- 5.3.4 Integrated Building-Management Services

- 5.4 By End User

- 5.4.1 Residential

- 5.4.2 Commercial

- 5.4.3 Industrial

- 5.5 By Application Vertical

- 5.5.1 Data Centers

- 5.5.2 Healthcare Facilities

- 5.5.3 Educational Institutions

- 5.5.4 Hospitality and Leisure

- 5.5.5 Retail Spaces

- 5.5.6 Government and Public Buildings

- 5.5.7 Others

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Mexico

- 5.6.2.4 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Benelux

- 5.6.3.5 Rest of Europe

- 5.6.4 APAC

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 Rest of APAC

- 5.6.5 Middle East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 South Africa

- 5.6.5.4 Rest of Middle East and Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Johnson Controls International PLC

- 6.4.2 Carrier Global Corporation

- 6.4.3 Daikin Industries Ltd.

- 6.4.4 Trane Technologies plc

- 6.4.5 Lennox International Inc.

- 6.4.6 Honeywell International Inc.

- 6.4.7 Siemens AG

- 6.4.8 LG Electronics Inc.

- 6.4.9 Electrolux AB

- 6.4.10 Robert Bosch GmbH

- 6.4.11 Fujitsu General Ltd.

- 6.4.12 Nortek Global HVAC

- 6.4.13 Mitsubishi Electric Corporation

- 6.4.14 Rheem Manufacturing Company

- 6.4.15 Danfoss A/S

- 6.4.16 GREE Electric Appliances Inc.

- 6.4.17 Midea Group Co. Ltd.

- 6.4.18 Johnson Service Group plc

- 6.4.19 Comfort Systems USA, Inc.

- 6.4.20 EMCOR Group Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

暖通空調服務管理軟體市場:2026-2030年全球市場預測(依產品類型、定價模式、平台/設備、部署類型、組織規模及最終用戶分類)

暖通空調服務管理軟體市場:2026-2030年全球市場預測(依產品類型、定價模式、平台/設備、部署類型、組織規模及最終用戶分類) 2026年全球電容器更換管服務市場報告

2026年全球電容器更換管服務市場報告 暖通空調服務市場分析及預測(至2035年):按類型、產品、服務、技術、組件、應用、安裝類型、設施、解決方案和最終用戶分類

暖通空調服務市場分析及預測(至2035年):按類型、產品、服務、技術、組件、應用、安裝類型、設施、解決方案和最終用戶分類 HVAC清潔服務市場-全球產業規模、佔有率、趨勢、機會和預測:按組件、清潔工具、清潔設備、最終用戶、地區和競爭格局分類,2021-2031年HVAC按需服務市場:按服務類型、交付模式、回應時間、支付模式、應用程式和最終用戶分類的全球預測,2026-2032年暖通空調維修服務市場按服務類型、設備類型、應用、最終用戶和分銷管道分類,全球預測(2026-2032年)

HVAC清潔服務市場-全球產業規模、佔有率、趨勢、機會和預測:按組件、清潔工具、清潔設備、最終用戶、地區和競爭格局分類,2021-2031年HVAC按需服務市場:按服務類型、交付模式、回應時間、支付模式、應用程式和最終用戶分類的全球預測,2026-2032年暖通空調維修服務市場按服務類型、設備類型、應用、最終用戶和分銷管道分類,全球預測(2026-2032年) 歐洲暖通空調服務市場:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)

歐洲暖通空調服務市場:市佔率分析、產業趨勢與統計、成長預測(2026-2031年) 2025-2029年全球暖通空調服務市場美國暖通空調服務:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)

2025-2029年全球暖通空調服務市場美國暖通空調服務:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年) 北美暖通空調服務市場:市場規模、佔有率和趨勢分析(按服務、設備、最終用途和國家/地區),按細分市場預測(2025-2030 年)

北美暖通空調服務市場:市場規模、佔有率和趨勢分析(按服務、設備、最終用途和國家/地區),按細分市場預測(2025-2030 年)