|

市場調查報告書

商品編碼

1850157

甘油:市場佔有率分析、產業趨勢、統計數據、成長預測(2025-2030)Glycerin - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

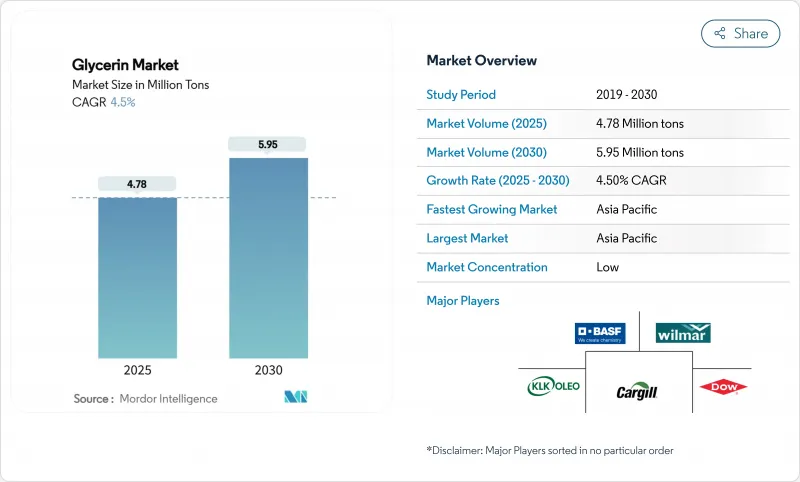

預計到 2025 年甘油市場規模為 478 萬噸,到 2030 年將達到 595 萬噸,預測期(2025-2030 年)複合年成長率為 4.5%。

醫藥級產品的應用、個人護理配方研發的蓬勃發展以及歐洲日益嚴格的生物基化學品法規,都在推動市場需求。生質柴油生產商與大型油脂化學公司之間的垂直整合有助於穩定原料供應,而煉油技術的進步則使規模較小的公司能夠將原油提純至精煉規格。亞太地區憑藉其龐大的製造業基礎保持著定價權,而美國對生物柴油的持續投資正在形成區域性盈餘,並流入出口管道。然而,甘油市場極易受到粗甘油價格波動的影響,而粗甘油價格又與生質柴油原料成本密切相關,迫使煉油商簽訂長期承購協議以保障利潤。

全球甘油市場趨勢與洞察

製藥業對USP級甘油的需求迅速成長

監管機構日益嚴格的品質法規推動了對純度為99.5%或更高的USP級甘油的需求。美國FDA現要求生產商確保二伸乙甘醇和乙二醇含量低於0.10%,迫使買家優先考慮完全可追溯的供應鏈。歐洲和亞洲的製藥公司正與能夠提供批次級認證的綜合精煉廠簽訂多年供應協議,從而在這個高階市場獲得更高的利潤。生產線正在升級,採用先進的氣相層析法系統來確保污染物控制,鞏固了精製甘油作為重要輔料的地位。對於甘油市場而言,製藥業的成長為其提供了一個穩固的需求支柱,該支柱在很大程度上不受生物柴油價格波動的影響。

在個人護理和化妝品行業中的使用日益增多

配方師正利用甘油的保濕功效,為潔淨標示產品提供持久的肌膚保濕效果。除了簡單的保濕作用外,越來越多的研究人員將甘油與神經醯胺和菸鹼醯胺結合,打造出深受消費者喜愛的屏障修復系統。雖然這一趨勢在亞洲最為顯著,但全球品牌也在升級其傳統產品線,提高天然成分的含量,使其平均含量達到3%或更高(以重量計)。精製甘油氣味成分低,能夠與以香氛為主的化妝品完美融合。來自美容領域的穩定需求有望抵消工業終端應用領域的周期性放緩,並增強甘油整體市場的銷售穩定性。

粗甘油價格波動與生質柴油原料價格波動有關。

粗甘油價格隨大豆、菜籽和廢油成本波動,為煉油商的利潤率帶來不確定性,並使預算預測變得複雜。轉向使用動物油脂會導致雜質含量升高,並迫使煉油商增加額外的精煉步驟,從而損害盈利。為了應對這種風險,主要買家正在轉向與指數掛鉤的契約,並採用精煉塔來適應原料品質的波動。儘管市場波動預計還將持續,但簽訂多年承購協議並實現原料來源多元化的公司將能夠保護自身利益,並對甘油市場的長期成長保持信心。

細分市場分析

到2024年,精製甘油將佔甘油市場68%的佔有率,預計到2030年將以每年4.9%的速度成長。這一成長反映了監管機構對污染物控制日益重視,以及個人護理和藥品上市產品對符合美國藥典(USP)標準的輔料的需求激增。精製甘油是精華液、乳液和注射劑必備的原料,因為其高純度能確保產品感官特性的一致性。

同時,粗甘油作為沼氣基材和藻類培養的碳源,正日益受到關注,從而實現下游收入多元化。隨著薄膜過濾和離子交換技術的成熟,精煉成本逐漸降低,不同等級甘油之間的價格差距也隨之縮小。

區域分析

預計亞太地區將在2024年佔據甘油市場48%的佔有率,並保持最快增速,到2030年將以5%的複合年成長率成長。中國憑藉其大規模的生物柴油生產和龐大的個人護理用品製造地,為該地區的供需提供了有力支撐。印度在油脂化學品領域的投資以及馬來西亞棕櫚油生物柴油的生產能力,也增強了該地區的自給自足能力。

北美是生物燃料的主要貢獻者,這得益於其成熟的生質燃料政策框架和發達的製藥業。美國計劃在2035年將生質燃料產量提高到130萬桶/日,並且擁有豐富的原油供應。

歐洲致力於引領永續性,德國、英國、義大利和法國等國在製藥、被覆劑和包裝領域廣泛使用精煉甘油。歐盟限制揮發性有機化合物(VOC)排放的法規正在推動以甘油基醇酸樹脂取代石油樹脂,而體積積層製造的實驗也正在擴大小眾市場的需求。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 亞洲和歐盟製藥業對USP級甘油的需求激增

- 在個人護理和化妝品行業中的應用日益廣泛

- 擴大生物柴油生產

- 對低揮發性有機化合物醇酸樹脂更嚴格的監管將增加甘油的使用(歐盟)

- 在中東、北非和東協地區,植物來源甘油在清真食品和純素食品中的應用日益廣泛。

- 市場限制

- 甘油的價格與原油價格和生質柴油原料價格的波動有關。

- 替代產品的供應情況

- 嚴格的藥品專論限制了工業級藥品的應用

- 價值鏈分析

- 原料分析

- 價格分析(歷史數據和預測)

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 按年級

- 粗甘油

- 精製甘油

- 按原料

- 生質柴油

- 脂肪酸

- 脂醇類

- 其他成分

- 透過使用

- 個人護理和化妝品

- 製藥

- 食品/飲料

- 聚醚多元醇

- 醇酸樹脂和表面塗料

- 煙草保濕劑

- 其他用途

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 加勒比海島嶼

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 南非

- 埃及

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略性舉措(併購、合資、夥伴關係)

- 市佔率(%)/排名分析

- 公司簡介

- ADM

- Aemetis, Inc.

- BASF

- Biodex-SA

- Cargill, Incorporated

- Dow

- Emery Oleochemicals

- Godrej Industries Group

- IOI Corporation Berhad

- Kao Corporation

- KLK OLEO

- Louis Dreyfus Company

- Munzer Bioindustrie GmbH

- Musim Mas Group

- Oleon NV

- Procter & Gamble

- Renewable Biofuels

- Thai Glycerine Co.

- Vance Group Ltd.

- Vantage Specialty Chemicals, Inc.

- Wilmar International Ltd.

第7章 市場機會與未來展望

The Glycerin Market size is estimated at 4.78 Million tons in 2025, and is expected to reach 5.95 Million tons by 2030, at a CAGR of 4.5% during the forecast period (2025-2030).

Demand is lifted by pharmaceutical grade adoption, robust personal-care formulation pipelines, and tighter European rules that encourage bio-based chemistries. Vertical integration among biodiesel producers and oleochemical majors is helping stabilize feedstock availability, while advances in purification technology enable smaller firms to upgrade crude streams to refined specifications. Asia-Pacific retains pricing power thanks to its sizable manufacturing base, and sustained biodiesel investments in the United States create regional surpluses that flow into export channels. However, the Glycerin market remains vulnerable to sharp swings in crude glycerin prices that track biodiesel feedstock costs, compelling refiners to sign long-term offtake contracts that protect margins.

Global Glycerin Market Trends and Insights

Surging Demand for USP-grade Glycerin in Pharmaceutical Industry

Tightening quality rules from regulators are boosting demand for USP-grade glycerin that consistently tests above 99.5% purity. The United States FDA now requires manufacturers to verify diethylene glycol and ethylene glycol levels below 0.10%, forcing buyers to prioritize fully traceable supply chains. European and Asian drug makers are locking in multi-year supply deals with integrated refiners that can furnish batch-level certificates, and this premium segment is capturing higher margins. Production lines are being upgraded with advanced gas chromatography systems to guarantee contaminant control, cementing refined glycerin's position as an indispensable excipient. For the Glycerin market, pharmaceutical uptake is adding a defensible demand pillar that is largely insulated from biodiesel price noise.

Increasing Use in the Personal Care and Cosmetics Industries

Formulators are leveraging glycerin's humectant capability to deliver durable skin hydration in clean-label products. Beyond simple moisturization, research laboratories are pairing glycerin with ceramides and niacinamide to build barrier-repair systems that heighten consumer appeal. The trend is strongest in Asia, but global brands are reformulating legacy lines to raise natural-origin content, lifting average inclusion rates above 3% by weight. Because refined grades carry fewer odor compounds, they integrate seamlessly into fragrance-forward cosmetics. This steady pull from beauty applications is expected to offset any cyclical slowdown in industrial end-uses, reinforcing volume stability for the overall Glycerin market.

Volatile Crude Glycerin Prices Linked to Biodiesel Feedstock Swings

Crude glycerin prices fluctuate with soybean, canola, and waste-oil costs, destabilizing refiner margins and complicating budget forecasts. Feedstock shifts toward animal fats introduce higher impurity loads, forcing additional purification steps that erode profitability. To manage the risk, large buyers are migrating to index-linked contracts and installing polishing columns that flex with variable input quality. While volatility is expected to persist, firms that lock in multi-year offtake deals and diversify feedstock sourcing can shield themselves, preserving confidence in long-term Glycerin market expansion.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Biodiesel Production

- Regulatory Push for Low-VOC Alkyd Resins

- Availability of Substitutes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Refined grades commanded 68% of the Glycerin market in 2024, and segment volume is forecast to grow 4.9% annually to 2030. The upswing reflects regulatory emphasis on contaminant control and the surge in personal-care and pharmaceutical launches that require USP-compliant excipients. Higher purity enables consistent sensory profiles, making refined glycerin indispensable in serum, lotion, and injectable formulations.

At the same time, crude glycerin is attracting interest as a biogas substrate and as a carbon feed in algae cultivation, diversifying downstream revenue. Purification costs are gradually falling as membrane filtration and ion-exchange technologies mature, narrowing the price gap between grades and inviting mid-tier producers to enter the refined arena.

The Glycerin Market Report Segments the Industry by Grade (Crude Glycerin and Refined Glycerin), Source (Biodiesel, Fatty Acids, Fatty Alcohols, and Other Sources), Application (Personal Care and Cosmetics, Pharmaceuticals, Food and Beverage, Polyether Polyols, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

Asia-Pacific led the Glycerin market with a 48% share in 2024 and is projected to register the fastest 5% CAGR to 2030. Thanks to extensive biodiesel build-outs and its sizable personal-care manufacturing hub, China anchors supply and demand. India's oleochemical investments and Malaysia's palm-based biodiesel capacity reinforce regional self-sufficiency.

North America contributes significantly, backed by its mature biofuel policy framework and sophisticated pharmaceutical sector. The United States plans to boost biofuel output to 1.3 million boepd by 2035, ensuring abundant crude glycerin flow.

Europe emphasizes sustainability leadership, with Germany, the United Kingdom, Italy, and France consuming refined glycerin in pharmaceuticals, coatings, and packaging. EU legislation limiting VOC emissions is spurring substitution of petro-resins by glycerin-based alkyds, and trials in volumetric additive manufacturing are expanding niche demand.

- ADM

- Aemetis, Inc.

- BASF

- Biodex-SA

- Cargill, Incorporated

- Dow

- Emery Oleochemicals

- Godrej Industries Group

- IOI Corporation Berhad

- Kao Corporation

- KLK OLEO

- Louis Dreyfus Company

- Munzer Bioindustrie GmbH

- Musim Mas Group

- Oleon NV

- Procter & Gamble

- Renewable Biofuels

- Thai Glycerine Co.

- Vance Group Ltd.

- Vantage Specialty Chemicals, Inc.

- Wilmar International Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Demand for USP-grade Glycerin in Pharmaceutical industry in Asia and EU

- 4.2.2 Increasing Use in the Personal Care and Cosmetics Industries

- 4.2.3 Expansion of Biodiesel Production

- 4.2.4 Regulatory Push for Low-VOC Alkyd Resins Boosting Glycerin Usage (EU)

- 4.2.5 Rising Adoption of Vegetable-sourced Glycerin in Halal and Vegan Foods in MENA, ASEAN Region

- 4.3 Market Restraints

- 4.3.1 Volatile Crude Glycerin Prices Linked to Biodiesel Feedstock Swings

- 4.3.2 Availability Of substitutes

- 4.3.3 Stringent Pharmaceutical Monographs Limiting Technical-grade Uptake

- 4.4 Value Chain Analysis

- 4.5 Feedstock Analysis

- 4.6 Pricing Analysis (Historical and Forecast)

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Grade

- 5.1.1 Crude Glycerin

- 5.1.2 Refined Glycerin

- 5.2 By Source

- 5.2.1 Biodiesel

- 5.2.2 Fatty Acids

- 5.2.3 Fatty Alcohols

- 5.2.4 Other Sources

- 5.3 By Application

- 5.3.1 Personal Care and Cosmetics

- 5.3.2 Pharmaceuticals

- 5.3.3 Food and Beverage

- 5.3.4 Polyether Polyols

- 5.3.5 Alkyd Resins and Surface Coatings

- 5.3.6 Tobacco Humectants

- 5.3.7 Other Applications

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.2.4 Caribbeans

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Turkey

- 5.4.5.4 South Africa

- 5.4.5.5 Egypt

- 5.4.5.6 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (Mergers and Acquisitions, JVs, Partnerships)

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global overview, Market overview, Core segments, Financials, Strategic info, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ADM

- 6.4.2 Aemetis, Inc.

- 6.4.3 BASF

- 6.4.4 Biodex-SA

- 6.4.5 Cargill, Incorporated

- 6.4.6 Dow

- 6.4.7 Emery Oleochemicals

- 6.4.8 Godrej Industries Group

- 6.4.9 IOI Corporation Berhad

- 6.4.10 Kao Corporation

- 6.4.11 KLK OLEO

- 6.4.12 Louis Dreyfus Company

- 6.4.13 Munzer Bioindustrie GmbH

- 6.4.14 Musim Mas Group

- 6.4.15 Oleon NV

- 6.4.16 Procter & Gamble

- 6.4.17 Renewable Biofuels

- 6.4.18 Thai Glycerine Co.

- 6.4.19 Vance Group Ltd.

- 6.4.20 Vantage Specialty Chemicals, Inc.

- 6.4.21 Wilmar International Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

- 7.2 Rapid Uptake of Glycerin in E-cigarette Liquids in Asia and Middle-East

粗甘油市場:依原料、等級、生產流程和最終用途分類-2026-2032年全球市場預測甘油市場:依原料、等級、應用和最終用戶分類-2026-2032年全球市場預測乙基己基甘油市場:按產品形式、功能、分銷管道、應用和最終用途分類的全球市場預測 – 2026–2032甘油市場:2026-2032年全球市場預測(依原料、純度、功能、應用及通路分類)食品級甘油市場:依實體形態、純度等級、原料及應用分類-2026-2032年全球市場預測

粗甘油市場:依原料、等級、生產流程和最終用途分類-2026-2032年全球市場預測甘油市場:依原料、等級、應用和最終用戶分類-2026-2032年全球市場預測乙基己基甘油市場:按產品形式、功能、分銷管道、應用和最終用途分類的全球市場預測 – 2026–2032甘油市場:2026-2032年全球市場預測(依原料、純度、功能、應用及通路分類)食品級甘油市場:依實體形態、純度等級、原料及應用分類-2026-2032年全球市場預測 全球化妝品用有機甘油市場規模、佔有率、趨勢和成長分析報告:2026-2034年技術級甘油市場規模、佔有率、成長率及產業分析:按類型、應用和地區劃分的分析與預測(2026-2034)

全球化妝品用有機甘油市場規模、佔有率、趨勢和成長分析報告:2026-2034年技術級甘油市場規模、佔有率、成長率及產業分析:按類型、應用和地區劃分的分析與預測(2026-2034) 全球甘油市場,市場規模(2025-2034 年)

全球甘油市場,市場規模(2025-2034 年) 2032 年食品甘油市場預測:按工藝、來源、等級、形式、應用、最終用戶和地區進行的全球分析

2032 年食品甘油市場預測:按工藝、來源、等級、形式、應用、最終用戶和地區進行的全球分析 食品級甘油市場報告:趨勢、預測和競爭分析(至 2031 年)

食品級甘油市場報告:趨勢、預測和競爭分析(至 2031 年)