|

市場調查報告書

商品編碼

1849915

生物分解聚合物:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)Bio-degradable Polymers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

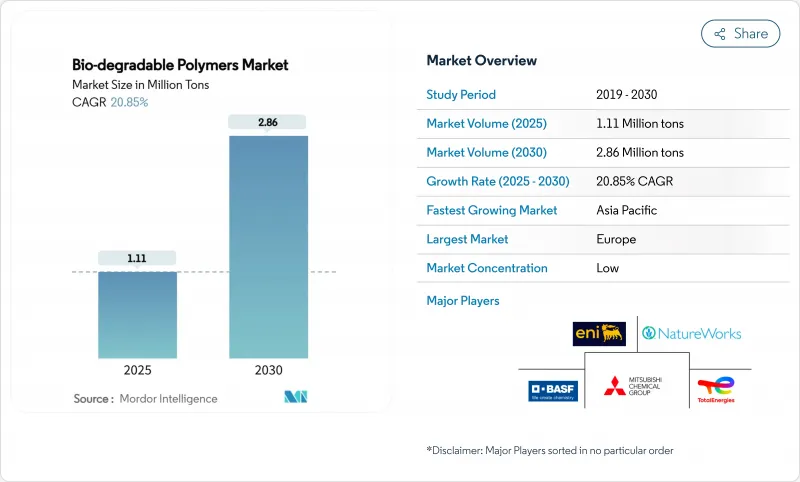

預計到 2025 年,可生物分解聚合物市場規模將達到 111 萬噸,到 2030 年將達到 286 萬噸,在預測期(2025-2030 年)內複合年成長率將達到 20.85%。

日益成長的監管壓力、不斷擴大的企業永續性目標以及微生物生產技術的快速發展,正在推動市場對高性能、低碳材料的需求。儘管歐洲仍是該地區最大的消費市場,但由於產業規模的擴大和相關法規的支持,亞太地區的發展速度最為快速。目前,產品創新主要集中在海洋可分解等級和經濟高效的聚羥基脂肪酸酯(PHAs)上,隨著大型石化企業、特種生質塑膠公司和新興企業同時增加對產能和研發的投資,市場競爭日益激烈。

全球可生物分解聚合物市場趨勢及洞察

政府對一次性塑膠製品的限制

全球法規正在重塑物質流動格局。歐盟的《包裝及包裝廢棄物條例》將於2024年最終定稿,該條例將強制要求在歐盟境內銷售的所有包裝必須可回收利用,並設定分階段的廢棄物減量目標,引導加工商使用經認證的可立即堆肥或回收的等級產品。英國將於2024年4月生效的塑膠濕紙巾禁令將進一步拓展衛生用品市場的機會。香港將於2024年禁止使用一次性吸管和EPS容器等物品,預示亞洲也將出現類似的趨勢。這些措施共同縮短了新建聚合物工廠的投資回收期,促進了承購協議的達成,並鼓勵下游品牌採用這些產品。

對永續包裝的需求日益成長

品牌所有者如今將永續性視為成長的驅動力,而非法規。高階食品和飲料製造商正轉向使用聚乳酸(PLA)、聚羥基脂肪酸酯(PHA)和塗佈紙等材料,以減少使用後的排放。朴茨茅斯大學實驗室的研究表明,PLA在海水和陽光照射下排放的微塑膠比傳統聚丙烯(PP)少九倍,這有助於提升品牌在具有海洋意識的消費者中的聲譽。可回收設計指南和電子商務的興起,正在創造對薄膜、托盤和硬質容器的巨大需求。

高昂的生產成本

設備攤銷、特殊原料以及工廠規模有限等因素導致平均售價高於普通聚乙烯(PE)和聚丙烯(PP)產品。丹尼默科學公司(Danimer Scientific)於2025年申請破產,凸顯了即使是技術領導企業也面臨著盈利的挑戰。儘管產能擴張和製程強化正在推動成本降低,但許多加工商仍對進入大眾市場包裝領域持謹慎態度。

細分市場分析

由於原料豐富且與現有吹膜和熱成型生產線相容,澱粉基聚合物佔據了可生物分解聚合物市場41.05%的佔有率。 PLA在硬質包裝和醫療設備領域保持著強勁的地位。 PHA可生物分解聚合物市場規模預計將以23.49%的複合年成長率成長,這主要得益於其快速的海洋分解特性和不斷提高的微生物發酵產量。聚酯基材料,例如PBS和PBAT,在捲邊膜和衛生背襯材料領域正不斷擴大市場佔有率,而纖維素基材料則被用於塗料和紙杯的生產。

成本平衡尚未實現。澱粉混合物享有農業補貼和簡化的配方,而PHA開發商則受益於碳捕獲額度和高利潤的醫藥銷售。可以預見,混合體系的趨勢可能會出現,從而實現更均衡的成本效益比。

區域分析

歐洲在環保領域領先39.19%,這主要歸功於政策的清晰性和消費者環保意識的增強。歐盟將於2024年最終確定的法規強制要求使用可回收或可堆肥包裝,而像芬蘭富騰公司(Fortum)的二氧化碳聚合物工廠這樣的開創性計劃則展示瞭如何將碳捕獲技術與生物基生產相結合。

亞太地區是成長最快的地區,複合年成長率達29.44%。中國正在加緊建設PHA和PBAT工廠,以滿足國家塑膠禁令的最後期限並供應農用薄膜。日本創新研發出含有二硫鍵的海洋可分解PBS,用於海洋浮標應用。

在北美,技術創新與企業自願目標之間保持平衡。陶氏化學與新能源藍公司(New Energy Blue)的協議將利用玉米秸稈生產生物乙烯,用於聚乙烯資產,從而為低碳替代能源鋪平道路。南美和中東仍在發展中,但已對可生物分解的覆蓋物表現出興趣,以減少露天焚燒。工業堆肥設施的缺乏限制了其短期應用,但也預示著長期基礎設施建設的機會。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 政府對一次性塑膠製品的使用進行限制

- 對永續和環保包裝的需求日益成長

- 醫療保健產業對生物分解性塑膠的採用率不斷提高

- 農業中可生物分解薄膜的使用激增

- 生物分解聚合物製造製程的技術創新及其產量提升

- 市場限制

- 與傳統塑膠相比,生產成本更高

- 限制車輛油耗的機械性質限制

- 缺乏工業堆肥設施

- 價值鏈分析

- 監理展望

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 按類型

- 澱粉基塑膠

- 聚乳酸(PLA)

- 聚羥基烷酯(PHA)

- 聚酯(PBS、PBAT、PCL)

- 纖維素衍生物

- 按原料

- 甘蔗和甜菜

- 玉米和其他澱粉作物

- 纖維素和木質生質能

- 廢棄植物油

- 藻類和微生物生質能

- 按最終用戶行業分類

- 包裹

- 消費品

- 紡織品

- 農業

- 衛生保健

- 其他行業(汽車、建築等)

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- ASEAN

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- BASF

- Biome Bioplastics

- BIOTEC Biologische Naturverpackungen GmbH & Co. KG.

- Braskem

- CJ CheilJedang Corp

- Danimer Scientific

- DuPont

- Evonik Industries AG

- FKuR

- GENECIS

- Mitsubishi Chemical Group Corporation

- NatureWorks LLC

- Eni SpA(Novamont)

- Plantic

- PTT MCC Biochem Co., Ltd.

- BEWI

- TEIJIN LIMITED

- TORAY INDUSTRIES, INC.

- TotalEnergies(Total Corbion)

- Zhejiang Hisun Biomaterials Co., Ltd.

第7章 市場機會與未來展望

The Bio-degradable Polymers Market size is estimated at 1.11 Million tons in 2025, and is expected to reach 2.86 Million tons by 2030, at a CAGR of 20.85% during the forecast period (2025-2030).

Heightened regulatory pressure, widening corporate sustainability goals, and rapid progress in microbial production technologies steer demand toward high-performance, low-carbon materials. Europe remains the largest regional consumer, while Asia-Pacific is advancing fastest due to industrial scale-up and supportive legislation. Product innovation now centers on marine-degradable grades and cost-efficient PHA, and competition is intensifying as petrochemical majors, specialty bioplastic firms, and start-ups invest simultaneously in capacity and research and development.

Global Bio-degradable Polymers Market Trends and Insights

Government Regulations Against Single-Use Plastics

Global rulemaking is reshaping material flows. The European Union's Packaging and Packaging Waste Regulation, finalized in 2024, obliges all packaging sold in the bloc to be recyclable and sets stepwise waste-reduction targets, immediately directing converters toward certified compostable or recyclable grades. The UK's ban on wet wipes containing plastic, introduced in April 2024, further enlarges the hygiene-product opportunity. Hong Kong's 2024 prohibition on single-use items such as straws and EPS containers signals similar momentum in Asia. Together, these measures are shortening payback periods for new polymer plants, accelerating off-take agreements, and incentivizing downstream brand adoption.

Growing Demand for Sustainable Packaging

Brand owners now treat sustainability as a growth driver rather than a compliance exercise. Premium food and beverage producers are shifting to PLA, PHA, and coated paper structures that lower end-of-life emissions. Laboratory evidence from the University of Portsmouth shows PLA emits nine times fewer microplastics under seawater-sunlight exposure than conventional PP, improving brand reputations among ocean-minded consumers. Design-for-recyclability guidelines and e-commerce expansion add to the pull, creating high-volume demand pockets for films, trays, and rigid containers.

High Production Cost

Equipment amortization, specialty feedstocks, and modest plant scales keep average selling prices above commodity PE and PP. The bankruptcy filing of Danimer Scientific in 2025 underscores profitability headwinds even for technology leaders. While increased capacity and process intensification are driving costs down, many converters still hesitate to commit to mass-market packaging segments.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Adoption in the Healthcare Industry

- Surge in Agricultural Films Usage

- Limited Mechanical Performance

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Starch-based grades hold 41.05% of the bio-degradable polymers market share due to abundant feedstock and compatibility with existing blown-film and thermoforming lines. PLA maintains a robust position in rigid packaging and medical devices. The bio-degradable polymers market size for PHA is projected to grow at a 23.49% CAGR, aided by its rapid marine degradation profile and improvements in microbial fermentation yields. Polyester families such as PBS and PBAT are gaining share in cling films and hygiene backsheets, while cellulosic derivatives serve coatings and paper cups.

Cost parity remains elusive. Starch blends enjoy agricultural subsidies and simpler compounding, but PHA developers benefit from carbon-capture credits and high-margin medical sales. A foreseeable convergence toward blended systems may deliver balanced cost-performance.

The Biodegradable Polymers Market Report Segments the Industry by Type (Starch-Based Plastics, Polylactic Acid (PLA), Polyhydroxy Alkanoates (PHA), and More), Feedstock (Sugarcane and Sugar Beets, Corn and Other Starch Crops, and More), End-User Industry (Packaging, Consumer Goods, Textile, and More), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

Europe's 39.19% leadership stems from policy clarity and consumer eco-awareness. The EU regulation finalized in 2024 forces recyclable or compostable packaging, and landmark projects such as Fortum's CO2-to-polymer plant in Finland illustrate how carbon capture integrates with bio-based production.

Asia-Pacific is the fastest-growing region at 29.44% CAGR. China ramps up PHA and PBAT plants to meet national plastic-ban deadlines and to supply agriculture films. Japan innovates marine-degradable PBS incorporating disulfide bonds for ocean buoy applications.

North America combines technological innovation with voluntary corporate targets. Dow's agreement with New Energy Blue uses corn stover to make bio-ethylene for PE assets, opening a low-carbon drop-in path. South America and the Middle East remain nascent but show interest in biodegradable mulch to reduce field-burning. Lack of industrial composting facilities curbs immediate uptake yet signals long-term infrastructure opportunities.

- BASF

- Biome Bioplastics

- BIOTEC Biologische Naturverpackungen GmbH & Co. KG.

- Braskem

- CJ CheilJedang Corp

- Danimer Scientific

- DuPont

- Evonik Industries AG

- FKuR

- GENECIS

- Mitsubishi Chemical Group Corporation

- NatureWorks LLC

- Eni S.p.A. (Novamont)

- Plantic

- PTT MCC Biochem Co., Ltd.

- BEWI

- TEIJIN LIMITED

- TORAY INDUSTRIES, INC.

- TotalEnergies (Total Corbion)

- Zhejiang Hisun Biomaterials Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government Regulations Againts the usage of SingleUse Plastics

- 4.2.2 Growing Demand for Sustainable and Eco-Friendly Packaging

- 4.2.3 Increasing Adoption of Bio Degradable Plastics in the Healthcare Industry

- 4.2.4 Surge in the Usage of Bio-Degradable Films in the Agricultural Industry

- 4.2.5 Growing Innovations in the Manufacturing Processes of Bio-Degradable Polymers Improving its Yield

- 4.3 Market Restraints

- 4.3.1 High Production Cost with Respect to Conventional Plastics

- 4.3.2 Limited Mechanical Performance Restricting Consumption in Automotive

- 4.3.3 Lack of Industrial Composting Facilities

- 4.4 Value Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Type

- 5.1.1 Starch-Based Plastics

- 5.1.2 Polylactic Acid (PLA)

- 5.1.3 Polyhydroxyalkanoates (PHA)

- 5.1.4 Polyesters (PBS, PBAT and PCL)

- 5.1.5 Cellulosic Derivatives

- 5.2 By Feedstock

- 5.2.1 Sugarcane and Sugar Beets

- 5.2.2 Corn and Other Starch Crops

- 5.2.3 Cellulose and Wood Biomass

- 5.2.4 Waste Vegetable Oils and Fats

- 5.2.5 Algal and Microbial Biomass

- 5.3 By End-user Industry

- 5.3.1 Packaging

- 5.3.2 Consumer Goods

- 5.3.3 Textile

- 5.3.4 Agriculture

- 5.3.5 Healthcare

- 5.3.6 Others (Automotive, Construction, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, Recent Developments)}

- 6.4.1 BASF

- 6.4.2 Biome Bioplastics

- 6.4.3 BIOTEC Biologische Naturverpackungen GmbH & Co. KG.

- 6.4.4 Braskem

- 6.4.5 CJ CheilJedang Corp

- 6.4.6 Danimer Scientific

- 6.4.7 DuPont

- 6.4.8 Evonik Industries AG

- 6.4.9 FKuR

- 6.4.10 GENECIS

- 6.4.11 Mitsubishi Chemical Group Corporation

- 6.4.12 NatureWorks LLC

- 6.4.13 Eni S.p.A. (Novamont)

- 6.4.14 Plantic

- 6.4.15 PTT MCC Biochem Co., Ltd.

- 6.4.16 BEWI

- 6.4.17 TEIJIN LIMITED

- 6.4.18 TORAY INDUSTRIES, INC.

- 6.4.19 TotalEnergies (Total Corbion)

- 6.4.20 Zhejiang Hisun Biomaterials Co., Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

- 7.2 Growing Inclination for Marine Degradable Polymers for Ocean Cleanups

生物分解聚合物市場:依產品類型、原料、最終用途及通路分類-2026-2030年全球市場預測

生物分解聚合物市場:依產品類型、原料、最終用途及通路分類-2026-2030年全球市場預測 電子產業用生物分解聚合物市場分析及預測(至2035年):依類型、產品、服務、技術、應用、材料類型、製程、最終用戶及功能分類

電子產業用生物分解聚合物市場分析及預測(至2035年):依類型、產品、服務、技術、應用、材料類型、製程、最終用戶及功能分類 2026年全球可生物分解聚合物市場報告

2026年全球可生物分解聚合物市場報告 澱粉基生物分解聚合物市場規模、佔有率和成長分析(按產品、最終用途、原料和地區分類)- 產業預測(2026-2033 年)

澱粉基生物分解聚合物市場規模、佔有率和成長分析(按產品、最終用途、原料和地區分類)- 產業預測(2026-2033 年) 生物分解聚合物市場規模、佔有率和成長分析(按類型、基材、最終用戶和地區分類)—2026-2033年產業預測

生物分解聚合物市場規模、佔有率和成長分析(按類型、基材、最終用戶和地區分類)—2026-2033年產業預測 酵素催化聚合物市場預測至2032年:按聚合物類型、酵素類型、生產流程、應用、最終用戶和地區分類的全球分析

酵素催化聚合物市場預測至2032年:按聚合物類型、酵素類型、生產流程、應用、最終用戶和地區分類的全球分析 酵素響應型生物分解聚合物市場規模、佔有率和趨勢分析報告:按材料、應用、地區和細分市場預測(2025-2033 年)

酵素響應型生物分解聚合物市場規模、佔有率和趨勢分析報告:按材料、應用、地區和細分市場預測(2025-2033 年) 生物分解聚合物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)電子產品用生物分解聚合物市場規模、佔有率和趨勢分析報告:按聚合物、應用、地區和細分市場預測(2025-2033 年)

生物分解聚合物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)電子產品用生物分解聚合物市場規模、佔有率和趨勢分析報告:按聚合物、應用、地區和細分市場預測(2025-2033 年) 對羥基肉桂酸:全球市佔率及排名、總收入及需求預測(2025-2031年)

對羥基肉桂酸:全球市佔率及排名、總收入及需求預測(2025-2031年)