|

市場調查報告書

商品編碼

1849870

觸控螢幕控制器:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030)Touch Screen Controllers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

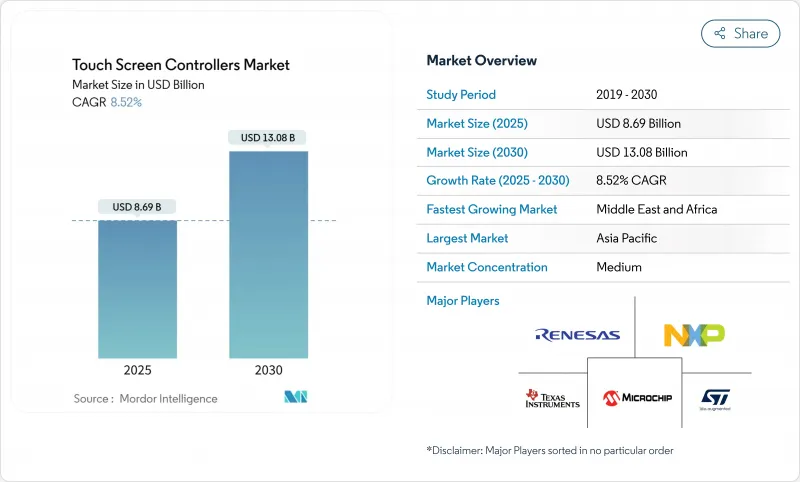

觸控螢幕控制器市場規模預計在 2025 年達到 86.9 億美元,到 2030 年將達到 130.8 億美元,複合年成長率為 8.52%。

成長的動力來自於智慧型手機中多點觸控介面的日益普及、更大的汽車顯示器以及產業向投射電容式 (PCAP) 面板的轉變。在供應方面,觸控和顯示器驅動IC(TDDI) 的整合減少了元件數量並實現了更薄的設備外形,而持續的晶圓級約束則支援高價位的汽車和醫療解決方案。零售自動化、需要超低功耗 32 位元控制器的穿戴式產品,以及驅動複雜邊緣偵測和防手掌誤觸控制器演算法的軟性 OLED 螢幕的日益普及,都增強了需求。由於電子製造地高度集中,亞太地區正迎來最強勁的發展勢頭,而中東和非洲則透過智慧城市計劃和自助結帳系統的推出釋放新的機會。

全球觸控螢幕控制器市場趨勢與洞察

軟性OLED智慧型手機顯示器中多點觸控電容技術的採用

智慧型手機製造商正在將顯示器延伸至曲面邊緣和折疊式鉸鏈鏈,這增加了觸控通道佈線和防手掌誤觸邏輯的複雜性。控制器必須處理不規則表面上不同的壓力輸入,同時最大限度地降低寄生電容。 2025 年展出的氧化物面板展示了整合式觸控路徑,可在螢幕佔比達到 90% 或更高的窄邊框中保持信噪比。邊緣屏蔽和局部驅動波形的專利組合正在觸控螢幕控制器市場中打造一個高階市場,使供應商能夠將其 IP 專門用於大批量旗艦設備,從而收益。

歐洲車載資訊娛樂系統升級至 2 級 ADAS

汽車儀錶板採用 34 吋曲面面板,整合了叢集、導航和媒體控制功能。這需要控制器具備寬動作溫度、嚴格的 EMI 抗擾度和容錯韌體。像 ATMXT3072M1 這樣的裝置採用 112 個可重構通道和獨特的互電容擷取方案,可將訊號雜訊比 (SNR) 提高 15 dB,即使在動力傳動系統和 ADAS 雷達的電磁應力下也能確保可靠偵測。顯示器上方嵌入的觸覺旋鈕可恢復觸覺回饋,提高駕駛注意力得分,並對控制器的掃描迴路施加額外的延遲限制。

55nm混合訊號晶圓供應鏈收緊

由於汽車 MCU 和工業IoT的需求與消費級觸控晶片競爭,關鍵 55nm 節點的晶圓代工配額依然緊張。控制器製造商擴大簽訂多年期合約以確保產能,這導致營運資金被轉移,設計週期被延長。一些公司正在針對 65nm 或 40nm 體矽 CMOS 製程重新設計產品,但這種移植可能會增加維修成本並增加晶粒尺寸。恩智浦揭露的配額有限,凸顯了整個觸控螢幕控制器市場近期的供應風險。

細分分析

電容式將在2024年佔據觸控螢幕控制器市場佔有率的71.5%,這反映出其在行動電話、平板電腦和汽車駕駛座領域的強勁應用。電容式透過蓋板玻璃感應,支援超過10個觸控點,在耐用性、光學清晰度和手勢豐富性方面具有關鍵的設計優勢。該細分市場受益於向整合TDDI晶片的持續過渡,該晶片可減少邊框數量和模組厚度。相反,電阻式產品繼續在手套式工廠主機和POS終端中採用,但由於PCAP價格下跌,其出貨量成長正在放緩。

到2030年,紅外線控制器的複合年成長率將達到10.8%,達到最高水準。邊框式發射器/接收器陣列使整合商能夠以適中的成本將產品擴展到100英寸以上,這對於教室、數位電子看板和重型資訊亭來說是一個關鍵優勢。紅外線LED驅動器效率的提升,加上改進的凝視引導演算法,正在降低延遲並提高對環境光的耐受性,從而鼓勵學校董事會和公司會議室考慮互動式牆。這種動態將保持觸控螢幕控制器市場的技術多樣性,供應商將同時提供PCAP、紅外線以及利基聲學或光學成像解決方案的產品線。

由於 I2C通訊協定具有兩線式的簡單性、低引腳數以及適用於系統晶片)環境的多主控功能,預計到 2024 年其收入將成長 43%。智慧型手機、穿戴式裝置和許多汽車顯示器都依賴 I2C 實現控制器和主處理器之間的低雜訊、低功耗通訊。 SPI 在頻寬要求不斷提高的平板電腦和高解析度平板電腦中蓬勃發展,而 UART 則用於需要極少韌體更新的傳統工業設備。

USB 憑藉其即插即用的特性以及支援觸控筆資料和懸停感應的高吞吐量,正在快速成長,複合年成長率高達 9.2%。自助服務終端、醫療推車和可拆卸顯示器的 ODM 對其標準連接器和與主機無關的枚舉流程青睞有加。白牌 PC 製造商也青睞 USB 觸控技術,因為它避免了增加橋接 IC 的成本。這種介面靈活性拓寬了應用範圍,擴大了觸控螢幕控制器市場的規模,並迫使供應商提供多介面韌體以實現無縫的現場重新配置。

區域分析

由於密集的零件供應鏈、高技能的勞動力以及政府對半導體自給自足的獎勵,亞太地區將在2024年佔據全球銷售額的61.8%。中國擁有主要的控制器IC晶圓廠和下游模組組裝商,為本土智慧型手機和消費性電子巨頭提供產品。像敦泰這樣的區域供應商持續創新,推出滿足汽車可靠性目標的整合顯示和觸控解決方案。韓國和日本憑藉其在OLED和氧化物TFT方面的專業知識引領產業,為軟性和折疊式設備貢獻高價值的控制器插座。

北美排名第二,這得益於汽車電子、醫療影像處理和工業自動化領域的平台創新。矽谷設計中心正專注於人工智慧增強訊號處理,以過濾複雜的噪音環境。零售連鎖店正在加速自助結帳設備的安裝,確保了對控制器單元的額外需求。該地區嚴格的網路安全要求正推動人們對內建於觸控控制器的硬體加速加密技術產生濃厚興趣。

歐洲嚴重依賴德國、法國和瑞典的汽車生產群集。嚴格的功能安全和電磁相容性標準導致設計時間更長,但也為合格供應商創造了市場空間。歐盟範圍內對 2 級和 3 級 ADAS 的推動,推動了採用更高通道數控制器的更大駕駛座顯示器的發展,從而增加了觸控螢幕控制器市場的應用多樣性。

到2030年,中東和非洲地區的複合年成長率將達到10.2%,居世界之冠。海灣經濟體的智慧城市專案正在訂購觸控式自助服務終端、數位電子看板和支付終端。零售和酒店業正在採用互動式系統,以減少服務等待時間。小型國內整合商正在透過全球經銷商採購控制器,並活性化本地設計活動。

在南美,隨著銀行升級ATM和教室技術,巴西和阿根廷市場呈現溫和擴張態勢。貨幣波動和關稅結構正在影響採購週期,而智慧型手機普及率的提高則推動了售後市場對翻新級觸控模組的需求。區域合作將拓寬觸控螢幕控制器市場的地域覆蓋範圍,並減少對亞洲產品的過度依賴。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場狀況

- 市場概況

- 市場促進因素

- 軟性OLED智慧型手機顯示器中多點觸控電容式的採用

- 歐洲車載資訊娛樂系統升級至 2 級 ADAS

- 北美勞動力短缺導致自助結帳系統POS機數量激增

- 攜帶式醫學影像設備的小型化

- 符合工業 4.0 標準的堅固型 PCAP 面板在中國取代了薄膜小鍵盤

- 觸控智慧型手錶轉向低功耗 32 位元控制器

- 市場限制

- 55nm混合訊號晶圓供應鏈凝聚力

- 24 吋及更大尺寸汽車電容式顯示器的 EMI/ESD 合規性問題

- 與印度白牌平板電腦製造商的控制器智慧財產權訴訟

- 由於面板製造商的垂直整合,平均售價下降

- 產業生態系統分析

- 技術概述(控制器架構和感測演算法)

- 監管環境(EMC 和汽車級標準)

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章市場規模及成長預測

- 依技術

- 阻力型

- 電容式(投射式和表面式)

- 表面聲波

- 紅外線的

- 光學成像

- 按介面

- I2C

- SPI

- USB

- UART

- 透過接觸點

- 單點觸控

- 多點觸控

- 按顯示尺寸

- 小於5英寸

- 5到10英寸

- 10吋或以上

- 按最終用戶產業

- 家電

- 工業和製造業

- 醫療保健和醫療設備

- 零售和 POS 終端

- 車

- 銀行和金融亭

- 其他(航空、教育)

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐國家(丹麥、瑞典、挪威、芬蘭)

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 東南亞

- 澳洲

- 其他亞太地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東

- GCC

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭態勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- NXP Semiconductors

- Renesas Electronics Corporation

- Samsung Electronics Co. Ltd.

- Texas Instruments Incorporated

- Analog Devices Inc.

- STMicroelectronics

- Microchip Technology Inc.

- Cypress(Infineon Technologies AG)

- Synaptics Incorporated

- Goodix Technology Inc.

- FocalTech Systems Co. Ltd.

- MELFAS Co. Ltd.

- Elan Microelectronics Corp.

- Novatek Microelectronics Corp.

- Ilitek I-SFT Technology Inc.

- Silicon Labs

- Himax Technologies Inc.

- Semtech Corporation

- Broadcom Inc.

- PixArt Imaging Inc.

- ROHM Semiconductor

- AMS OSRAM AG

- Raydium Semiconductor Corp.

第7章 市場機會與未來展望

The touch screen controllers market size is estimated at USD 8.69 billion in 2025 and is projected to reach USD 13.08 billion by 2030, reflecting an 8.52% CAGR.

Growth is propelled by rising adoption of multi-touch interfaces in smartphones, larger in-vehicle displays, and industrial migration to projected capacitive (PCAP) panels. On the supply side, integrated touch-and-display driver ICs (TDDI) are trimming component counts and enabling thinner device profiles, while ongoing wafer-level constraints encourage premium-priced automotive and medical solutions. Demand is reinforced by retail automation, wearables that require ultra-low-power 32-bit controllers, and expanding use of flexible OLED screens that push controller algorithms toward complex edge detection and palm rejection. Regional momentum is greatest in Asia Pacific because of its dense electronics manufacturing base, with incremental opportunities building in the Middle East and Africa through smart-city projects and self-checkout deployments.

Global Touch Screen Controllers Market Trends and Insights

Multi-touch Capacitive Adoption in Flexible OLED Smartphone Displays

Smartphone makers are stretching displays over curved edges and foldable hinges, raising complexity for touch-channel routing and palm-rejection logic. Controllers must process variable pressure inputs over irregular surfaces while minimizing parasitic capacitance. Oxide-based panels showcased in 2025 demonstrated integrated touch paths that sustain signal-to-noise ratios at narrow bezels above 90% screen-to-body levels. Patent portfolios around edge shielding and localized drive waveforms create a premium tier inside the touch screen controllers market, where suppliers monetize specialized IP against high-volume flagship handsets.

In-Vehicle Infotainment Upgrades with Level-2 ADAS in Europe

Car dashboards now host curved 34-inch panels that merge cluster, navigation, and media controls. Controllers, therefore, need wide operating temperatures, stringent EMI resilience, and fault-tolerant firmware. Devices such as the ATMXT3072M1 adopt 112 reconfigurable channels and proprietary mutual-cap acquisition schemes that raise SNR by 15 dB, ensuring reliable detection under electromagnetic stress from powertrains and ADAS radars. Haptic knobs embedded atop displays restore tactile feedback, improving driver attention scores and placing additional latency constraints on the controller's scan loop.

55 nm Mixed-Signal Wafer Supply-Chain Tightness

Foundry allocations at key 55 nm nodes remain strained because automotive MCU and industrial IoT demand compete with consumer touch chips. Controller makers increasingly sign multi-year take-or-pay contracts to guarantee capacity, diverting working capital and elongating design cycles. Some firms are redesigning products for 65 nm or 40 nm bulk CMOS, though such porting introduces requalification costs and can raise die size. NXP's disclosure of limited allocation windows underscores near-term supply risk across the touch screen controllers market.

Other drivers and restraints analyzed in the detailed report include:

- Self-Checkout POS Proliferation amid North-American Labor Shortages

- Industry 4.0 Rugged PCAP Panels Replacing Membrane Keypads in China

- EMI/ESD Compliance Issues for >24" Capacitive Automotive Displays

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Capacitive solutions captured 71.5% of the touch screen controllers market share in 2024, reflecting strong adoption in phones, tablets, and vehicle cockpits. Their ability to sense through cover-glass and to support ten-plus touch points secures design wins where durability, optical clarity, and gesture richness matter. The segment benefits from ongoing migration to integrated TDDI chips that lower bezel count and shrink module thickness. Conversely, resistive products continue serving glove-based factory consoles and point-of-sale terminals, though incremental volumes decline as PCAP pricing falls.

Infrared controllers post the highest 10.8% CAGR to 2030. Bezel-mounted emitter-receiver arrays let integrators scale beyond 100 inches at moderate cost, a key advantage for classrooms, digital signage, and heavy-duty kiosks. Efficiency gains in IR LED drivers combined with refined line-of-sight algorithms are reducing latency and improving ambient light immunity, prompting education boards and corporate meeting rooms to consider interactive walls. This dynamic keeps technology diversity alive inside the touch screen controllers market, encouraging vendors to maintain parallel product lines across PCAP, IR, and niche acoustic or optical imaging solutions.

The I2C protocol delivered 43% revenue in 2024 thanks to its two-wire simplicity, low pin count, and multi-master capability, catering to system-on-chip environments. Smartphones, wearables, and many automotive displays rely on I2C for low-noise, low-power communication between the controller and host processor. SPI holds steady in panel PCs and higher-resolution tablets where bandwidth requirements rise, while UART persists in legacy industrial terminals seeking minimal firmware updates.

USB emerges as the fastest-growing at a 9.2% CA,GR given its plug-and-play nature and high throughput that supports stylus data and hover sensing. ODMs targeting kiosks, medical carts, and detachable monitors appreciate the standard connector and host-agnostic enumeration process. White-box PC makers also favor USB touch due to the cost avoidance of additional bridge ICs. This interface flexibility widens application reach, adds volumes to the touch screen controllers market, and pressures vendors to supply multi-interface firmware capable of seamless field reconfiguration.

The Touch Screen Controllers Market Report is Segmented by Technology (Resistive, Capacitive, and More), Interface (I2C, SPI, USB, and UART), Touch Points (Single-Touch, and Multi-Touch), Display Size (Less Than 5 Inch, 5-10 Inch, and Above 10 Inch), End-User Industry (Consumer Electronics, Industrial and Manufacturing, Retail and POS Terminals, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific held 61.8% revenue in 2024, supported by dense component supply chains, skilled labor, and government incentives for semiconductor self-sufficiency. China hosts major controller IC fabs plus downstream module assemblers that feed local smartphone and appliance giants. Regional suppliers such as FocalTech continue to innovate with integrated display-and-touch solutions that meet automotive reliability goals focaltech-electronics.com. South Korea and Japan contribute leading OLED and oxide TFT expertise, fueling high-value controller sockets in flexible and foldable devices.

North America ranks second, driven by platform innovation in automotive electronics, medical imaging, and industrial automation. Silicon Valley design centers emphasize AI-enhanced signal processing that filters complex noise environments. Retail chains accelerate self-checkout installations, securing additional controller unit demand. Robust cybersecurity requirements in this region elevate interest in hardware-accelerated encryption embedded within touch controllers.

Europe follows closely and relies heavily on automotive production clusters in Germany, France, and Sweden. Stringent functional-safety and electromagnetic-compatibility norms lengthen design timelines yet create defendable niches for certified suppliers. EU-wide push toward Level-2 and Level-3 ADAS drives larger cockpit displays that utilize high-channel-count controllers, enriching application diversity in the touch screen controllers market.

The Middle East and Africa region posts the fastest 10.2% CAGR through 2030. Smart-city programs in Gulf economies order touch-enabled kiosks, digital signage, and payment terminals. Retail and hospitality segments adopt interactive systems that shorten service queues. Smaller domestic integrators procure controllers via global distributors, raising local design activity.

South America shows gradual expansion, with Brazil and Argentina upgrading banking ATMs and classroom technology. Currency volatility and tariff structures influence procurement cycles, yet growing smartphone penetration nourishes aftermarket demand for repair-grade touch modules. Collective regional progress broadens the geographic footprint of the touch screen controllers market, mitigating overreliance on Asia-based output.

- NXP Semiconductors

- Renesas Electronics Corporation

- Samsung Electronics Co. Ltd.

- Texas Instruments Incorporated

- Analog Devices Inc.

- STMicroelectronics

- Microchip Technology Inc.

- Cypress (Infineon Technologies AG)

- Synaptics Incorporated

- Goodix Technology Inc.

- FocalTech Systems Co. Ltd.

- MELFAS Co. Ltd.

- Elan Microelectronics Corp.

- Novatek Microelectronics Corp.

- Ilitek I-SFT Technology Inc.

- Silicon Labs

- Himax Technologies Inc.

- Semtech Corporation

- Broadcom Inc.

- PixArt Imaging Inc.

- ROHM Semiconductor

- AMS OSRAM AG

- Raydium Semiconductor Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Multi-Touch capacitive Adoption in Flexible OLED Smartphone Displays

- 4.2.2 In-Vehicle Infotainment Upgrades with Level-2 ADAS in Europe

- 4.2.3 Self-Checkout POS Proliferation amid North-American Labor Shortages

- 4.2.4 Hand-held Medical Imaging Devices Miniaturization

- 4.2.5 Industry 4.0 Rugged PCAP Panels Replacing Membrane Keypads in China

- 4.2.6 Touch-Enabled Smartwatch Shift Driving Low-Power 32-bit Controllers

- 4.3 Market Restraints

- 4.3.1 55 nm Mixed-Signal Wafer Supply-Chain Tightness

- 4.3.2 EMI/ESD Compliance Issues for Above 24-inch capacitive Automotive Displays

- 4.3.3 Controller-IP Litigation with Indian White-Box Tablet Makers

- 4.3.4 ASP Erosion from Panel-Maker Vertical Integration

- 4.4 Industry Ecosystem Analysis

- 4.5 Technological Outlook (Controller Architectures and Sensing Algorithms)

- 4.6 Regulatory Outlook (EMC and Automotive-Grade Standards)

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Technology

- 5.1.1 Resistive

- 5.1.2 capacitive (Projected and Surface)

- 5.1.3 Surface Acoustic Wave

- 5.1.4 Infrared

- 5.1.5 Optical Imaging

- 5.2 By Interface

- 5.2.1 I2C

- 5.2.2 SPI

- 5.2.3 USB

- 5.2.4 UART

- 5.3 By Touch Points

- 5.3.1 Single-Touch

- 5.3.2 Multi-Touch

- 5.4 By Display Size

- 5.4.1 Less than 5 Inch

- 5.4.2 5 - 10 Inch

- 5.4.3 Above 10 Inch

- 5.5 By End-user Industry

- 5.5.1 Consumer Electronics

- 5.5.2 Industrial and Manufacturing

- 5.5.3 Healthcare and Medical Devices

- 5.5.4 Retail and POS Terminals

- 5.5.5 Automotive

- 5.5.6 Banking and Financial Kiosks

- 5.5.7 Others (Aviation, Education)

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Nordics (Denmark, Sweden, Norway, Finland)

- 5.6.2.7 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 South Korea

- 5.6.3.4 India

- 5.6.3.5 Southeast Asia

- 5.6.3.6 Australia

- 5.6.3.7 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle East

- 5.6.5.1 Gulf Cooperation Council Countries

- 5.6.5.2 Turkey

- 5.6.5.3 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 NXP Semiconductors

- 6.4.2 Renesas Electronics Corporation

- 6.4.3 Samsung Electronics Co. Ltd.

- 6.4.4 Texas Instruments Incorporated

- 6.4.5 Analog Devices Inc.

- 6.4.6 STMicroelectronics

- 6.4.7 Microchip Technology Inc.

- 6.4.8 Cypress (Infineon Technologies AG)

- 6.4.9 Synaptics Incorporated

- 6.4.10 Goodix Technology Inc.

- 6.4.11 FocalTech Systems Co. Ltd.

- 6.4.12 MELFAS Co. Ltd.

- 6.4.13 Elan Microelectronics Corp.

- 6.4.14 Novatek Microelectronics Corp.

- 6.4.15 Ilitek I-SFT Technology Inc.

- 6.4.16 Silicon Labs

- 6.4.17 Himax Technologies Inc.

- 6.4.18 Semtech Corporation

- 6.4.19 Broadcom Inc.

- 6.4.20 PixArt Imaging Inc.

- 6.4.21 ROHM Semiconductor

- 6.4.22 AMS OSRAM AG

- 6.4.23 Raydium Semiconductor Corp.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

全球多點觸控螢幕市場(按技術、應用、最終用戶和麵板尺寸)—2025-2032 年全球預測

全球多點觸控螢幕市場(按技術、應用、最終用戶和麵板尺寸)—2025-2032 年全球預測 2025年全球零售觸控螢幕顯示器市場報告2025年觸控螢幕控制器全球市場報告

2025年全球零售觸控螢幕顯示器市場報告2025年觸控螢幕控制器全球市場報告 全球非接觸式感測市場

全球非接觸式感測市場 2025 年至 2033 年多點觸控螢幕市場規模、佔有率、趨勢及預測(依產品、技術、應用及地區)

2025 年至 2033 年多點觸控螢幕市場規模、佔有率、趨勢及預測(依產品、技術、應用及地區) 2025-2029年全球筆記型電腦觸控螢幕市場

2025-2029年全球筆記型電腦觸控螢幕市場 2025-2029年全球零售觸控螢幕顯示器市場汽車觸控螢幕控制系統市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

2025-2029年全球零售觸控螢幕顯示器市場汽車觸控螢幕控制系統市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測 全球汽車觸控螢幕控制系統市場(2025-2029)

全球汽車觸控螢幕控制系統市場(2025-2029) 亞太地區觸控螢幕控制器:市場佔有率分析、產業趨勢、成長預測(2025-2030)

亞太地區觸控螢幕控制器:市場佔有率分析、產業趨勢、成長預測(2025-2030)