|

市場調查報告書

商品編碼

1849869

汽車塑膠:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)Automotive Plastics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

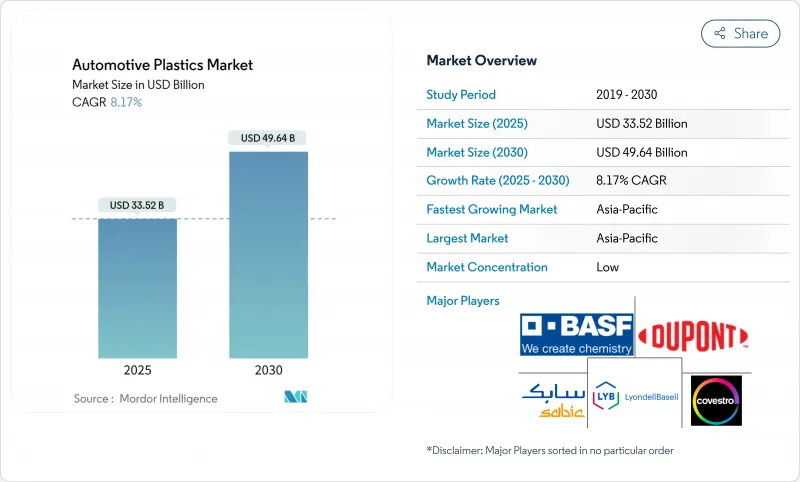

據估計,2025 年汽車塑膠市場價值為 335.2 億美元,預計到 2030 年將達到 496.4 億美元,預測期(2025-2030 年)複合年成長率為 8.17%。

這一穩步成長反映了汽車製造商為平衡嚴格的排放氣體法規和性能目標而轉向輕量化材料。先進聚合物解決方案的加速應用,尤其是在電動車 (EV) 平台上的應用,正推動汽車塑膠市場以遠超過以往的速度成長。亞太地區佔全球需求的近一半,也是複合材料市場成長最快的地區。同時,聚丙烯 (PP) 在關鍵汽車系統中繼續保持著性價比的標竿地位。

全球汽車塑膠市場趨勢與洞察

電動車對輕量材料的需求日益成長

續航焦慮和電池組成本使得輕量化成為電動車工程的核心。如今,電動車中聚丙烯(PP)複合材料的使用量遠高於同類內燃機汽車,這主要是因為減輕重量可以直接提高續航里程,而無需改變電池尺寸。除了儀錶面板和裝飾件外,高介電常數聚丙烯和先進的聚醯胺材料也擴大用於結構外殼和高壓匯流排。電動車專用平台使設計師擺脫了傳統金屬連接點的束縛,從而能夠將更多塑膠零件整合到車身結構和溫度控管通道中。

碳排放法規加速聚丙烯保險桿的採用

歐洲和北美的車隊平均排放氣體法規對二氧化碳排放超標處以重罰。因此,汽車製造商正尋求「快速見效」的措施,例如將金屬加固保險桿更換為全聚丙烯(PP)保險桿,這樣既能顯著減輕重量,又能降低系統成本。產業生命週期評估始終表明,考慮到使用過程中的燃油節省,PP保險桿的碳足跡比鋼或鋁製保險桿更小。

氣味和易燃性會延緩生物基聚醯胺的OEM認證。

生物基聚醯胺有望實現從原料生產到最終交付的全過程減排,但殘留氣味和不穩定的燃燒性能使其難以獲得駕駛室和引擎室的認證。針對纖維素纖維增強生物基聚醯胺的學術研究發現,由於纖維分散性問題,其機械性質有較大差異。產業組織正在向監管機構請願,希望延長檢驗週期,以便材料供應商能夠對其配方進行微調。

細分市場分析

由於聚丙烯在成本、加工性能和物理性能方面具有良好的平衡性,預計到2024年,其在汽車塑膠市場將佔據34.18%的佔有率。聚丙烯的主要應用領域包括內部裝潢建材、車門飾板和中央控制台,而玻璃纖維增強型聚丙烯也用於半結構性座椅支架和後擋板。

到2030年,隨著高溫電動動力傳動系統對隔熱和絕緣性能要求的提高,聚醯胺的年複合成長率將達到8.87%。 PA66和部分芳香族PA6/6T共混物正在取代電池冷板組件、逆變器外殼和渦輪增壓器風道中的金屬支架。生物基聚醯胺目前尚未成為主流,但一旦克服了氣味和阻燃方面的障礙,它們將吸引那些尋求範圍3碳減排的原始設備製造商(OEM)。

到2024年,內裝塑膠將佔汽車塑膠市場規模的32.97%,這主要得益於對觸感柔軟的儀表板、環境燈門板以及一體成型顯示器的需求。觸感塗層和雷射蝕刻圖案則依賴特殊的叢集 、ABS和PC/PMMA共混物,進一步強化了塑膠在體驗式設計中的重要作用。

雖然引擎室內零件的絕對體積較小,但其年成長率高達 8.98%。隨著電氣化架構整合更多電子元件並需要更複雜的冷卻通道,耐熱的 PA、PPS 和 PBT 材料正在取代晶粒鋁,用於製造電子馬達冷卻套和高壓匯流排罩。

區域分析

到2024年,亞太地區將佔據全球汽車塑膠市場48.25%的佔有率,並在2030年之前保持9.82%的最高複合年成長率。中國大規模推廣電動車,得益於與電池製造商的合作以及政府的激勵措施,正推動PP、PA和PBT價值鏈上聚合物產能的擴張。印度乘用車產量預計將實現兩位數成長,這將促使當地投資建造複合材料生產中心,以降低對進口的依賴。韓國和日本正在改進用於抗衝擊外飾板的超高分子量聚合物,進一步鞏固了創新和產能成長的良性循環。

北美呈現出成熟又充滿創新活力的市場格局。為了滿足日益嚴格的企業平均燃油經濟性(CAFE)標準,汽車製造商(OEM)正在推廣多材料架構,以最大限度地利用塑膠材料製造尾門、電池組和高級駕駛輔助感測器外殼。美國也在樹脂供應商和一級模塑商之間率先建立閉合迴路回收夥伴關係,支持該地區的循環經濟目標。

在高階市場和嚴格的法律規範的推動下,歐洲市場對再生塑膠的需求依然強勁。建議的乘用車25%再生材料含量標準將促進相容劑添加劑和除臭系統的研究與開發,從而提升消費後再生樹脂的性能。德國在纖維增強聚醯胺(PA)橫樑技術的推廣應用方面處於領先地位,而法國和英國則透過公共資金資助生物聚合物試點生產線。然而,由於能源成本波動,該地區面臨利潤壓力,因此提高材料效率已成為一項戰略要務。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 電動車對輕量化材料的需求日益成長

- 碳排放罰款加速聚丙烯保險桿的普及

- 轉向採用射出成型成型混合材料的模組化前端載體(MEC)

- 汽車產業對靈活且經濟高效的工程材料的需求不斷成長

- 全球汽車產業穩定擴張

- 市場限制

- 氣味和易燃性會延緩生物基聚醯胺的OEM認證。

- 高昂的材料和加工成本

- 汽車產業替代材料的競爭日益加劇

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 材料

- 聚丙烯(PP)

- 聚氨酯(PU)

- 聚氯乙烯(PVC)

- 聚乙烯(PE)

- 丙烯腈丁二烯苯乙烯(ABS)

- 聚醯胺(PA)

- 聚碳酸酯(PC)

- 其他成分

- 透過使用

- 外部的

- 內部的

- 引擎蓋下

- 其他用途

- 按車輛類型

- 傳統車輛

- 電動車

- 按原料

- 原生塑膠

- 回收塑膠

- 生物基塑膠

- 按地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- Arkema

- Asahi Kasei Advance Corporation

- BASF SE

- Borealis AG

- Braskem

- Celanese Corporation

- Covestro AG

- Daicel Corporation

- Dow

- dsm-firmenich

- DuPont

- Evonik Industries AG

- Exxon Mobil Corporation

- INEOS

- LANXESS

- LG Chem

- LyondellBasell Industries Holdings BV

- Mitsui Chemicals Inc.

- SABIC

- TEIJIN LIMITED

第7章 市場機會與未來展望

The Automotive Plastics Market size is estimated at USD 33.52 billion in 2025, and is expected to reach USD 49.64 billion by 2030, at a CAGR of 8.17% during the forecast period (2025-2030).

The steady uptick reflects automakers' pivot toward lighter materials to reconcile strict emission rules with performance targets. Accelerated adoption of advanced polymer solutions, especially in electric-vehicle (EV) platforms, is pushing the automotive plastics market well ahead of its historical pace. Asia-Pacific commands almost half of global demand and is compounding at the fastest regional rate, while polypropylene (PP) continues to set the benchmark for cost-to-performance across major vehicle systems.

Global Automotive Plastics Market Trends and Insights

Increasing demand for lightweight materials in electric vehicles

Range anxiety and battery-pack cost keep lightweighting at the center of EV engineering. PP compounds now appear in larger volumes per EV than in comparable internal-combustion cars, largely because lower mass converts directly into added driving range without resizing the battery. Beyond instrument panels and trims, high-dielectric PP and advanced polyamide grades are entering structural housings and high-voltage busbars. Dedicated EV platforms free designers from legacy metal hard-points, allowing more plastic integration into body structures and thermal-management channels.

Carbon-emission penalties accelerating polypropylene bumper adoption

Fleet-average emissions standards in Europe and North America impose significant financial penalties for excess CO2. Automakers therefore target "quick wins" such as switching from metal-reinforced to fully PP bumpers, achieving meaningful mass savings at lower system cost. Industry life-cycle assessments consistently show PP bumpers delivering a smaller carbon footprint than steel or aluminum alternatives once use-phase fuel savings are incorporated.

OEM qualification delays for Bio-PA due to odor & flammability

Bio-sourced polyamides promise lower cradle-to-gate emissions, yet residual odor and inconsistent ignition behavior complicate cabin and under-hood approvals. Academic work on cellulosic-fiber-reinforced Bio-PA confirms wide variability in mechanical properties stemming from fiber dispersion challenges. Industry groups have petitioned regulators to allow longer validation cycles so material suppliers can fine-tune formulations.

Other drivers and restraints analyzed in the detailed report include:

- Shift to Modular Front-End Carriers (MECs) via injection-molded hybrids

- Growing demand for flexible and cost-efficient design materials

- High materials and processing cost

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polypropylene held a commanding 34.18% automotive plastics market share in 2024 on the back of balanced cost, processability and property retention. Interior fascia, door trims and center consoles dominate PP usage, but glass-fiber-reinforced grades now extend into semi-structural seat carriers and tailgates.

Polyamides are climbing an 8.87% CAGR trajectory through 2030 as high-temperature electrified powertrains demand better thermal and dielectric insulation. PA66 and partially aromatic PA6/6T blends displace metal brackets in battery-cold-plate assemblies, inverter housings and turbo-air ducts. Bio-based PA grades, while not yet mainstream, attract OEMs seeking Scope-3 carbon reductions once odor and flame-spread hurdles are cleared.

Interior accounted for 32.97% of the automotive plastics market size in 2024, buoyed by demand for soft-touch dashboards, ambient-lit door panels, and integrating display clusters into single multi-shot molded units. Haptic coatings and laser-etch graphics depend on specialty PP, ABS, and PC/PMMA blends, reinforcing plastics' role in experiential design.

Under-bonnet components, though smaller in absolute volume, are growing at 8.98% per year. Electrified architectures pack more electronics and require intricate cooling channels; thus, heat-stabilized PA, PPS, and PBT replace die-cast aluminum for e-motor cooling jackets and high-voltage busbar covers.

The Automotive Plastics Market Report Segments the Industry by Material (Polypropylene (PP), Polyurethane (PU), Polyvinyl Chloride (PVC), and More), Application (Exterior, Interior, and More), Vehicle Type (Conventional/Traditional Vehicles, and Electric Vehicles), Source (Virgin Plastic, Recycled Plastic, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa).

Geography Analysis

Asia-Pacific dominated the automotive plastics market with a 48.25% stake in 2024 and mirrors the highest regional CAGR at 9.82% to 2030. China's large-scale EV rollout, supported by battery-maker alliances and state incentives, is spurring polymer capacity expansions across PP, PA and PBT value chains. India records double-digit growth in passenger-car output, triggering investments in local compounding hubs to curb import reliance. South Korea and Japan refine ultra-high-molecular-weight grades for impact-resistant exterior panels, further embedding a virtuous innovation-capacity loop.

North America presents a mature yet inventive landscape. Compliance with tightening Corporate Average Fuel Economy standards pushes OEMs toward multi-material architectures that maximize plastics in liftgates, battery packs and advanced driver-assistance sensor housings. The United States also hosts pioneering work in closed-loop recycling partnerships between resin suppliers and tier-one molders, supporting local circular-economy targets.

Europe maintains sizeable demand anchored by premium vehicle segments and aggressive regulatory frameworks. The proposed 25% recycled-content threshold in passenger cars catalyzes R&D around compatibilizer additives and de-odorizing systems that elevate post-consumer resin performance. Germany leads technology deployments in fiber-reinforced PA cross-members, while France and the United Kingdom channel public funding toward biopolymer pilot lines. The region nevertheless faces margin pressures from energy-cost volatility, making material efficiency a strategic imperative.

- Arkema

- Asahi Kasei Advance Corporation

- BASF SE

- Borealis AG

- Braskem

- Celanese Corporation

- Covestro AG

- Daicel Corporation

- Dow

- dsm-firmenich

- DuPont

- Evonik Industries AG

- Exxon Mobil Corporation

- INEOS

- LANXESS

- LG Chem

- LyondellBasell Industries Holdings B.V.

- Mitsui Chemicals Inc.

- SABIC

- TEIJIN LIMITED

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Demand for Lighweight Materials in Electric Vehicles

- 4.2.2 Carbon Emission Penalties Accelerating Polypropylene Bumper Adoption

- 4.2.3 Shift to Modular Front-End Carriers (MECs) via Injection-Molded Hybrids

- 4.2.4 Growing Demand for Flexible and Cost Efficient Design Materials in Automotive

- 4.2.5 Consistent Expansion of the Global Automotive Sector

- 4.3 Market Restraints

- 4.3.1 OEM Qualification Delays for Bio-PA due to Odor and Flammability

- 4.3.2 High Materials and Processing Cost

- 4.3.3 Incraesing Competion from Alternative Materials in Automotive

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Material

- 5.1.1 Polypropylene (PP)

- 5.1.2 Polyurethane (PU)

- 5.1.3 Polyvinyl Chloride (PVC)

- 5.1.4 Polyethylene (PE)

- 5.1.5 Acrylonitrile Butadiene Styrene (ABS)

- 5.1.6 Polyamides (PA)

- 5.1.7 Polycarbonate (PC)

- 5.1.8 Other Materials

- 5.2 By Application

- 5.2.1 Exterior

- 5.2.2 Interior

- 5.2.3 Under Bonnet

- 5.2.4 Other Applications

- 5.3 Vehicle Type

- 5.3.1 Conventional/Traditional Vehicles

- 5.3.2 Electic Vehicles

- 5.4 Source

- 5.4.1 Virgin Plastic

- 5.4.2 Recycled Plastic

- 5.4.3 Bio-based Plastic

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 Japan

- 5.5.1.3 India

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles {(includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)}

- 6.4.1 Arkema

- 6.4.2 Asahi Kasei Advance Corporation

- 6.4.3 BASF SE

- 6.4.4 Borealis AG

- 6.4.5 Braskem

- 6.4.6 Celanese Corporation

- 6.4.7 Covestro AG

- 6.4.8 Daicel Corporation

- 6.4.9 Dow

- 6.4.10 dsm-firmenich

- 6.4.11 DuPont

- 6.4.12 Evonik Industries AG

- 6.4.13 Exxon Mobil Corporation

- 6.4.14 INEOS

- 6.4.15 LANXESS

- 6.4.16 LG Chem

- 6.4.17 LyondellBasell Industries Holdings B.V.

- 6.4.18 Mitsui Chemicals Inc.

- 6.4.19 SABIC

- 6.4.20 TEIJIN LIMITED

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

- 7.2 Technological Developments in Electric Vehicles

汽車塑膠市場(按應用、材料類型、工藝類型、車輛類型和最終用途)—2025-2032 年全球預測汽車外飾塑膠市場按材料類型、應用、車輛類型和最終用戶分類-2025-2032年全球預測

汽車塑膠市場(按應用、材料類型、工藝類型、車輛類型和最終用途)—2025-2032 年全球預測汽車外飾塑膠市場按材料類型、應用、車輛類型和最終用戶分類-2025-2032年全球預測 2025年全球汽車塑膠市場報告2025年全球汽車外飾塑膠市場報告

2025年全球汽車塑膠市場報告2025年全球汽車外飾塑膠市場報告 全球汽車塑膠市場,2024-2031年

全球汽車塑膠市場,2024-2031年 汽車裝飾的全球市場:材料·產品類型·裝飾件類型·車輛類型·車輛級·車輛推動區分·銷售頻道·各地區 (~2032年)

汽車裝飾的全球市場:材料·產品類型·裝飾件類型·車輛類型·車輛級·車輛推動區分·銷售頻道·各地區 (~2032年) 玻璃纖維增強基材市場,按材料類型、應用、基材類型、最終用途產業、國家和地區分類-2025 年至 2032 年全球產業分析、市場規模、市場佔有率及預測

玻璃纖維增強基材市場,按材料類型、應用、基材類型、最終用途產業、國家和地區分類-2025 年至 2032 年全球產業分析、市場規模、市場佔有率及預測 全球汽車外觀裝飾市場汽車塑膠複合材料市場(按產品、應用、最終用戶、國家和地區)-2025 年至 2032 年全球產業分析、市場規模、市場佔有率及預測玻璃強化基板市場規模、佔有率及趨勢分析報告:依基板類型、應用、厚度、最終用途產業、地區和細分市場進行預測,2025 年至 2033 年

全球汽車外觀裝飾市場汽車塑膠複合材料市場(按產品、應用、最終用戶、國家和地區)-2025 年至 2032 年全球產業分析、市場規模、市場佔有率及預測玻璃強化基板市場規模、佔有率及趨勢分析報告:依基板類型、應用、厚度、最終用途產業、地區和細分市場進行預測,2025 年至 2033 年