|

市場調查報告書

商品編碼

1849862

蠟:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)Wax - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

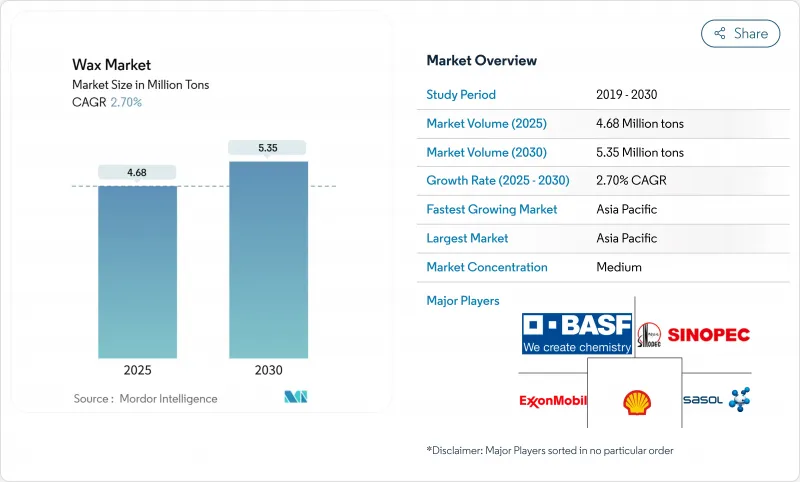

預計到 2025 年,蠟市場規模將達到 468 萬噸,到 2030 年將達到 535 萬噸,在預測期(2025-2030 年)內,複合年成長率將達到 2.70%。

蠟市場正從以石油為主導的供應模式轉型為包含天然蠟和高性能合成蠟在內的多元化混合供應模式。更清潔的配方、快速發展的電子商務物流以及新型乙烷裂解裝置生產的成本優勢聚乙烯蠟,為生產商開闢了新的成長途徑,即便成熟的蠟燭、包裝和橡膠應用市場成長趨於平緩。亞太地區的領先地位得益於其一體化的煉油能力、龐大的消費品產業以及全球成長最快的線上零售通路。在歐洲,對多環芳烴(PAHs)和一次性塑膠的監管持續推動對植物來源替代品和食品被覆劑的需求。在北美,頁岩氣衍生的乙烷保持著良好的生產經濟效益,使區域性企業能夠客製化針對塗料、複合材料和熱熔膠等應用領域的蠟品等級,並開拓出口市場。

全球蠟市場趨勢與洞察

亞太地區電子商務的蓬勃發展推動了對熱熔膠級FT蠟的需求。

中國、印度和東南亞地區線上零售的爆炸性成長推動了對費托(FT)改性熱熔膠的需求,增強了紙箱密封性和標籤黏合力。這些FT改質熱熔膠具有更高的熔點和內聚強度,使包裝能夠在潮濕的季風地區和冷鏈運輸中保持密封。包裝加工商報告稱,使用FT蠟添加劑配製的包裝可減少高達35%的運輸廢棄物率。因此,蠟市場受益於小包裹的成長和高性能混合膠的高價位。提供區域倉庫庫存的供應商也看到了前置作業時間的縮短以及來自尋求堅固耐用、防潮包裝解決方案的物流網路的重複業務。

歐洲潔淨標示化妝品加速向植物來源巴西棕櫚蠟和蜂蠟轉型

歐洲美妝品牌正迅速轉向成分透明化標註,鼓勵負責人用巴西棕櫚蠟、小燭樹蠟和蜂蠟替代合成蠟和石蠟。這些生物基原料能為唇部護理產品、潤唇膏和潤膚棒提供所需的天然光澤、成膜性和潤膚特性。一項2025年的研究表明,以巴西棕櫚蠟為基礎的、結構合理的純素唇膏,其硬度、顯色度和熔化穩定性可與蜂蠟媲美。在巴西和東南亞擁有可追溯供應鏈的蠟製品市場參與企業維持著價格溢價,而歐洲的契約製造則尋求更短的前置作業時間。

歐洲加強了對石蠟玩具和化妝品中多環芳烴的限制(REACH法規)。

歐洲REACH法規更新後的多環芳烴(PAH)基準值現已適用於玩具和免沖洗保養品中使用的石蠟。合規認證增加了成本和複雜性,不合規的進口產品將面臨海關扣押和零售商下架的風險。跨國品牌所有者僅對上游來源明確的蠟品進行預認證,這促使買家轉向合成費托蠟和植物來源替代品。因此,在精煉廠全面完成技術升級之前,傳統石蠟市場的利潤率將會受到壓縮。

細分市場分析

預計到2024年,石蠟和礦物蠟將保持58%的蠟市場佔有率,這主要得益於其成本競爭力以及在蠟燭、板材施膠和橡膠化合物等領域的廣泛應用。然而,以巴西棕櫚蠟、小燭樹蠟和蜂蠟為代表的天然蠟市場預計將以3.43%的複合年成長率成長,凸顯了消費者對可再生原料的顯著轉向。可追溯來源、低多環芳烴含量和純素產品的需求不斷成長,使得巴西和墨西哥的認證人工林成為重要的策略資產。以費托合成蠟和聚乙烯蠟為代表的合成蠟則佔據了創新優勢,能夠為對高溫和高濕環境敏感的應用提供客製化的熔融特性和硬度等級。

高階潔淨標示化妝品、可食用水果和蔬菜被覆劑和特殊包裝被覆劑是推動天然蠟市場成長的主要動力。相反,對成本敏感的領域,例如瓦楞紙箱尺寸,仍然更青睞石蠟混合物。在預測期內,氣轉液(GTL)裝置的產能擴張可望緩解合成蠟的價格波動,而無溶劑萃取的新技術旨在提高植物性蠟的產量。生產商與歐洲美容品牌之間的策略性承購協議將確保供應,並進一步推動天然替代品融入蠟市場。

到2024年,以固態蠟為燃料基質和香料載體的蠟燭將佔據蠟市場60%的佔有率。這種長期主導地位在注重氛圍產品的成熟經濟體以及家居裝飾支出不斷成長的新興市場中得以維持。然而,化妝品將以3.65%的複合年成長率實現最高成長,因為負責人越來越依賴蠟來構建唇部、頭髮和身體護理產品的結構、提升顯色度和改善膚感。直接面對消費者的品牌正在選擇符合其清潔美容定位的高純度或生物基蠟,並加速小批量產品的推出。

用於電商包裝的熱熔膠、紙箱的阻隔被覆劑以及PVC型材的擠出潤滑劑的應用範圍正在不斷擴大。可食用被覆劑正在取代用於水果和乳酪的石油化學包裝,這不僅體現了其與永續性的協同效應,也突顯了蠟的多功能性。研發工作將蠟的市場配方定位在功能性和循環性的交匯點,使品牌所有者能夠共同開發特定應用的配方,並在創紀錄的時間內擴大試點生產規模。

區域分析

預計亞太地區將在2024年佔據45%的蠟市場佔有率,並在2030年前維持3.2%的複合年成長率,成為成長最快的地區。中國龐大的蠟燭、包裝和個人護理叢集將支撐市場需求,而印度不斷壯大的中產階級正在推動化妝品和家居香氛消費的成長。東協物流樞紐將促進熱熔膠的應用,使蠟市場成長與小包裹量直接掛鉤。印尼和馬來西亞政府對下游石化產業的激勵措施將繼續吸引對合成蠟裝置的投資,從而實現在地化供應並縮短從運輸到商店的週期。

北美蠟市場格局平衡,既有成熟的蠟燭和板材應用,也有特種聚乙烯蠟領域的創新發展。低成本的頁岩乙烷為新的裂解裝置提供原料,使美國和加拿大生產商能夠擴大出口,特別是對拉丁美洲和歐洲的出口。汽車輕量化、粉末塗料和3D列印絲材添加劑的應用,為精細分級餾合成纖維開闢了下一代應用領域。美國墨加協定(USMCA)框架下的跨國物流確保了上游中間體和成品蠟混合物的免稅流通。

歐洲蠟市場在極其嚴格的法規環境下運作,推動消費轉向低多環芳烴(PAH)含量的石蠟、全合成費托蠟和經認證的天然蠟。德國和荷蘭擁有用於高階化妝品的精煉中心,而義大利的水果出口產業正在擴大食用巴西棕櫚蠟塗層的試驗規模,以滿足零售保存期限規定。一次性塑膠的禁令正在使塗有生物蠟阻隔層的紙質包裝重獲新生,並為乳液配方創造了新的市場需求。研究表明,塗蠟的農產品包裝有助於實現歐盟從農場到餐桌的目標,並將零售環節的食物浪費減少兩位數百分比。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 亞太地區電子商務的蓬勃發展推動了對熱熔膠級FT蠟的需求。

- 歐洲潔淨標示化妝品加速向植物來源巴西棕櫚蠟和蜂蠟轉型

- 北美乙烷裂解裝置擴建降低了聚乙烯蠟的生產成本

- 亞太地區個人護理產業的成長

- 食品級蠟:歐洲生鮮食品供應鏈中塑膠薄膜的替代塗層

- 市場限制

- REACH法規對歐洲玩具和化妝品用增強型石蠟中的多環芳烴含量限制

- 原油和天然氣價格的波動會影響合成油和石蠟油的利潤率。

- 純素化妝品趨勢:用油性乳化劑代替蜂蠟

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模及成長預測(銷售)

- 按類型

- 石蠟和礦物蠟

- 合成蠟

- 天然蠟

- 透過使用

- 蠟燭製作

- 包裹

- 化妝品

- 膠水

- 橡皮

- 其他用途

- 按年級

- 食品級

- 工業級

- 化妝品和製藥業

- 按形式

- 固體的

- 粉末

- 乳液和液體

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- ASEAN

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- BASF SE

- BP plc

- Calumet, Inc.,

- CALWAX

- China Petrochemical Corporation

- CLARIANT

- Evonik Industries AG

- Exxon Mobil Corporation

- H&R GROUP

- Honeywell International Inc.

- Ilumina Wax doo

- Koster Keunen

- Moeve

- NIPPON SEIRO CO., LTD.

- Petrobras

- Petro-Canada Lubricants Inc.

- Sasol Ltd.

- Shell plc

- Strahl & Pitsch LLC

- The International Group, Inc.

第7章 市場機會與未來展望

The Wax Market size is estimated at 4.68 Million tons in 2025, and is expected to reach 5.35 Million tons by 2030, at a CAGR of 2.70% during the forecast period (2025-2030).

The Wax market is moving from a petroleum-centric supply base toward a wider mix that includes natural and high-performance synthetic grades. Cleaner formulations, fast-moving e-commerce logistics, and cost-advantaged polyethylene wax from new ethane crackers are giving producers fresh avenues for growth even as mature candle, packaging, and rubber uses level off. Asia-Pacific's dominance rests on its integrated refining capacity, large consumer goods sector, and the world's fastest-growing online retail channel. Europe's regulations on polycyclic aromatic hydrocarbons (PAHs) and single-use plastics continue to funnel demand toward plant-based alternatives and food-grade coatings. In North America, shale-derived ethane keeps production economics favorable, allowing regional players to penetrate export markets with tailored grades that target coatings, composites, and hot-melt adhesives.

Global Wax Market Trends and Insights

Asia-Pacific E-commerce Boom Driving Hot-Melt Adhesive-Grade FT Waxes Demand

Explosive online retail growth across China, India, and Southeast Asia requires stronger carton sealing and label adhesion, which in turn raises demand for Fischer-Tropsch (FT) wax-modified hot-melt adhesives. These FT grades deliver higher melting points and cohesive strength, containing packages in humid monsoon zones and cold-chain routes alike. Packaging converters report up to 35% fewer shipment failures when formulations include FT wax additives. The Wax market therefore benefits from both higher volume of parcels and premium-priced performance blends. Suppliers that offer regionally warehoused inventories shorten lead times and secure repeat contracts from logistics networks seeking robust, moisture-resistant packaging solutions.

Clean-Label Cosmetics in Europe Accelerating Shift to Plant-Based Carnauba & Beeswax

European beauty brands have moved rapidly to transparent ingredient statements, pushing formulators to swap synthetic and paraffin waxes for carnauba, candelilla, and beeswax. These bio-based options supply natural gloss, film-forming, and emollient properties required in lip care, balms, and skin sticks. A 2025 study shows properly structured vegan lipsticks based on carnauba wax can match hardness, pay-off, and melting stability achieved with beeswax. As retailers widen eco-certified shelf space, Wax market participants that secure traceable supply chains in Brazil and Southeast Asia hold a pricing premium, while contract manufacturers in Europe seek shorter lead times for boutique batches.

REACH PAH Limits Tightening on Paraffin Wax in Europe Toys & Cosmetics

Europe's updated PAH thresholds under REACH now apply to paraffin wax used in toys and leave-on skin products, compelling refiners to invest in deep-hydrotreatment or source alternative feedstock. Compliance certificates drive up cost and complexity, while non-compliant imports face customs seizures and retailer delistings. Multinational brand owners pre-qualify only wax grades with transparent upstream provenance, encouraging buyers to shift toward synthetic Fischer-Tropsch or plant-based substitutes. The Wax market therefore confronts margin compression in conventional paraffin segments until refiners fully execute technology upgrades.

Other drivers and restraints analyzed in the detailed report include:

- North American Ethane Cracker Expansions Lowering PE Wax Production Costs

- Growing Personal Care Industry in the Asia-Pacific Region

- Vegan Cosmetics Trend Substituting Beeswax with Oleochemical Emulsifiers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Paraffin and mineral waxes retained a 58% Wax market share in 2024, buoyed by their broad availability and cost competitiveness across candles, board sizing, and rubber compounding. Yet the natural wax segment, anchored by carnauba, candelilla, and beeswax, is set to grow at a 3.43% CAGR, highlighting a decisive consumer tilt toward renewable ingredients. Heightened demand for traceable supply, low-PAH content, and vegan compliance positions certified plantations in Brazil and Mexico as strategic assets. Synthetic waxes, principally Fischer-Tropsch and polyethylene variants, occupy an innovation sweet spot, offering custom melting profiles and hardness levels that address high-temperature or moisture-sensitive applications.

Premium clean-label cosmetics, edible produce coatings, and specialty packaging coatings drive the strongest natural wax pull-through. Conversely, cost-sensitive sectors such as corrugated box sizing still prefer paraffin blends. Over the forecast window, capacity expansions in gas-to-liquids (GTL) facilities are expected to temper price volatility for synthetic grades, while new solvent-free extraction technologies aim to raise yields in plant-based operations. Strategic offtake agreements between growers and European beauty houses lock in supply assurance, embedding natural alternatives more firmly into the Wax market.

Candles commanded 60% of the Wax market size in 2024 by virtue of their fundamental dependence on solid wax as both fuel matrix and fragrance carrier. This long-standing dominance persists in mature economies that value ambience products and in emerging markets experiencing rising home decor spending. Nonetheless, cosmetics exhibits the highest 3.65% CAGR as formulators exploit waxes for structure, payoff, and skin feel in lip, hair, and body products. Direct-to-consumer brands accelerate small-batch launches, selecting high-purity or bio-origin wax grades that align with clean beauty positioning.

Hot-melt adhesives for e-commerce packaging, barrier coatings for cartons, and extrusion lubricants for PVC profiles represent rising application niches. Edible coatings demonstrate sustainability synergy by replacing petrochemical wraps on fruit and cheese, underscoring wax versatility. Research placing Wax market formulations at the intersection of functionality and circularity encourages brand owners to co-develop application-specific blends, bringing pilot runs to scale in record timelines.

The Wax Market Report Segments the Industry by Type (Paraffin and Mineral Wax, Synthetic Wax, and More), Application (Candle Making, Packaging, Cosmetics, and More), Grade (Food Grade, Industrial Grade, and More), Form (Solid, Powdered, Emulsions and Liquids) and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (tons).

Geography Analysis

Asia-Pacific secured 45% of the Wax market share in 2024 and is forecast to record the fastest 3.2% CAGR through 2030. China anchors demand with its vast candle, packaging, and personal care clusters, while India's surging middle class elevates consumption across cosmetics and home fragrance. ASEAN logistics hubs propel hot-melt adhesive usage, linking Wax market growth directly to parcel volumes. Government incentives for downstream petrochemicals in Indonesia and Malaysia continue to attract investment in synthetic wax units, delivering localized supply and shortening ship-to-shelf cycles.

North America maintains a balanced Wax market, coupling mature candle and board applications with innovative strides in specialized polyethylene waxes. Low-cost shale ethane feeds new cracker capacity, positioning U.S. and Canadian producers for export gains, especially to Latin America and Europe. Automotive lightweighting, powder coatings, and 3D-printing filament additives open next-generation uses for finely fractionated synthetic wax streams. Cross-border logistics within the United States-Mexico-Canada Agreement (USMCA) ensure duty-free flow of upstream intermediates and finished wax blends.

Europe's Wax market operates under the strictest regulatory environment, steering consumption toward low-PAH paraffin, fully synthetic Fischer-Tropsch, and certified natural grades. Germany and the Netherlands host refinement hubs that feed high-end cosmetics, while Italy's fruit-export sector scales trials of edible carnauba coatings to meet retailer shelf-life mandates. Single-use plastic bans energize paper-based packaging coated with bio-wax barriers, opening demand pockets for emulsified formulations. Research indicates that wax-coated produce packs cut retail food waste by double-digit percentages, supporting EU Farm-to-Fork objectives.

- BASF SE

- BP p.l.c.

- Calumet, Inc.,

- CALWAX

- China Petrochemical Corporation

- CLARIANT

- Evonik Industries AG

- Exxon Mobil Corporation

- H&R GROUP

- Honeywell International Inc.

- Ilumina Wax d.o.o.

- Koster Keunen

- Moeve

- NIPPON SEIRO CO., LTD.

- Petrobras

- Petro-Canada Lubricants Inc.

- Sasol Ltd.

- Shell plc

- Strahl & Pitsch LLC

- The International Group, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Asia-Pacific E-commerce Boom Driving Hot-Melt Adhesive-Grade FT Waxes Demand

- 4.2.2 Clean-Label Cosmetics in Europe Accelerating Shift to Plant-Based Carnauba and Beeswax

- 4.2.3 North American Ethane Cracker Expansions Lowering PE Wax Production Costs

- 4.2.4 Growing Personal Care Industry in the Asia-Pacific Region

- 4.2.5 Food-Grade Wax Coatings Replacing Plastic Films in Europe Fresh Produce Supply Chain

- 4.3 Market Restraints

- 4.3.1 REACH PAH Limits Tightening on Paraffin Wax in Europe Toys and Cosmetics

- 4.3.2 Crude and Gas Price Volatility Impacting Synthetic and Paraffin Wax Margins in APAC

- 4.3.3 Vegan Cosmetics Trend Substituting Beeswax with Oleochemical Emulsifiers

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Type

- 5.1.1 Paraffin and Mineral Wax

- 5.1.2 Synthetic Wax

- 5.1.3 Natural Wax

- 5.2 By Application

- 5.2.1 Candle Making

- 5.2.2 Packaging

- 5.2.3 Cosmetics

- 5.2.4 Adhesives

- 5.2.5 Rubber

- 5.2.6 Other Applications

- 5.3 By Grade

- 5.3.1 Food Grade

- 5.3.2 Industrial Grade

- 5.3.3 Cosmetic and Pharmaceutical garde

- 5.4 By Form

- 5.4.1 Solid

- 5.4.2 Powdered

- 5.4.3 Emulsions and Liquids

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 BASF SE

- 6.4.2 BP p.l.c.

- 6.4.3 Calumet, Inc.,

- 6.4.4 CALWAX

- 6.4.5 China Petrochemical Corporation

- 6.4.6 CLARIANT

- 6.4.7 Evonik Industries AG

- 6.4.8 Exxon Mobil Corporation

- 6.4.9 H&R GROUP

- 6.4.10 Honeywell International Inc.

- 6.4.11 Ilumina Wax d.o.o.

- 6.4.12 Koster Keunen

- 6.4.13 Moeve

- 6.4.14 NIPPON SEIRO CO., LTD.

- 6.4.15 Petrobras

- 6.4.16 Petro-Canada Lubricants Inc.

- 6.4.17 Sasol Ltd.

- 6.4.18 Shell plc

- 6.4.19 Strahl & Pitsch LLC

- 6.4.20 The International Group, Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

- 7.2 Increasing Use of Mineral Wax in Rubber Production

蟲膠塗料市場:依形狀、等級、顏色、最終用途產業、通路和應用方法分類-2026-2032年全球預測醯胺蠟市場:依產品類型、應用、終端用戶產業及通路分類-2026-2032年全球預測費托蠟市場按應用、產品類型和銷售管道,全球預測(2026-2032年)

蟲膠塗料市場:依形狀、等級、顏色、最終用途產業、通路和應用方法分類-2026-2032年全球預測醯胺蠟市場:依產品類型、應用、終端用戶產業及通路分類-2026-2032年全球預測費托蠟市場按應用、產品類型和銷售管道,全球預測(2026-2032年) 全球合成蠟市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球合成蠟市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 日本蠟市場報告:按類型、形態、應用和地區分類(2026-2034年)

日本蠟市場報告:按類型、形態、應用和地區分類(2026-2034年) 蒙大拿蠟市場 - 全球產業規模、佔有率、趨勢、機會及預測(按類型、功能、應用、最終用途、地區和競爭格局分類),2021-2031年防靜電地板蠟市場按產品類型、應用、分銷管道和最終用戶分類-2026-2032年全球預測

蒙大拿蠟市場 - 全球產業規模、佔有率、趨勢、機會及預測(按類型、功能、應用、最終用途、地區和競爭格局分類),2021-2031年防靜電地板蠟市場按產品類型、應用、分銷管道和最終用戶分類-2026-2032年全球預測 蠟市場規模、佔有率和成長分析(按產品類型、應用和地區分類)-2026-2033年產業預測

蠟市場規模、佔有率和成長分析(按產品類型、應用和地區分類)-2026-2033年產業預測 費托蠟市場規模、佔有率和趨勢分析報告:按產品、應用、地區和細分市場預測(2025-2033 年)

費托蠟市場規模、佔有率和趨勢分析報告:按產品、應用、地區和細分市場預測(2025-2033 年) 全球費托合成(FT)蠟市場報告、歷史及預測(2020-2031年)

全球費托合成(FT)蠟市場報告、歷史及預測(2020-2031年)