|

市場調查報告書

商品編碼

1849853

北美位置分析:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)North America Location Analytics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

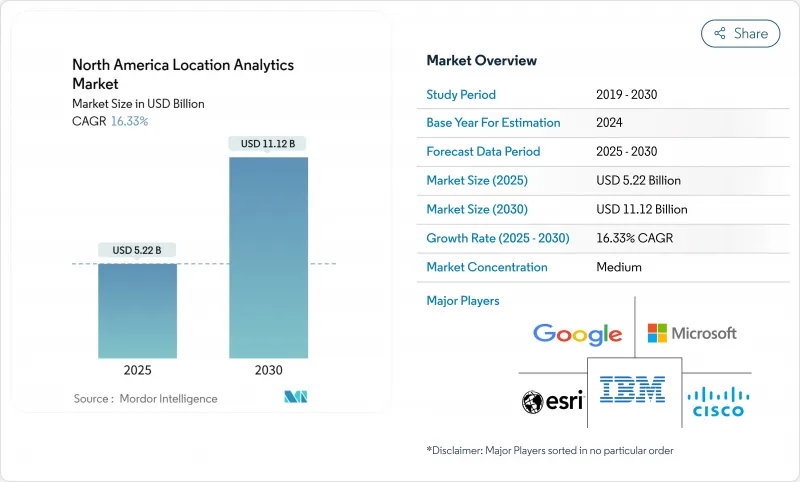

預計到 2025 年北美位置分析市場將成長至 52.2 億美元,到 2030 年將成長至 111.2 億美元,複合年成長率為 16.33%。

強大的推動力包括:全通路零售商尋求精準的地理行銷;物聯網感測器的普及,即時傳輸空間資料;以及向縮短部署週期的雲端原生地理空間平台的廣泛遷移。企業正在從基本的經緯度追蹤轉向豐富的空間分析,以最佳化商品行銷、路線規劃和設施吞吐量。民用5G和CBRS網路正在縮小室內定位精度差距,政府對緊急應變地理技術的投資也正在增加機構需求。雖然日益嚴格的隱私法規是一個主要限制因素,但合規的資料探勘架構已經出現,以保持北美位置分析市場的強勁發展勢頭。

北美位置分析市場趨勢與洞察

全通路零售地理宣傳活動激增

零售商正在將地理圍欄工具與其 CRM 套件相結合,以推出即時促銷活動並提高門市層面的轉換率。展示室最佳化研究表明,策略性的店內產品佈局和擴大的地理覆蓋範圍可以提升銷售和消費者信任。隨著實體店與點擊的連結日益緊密,差異化的位置內容將成為純粹電商無法比擬的忠誠度槓桿。

加強隱私和消費者選擇退出法規

加州的《加州消費者隱私法案》(CCPA)強調了地理位置資料的個人屬性,並強制要求明確選擇退出並強化同意流程。企業現在需要將隱私工程融入其整個分析堆疊中,有時甚至需要降低資料粒度以保持合規性。

細分分析

隨著GPS/GNSS為運輸和物流賦能,戶外定位服務將在2024年佔據北美位置分析市場55%的佔有率。然而,受CBRS私有5G和超寬頻部署帶來的亞米級精度推動,室內定位將以18.4%的複合年成長率成長。製造商正在採用這項技術來實現資產級可視性,醫院也正在利用它來追蹤高價值設備。

日益成長的混合需求迫使供應商將室內和室外層整合到單一真實來源儀表板中。工業 4.0 藍圖要求工人安全地理區域和自動導引車需要連續的座標流。因此,北美位置分析市場正在轉向能夠適應室外 GPS 漂移和室內多路徑校正的多模態引擎。

到2024年,本地系統仍將佔北美位置分析市場規模的60%,反映出在這個高度監管的產業中,資料主權的重要性日益凸顯。雲端選項正以20.1%的複合年成長率擴張,按計量收費處理和本地協作模式吸引了資本支出有限的公司。結合邊緣推理和雲端建模的混合架構也正在興起,從而支援低延遲用例。

私有 CBRS 網路提供了一種結合雲端協作和自主資料路徑的現場替代方案,為工廠提供了避免公共雲端鎖定的途徑。 GeoParquet 等格式化創新技術可最大限度地降低 ETL 開銷,從而解鎖先前需要專門 GIS 腳本編寫的敏捷工作流程。

北美位置分析市場按位置(室內、室外)、部署模式(本地、雲端、其他)、組件(解決方案、其他)、技術(GPS/GNSS、Wi-Fi、其他)、終端用戶垂直領域(零售、銀行、製造、政府、其他)、應用(風險管理、其他)和國家細分。市場預測以美元計算。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場狀況

- 市場概況

- 市場促進因素

- 全通路零售地理宣傳活動激增

- 物聯網感測器和連接設備的激增

- 加速採用雲端原生地理空間分析平台

- 企業對混合工作場所佔用資訊的需求

- CBRS Private 5G 提升室內定位精度

- 市場限制

- 加強隱私和消費者選擇退出法規

- 即時室內定位系統的總擁有成本高

- 地理空間資料科學人才短缺

- 價值/供應鏈分析

- 監管格局

- 技術展望

- 五力分析

- 買方的議價能力

- 供應商的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章市場規模及成長預測

- 按位置類型

- 室內的

- 戶外

- 按部署模型

- 本地部署

- 雲

- 混合

- 邊緣(在設備上)

- 按組件

- 解決方案

- 服務

- 依技術

- GPS/GNSS

- Wi-Fi

- 低功耗藍牙 (BLE)

- 超寬頻(UWB)

- 蜂窩網路(包括 4G/5G 和 CBRS)

- RFID 和 NFC

- 磁性及其他

- 按最終用戶

- 零售與電子商務

- 銀行、金融服務和保險(BFSI)

- 製造業

- 醫療保健和生命科學

- 政府和國防

- 能源與公共產業

- 運輸/物流

- 通訊/IT

- 房地產和智慧建築

- 其他行業

- 按用途

- 風險管理

- 供應鍊和庫存最佳化

- 銷售和行銷最佳化

- 設施和資產管理

- 人力資源與現場管理

- 遠端監控和預測性維護

- 緊急和災難應變管理

- 客戶體驗與參與

- 詐欺與合規分析

- 其他

- 按國家

- 美國

- 加拿大

- 墨西哥

第6章 競爭態勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Cisco Systems Inc.

- SAP SE

- Esri Inc.

- Aruba Networks(HPE Development LP)

- IBM Corporation

- SAS Institute Inc.

- Pitney Bowes Inc.

- HERE Global BV

- TIBCO Software Inc.

- Ericsson Inc.

- Microsoft Corporation

- Google LLC

- Oracle Corporation

- Alteryx Inc.

- Mapbox Inc.

- CARTO

- Trimble Inc.

- Zebra Technologies Corp.

- Inpixon

- Foursquare Labs Inc.

- Precisely

- TomTom NV

- Mapsted Corp.

第7章 市場機會與未來展望

The North America location analytics market size is valued at USD 5.22 billion in 2025 and is projected to advance to USD 11.12 billion by 2030, expanding at a 16.33% CAGR.

Strong tailwinds come from omni-channel retail organizations demanding precise geo-marketing, the surge of IoT sensors streaming real-time spatial data, and widespread migration to cloud-native geospatial platforms that compress deployment cycles. Enterprises are moving beyond basic latitude-and-longitude tracking toward rich spatial analytics that optimize merchandising, routing, and facility throughput. Private-5G and CBRS networks shorten indoor accuracy gaps, while government investment in emergency-response geotechnology adds an institutional layer of demand. Rising privacy regulation represents the main tempering factor, yet compliant data-mining architectures are already emerging to keep momentum intact for the North America location analytics market.

North America Location Analytics Market Trends and Insights

Surge in Omni-Channel Retail Geo-Marketing Campaigns

Retailers pair geofencing tools with CRM suites to trigger real-time promotions, driving higher conversion at store level. Showroom optimization research indicates that strategic in-store product placement and geographic reach expansion lift sales and consumer confidence. As brick-and-click convergence deepens, differentiated location content becomes a loyalty lever that pure-play e-commerce cannot replicate.

Heightened Privacy and Consumer Opt-Out Regulations

California's CCPA enforcement sweep spotlights the personal nature of geolocation data, requiring explicit opt-outs and stronger consent flows. Enterprises must now embed privacy engineering into every analytics stack, sometimes trimming data granularity to stay compliant.

Other drivers and restraints analyzed in the detailed report include:

- Proliferation of IoT Sensors & Connected Devices

- Accelerated Adoption of Cloud-Native Geospatial Analytics Platforms

- Corporate Demand for Hybrid Workplace Occupancy Intelligence

- High Total Cost of Ownership for Real-Time Indoor Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Outdoor services retained 55% North America location analytics market share in 2024 as GPS/GNSS underpins transportation and logistics. Indoor positioning, however, compounds at 18.4% CAGR, powered by sub-meter accuracy from CBRS-enabled private 5G and ultra-wideband deployments. Manufacturers embed the technology for asset-level visibility, while hospitals apply it to track high-value equipment.

Growing hybrid demand obliges vendors to fuse indoor and outdoor layers into single source-of-truth dashboards. Industry 4.0 blueprints call for worker safety geozones and automated guided vehicles requiring continuous coordinate streams. The North America location analytics market therefore pivots to multi-modal engines that reconcile GPS drift outdoors with multipath corrections indoors.

On-premise systems still accounted for 60% of the North America location analytics market size in 2024, reflecting data-sovereignty priorities among heavily regulated sectors. Cloud options are scaling at a 20.1% CAGR as pay-as-you-go processing and native collaboration entice enterprises with limited capex. Hybrid architectures are also rising, combining edge inference with cloud modeling for low-latency use cases.

Private CBRS networks offer an on-site alternative that marries cloud orchestration with sovereign data paths, giving factories a route around public-cloud lock-in. Format innovations such as GeoParquet minimize ETL overhead, unlocking agile workflows that previously demanded specialist GIS scripting.

The North America Location Analytics Market Segmented by Location (Indoor, Outdoor), Deployment Model (On-Premises, Cloud and More), Component (Solutions and More), Technology (GPS / GNSS, Wi-Fi and More), End-User Vertical (Retail, Banking, Manufacturing, Government, and More), Application (Risk Management and More), and by Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Cisco Systems Inc.

- SAP SE

- Esri Inc.

- Aruba Networks (HPE Development LP)

- IBM Corporation

- SAS Institute Inc.

- Pitney Bowes Inc.

- HERE Global BV

- TIBCO Software Inc.

- Ericsson Inc.

- Microsoft Corporation

- Google LLC

- Oracle Corporation

- Alteryx Inc.

- Mapbox Inc.

- CARTO

- Trimble Inc.

- Zebra Technologies Corp.

- Inpixon

- Foursquare Labs Inc.

- Precisely

- TomTom N.V.

- Mapsted Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in omni-channel retail geo-marketing campaigns

- 4.2.2 Proliferation of IoT sensors & connected devices

- 4.2.3 Accelerated adoption of cloud-native geospatial analytics platforms

- 4.2.4 Corporate demand for hybrid workplace occupancy intelligence

- 4.2.5 Availability of CBRS private-5G improving indoor location accuracy

- 4.3 Market Restraints

- 4.3.1 Heightened privacy and consumer opt-out regulations

- 4.3.2 High total cost of ownership for real-time indoor location systems

- 4.3.3 Shortage of geospatial data-science talent

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porters Five Forces

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE & GROWTH FORECASTS (VALUE)

- 5.1 By Location Type

- 5.1.1 Indoor

- 5.1.2 Outdoor

- 5.2 By Deployment Model

- 5.2.1 On-premise

- 5.2.2 Cloud

- 5.2.3 Hybrid

- 5.2.4 Edge (on-device)

- 5.3 By Component

- 5.3.1 Solutions

- 5.3.2 Services

- 5.4 By Technology

- 5.4.1 GPS / GNSS

- 5.4.2 Wi-Fi

- 5.4.3 Bluetooth Low-Energy (BLE)

- 5.4.4 Ultra-Wideband (UWB)

- 5.4.5 Cellular (4G/5G incl. CBRS)

- 5.4.6 RFID & NFC

- 5.4.7 Magnetic & Other

- 5.5 By End-User Vertical

- 5.5.1 Retail & E-Commerce

- 5.5.2 Banking, Financial Services & Insurance (BFSI)

- 5.5.3 Manufacturing

- 5.5.4 Healthcare & Life Sciences

- 5.5.5 Government & Defense

- 5.5.6 Energy & Utilities

- 5.5.7 Transportation & Logistics

- 5.5.8 Telecom & IT

- 5.5.9 Real Estate & Smart Buildings

- 5.5.10 Other Verticals

- 5.6 By Application

- 5.6.1 Risk Management

- 5.6.2 Supply Chain & Inventory Optimization

- 5.6.3 Sales & Marketing Optimization

- 5.6.4 Facility & Asset Management

- 5.6.5 Workforce & Field-Force Management

- 5.6.6 Remote Monitoring & Predictive Maintenance

- 5.6.7 Emergency & Disaster Response Management

- 5.6.8 Customer Experience & Engagement

- 5.6.9 Fraud & Compliance Analytics

- 5.6.10 Others

- 5.7 By Country

- 5.7.1 United States

- 5.7.2 Canada

- 5.7.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Cisco Systems Inc.

- 6.4.2 SAP SE

- 6.4.3 Esri Inc.

- 6.4.4 Aruba Networks (HPE Development LP)

- 6.4.5 IBM Corporation

- 6.4.6 SAS Institute Inc.

- 6.4.7 Pitney Bowes Inc.

- 6.4.8 HERE Global BV

- 6.4.9 TIBCO Software Inc.

- 6.4.10 Ericsson Inc.

- 6.4.11 Microsoft Corporation

- 6.4.12 Google LLC

- 6.4.13 Oracle Corporation

- 6.4.14 Alteryx Inc.

- 6.4.15 Mapbox Inc.

- 6.4.16 CARTO

- 6.4.17 Trimble Inc.

- 6.4.18 Zebra Technologies Corp.

- 6.4.19 Inpixon

- 6.4.20 Foursquare Labs Inc.

- 6.4.21 Precisely

- 6.4.22 TomTom N.V.

- 6.4.23 Mapsted Corp.

7 MARKET OPPORTUNITIES & FUTURE OUTLOOK

- 7.1 White-space & Unmet-need Assessment

位置分析市場:按組件、部署類型、分析類型和應用分類-2026-2032年全球市場預測

位置分析市場:按組件、部署類型、分析類型和應用分類-2026-2032年全球市場預測 2026年全球位置分析市場報告

2026年全球位置分析市場報告 位置分析市場規模、佔有率、趨勢和預測:按組件、部署類型、位置類型、應用、最終用戶行業和地區分類,2026-2034 年

位置分析市場規模、佔有率、趨勢和預測:按組件、部署類型、位置類型、應用、最終用戶行業和地區分類,2026-2034 年 位置分析市場分析及預測(至 2035 年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶和解決方案分類

位置分析市場分析及預測(至 2035 年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶和解決方案分類 位置分析市場規模、佔有率、成長率和全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測

位置分析市場規模、佔有率、成長率和全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測 全球位置分析市場(至 2035 年):按組件類型、位置類型、部署類型、應用類型、行業類型、地區、行業趨勢和預測

全球位置分析市場(至 2035 年):按組件類型、位置類型、部署類型、應用類型、行業類型、地區、行業趨勢和預測 全球位置分析工具市場,2025-2029年

全球位置分析工具市場,2025-2029年 位置分析市場 - 全球產業規模、佔有率、趨勢、機會和預測,按組件、位置類型、部署方式、應用、垂直產業、地區和競爭格局分類,2021-2031 年預測

位置分析市場 - 全球產業規模、佔有率、趨勢、機會和預測,按組件、位置類型、部署方式、應用、垂直產業、地區和競爭格局分類,2021-2031 年預測 MEA 位置分析:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)

MEA 位置分析:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年) 2032 年位置分析市場預測:按類型、組件、部署模式、應用、最終用戶和地區進行的全球分析

2032 年位置分析市場預測:按類型、組件、部署模式、應用、最終用戶和地區進行的全球分析