|

市場調查報告書

商品編碼

1849824

汽車微型馬達:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)Automotive Micro Motor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

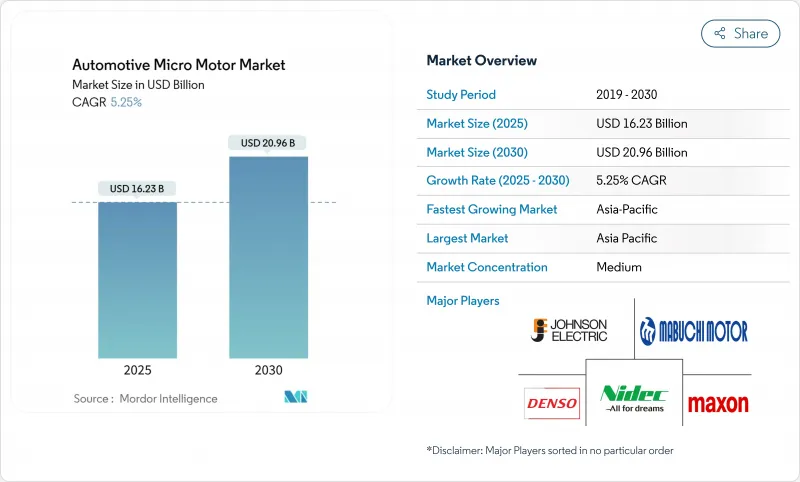

預計2025年汽車微馬達市場規模將達162.3億美元,2030年將達到約209.6億美元,複合年成長率為5.25%。

這得益於電動車數量的快速成長、向48V輕度混合動力架構的轉變,以及每輛車動力傳動系統、安全性和舒適性模組的不斷增加。日本電產已投入超過70億美元的累計,用於擴大其電力驅動橋產能,以在無刷馬達技術。

全球汽車微電機市場趨勢與洞察

電動車產量快速成長

全球電動車出貨量持續超過輕型車的整體成長速度,每款純電池車型都依賴數十台輔助微型馬達進行溫度控管、空氣動力學、轉向、煞車和電池組冷卻。 《組裝雜誌》預測,到 2034 年,牽引馬達產量將成長四倍,超過 1.2 億台,這一趨勢將波及整個子系統對小型馬達的需求。中國 2023 年汽車出口量將達到 491 萬台,超過日本,反映了這一轉變,大部分汽車微型馬達市場集中在中國。高階電動車中的 800V 高壓架構進一步提高了基於碳化矽元件的微型馬達控制電子設備的性能標準,促使供應商轉向強大的高頻驅動器模組。

48V輕度混合動力架構的興起

透過從傳統的 12V 電源轉換為 48V 電源,汽車製造商可以降低高達 15% 的油耗,同時開闢新的微型馬達應用,例如主動懸吊、啟動和停止和電動增壓。 CLEPA 預測,到 2025 年,每 10 輛新車就有 1 輛將配備 48V 系統。 48V 電池市場預計將隨之成長,為汽車微型馬達市場創造巨大的設計機會。特斯拉在 Cybertruck 採用 48V 線路正在加速產業轉型,但傳統製造商將需要徹底改造其線束、連接器和檢驗工具,以適應更高的電壓。

稀土磁鐵價格走勢

永久磁鐵價格波動是汽車微型馬達供應商面臨的最嚴峻成本挑戰。過去一年,釹鐵硼現貨價格下跌了42%,但隨著中國加強出口限制,長期供應風險隱現。已有報導稱,一些汽車項目,例如日本鈴木雨燕生產線,因磁鐵供應中斷而停產。業內企業正在實現採購多元化:日本電產株式會社(Nidec)已簽署2025年契約,將使用美國生產的Noveon Ecoflux磁鐵,以緩解貨幣和地緣政治衝擊。

細分分析

到2024年,12-24V級馬達將佔據汽車微型馬達市場佔有率的42.44%。然而,隨著汽車製造商採用輕度混合動力和800V電動車傳動系統以提高效率,高壓(48V及以上)馬達市場的複合年成長率將達到5.78%,成為最快的市場。這種轉變將擴大汽車微型馬達的市場規模,這類馬達將高扭力無刷馬達與低規格線束結合,從而降低電阻損耗並減輕熱負荷。特斯拉推出48V線束,凸顯了業界對下一代電氣標準的廣泛共識。

CLEPA 已確認 48V 技術可降低高達 15% 的燃油消耗,加速其在歐洲二氧化碳合規策略中的應用。因此,供應商正在擴展其模組化定子系列,以涵蓋從 24V 鼓風機馬達到 400V 牽引配件的所有產品,從而最大限度地提高平台的重複使用率。新興的低功耗(<11V)細分市場與感測器節點相關,但其收益佔有率有限。

到2024年,DC馬達將佔總收入的59.65%,這得益於車窗升降器、座椅調節器和暖通空調風門等經濟高效的設計。然而,AC馬達的複合年成長率將達到6.5%,因為變速運轉可以降低轉向、煞車和冷卻水泵幫浦的能耗。因此,汽車微型馬達市場提供了均衡的產品組合,直流馬達平台仍然適用於開關驅動,而逆變器驅動的交流馬達則滿足了電動方向盤的效率目標。

日本電產 (Nidec) 的 SynRA 產品線標誌著同步磁阻架構的突破,該架構可消除稀土磁鐵並提高供應彈性。Johnson Electric2023/24 會計年度的銷售額顯示,兩種類型的馬達均持續受到原始設備製造商的青睞,檢驗了其多技術藍圖的可行性。

區域分析

預計到2024年,亞太地區將佔全球銷售額的48.48%,到2030年的複合年成長率將達到6.20%,使該地區成為汽車微電機市場的領頭羊。 2023年,中國汽車出口量將達到491萬輛,超過日本,從而建立起廣泛的微型電機、半導體和磁鐵供應基礎。日本電產計畫將大連工廠的員工人數增加至多50%,使其成為全球最大的電動車馬達中心,年產能達到100萬台。泰國和印尼將進行新的投資,以建立一體化的電動車供應鏈,擴大本地採購選擇。

隨著排放法規趨嚴,48V 技術的引入以及高階原始設備製造商對主動空氣動力學的青睞,歐洲正在穩步發展。歐洲汽車製造商環保署 (CLEPA) 正在大力推動輕度混合動力傳動系統的發展,而捨弗勒與 Vitesco 將於 2024 年合併,這將增強歐洲本土的電機專業技術。德國新興企業DeepDrive 已獲得 3,350 萬美元融資,用於將雙轉子設計商業化,該設計使用的磁鐵數量將減少 50%,彰顯了歐洲在輕質材料創新方面的努力。

北美市場受回流政策和特斯拉主導的電壓標準化所推動。 KPS資本合夥公司以35億歐元收購西門子Innomotics部門,彰顯了私募股權對高價值汽車品牌的興趣。南美市場基數較小,但成長強勁,這得益於巴西和阿根廷電子產品在生產中的比例不斷上升。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場狀況

- 市場概況

- 市場促進因素

- 電動車產量快速成長

- 對豪華和高檔內裝的需求不斷成長

- 推動車輛輕量化和零件小型化

- 48V輕度混合動力架構的興起

- 整合到主動空氣動力學系統中

- 客房保健設施普及(離子產生器、空氣清新劑)

- 市場限制

- 稀土元素磁鐵價格上漲

- 持續的技術升級推動單位成本上升

- 嚴格的公差規範增加了認證成本

- 壓電致動器替代品的出現

- 價值鏈/供應鏈分析

- 監管格局

- 技術展望

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章市場規模和成長預測(價值(美元)和數量(單位))

- 按功耗

- 11V或更低

- 12~24V

- 25~48V

- 48V或更高

- 依馬達類型

- DC馬達

- AC馬達

- 依技術

- 有刷微電機

- 無刷微電機

- 按用途

- 車身電子設備(車窗、座椅、後視鏡)

- 動力傳動系統傳動系統

- 底盤和轉向

- 安全性和 ADAS 模組

- 資訊娛樂和連接

- 按車輛類型

- 搭乘用車

- 商用車

- 按銷售管道

- OEM

- 售後市場

- 按地區

- 北美洲

- 美國

- 加拿大

- 其他北美地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲和紐西蘭

- 其他亞太地區

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 南非

- 其他中東和非洲地區

- 北美洲

第6章 競爭態勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Nidec Corporation

- Johnson Electric Holdings Ltd.

- Mabuchi Motor Co., Ltd.

- Maxon Motor AG

- Mitsuba Corporation

- Buhler Motor GmbH

- Denso Corporation

- Robert Bosch GmbH

- Continental AG

- Valeo SA

- Brose Fahrzeugteile SE

- Ametek Inc.

- MinebeaMitsumi Inc.

- Mitsumi Electric Co., Ltd.

- Shenzhen Kinmore Motor Co.

- Constar MicroMotor

- Wellings Holdings Ltd.

第7章 市場機會與未來展望

The automotive micromotor market size stood at USD 16.23 billion in 2025 and is forecast to reach about USD 20.96 billion by 2030, advancing at a 5.25% CAGR.

Gains stem from fast-rising electric-vehicle (EV) volumes, the migration to 48 V mild-hybrid architectures and growing content per vehicle across powertrain, safety and comfort modules. Manufacturers are scaling regional production hubs to meet local sourcing rules; Nidec alone earmarked more than USD 7 billion for expanded E-Axle capacity to capture additional automotive micromotor market share. Asia-Pacific remains the demand epicentre, helped by China's export leadership, while higher-voltage platforms spur the fastest adoption of brushless motor technologies in North America and Europe.

Global Automotive Micro Motor Market Trends and Insights

Surge in EV Production Volumes

Global EV shipments continue to outpace overall light-vehicle growth, and each pure battery model relies on dozens of auxiliary micromotors for thermal management, aerodynamics, steering, braking and battery-pack cooling. Assembly Magazine forecasts a fourfold jump in traction-motor output to more than 120 million units by 2034, a trend that cascades into parallel demand for smaller motors across sub-systems. China's rise to 4.91 million vehicle exports in 2023, surpassing Japan, reflects this shift and concentrates much of the automotive micromotor market in the region. Higher 800 V architectures in premium EVs further raise the performance bar for micromotor control electronics built around silicon-carbide devices, pushing suppliers toward robust, high-frequency driver modules.

Rise in 48V Mild-Hybrid Architectures

Moving from traditional 12 V electrics to 48 V boards allows automakers to cut fuel use by up to 15% while unlocking new micromotor applications in active suspension, start-stop and electric superchargers. CLEPA projects 48 V systems in one out of every ten new cars by 2025. The accompanying 48 V battery segment is anticipated to climb, giving the automotive micromotor market a sizeable design-in opportunity. Tesla's adoption of 48 V wiring in the Cybertruck accelerates industry conversion, although legacy manufacturers must overhaul harnesses, connectors and validation tools to cope with higher voltages.

Up-trend in Rare-Earth Magnet Prices

Permanent-magnet pricing volatility is the most acute cost challenge for automotive micromotor suppliers. Neodymium spot values slid 42% over the past year, yet long-term supply risk looms as China tightens export controls. Vehicle programmes already report production pauses, such as Suzuki's Swift line in Japan, when magnet shipments stalled. Industry players are diversifying sourcing: Nidec signed a 2025 deal to adopt Noveon Ecoflux magnets produced in the United States, buffering currency and geopolitical shocks.

Other drivers and restraints analyzed in the detailed report include:

- Growing Demand for Luxury & Premium Interiors

- Vehicle Lightweighting & Component Miniaturisation Push

- Constant Tech Upgrades Inflating Unit Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The 12 to 24 V class held 42.44% of the 2024 automotive micromotor market share, reflecting legacy electrical architectures across the light-vehicle parc. Higher-voltage (More than 48 V) segments, however, register the fastest 5.78% CAGR as OEMs adopt mild-hybrid and 800 V EV drivetrains for efficiency gains. This shift enlarges the automotive micromotor market size for high-torque brushless units paired with low-gauge wiring harnesses, cutting resistive losses and easing thermal loads. Tesla's 48 V harness rollout underscores broad industry alignment on the next electrical standard.

CLEPA confirms that 48 V technology can trim fuel use by up to 15%, accelerating its inclusion in European CO2-compliance strategies. Suppliers therefore scale modular stator families that cover 24 V blower motors through 400 V traction auxiliaries, maximising platform reuse. Emerging low-power (Less than 11 V) niches remain relevant for sensor nodes yet represent a limited portion of revenue.

DC motors commanded 59.65% of 2024 revenue thanks to cost-effective designs for window lifts, seat adjusters and HVAC flaps. Nevertheless, AC machines record a robust 6.5% CAGR because variable-speed operation reduces energy draw in steering, braking and coolant pumps. The automotive micromotor market therefore witnesses a balanced portfolio where DC platforms remain viable for on-off actuation, while inverter-driven AC options satisfy efficiency targets in electric power steering.

Nidec's SynRA line illustrates the push toward synchronous-reluctance architectures that remove rare-earth magnets, boosting supply resilience. Johnson Electric's FY23/24 sales indicate sustained OEM uptake across both motor types, validating a multi-technology roadmap.

The Automotive Micro Motors Market Report is Segmented by Power Consumption (Below 11V, 12 To 24V, and More), Motor Type (DC Motor and AC Motor), Technology (Brushed Micromotor and Brushless Micromotor), Application (Body Electronics and More), Vehicle Type (Passenger Cars and Commercial Vehicles), Sales Channel (OEM and Aftermarket), and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Geography Analysis

Asia-Pacific generated 48.48% of global revenue in 2024, and its 6.20% CAGR to 2030 keeps the region at the forefront of the automotive micromotor market. Chinese exporters shipped 4.91 million vehicles in 2023, surpassing Japan and consolidating a broad supply base for micromotors, semiconductors and magnets. Nidec plans to raise headcount at its Dalian complex by up to 50%, turning it into the world's largest EV-motor site capable of one-million-unit output a year. Thailand and Indonesia court fresh investment to create integrated EV supply chains, broadening regional sourcing options.

Europe advances at a steady rate as strict emissions targets spur 48 V roll-outs and premium OEMs adopt active aerodynamics. CLEPA's promotion of mild-hybrid powertrains and Schaeffler's 2024 merger with Vitesco bolster local motor expertise. German start-up DeepDrive secured USD 33.5 million to commercialise dual-rotor designs using 50% fewer magnets, highlighting Europe's push for material-light innovations.

North America is powered by reshoring policies and Tesla-led voltage standardisation. KPS Capital Partners' EUR 3.5 billion takeover of Siemens' Innomotics division signals private equity appetite for high-value motor brands. South America exhibits the highr growth off a smaller base, aided by rising electronics content in Brazilian and Argentine production.

- Nidec Corporation

- Johnson Electric Holdings Ltd.

- Mabuchi Motor Co., Ltd.

- Maxon Motor AG

- Mitsuba Corporation

- Buhler Motor GmbH

- Denso Corporation

- Robert Bosch GmbH

- Continental AG

- Valeo SA

- Brose Fahrzeugteile SE

- Ametek Inc.

- MinebeaMitsumi Inc.

- Mitsumi Electric Co., Ltd.

- Shenzhen Kinmore Motor Co.

- Constar MicroMotor

- Wellings Holdings Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in EV production volumes

- 4.2.2 Growing demand for luxury & premium interiors

- 4.2.3 Vehicle lightweighting & component miniaturisation push

- 4.2.4 Rise in 48 V mild-hybrid architectures

- 4.2.5 Integration in active aerodynamics systems

- 4.2.6 Proliferation of cabin wellness features (ionizers, scent dispensers)

- 4.3 Market Restraints

- 4.3.1 Up-trend in rare-earth magnet prices

- 4.3.2 Constant tech upgrades inflating unit costs

- 4.3.3 Tight tolerance specs raising qualification costs

- 4.3.4 Emerging piezo-actuator substitutes

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Power Consumption

- 5.1.1 Below 11 V

- 5.1.2 12 to 24 V

- 5.1.3 25 to 48 V

- 5.1.4 Above 48 V

- 5.2 By Motor Type

- 5.2.1 DC Motor

- 5.2.2 AC Motor

- 5.3 By Technology

- 5.3.1 Brushed Micromotor

- 5.3.2 Brushless Micromotor

- 5.4 By Application

- 5.4.1 Body Electronics (window, seat, mirror)

- 5.4.2 Powertrain & Drivetrain Systems

- 5.4.3 Chassis & Steering

- 5.4.4 Safety & ADAS Modules

- 5.4.5 Infotainment & Connectivity

- 5.5 By Vehicle Type

- 5.5.1 Passenger Cars

- 5.5.2 Commercial Vehicles

- 5.6 By Sales Channel

- 5.6.1 OEM

- 5.6.2 Aftermarket

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Rest of North America

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 Germany

- 5.7.3.2 United Kingdom

- 5.7.3.3 France

- 5.7.3.4 Italy

- 5.7.3.5 Spain

- 5.7.3.6 Russia

- 5.7.3.7 Rest of Europe

- 5.7.4 Asia-Pacific

- 5.7.4.1 China

- 5.7.4.2 Japan

- 5.7.4.3 India

- 5.7.4.4 South Korea

- 5.7.4.5 Australia & New Zealand

- 5.7.4.6 Rest of Asia-Pacific

- 5.7.5 Middle East and Africa

- 5.7.5.1 Saudi Arabia

- 5.7.5.2 United Arab Emirates

- 5.7.5.3 Turkey

- 5.7.5.4 South Africa

- 5.7.5.5 Rest of Middle East and Africa

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Nidec Corporation

- 6.4.2 Johnson Electric Holdings Ltd.

- 6.4.3 Mabuchi Motor Co., Ltd.

- 6.4.4 Maxon Motor AG

- 6.4.5 Mitsuba Corporation

- 6.4.6 Buhler Motor GmbH

- 6.4.7 Denso Corporation

- 6.4.8 Robert Bosch GmbH

- 6.4.9 Continental AG

- 6.4.10 Valeo SA

- 6.4.11 Brose Fahrzeugteile SE

- 6.4.12 Ametek Inc.

- 6.4.13 MinebeaMitsumi Inc.

- 6.4.14 Mitsumi Electric Co., Ltd.

- 6.4.15 Shenzhen Kinmore Motor Co.

- 6.4.16 Constar MicroMotor

- 6.4.17 Wellings Holdings Ltd.