|

市場調查報告書

商品編碼

1849809

金融雲:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)Finance Cloud - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

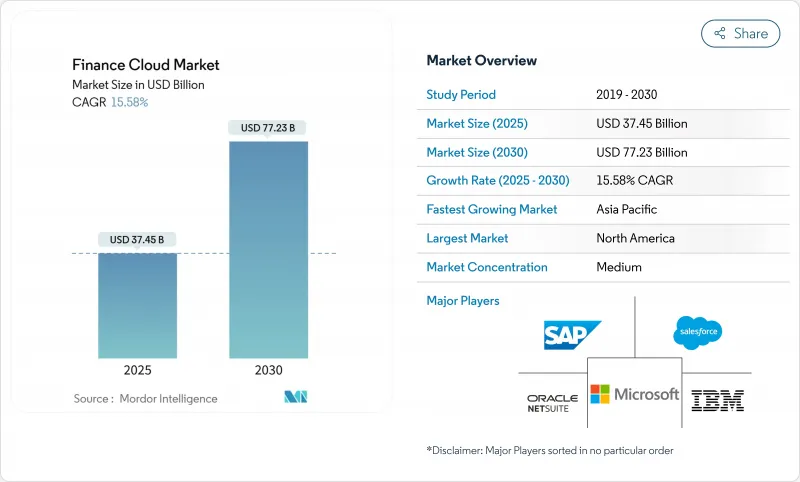

預計2025年金融雲市場規模將達374.5億美元,2030年將達772.3億美元,複合年成長率為15.6%。

消費者對數位優先世界的期望不斷提高、法律規範加大以及雲端安全框架日趨成熟,推動公共雲端雲和混合雲端。僅歐盟的數位和營運彈性法案 (DORA) 就要求約 22,000 家金融機構及其技術合作夥伴升級 ICT 風險管理,從而加速整個全部區域的平台現代化。同時,98% 的全球金融機構已經使用至少一種雲端服務,高於 2020 年的 91%,證實了金融雲市場已經達到臨界規模。現在,在雲端基礎架構上部署生成性人工智慧支撐著從自動對帳到預測現金流建模的一切,使雲端供應商成為策略合作夥伴以獲得競爭優勢。北美銀行正在投資數十億美元的技術預算來遷移數千個應用程式,而亞太金融機構正在擴展其雲端原生核心以服務其龐大的數位客戶群。

全球金融雲市場趨勢與洞察

需要改進客戶關係管理

雲端基礎的CRM 套件使金融機構能夠即時洞察行為模式,從而提供高度個人化的服務,並在競爭激烈的市場中提高客戶留存率。亞太地區的銀行正在運行能夠支援數千萬並發會話的雲端平台,例如 AIBank 的微服務核心,它服務超過 1 億客戶。同時,北美金融機構正在整合雲端分析和忠誠度引擎,以減少客戶流失,而客戶流失問題仍影響著超過 60% 的傳統金融機構。由於金融數據受到嚴格監管,供應商正在透過平台內加密、審核追蹤和資料居住管理來脫穎而出,這些技術既能實現跨通路編配,又能滿足監管機構的要求。隨著客戶生命週期價值成為關鍵的 KPI,隨著銀行尋求以彈性、支援人工智慧的替代方案取代老舊的 CRM 工具,金融雲市場正在獲得進一步的發展動能。

金融領域對營運效率的需求

將財務工作負載遷移到消費雲可將資本支出轉化為可變營運成本,從而釋放資金用於產品創新。已完全遷移到雲端的金融機構報告稱,其月末結帳週期縮短了 20-30%,監管報告速度也有類似的提升。雲端 ERP 內建的自動化功能消除了手動會計分錄的需要,而無伺服器運算則使它們能夠處理不可預測的支付量激增,而不會降低效能。例如,Discover Financial Services 依靠混合資產在季節性支出高峰期間靈活調配資源。隨著利潤率收緊,成本收入比現在與收益一起出現在董事會儀表板上,這強化了持續推動金融雲市場發展的效率概念。

雲端基礎的網路威脅的興起

金融服務仍然是高階攻擊的首要目標,而雲端環境的威脅面正在不斷擴大。美國監管機構報告稱,勒索軟體攻擊不斷升級,破壞了關鍵的支付基礎設施,迫使銀行加倍投資於零信任架構和增強型檢測平台。如果金融機構遷移敏感資料時沒有進行相應的安全改進,則可能面臨超過其年度IT預算的監管罰款。雲端供應商正在製定機密運算、硬體加密和主權雲端的藍圖來應對這項挑戰,但實施這些控制措施的成本和複雜性將限制金融雲端市場近期的成長。

細分分析

2024年,財務預測與規劃部門的收益將達到38.3%,反映出在持續的經濟波動中,情境建模的普遍需求。雲端基礎的EPM套件使財務團隊能夠跨數千個成本中心創建滾動預測,從而增強數據主導的決策能力。整合的基於促進因素的模型可在利率或外匯衝擊後即時更新利潤預測,進一步凸顯了轉型的緊迫性。同時,在DORA和類似法規的推動下,風險、合規和監管科技是成長最快的解決方案領域,到2030年,其複合年成長率將達到15.9%。供應商正在整合支援API的監管庫,使金融機構只需點擊即可向監管機構報告詳細的交易資料。持續的管理監控功能減輕了審核準備的負擔,直接影響合規預算,並推動了金融雲端市場的需求。

核心會計和總分類帳平台仍然至關重要,它們是所有其他雲端財務模組的記錄系統基石。資金籌措。例如,花旗集團擴展了其雲端財務工作區,以提供全球現金部位的逐分鐘總結。 Workday 的最新版本捆綁了勞動力規劃和支出分析,清楚地展示了整合套件如何改善企業協調。隨著供應商將這些功能打包到統一的資料架構下,它將擴大提升銷售管道,並推動財務雲端市場永續的收益源。

受超大規模雲端運算供應商的全球企業發展、先進的安全認證和持續創新藍圖的推動,公有雲將佔2024年總收入的57.6%。銀行通常採用託管的PaaS資料庫來加速新產品的推出,而無需配置硬體。然而,對單一供應商的依賴引發了對彈性的擔憂,推動混合雲和多重雲端的採用,複合年成長率達到17.0%。歐洲金融機構意識到監管機構提到的集中風險,擴大將工作負載分散到至少兩家供應商,同時將超低延遲交易引擎保留在私有雲端中。 Form3的支付平台就體現了這個策略,它抽象化了路由邏輯,使銀行能夠在發生故障時在雲端之間切換端點。

對於對效能和資料完整性要求極高的用例來說,私有雲端仍然至關重要。摩根大通斥資20億美元新建四個私有雲端資料中心,以支援對延遲敏感的風險運算。統一的可觀察性堆疊和策略即程式碼減少了混合設施之間的運作摩擦,使混合雲真正無縫銜接。隨著監管機構對「退出計畫」的明確規定,金融機構更傾向於容器化工作負載和開放API,以避免鎖定。

區域分析

2024年,北美將占到全球金融雲收入的41.0%,這得益於強勁的技術預算和清晰的監管環境,這些因素加速了金融雲的遷移。光是在美國,摩根大通每年就投入170億美元用於技術開發,並將6,000個應用程式遷移到雲端平台。加拿大的開放銀行指南鼓勵建立安全的API生態系統,墨西哥銀行也正在採用雲端技術以滿足跨國報告標準。在網路安全和數位身分框架方面的公私合作進一步降低了採用風險,並增強了該地區的金融雲端市場。供應商正在提高資料中心密度,以滿足高頻交易者低於10毫秒的延遲需求。

亞太地區是成長最快的地區,到2030年的複合年成長率將達到16.2%。政府驅動的數位經濟藍圖將雲端運算置於金融包容性計畫的核心位置,以支持該地區的數位經濟價值,預計2030年將達到1兆美元。中國的AIBank透過容器化平台為超過1億客戶提供服務,展現了雲端運算的可擴展性。印度的公共雲端政策允許監管和政策制定者在嚴格的加密金鑰下將核心資料託管在海外,從而刺激了超大規模企業的採用。日本和澳洲已經核准了行業雲模型,這些模型可為當地監管機構提供預先認證的合規交付成果。亞太地區的銀行預計,到2030年,數位相關服務將貢獻其40%的利潤。再加上不斷成長的收費收益目標,這些趨勢確保了金融雲市場的持續成長。

在歐洲,根據 DORA 營運恢復指令,雲端現代化正在加速,影響到約 22,000 家金融機構。德國、法國和英國正在推出網路事件模擬的共用測試框架,並鼓勵採用可自動收集證據的平台。由領先供應商營運的主權雲端區域符合資料主權規定,多供應商策略可降低系統性風險。南美洲正在呈現強勁成長,巴西的無分行挑戰者分店(例如 Nubank)累計,在完全依靠雲端基礎設施營運的情況下,2024 年的利潤將達到 20 億美元。中東和非洲的雲端採用正在加速,該地區 83% 的金融機構使用雲端工作負載,預計兩年內每年可節省 2,114 萬美元的成本。海灣合作理事會的銀行正在將國家雲端授權與雄心勃勃的數位轉型藍圖相結合,鞏固金融雲端市場的新需求。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場狀況

- 市場概況

- 市場促進因素

- 需要改進客戶關係管理

- 金融領域對營運效率的需求

- 監管推動即時透明度和報告

- 支持 GenAI 的自助財務分析

- 採用 FinOps 最佳化雲端支出

- 面向 BFSI 產業的產業雲平台

- 市場限制

- 雲端基礎的網路威脅的興起

- 遺留核心整合的複雜性

- 雲端金融營運與數據工程人才缺口

- 供應商鎖定和 GenAI 成本超支

- 價值鏈分析

- 監管格局

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 評估宏觀經濟趨勢對市場的影響

第5章市場規模及成長預測

- 按解決方案

- 核心會計和總帳

- 財務預測與規劃

- 風險、合規和監管科技

- 財務和現金管理

- 薪資核算和勞動力財務

- 按部署模型

- 公共雲端

- 私有雲端

- 混合/多重雲端

- 按最終用戶

- 銀行業

- 保險

- 資本市場

- 金融科技/新銀行

- 按公司規模

- 主要企業

- 小型企業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 其他亞太地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 埃及

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭態勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Oracle Corporation(Netsuite)

- SAP

- Microsoft

- Salesforce

- IBM

- Workday

- Sage Intacct

- Unit4/FinancialForce

- Intuit

- Anaplan

- Workiva

- BlackLine

- Coupa

- Xero

- FIS

- Fiserv

- Temenos

- Finastra

- Acumatica

- AWS

- Google Cloud

- Huawei

第7章 市場機會與未來展望

The finance cloud market size is valued at USD 37.45 billion in 2025 and is set to reach USD 77.23 billion by 2030, advancing at a 15.6% CAGR.

Rising digital-first consumer expectations, tighter regulatory oversight, and the maturation of cloud security frameworks are driving widespread migration of core finance workloads to public and hybrid clouds. The European Union's Digital Operational Resilience Act (DORA) alone mandates upgraded ICT risk controls for about 22,000 financial entities and their technology partners, accelerating platform modernization across the region. At the same time, 98% of financial institutions globally already use at least one cloud service, up from 91% in 2020, confirming that the finance cloud market has reached critical mass. Generative AI roll-outs on cloud infrastructure now underpin everything from automated reconciliation to predictive cash-flow modelling, turning cloud providers into strategic partners for competitive differentiation. North American banks fund multibillion-dollar tech budgets to migrate thousands of applications, while Asia-Pacific institutions scale cloud-native cores to serve massive digital customer bases-all of which keeps the finance cloud market on a steep growth trajectory.

Global Finance Cloud Market Trends and Insights

Need for Improved Customer Relationship Management

Cloud-based CRM suites give financial institutions real-time insight into behavioural patterns, enabling hyper-personalised offers that improve retention in crowded markets. Asia-Pacific banks run cloud platforms capable of supporting tens of millions of concurrent sessions, as illustrated by AIBank's micro-services core that serves more than 100 million customers. In parallel, North American lenders integrate cloud analytics with loyalty engines to cut churn that still affects over 60% of legacy institutions. Because finance data is highly regulated, vendors differentiate through in-platform encryption, audit trails, and data-residency controls that satisfy regulators while still allowing cross-channel orchestration. As customer lifetime value becomes a pivotal KPI, the finance cloud market gains further momentum from banks' willingness to replace ageing CRM tools with elastic, AI-ready alternatives.

Demand for Operational Efficiency in Financial Sector

Moving finance workloads to consumption-based clouds converts capital expenditure into variable operating cost, releasing cash for product innovation. Institutions that completed full cloud migrations report 20-30% reductions in month-end close cycles and similar gains in regulatory reporting speed. Automation natively embedded in cloud ERPs eliminates manual journals, while serverless compute handles unpredictable spikes in payment volumes without performance degradation. Discover Financial Services, for example, relies on a hybrid estate to flex resources during seasonal spending peaks. As margins tighten, cost-to-income ratios now appear on board dashboards alongside revenue, reinforcing the efficiency narrative that will continue to propel the finance cloud market.

Rise of Cloud-based Cyber Threats

Financial services remain the top target for sophisticated attacks, and cloud environments enlarge the threat surface. US regulators report escalating ransom incidents that disrupt critical payment infrastructures, prompting banks to double investments in zero-trust architectures and extended detection platforms. Migrating sensitive data without commensurate security uplift exposes institutions to regulatory fines that can exceed annual IT budgets. Cloud providers answer with confidential computing, hardware-rooted encryption, and sovereign-cloud blueprints, yet implementing these controls adds cost and complexity, muting short-term acceleration in the finance cloud market.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Push for Real-Time Transparency and Reporting

- GenAI-enabled Self-service Finance Analytics

- Legacy-core Integration Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The Financial Forecasting and Planning segment retained 38.3% revenue in 2024, reflecting the universal need for scenario modelling when economic volatility remains high. Cloud-based EPM suites let finance teams generate rolling forecasts across thousands of cost centres, elevating data-driven decision-making. Integrated driver-based models update profit outlooks instantly after rate or FX shocks, reinforcing migration urgency. Concurrently, Risk, Compliance, and RegTech is the fastest-growing solution line, advancing at 15.9% CAGR through 2030 on the back of DORA and comparable regimes. Vendors embed API-ready regulatory libraries so institutions can push granular transaction data to supervisors with one-click reporting. Continuous control monitoring features lower audit-prep workloads, translating compliance budgets directly into demand for the finance cloud market.

Core Accounting and General Ledger platforms remain indispensable, acting as system-of-record anchors for all other cloud finance modules. Treasury and Cash-Management tools gain new momentum as volatile funding markets prioritise real-time liquidity insight. Citigroup, for instance, expanded its cloud treasury workspace to aggregate global cash positions minute-by-minute. Payroll and Workforce Finance applications benefit from tight finance-HR convergence; Workday's latest release bundles headcount planning with spend analytics, underscoring how integrated suites improve enterprise alignment. As vendors package these capabilities under unified data fabrics, upsell pipelines expand, driving sustainable revenue streams within the finance cloud market.

Public clouds controlled 57.6% of 2024 revenue due to hyperscalers' global footprints, advanced security certifications, and continuous innovation roadmaps. Banks routinely adopt managed PaaS databases to accelerate new product rollouts without provisioning hardware. Yet dependence on a single provider raises resilience concerns, propelling Hybrid and Multi-Cloud uptake at 17.0% CAGR. European lenders, mindful of concentration risk outlined by regulators, increasingly split workloads across at least two vendors, while retaining ultra-low-latency trading engines on private clouds. Form3's payment platform exemplifies this strategy, abstracting routing logic so banks can toggle endpoints among clouds during outages.

Private clouds remain vital for use cases with stringent performance or data-sovereignty requirements. JPMorgan Chase is spending USD 2 billion on four new private cloud data centres that anchor latency-sensitive risk computations. Unified observability stacks and policy-as-code reduce operational friction across mixed estates, making hybrid truly seamless. Because regulatory discourse now explicitly references "exit plans," institutions favour containerised workloads and open APIs to avoid lock-in, a development that further broadens addressable opportunity for the finance cloud market.

The Finance Cloud Market Report is Segmented by Solution (Core Accounting and GL, Financial Forecasting and Planning, and More), Deployment Model (Public Cloud, Private Cloud, and Hybrid / Multi-Cloud), End-User (Banking, Insurance, Capital Markets, and More), Organization Size (Large Enterprises and Small and Medium Enterprises (SMEs)), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 41.0% of 2024 revenue thanks to deep technology budgets and regulatory clarity that fosters accelerated migration. The United States anchors the region, with JPMorgan Chase alone allocating USD 17 billion annually to tech and moving 6,000 applications to cloud platforms. Canada follows with open-banking guidelines that encourage secure API ecosystems, while Mexican banks adopt cloud to meet cross-border reporting standards. Public-private collaboration on cybersecurity and digital-identity frameworks further de-risks adoption, strengthening the finance cloud market in the region. Providers leverage dense data-centre footprints to meet sub-10-millisecond latency thresholds demanded by high-frequency traders.

Asia-Pacific is the fastest-growing territory at 16.2% CAGR through 2030. Government-backed digital-economy blueprints place cloud at the centre of financial-inclusion agendas, underpinning a regional digital-economy value expected to reach USD 1 trillion by 2030. China's AIBank demonstrates cloud scalability by serving over 100 million customers on a containerised platform. India's public-cloud policy now allows regulated entities to host core data offshore under strict encryption keys, unlocking broader hyperscaler adoption. Japan and Australia endorse Industry-Cloud models that deliver pre-certified compliance artefacts for local supervisory bodies. Coupled with rising fee-based revenue targets-APAC banks expect digital adjacencies to supply 40% of profit pools by 2030-these trends ensure sustained upside for the finance cloud market.

Europe accelerates cloud modernisation under DORA's operational-resilience mandate, affecting roughly 22,000 financial organisations. Germany, France, and the United Kingdom roll out shared testing frameworks for cyber-incident simulations, incentivising the adoption of platforms that automate evidence collection. Sovereign-cloud regions operated by large providers satisfy data-sovereignty clauses, while multi-vendor strategies mitigate systemic risk. South America charts high growth, powered by Brazil's branchless challenger banks such as Nubank, which posted USD 2 billion profit in 2024 while operating entirely on cloud infrastructure. Middle East and Africa adoption climbs swiftly; 83% of MENA financial firms now run cloud workloads and expect USD 21.14 million in annual savings within two years. Gulf Cooperation Council banks align national cloud mandates with ambitious digital transformation roadmaps, solidifying new demand pockets for the finance cloud market.

- Oracle Corporation(Netsuite)

- SAP

- Microsoft

- Salesforce

- IBM

- Workday

- Sage Intacct

- Unit4 / FinancialForce

- Intuit

- Anaplan

- Workiva

- BlackLine

- Coupa

- Xero

- FIS

- Fiserv

- Temenos

- Finastra

- Acumatica

- AWS

- Google Cloud

- Huawei

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Need for improved customer relationship management

- 4.2.2 Demand for operational efficiency in financial sector

- 4.2.3 Regulatory push for real-time transparency and reporting

- 4.2.4 GenAI-enabled self-service finance analytics

- 4.2.5 FinOps adoption to optimise cloud spending

- 4.2.6 Industry-cloud platforms for BFSI verticals

- 4.3 Market Restraints

- 4.3.1 Rise of cloud-based cyber threats

- 4.3.2 Legacy-core integration complexity

- 4.3.3 Talent gap in cloud-FinOps and data engineering

- 4.3.4 Vendor lock-in and GenAI cost overruns

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assessment of the Impact of Macroeconomic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Solution

- 5.1.1 Core Accounting and GL

- 5.1.2 Financial Forecasting and Planning

- 5.1.3 Risk, Compliance and Reg-Tech

- 5.1.4 Treasury and Cash-Management

- 5.1.5 Payroll and Workforce Finance

- 5.2 By Deployment Model

- 5.2.1 Public Cloud

- 5.2.2 Private Cloud

- 5.2.3 Hybrid / Multi-Cloud

- 5.3 By End-User

- 5.3.1 Banking

- 5.3.2 Insurance

- 5.3.3 Capital Markets

- 5.3.4 FinTech / Neo-banks

- 5.4 By Organisation Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises (SMEs)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Nigeria

- 5.5.5.2.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Oracle Corporation(Netsuite)

- 6.4.2 SAP

- 6.4.3 Microsoft

- 6.4.4 Salesforce

- 6.4.5 IBM

- 6.4.6 Workday

- 6.4.7 Sage Intacct

- 6.4.8 Unit4 / FinancialForce

- 6.4.9 Intuit

- 6.4.10 Anaplan

- 6.4.11 Workiva

- 6.4.12 BlackLine

- 6.4.13 Coupa

- 6.4.14 Xero

- 6.4.15 FIS

- 6.4.16 Fiserv

- 6.4.17 Temenos

- 6.4.18 Finastra

- 6.4.19 Acumatica

- 6.4.20 AWS

- 6.4.21 Google Cloud

- 6.4.22 Huawei

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

全球金融雲市場

全球金融雲市場 金融雲市場:2026年至2032年全球預測(依部署模式、應用程式類型、組織規模及最終用戶產業分類)

金融雲市場:2026年至2032年全球預測(依部署模式、應用程式類型、組織規模及最終用戶產業分類) 金融雲市場報告:按類型、部署模式、企業規模、應用程式和地區分類(2026-2034 年)

金融雲市場報告:按類型、部署模式、企業規模、應用程式和地區分類(2026-2034 年) 2026-2030年全球雲端金融營運自動化工具市場

2026-2030年全球雲端金融營運自動化工具市場 金融雲市場-2026-2031年預測

金融雲市場-2026-2031年預測 金融雲市場-全球產業規模、佔有率、趨勢、機會與預測:按雲端類型、服務、地區和競爭對手分類,2021-2031年

金融雲市場-全球產業規模、佔有率、趨勢、機會與預測:按雲端類型、服務、地區和競爭對手分類,2021-2031年 FinOps市場預測至2032年:按組件、解決方案類型、服務類型、部署模式、組織規模、最終用戶和地區分類的全球分析

FinOps市場預測至2032年:按組件、解決方案類型、服務類型、部署模式、組織規模、最終用戶和地區分類的全球分析 2025年全球金融雲市場報告

2025年全球金融雲市場報告 金融雲市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

金融雲市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測 金融雲市場規模、佔有率、成長分析(按解決方案、按服務、按部署、按公司規模、按應用、按最終用途、按地區)-2025 年至 2032 年產業預測

金融雲市場規模、佔有率、成長分析(按解決方案、按服務、按部署、按公司規模、按應用、按最終用途、按地區)-2025 年至 2032 年產業預測