|

市場調查報告書

商品編碼

1848321

單寧:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)Tannin - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

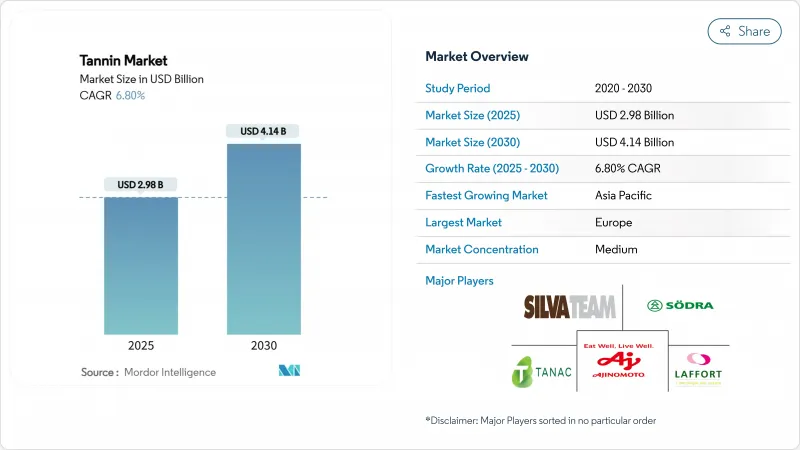

預計到 2025 年,單寧市場規模將達到 29.8 億美元,到 2030 年將達到 41.4 億美元,預測期內複合年成長率為 6.80%。

這項繁榮主要得益於皮革、葡萄酒、木質複合材料和特殊營養品等產業對天然材料的日益青睞。隨著監管日益嚴格,消費者對永續和環保產品的需求不斷成長,合成添加劑的使用量顯著減少。尤其是在農業廢棄物、樹皮和海藻等原料的利用方面,創新增強了供應鏈的韌性,並與循環經濟的目標相契合。這些進步不僅減少了對傳統原料的依賴,也有助於環境的永續性。此外,無鉻皮革、有機葡萄酒標準和無甲醛木材黏合劑的迅速普及,也證明了產業和消費者對生物基多酚的需求激增。儘管市場競爭依然溫和,但擁有先進萃取技術和垂直整合能力的公司正在脫穎而出,佔據明顯的優勢。這些先行企業不僅提高了營運效率,還獲得了高價契約,鞏固了其市場地位。在技術創新、永續性和消費者偏好轉變的共同推動下,這一發展趨勢預示著單寧市場長期前景光明。

全球單寧市場趨勢與洞察

皮革業對天然環保鞣劑的需求很高

隨著皮革產業將重點轉向永續鞣製,環保型植物鞣劑作為傳統鉻基化學品的替代品,需求顯著成長。歐盟的REACH法規收緊了對皮革加工中有害化學品使用的限制,促使製造商轉向天然替代品。在北美,美國環保署將某些鉻化合物列為致癌性後,植物來源鞣劑的普及速度加快。植物鞣革不僅在奢侈品市場享有溢價,也與領先時尚品牌的永續性最後加工不謀而合。這些品牌如今在其採購政策中優先考慮無鉻材料,既滿足了消費者的偏好,也符合監管要求。此外,先進生物整理系統的出現正在革新皮革加工,提供可生物分解的解決方案,在提升耐用性和美觀性的同時,也符合永續發展標準。這些行業範圍內的變化清晰地表明,消費者對永續性產品的需求日益成長,同時也響應了減少工業化學品使用的法規要求。推動這項變革的關鍵產業包括汽車內部裝潢建材、高檔皮革製品和鞋類,這些產業對永續的高品質材料的需求日益成長。此外,對循環經濟原則的日益重視也促使皮革產業朝著減少廢棄物和提高資源利用效率的方向發展,從而支持永續鞣革製程的轉型。

葡萄酒和飲料生產中單寧用量不斷增加

隨著釀酒商尋求提高葡萄酒的色彩穩定性、改善口感、最佳化陳年特性,同時還要滿足不斷變化的監管要求,釀酒單寧的需求正在顯著成長。在美國,酒精和菸草稅收貿易局 (TTB) 制定了明確的使用限量,允許紅葡萄酒中單寧的含量最高為每千加侖 24 磅,白葡萄酒中最高為每千加侖 6.4 GAE。這些標準化指南促進了整個產業的統一應用。在歐洲,歐洲食品安全局已核准在動物飼料中使用單寧酸,含量最高可達每公斤 15 毫克,將其用途擴展到傳統葡萄酒生產之外。在全球範圍內,國際葡萄與葡萄酒組織 (OIV) 透過制定植物來源(包括堅果、栗子、橡木和葡萄籽)的品質標準,使釀酒單寧的使用合法化。此外,美國食品藥物管理局(FDA)對某些化合物的「公認安全」(GRAS)認定,促進了它們在更廣泛的食品和飲料應用中的推廣。有機認證體系則透過為天然單寧提供高階市場機會,進一步加劇了市場分散化。

複雜的提取工藝限制了商業性規模生產。

單寧提取製程的技術複雜性和資金需求阻礙了市場擴張,小型生產商和新進入者深受其害。美國專利商標局登記的200多項單寧提取方法專利證明了高效生產所需的技術複雜性。國際標準化組織(ISO)對單寧產品製定了嚴格的品質標準,要求對提取參數進行精確控制,這對缺乏尖端設備的公司構成了挑戰。同時,歐洲藥品管理局(EMA)的《藥品單寧良好生產規範》(GMP)要求先進的品管和經過驗證的萃取方法。同樣,美國食品藥物管理局(FDA)現行的《膳食補充劑良好生產規範》(GMP)指南對植物萃取物提出了詳細的要求,推高了合規成本並增加了技術難度。這些監管和技術障礙不僅延緩了市場准入,也推高了生產成本。這可能會削弱單寧基產品與合成替代品的競爭力,尤其是在價格敏感型產業和新興市場。

細分市場分析

2024年,植物來源單寧將佔據市場主導地位,市佔率高達82.43%。這得益於數十年來不斷改進的提取方法和可靠的供應鏈。這些單寧主要來自奎布拉喬樹、相思樹、栗樹和橡樹等傳統樹種。完善的農業實踐和加工設施進一步鞏固了其市場領先地位,確保了產品的一流品質和穩定供應。美國林務局對從美國本土森林中提取樹皮單寧進行了深入研究,為建立可靠的供應鏈鋪平了道路。同時,歐洲森林協會制定了永續樹皮採伐指南,以平衡森林活力與單寧原料需求。這些傳統來源已被監管機構廣泛認可,美國食品藥物管理局(FDA)已認定某些植物來源寧可安全用於食品。此外,國際森林研究組織聯合會也支持永續的採購方式,確保在不損害環境標準的前提下,單寧供應穩定。

褐藻已成為成長最快的來源,預計到2030年將以8.04%的複合年成長率成長。這種快速成長歸功於褐藻中優異的間苯三酚生物活性及其在醫藥領域日益成長的應用。美國海洋暨大氣總署(NOAA)已將褐藻養殖認定為一種永續的海洋資源,其收穫不會對環境造成損害。歐洲海洋和漁業基金也支持這一觀點,並資助海洋生物技術研究,重點關注間苯三酚的萃取及其在醫藥和營養保健品領域的應用。在日本,日本海洋地球科學技術廳(JAMSTEC)率先採用先進的養殖方法,確保褐藻間苯三酚的穩定全年生產。國際海藻協會(ISCA)制定了這些海洋來源單寧的品質標準,促進了其在高階應用中的整合。這些進展不僅使褐藻成為小眾應用領域備受追捧的資源,而且還解決了與陸生植物收穫相關的永續性挑戰。

區域分析

到2024年,歐洲將佔據全球34.11%的市場佔有率,這得益於嚴格的環境法規和強大的產業框架,這些都為天然單寧的應用提供了支持。歐洲食品安全局已製定了明確的食品、飼料和工業應用中單寧的安全通訊協定,為吸引投資提供了監管確定性。同時,歐洲藥品管理局已批准某些單寧化合物作為藥品,從而開拓了利潤豐厚的市場。歐盟的REACH法規限制了工業中危險化學品的使用,並強制要求轉向更安全的天然替代品,例如單寧。歐盟委員會的循環經濟行動計畫鼓勵將農業和廢棄物轉化廢棄物生物基化學品。從金融角度來看,歐洲投資銀行正在支持包括單寧提取和加工在內的永續技術企業,從而加強該地區的基礎設施建設。

亞太地區正經歷快速成長,預計到2030年將以7.74%的複合年成長率成長,這主要得益於快速的工業化進程和有利於天然產品使用的法規的不斷完善。中國國家發展和改革委員會主導的戰略發展規劃重點發展生物基化學品,為單寧的生產鋪平了道路。在印度,化學和肥料部推出了與生產掛鉤的激勵措施,以加強天然產品的生產,特別是從農產品中提取單寧。日本厚生勞動省擴大了機能性食品的範圍,將各種形式的單寧基成分納入其中。東南亞國家聯盟(ASNAN)制定了天然產品的區域標準,以簡化單寧原料的貿易。在澳大利亞,農業部啟動了有機認證計劃,為天然單寧的高階市場鋪平了道路,並使區域市場格局更加多元化。

北美市場正穩步成長,這主要得益於有利於天然替代品而非合成替代品的監管措施。美國食品藥物管理局(FDA)對單寧化合物的GRAS認證,為其在食品飲料產業的應用鋪平了道路。美國環保署(EPA)制定的甲醛排放標準也支持在木材加工中使用單寧基黏合劑。同時,美國酒精和菸草稅收貿易局(ATTB)完善了葡萄酒處理材料的監管規定,並制定了明確的單寧使用指南和限制,力求在創新與安全之間取得平衡。在原料豐富的南美洲,巴西正主導永續林業的投資,並持續強化其單寧供應鏈。在中東和非洲,受倡導農業廢棄物回收的國際計畫以及人們對循環經濟理念日益成長的認知的推動,單寧市場也呈現出蓬勃發展的態勢。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 皮革產業對天然環保鞣劑的需求日益成長

- 葡萄酒和飲料生產中單寧用量不斷增加

- 食品業對永續和天然成分的偏好

- 木材膠粘劑和塑合板行業的成長

- 永續提取自農業廢棄物和樹皮提取物

- 單寧的抗氧化特性和其他特性使其在膳食補充劑中得到應用。

- 市場限制

- 複雜的提取工藝限制了商業化規模生產。

- 提取產量的區域差異

- 嚴格的FDA和歐盟法規增加了合規成本。

- 來自合成替代品的競爭

- 供應鏈分析

- 監理展望

- 波特五力模型

- 新進入者的威脅

- 買方/消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 按原料

- 植物

- 褐藻

- 透過使用

- 食品/飲料

- 藥品和營養補充劑

- 皮革產業

- 木材工業

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 北美其他地區

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 亞太其他地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東和非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市場排名分析

- 公司簡介

- Sodra Skogsagarna

- Ajinomoto Co., Inc

- Silvateam Group

- Laffort Holding

- TANAC

- Ulrich Holding GmbH

- Esseco Group Srl

- Tanin dd Sevnica

- Tannin Corporation

- NTE Company(Pty)Limited

- Gallotannin Co. Ltd

- Forestal Quebracho SA

- Polson Ltd.

- UCL Company(Pty)Ltd

- Silvateam group

- Xi'an Prius Biological Engineering Co.,Ltd

- Forestal Mimosa Limited

- ChemFaces Biochemical Co., Ltd.

- Glentham Life Sciences Limited

- FUJIFILM Wako Pure Chemical Corporation

第7章 市場機會與未來展望

The tannin market size reached USD 2.98 billion in 2025 and is projected to reach USD 4.14 billion by 2030, expanding at a compound annual growth rate (CAGR) of 6.80% during the forecast period.

This upswing is largely fueled by a rising inclination towards natural inputs in sectors like leather, wine, wood composites, and specialty nutrition. As regulations tighten and consumers increasingly demand sustainable, eco-friendly products, there's a pronounced shift away from synthetic additives. Innovations in sourcing, especially with agro-waste, bark, and seaweed, bolster supply chain resilience and resonate with circular economy goals. Such strides not only lessen reliance on conventional raw materials but also champion environmental sustainability. Furthermore, the swift embrace of chrome-free leather, organic wine standards, and formaldehyde-free wood adhesives underscores the burgeoning appetite for bio-based polyphenols in both industrial and consumer realms. While market competition remains moderate, firms excelling in extraction technology and pursuing vertical integration are carving out a distinct advantage. These pioneers are not only enhancing operational efficiencies but also clinching premium contracts and solidifying their market stance. This trajectory paints a bullish long-term outlook for the tannin market, propelled by innovation, sustainability, and shifting consumer tastes.

Global Tannin Market Trends and Insights

High demand for natural and eco-friendly tanning agents in leather industry

As the leather industry pivots towards sustainable tanning, there's a notable surge in demand for vegetable tannins, seen as eco-friendly alternatives to traditional chromium-based chemicals. Stricter limitations on hazardous chemicals in leather processing, driven by the European Union's REACH regulation, are pushing manufacturers towards natural substitutes. In North America, the U.S. Environmental Protection Agency's designation of certain chromium compounds as carcinogenic has hastened the shift to plant-based tanning agents. Reports highlight that vegetable-tanned leather not only fetches a premium in luxury markets but also resonates with the sustainability ethos of leading fashion brands. These brands are now prioritizing chrome-free materials in their sourcing policies, aligning with both consumer preferences and regulatory demands. Moreover, the advent of advanced bio-finishing systems is transforming leather processing, offering biodegradable solutions that boost durability and aesthetic appeal while meeting sustainability benchmarks. This industry-wide shift underscores a response to heightened consumer demand for eco-friendly products and regulatory pushes to curtail industrial chemical use. Key sectors championing this change include automotive upholstery, luxury leather goods, and footwear, all witnessing a rising appetite for sustainable, high-quality materials. Furthermore, a growing emphasis on circular economy principles is steering the leather industry towards waste minimization and resource efficiency, bolstering the move to sustainable tanning.

Increasing use of tannins in wine and beverage production

The demand for oenological tannins is witnessing significant growth as winemakers aim to improve color stability, enhance mouthfeel, and optimize aging characteristics, all while adhering to evolving regulatory requirements. In the United States, the Alcohol and Tobacco Tax and Trade Bureau (TTB) has established precise usage limits, allowing up to 24 pounds of tannins per 1000 gallons in red wine and 6.4 GAE per 1000 gallons in white wine. These standardized guidelines are driving consistent adoption across the industry. In Europe, the European Food Safety Authority has approved tannic acid for use in animal feed at concentrations up to 15 mg/kg, thereby expanding its applications beyond traditional wine production. Globally, the International Organisation of Vine and Wine (OIV) has legitimized the use of oenological tannins by defining quality standards for botanical sources such as nutgalls, chestnut, oak, and grape seeds. Additionally, the FDA's GRAS (Generally Recognized As Safe) designation for specific tannin compounds has facilitated their integration into broader food and beverage applications. Organic certification programs further contribute to market segmentation by creating premium opportunities for naturally sourced tannins.

Complex extraction processes limit commercial scaling

Market expansion faces hurdles due to the technical intricacies and capital demands of tannin extraction processes, with smaller producers and newcomers feeling the pinch. Over 200 patents on tannin extraction methods, recorded by the U.S. Patent and Trademark Office, underscore the technological finesse needed for efficient production. The International Organization for Standardization has set stringent quality benchmarks for tannin products, necessitating meticulous control over extraction parameters. This poses challenges for firms without cutting-edge equipment. Meanwhile, the European Medicines Agency's Good Manufacturing Practice mandates for pharmaceutical-grade tannins call for advanced quality control and validated extraction methods. Similarly, the FDA's Current Good Manufacturing Practice guidelines for dietary supplements stipulate detailed botanical extraction requirements, driving up compliance costs and adding to technical challenges. Such regulatory and technical hurdles not only decelerate market entry but also inflate production expenses. This could hinder the competitiveness of tannin-based products, especially against synthetic counterparts, in price-sensitive sectors and emerging markets.

Other drivers and restraints analyzed in the detailed report include:

- Tannin's antioxidant and other properties drives its use in nutraceuticals

- Growth in the wood adhesive and particleboard industry

- Variability in extraction yiels across geography

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2024, plant-based tannins dominate the market with an 82.43% share, a testament to decades of refined extraction methods and dependable supply chains. These tannins are sourced from traditional favorites like quebracho, acacia, chestnut, and oak. This market leadership is bolstered by robust agricultural practices and processing facilities, ensuring top-notch quality and dependable supply. The U.S. Department of Agriculture's Forest Service has conducted in-depth studies on extracting bark tannins from the nation's forests, paving the way for a solid supply chain. Meanwhile, the European Forest Institute has rolled out sustainable bark harvesting guidelines, balancing forest vitality with the demand for tannin raw materials. These traditional sources enjoy broad regulatory acceptance, with the FDA deeming specific plant-derived tannins safe for food use. Furthermore, the International Union of Forest Research Organizations champions sustainable sourcing practices, ensuring a steady supply of tannins without compromising environmental standards.

Brown algae is emerging as the fastest-growing source, boasting an 8.04% CAGR projected through 2030. This surge is attributed to the algae's superior phlorotannin bioactivity and its burgeoning role in pharmaceuticals. The National Oceanic and Atmospheric Administration vouches for brown algae cultivation, deeming it a sustainable marine resource that can be harvested without harming the environment. Backing this, the European Maritime and Fisheries Fund is funding research into marine biotechnologies, spotlighting phlorotannin extraction for both pharmaceutical and nutraceutical applications. In Japan, the Agency for Marine-Earth Science and Technology has pioneered advanced cultivation methods, ensuring brown algae consistently yield phlorotannins year-round. The International Seaweed Association has set quality benchmarks for these marine-derived tannins, facilitating their integration into premium applications. Such advancements not only elevate brown algae as a sought-after source for niche applications but also address the sustainability challenges tied to harvesting terrestrial plants.

The Tannin Market Report is Segmented by Source (Plant and Brown Algae); Application (Food and Beverage, Pharmaceutical and Nutraceutical, Leather Industry, Wood Industry, and Others); and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

In 2024, Europe commands a dominant 34.11% market share, bolstered by stringent environmental regulations and a robust industrial framework that champions natural tannin applications. The European Food Safety Authority has set forth definitive safety protocols for tannins in food, feed, and industrial uses, fostering a climate of regulatory certainty that attracts investments. Meanwhile, the European Medicines Agency has greenlit specific tannin compounds for pharmaceutical use, carving out lucrative market niches. The EU's REACH regulation curbs hazardous chemicals in industries, mandating a shift towards safer, natural alternatives like tannins. Further underscoring the region's commitment, the European Commission's Circular Economy Action Plan champions the transformation of agricultural and forestry waste into bio-based chemicals. On the financial front, the European Investment Bank is backing sustainable tech ventures, including tannin extraction and processing, bolstering the region's infrastructure.

Asia-Pacific is on a rapid ascent, projected to grow at a 7.74% CAGR through 2030, fueled by swift industrialization and evolving regulations that endorse natural product uses. China's strategic development plans, spearheaded by the National Development and Reform Commission, now spotlight bio-based chemicals, paving the way for tannin production. In India, the Ministry of Chemicals and Fertilizers rolls out production-linked incentives, bolstering the manufacturing of natural products, notably tannin extraction from agricultural byproducts. Japan's Ministry of Health, Labour and Welfare broadens the horizon for functional foods, now embracing tannin-based ingredients in varied formats. The Association of Southeast Asian Nations sets the stage with regional standards for natural products, streamlining trade for tannin materials. Down under, Australia's Department of Agriculture launches organic certification programs, paving the way for a premium market for naturally sourced tannins, thus diversifying the regional market landscape.

North America charts a steady growth trajectory, driven by regulatory measures that champion natural substitutes over synthetic ones. The U.S. Food and Drug Administration's GRAS determinations for tannin compounds pave their way into the food and beverage sector. The U.S. Environmental Protection Agency's standards on formaldehyde emissions bolster the case for tannin-based adhesives in wood manufacturing. Meanwhile, the Alcohol and Tobacco Tax and Trade Bureau refines regulations on wine treating materials, setting clear guidelines and limits for tannin use, balancing innovation with safety. South America, with its rich tapestry of raw material sources, sees Brazil spearheading investments in sustainable forestry, fortifying tannin supply chains. In the Middle East and Africa, there's a burgeoning interest, spurred by international programs advocating agricultural waste valorization and a rising consciousness of circular economy tenets.

- Sodra Skogsagarna

- Ajinomoto Co., Inc

- Silvateam Group

- Laffort Holding

- TANAC

- Ulrich Holding GmbH

- Esseco Group Srl

- Tanin d.d. Sevnica

- Tannin Corporation

- NTE Company (Pty) Limited

- Gallotannin Co. Ltd

- Forestal Quebracho S.A.

- Polson Ltd.

- UCL Company (Pty) Ltd

- Silvateam group

- Xi'an Prius Biological Engineering Co.,Ltd

- Forestal Mimosa Limited

- ChemFaces Biochemical Co., Ltd.

- Glentham Life Sciences Limited

- FUJIFILM Wako Pure Chemical Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 High Demand for Natural and Eco-Friendly Tanning Agents in Leather Industry

- 4.2.2 Increasing Use of Tannins in Wine and Beverage Production

- 4.2.3 Preference of Sustainable, And Natural Ingredients in Food Industry

- 4.2.4 Growth in the Wood Adhesive and Particleboard Industry

- 4.2.5 Sustainable Sourcing from Agro-Waste and Bark Extracts

- 4.2.6 Tannin's Antioxidant and Other Properties Drives Its Use in Nutraceuticals

- 4.3 Market Restraints

- 4.3.1 Complex Extraction Processes Limit Commercial Scaling

- 4.3.2 Variability In Extraction Yield Across Geography

- 4.3.3 Stringent FDA And EU Regulation Increase Compliance Costs

- 4.3.4 Competition From Synthetic Alternatives

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Source

- 5.1.1 Plant

- 5.1.2 Brown Algae

- 5.2 By Application

- 5.2.1 Food and Beverage

- 5.2.2 Pharmaceutical and Nutraceutical

- 5.2.3 Leather Industry

- 5.2.4 Wood Industry

- 5.2.5 Others

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 Italy

- 5.3.2.4 France

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 Australia

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 South Africa

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 United Arab Emirates

- 5.3.5.4 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Ranking Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials (if available), Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Sodra Skogsagarna

- 6.4.2 Ajinomoto Co., Inc

- 6.4.3 Silvateam Group

- 6.4.4 Laffort Holding

- 6.4.5 TANAC

- 6.4.6 Ulrich Holding GmbH

- 6.4.7 Esseco Group Srl

- 6.4.8 Tanin d.d. Sevnica

- 6.4.9 Tannin Corporation

- 6.4.10 NTE Company (Pty) Limited

- 6.4.11 Gallotannin Co. Ltd

- 6.4.12 Forestal Quebracho S.A.

- 6.4.13 Polson Ltd.

- 6.4.14 UCL Company (Pty) Ltd

- 6.4.15 Silvateam group

- 6.4.16 Xi'an Prius Biological Engineering Co.,Ltd

- 6.4.17 Forestal Mimosa Limited

- 6.4.18 ChemFaces Biochemical Co., Ltd.

- 6.4.19 Glentham Life Sciences Limited

- 6.4.20 FUJIFILM Wako Pure Chemical Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

2026年全球單寧市場報告

2026年全球單寧市場報告 單寧酸粉末市場按類型、純度、應用和通路分類 - 全球預測 2026-2032

單寧酸粉末市場按類型、純度、應用和通路分類 - 全球預測 2026-2032 單寧市場規模、佔有率和成長分析(按來源、產品、應用和地區分類)—2026-2033年產業預測

單寧市場規模、佔有率和成長分析(按來源、產品、應用和地區分類)—2026-2033年產業預測 單寧酸粉:全球市佔率及排名、總收入及需求預測(2025-2031年)單寧市場按類型、來源、形態、應用和分銷管道分類-2025-2032年全球預測

單寧酸粉:全球市佔率及排名、總收入及需求預測(2025-2031年)單寧市場按類型、來源、形態、應用和分銷管道分類-2025-2032年全球預測 單寧市場報告,按來源(植物、褐藻)、產品(水解單寧、縮合單寧、褐藻單寧)、應用(食品和飲料、皮革鞣製、木材黏合劑等)和地區分類,2025 年至 2033 年飼料級單寧酸市場按產品類型、成分類型、功能用途、銷售管道和動物類型分類-2025-2030 年全球預測

單寧市場報告,按來源(植物、褐藻)、產品(水解單寧、縮合單寧、褐藻單寧)、應用(食品和飲料、皮革鞣製、木材黏合劑等)和地區分類,2025 年至 2033 年飼料級單寧酸市場按產品類型、成分類型、功能用途、銷售管道和動物類型分類-2025-2030 年全球預測 單寧市場分析及預測(至2034年):類型、產品、應用、技術、最終用戶、形式、材料類型、製程、成分、功能

單寧市場分析及預測(至2034年):類型、產品、應用、技術、最終用戶、形式、材料類型、製程、成分、功能 丹寧的全球市場:市場規模·佔有率·趨勢,產業分析 (各原料·各產品種類·各用途·各地區),未來預測 (2025年~2034年)

丹寧的全球市場:市場規模·佔有率·趨勢,產業分析 (各原料·各產品種類·各用途·各地區),未來預測 (2025年~2034年) 單寧酸粉全球市場,實績及預測(2019-2030)

單寧酸粉全球市場,實績及預測(2019-2030)