|

市場調查報告書

商品編碼

1846257

汽車電源模組封裝:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)Automotive Power Module Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

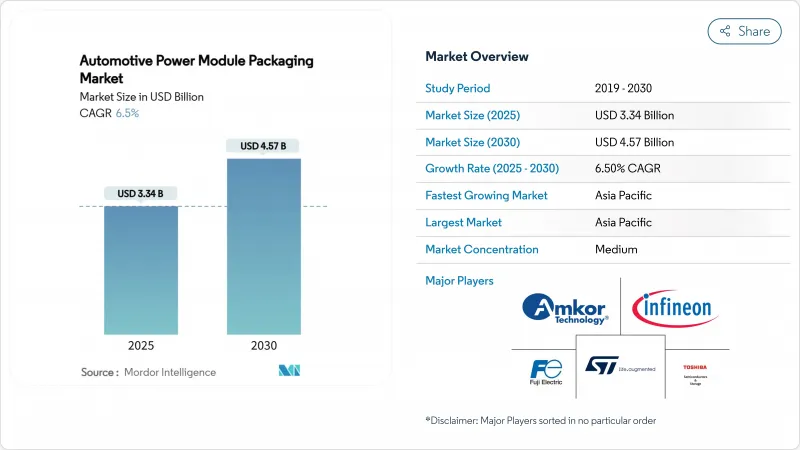

預計到 2025 年,汽車電源模組封裝市場規模將達到 33.4 億美元,到 2030 年將達到 45.7 億美元,複合年成長率為 6.5%。

隨著汽車製造商加速推進電氣化進程、推動高壓架構的大規模生產以及對寬能能隙帶元件先進溫度控管解決方案的需求,汽車功率模組封裝市場正在不斷擴張。對200毫米碳化矽晶圓廠投資的增加、縮短開發週期的夥伴關係以及日益嚴格的排放法規,都在強化市場的長期需求。專注於無打線接合合互連、雙面冷卻和銀燒結技術的供應商在牽引逆變器、車用充電器和DC-DC轉換器設計領域佔有優勢。同時,碳化矽基板供應的限制和分散的認證規則仍然是市場發展的阻礙。

全球汽車電源模組封裝:市場趨勢與洞察

電動車和混合動力汽車產量快速成長

預計到2024年,全球純電動和混合動力汽車產量將大幅成長,汽車應用已佔碳化矽需求的70%以上。特斯拉Cybertruck的電源轉換器展示了800V平台如何使電壓應力翻倍,並增加對溫度控管的需求。包括ZF的300kW eBeam車橋在內的商用車專案進一步擴大了加固型封裝的應用範圍。

向SiC和GaN寬能能隙元件的轉變

第四代碳化矽 (SiC) MOSFET 的結溫現已超過 200°C,這增加了對銅夾、銀燒結和直接晶粒冷卻的需求。英飛凌預測,2025 年將是汽車級氮化鎵 (GaN) 的轉捩點,尤其是在車載充電器和高頻直流-直流轉換器方面。 SiC基板供應瓶頸主要集中在向 200 毫米晶圓的過渡以及為穩定產能而達成的多供應商協議上。

缺乏標準化的認證通訊協定

由於不同地區的原始設備製造商 (OEM) 對 AEC-Q100、AEC-Q101 和 AEC-Q200 的解讀各不相同,電力電子供應商面臨著反覆測試的困境,導致產品上市時間延長,一次性成本增加。國際電工委員會 (IECQ)推出了汽車認證計劃 (AQP) 以統一認證流程,但該計劃的實施情況並不均衡。

細分市場分析

智慧功率模組將佔2024年銷量的38.1%,並將繼續成為入門級電動車和混合動力汽車的首選。儘管成本較高,但由於高階和商用平台優先考慮效率,碳化矽(SiC)功率模組的複合年成長率預計仍將達到15.4%。到2030年,SiC元件的汽車功率模組封裝市場預計將再成長7.5個百分點。 ROHM和Valeo的TRCDRIVE封裝表明,SiC能夠在不影響散熱性能的前提下實現逆變器的小型化。同時,氮化鎵(GaN)已滲透到車載充電器中,其高頻開關特性克服了電流限制。 IGBT和FET模組繼續用於中程和輔助負載,三菱馬達最近推出的一款產品在提高防潮性能的同時,將開關損耗降低了15%。

隨著汽車原始設備製造商 (OEM) 在成本、效率和供貨能力之間尋求平衡,汽車功率模組封裝市場持續多元化發展。隨著 200 毫米晶圓實現量產以及垂直整合策略的日益成熟,碳化矽 (SiC) 的成本預計將會下降。因此,能夠提供設計工具、閘極驅動器和熱最佳化封裝等整合解決方案的供應商,預計將贏得多年期平台合約。隨著客戶對承包模組化子系統的需求不斷成長,整合設備製造商和組裝專家之間的競爭差距可能會縮小。

到2024年,電壓最高600V的系統將維持44.3%的市場佔有率,這主要得益於現有400V乘用車平台的普及。然而,在汽車功率模組封裝市場,601-1200V電壓頻寬的成長速度最快,複合年成長率達6.9%,反映出市場正向800V拓樸結構轉變,進而縮短快速充電時間。安波福解釋了絕緣挑戰和爬電距離要求如何提升了堅固型封裝的價值。電壓高於1200V的模組仍屬於小眾市場,主要面向重型車輛和基礎設施應用。

更高的電壓需求推動了更厚絕緣凝膠、低電感銅夾以及額定電壓超過 1.5 kV 的壓入式引腳的研發。英飛凌的 1200 V CoolSiC MOSFET 已被 Forvia Hella 應用於其 800 V DC-DC 轉換器,這標誌著平台技術的轉變。隨著 OEM 廠商將下一代高壓域控制器作為標準,能夠確保局部放電耐久性和現場故障分析的封裝供應商有望贏得規範制定權。

汽車功率模組封裝市場按模組類型(IPM、SiC 功率模組、GaN 功率模組、其他)、額定功率(最高 600V、601-1200V、其他)、封裝技術(打線接合、無引線打線接合合/功率覆蓋、其他)、驅動類型(BEV、HEV、PHEV、FCEV-DC轉換器、輔助/空調/EPS)和地區進行細分。

區域分析

預計亞太地區在2024年將維持57.2%的市場佔有率,並在2030年之前維持8.9%的最高複合年成長率。中國的雙軌制信用政策和規模優勢吸引了大量碳化矽投資,其中包括英飛凌在馬來西亞投資20億美元建設的200毫米晶圓廠,該晶圓廠提升了該地區的產能韌性。涵蓋基板、金屬化漿料和封裝材料的本地化供應鏈縮短了前置作業時間並降低了成本。

Onsemi 投資 20 億美元在捷克共和國建立了一條端到端的 SiC 生產線,確保從晶圓到組件的控制,減少對進口的依賴,而聯邦製造業扣除額也鼓勵了在美國進行組件組裝。

在歐洲,關注的焦點是高階電動車品牌和更嚴格的排放法規。維特斯科科技公司投資5.76億歐元(約6.5億美元)擴大在奧斯特拉瓦的先進電子產品生產,體現了該公司對該地區電氣化發展勢頭的信心。區域多元化措施正匯聚成一股力量,旨在降低單一區域的風險,並促進技術轉讓,從而提升全球品質標準。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 電動車和混合動力汽車產量快速成長

- 向SiC和GaN寬能能隙元件的轉變

- 車輛電氣化需要更高功率密度的模組

- 嚴格的全球廢氣排放法規

- OEM採用無焊接線/頂部冷卻封裝

- 採用整合功率模組的電池到包裝一體化架構

- 市場限制

- 缺乏標準化的認證通訊協定

- SiC/GaN基板高成本且供應受限

- 新興800V平台的溫度控管局限性

- 碳化矽供應鏈可能有供給能力

- 宏觀經濟因素的影響

- 價值鏈分析

- 監管狀況

- 技術展望

- 波特五力分析

- 買方的議價能力

- 供應商的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 按模組類型

- 智慧型電源模組(IPM)

- SiC功率模組

- 氮化鎵功率模組

- IGBT模組

- FET模組

- 額定功率

- 最高可達 600 伏

- 601~1200 V

- 1200伏特或以上

- 依封裝技術

- 打線接合

- 引線鍵結/電源覆蓋層

- 壓入配合/直接壓入晶粒

- PCB嵌入

- 依推進類型

- 純電動車(BEV)

- 混合動力汽車(HEV)

- 插電式混合動力車(PHEV)

- 燃料電池電動車(FCEV)

- 按車輛類型

- 搭乘用車

- 輕型商用車

- 大型商用車輛和巴士

- 透過使用

- 牽引逆變器

- 車用充電器

- 直流-直流轉換器

- 輔助/氣候/EPS

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 其他南美

- 歐洲

- 德國

- 法國

- 英國

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略舉措

- 市佔率分析

- 公司簡介

- Amkor Technology, Inc.

- Kulicke & Soffa Industries, Inc.

- Powertech Technology Inc.(PTI)

- Infineon Technologies AG

- STMicroelectronics NV

- Fuji Electric Co., Ltd.

- Toshiba Electronic Devices & Storage Corporation

- SEMIKRON Danfoss GmbH & Co. KG

- JCET Group Co., Ltd.

- StarPower Semiconductor Ltd.

- Mitsubishi Electric Corporation

- ROHM Co., Ltd.

- onsemi Corporation

- Nexperia BV

- Wolfspeed, Inc.

- Microchip Technology Inc.

- Littelfuse, Inc.(IXYS)

- Vitesco Technologies Group AG

- Vincotech GmbH

- CISSOID SA

- Hitachi Astemo, Ltd.

- Danfoss Silicon Power GmbH

- BYD Semiconductor Co., Ltd.

- Dynex Semiconductor Ltd.

- Shenzhen BASiC Semiconductor Ltd.

第7章 市場機會與未來展望

The automotive power module packaging market size reached USD 3.34 billion in 2025 and is forecast to climb to USD 4.57 billion by 2030, reflecting a compound annual growth rate (CAGR) of 6.5%.

The automotive power module packaging market is expanding because automakers accelerated electrification programs, pushed higher voltage architectures into volume production, and demanded advanced thermal-management solutions for wide-bandgap devices. Rising investments in 200 mm SiC wafer fabs, partnerships that compress development cycles, and tighter emission standards collectively reinforce long-term demand. Suppliers that master wire-bondless interconnects, double-sided cooling, and silver sintering are securing design wins in traction inverters, on-board chargers, and DC-DC converters. Meanwhile, supply constraints for SiC substrates and fragmented qualification rules remain headwinds.

Global Automotive Power Module Packaging Market Trends and Insights

Rapid EV and HEV production growth

Global battery-electric and hybrid output climbed sharply in 2024, and automotive applications already accounted for more than 70% of SiC demand. Tesla's Cybertruck power converter illustrated how 800 V platforms double voltage stresses and intensify thermal management needs. Tier-1 suppliers such as BorgWarner reported 47% year-on-year eProduct sales growth, signaling that established drivetrain specialists are pivoting resources toward high-density modules.Commercial vehicle programs, including ZF's 300 kW eBeam axle, further widen the addressable base for ruggedized packaging.

Shift toward SiC and GaN wide-bandgap devices

Fourth-generation SiC MOSFETs now sustain junction temperatures above 200 °C, intensifying the need for copper clips, silver sintering, and direct die cooling. Infineon forecasts 2025 as an inflection year for automotive GaN, especially in on-board chargers and high-frequency DC-DC converters. Supply bottlenecks for SiC substrates sharpened focus on 200 mm wafer transitions and on multi-source agreements that stabilize capacity.

Lack of standardized qualification protocols

Power-electronics suppliers faced repeated test loops because AEC-Q100, AEC-Q101, and AEC-Q200 were interpreted differently by regional OEMs, prolonging time-to-market and inflating non-recurring expenses. IECQ launched its Automotive Qualification Programme to harmonize procedures, yet adoption remained uneven.

Other drivers and restraints analyzed in the detailed report include:

- Vehicle electrification demands higher power-density modules

- Stringent global emission regulations

- High cost and supply constraints of SiC/GaN substrates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Intelligent Power Modules held 38.1% of 2024 revenue and remained the volume choice for entry-level EVs and hybrids. SiC Power Modules, though costlier, achieved 15.4% CAGR forecasts as premium and commercial platforms prioritized efficiency. The automotive power module packaging market size for SiC devices is projected to capture an additional 7.5 percentage-point share by 2030. ROHM and Valeo's TRCDRIVE pack showed how SiC enables inverter downsizing without thermal compromise. Meanwhile, GaN penetrated on-board chargers where high-frequency switching outweighed current limits. IGBT and FET modules continue to serve mid-range and auxiliary loads, and recent Mitsubishi Electric releases reduced switching losses by 15% while extending moisture tolerance.

Market diversification persisted across the automotive power module packaging market as OEMs balanced cost, efficiency, and availability. SiC cost declines are expected once 200 mm wafers reach scale and vertical-integration strategies mature. Hence, suppliers that bundle design tools, gate drivers, and thermally optimized housings are positioning themselves to capture multi-year platform awards. The competitive split between integrated device makers and specialized assembly firms is likely to narrow as customers demand turnkey module sub-systems.

Systems up to 600 V retained a 44.3% share in 2024, anchored by existing 400 V passenger-car platforms. However, the 601-1200 V band is the automotive power module packaging market's fastest climber at 6.9% CAGR, mirroring the shift to 800 V topologies that cut fast-charging times. Aptiv outlined insulation challenges and creepage requirements that raise the value of robust packaging. Above-1200V modules remain niche, targeting heavy-duty and infrastructure roles.

Higher voltage demands intensified the development of thicker insulation gels, copper clips with lower inductance, and press-fit pins rated beyond 1.5 kV. Infineon's 1200 V CoolSiC MOSFETs were selected by Forvia Hella for 800 V DC-DC converters, underscoring the platform shift. Packaging suppliers that guarantee partial discharge endurance and field-failure analytics will win specifications as OEMs standardize on next-generation high-voltage domain controllers.

Automotive Power Module Packaging Market is Segmented by Module Type (IPM, Sic Power Module, Gan Power Module, and More), Power Rating (Up To 600V, 601-1200V, and More), Packaging Technology (Wire-Bond, Wire-bondless/Power Overlay, and More), Propulsion Type (BEV, HEV, PHEV, and FCEV), Vehicle Type (Passenger Cars, and More), Application (Traction Inverter, On-Board Charger, DC-DC Converter, Auxiliary/Climate/EPS), and Geography.

Geography Analysis

Asia-Pacific retained a 57.2% share in 2024 and posted the highest outlook at 8.9% CAGR to 2030. China's dual-credit rules and scale advantages drew major SiC investments, including Infineon's USD 2 billion 200 mm fab in Malaysia that addressed regional capacity resilience. Local supply chains spanning substrates, metallization pastes, and molding compounds shortened lead times and trimmed costs.

North American demand accelerated as domestic OEMs unveiled new 800 V pickups and SUVs. onsemi committed USD 2 billion to build an end-to-end SiC line in the Czech Republic, ensuring wafer-to-module control and reducing import dependency. Federal manufacturing tax credits also encouraged module assembly within the United States.

Europe focused on premium EV brands and strict emissions mandates. Vitesco Technologies invested EUR 576 million (USD 650 million) to expand advanced-electronics production in Ostrava, signaling confidence in regional electrification momentum. Collectively, regional diversification initiatives are diluting single-region risk and fostering technology transfers that elevate global quality benchmarks.

- Amkor Technology, Inc.

- Kulicke & Soffa Industries, Inc.

- Powertech Technology Inc. (PTI)

- Infineon Technologies AG

- STMicroelectronics N.V.

- Fuji Electric Co., Ltd.

- Toshiba Electronic Devices & Storage Corporation

- SEMIKRON Danfoss GmbH & Co. KG

- JCET Group Co., Ltd.

- StarPower Semiconductor Ltd.

- Mitsubishi Electric Corporation

- ROHM Co., Ltd.

- onsemi Corporation

- Nexperia B.V.

- Wolfspeed, Inc.

- Microchip Technology Inc.

- Littelfuse, Inc. (IXYS)

- Vitesco Technologies Group AG

- Vincotech GmbH

- CISSOID SA

- Hitachi Astemo, Ltd.

- Danfoss Silicon Power GmbH

- BYD Semiconductor Co., Ltd.

- Dynex Semiconductor Ltd.

- Shenzhen BASiC Semiconductor Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid EV and HEV production growth

- 4.2.2 Shift toward SiC and GaN wide-bandgap devices

- 4.2.3 Vehicle electrification demanding higher power-density modules

- 4.2.4 Stringent global emission regulations

- 4.2.5 OEM adoption of wire-bondless / top-side-cooling packages

- 4.2.6 Cell-to-pack architectures integrating power modules

- 4.3 Market Restraints

- 4.3.1 Lack of standardized qualification protocols

- 4.3.2 High cost and supply constraints of SiC / GaN substrates

- 4.3.3 Thermal-management limits in emerging 800 V platforms

- 4.3.4 Potential SiC supply-chain over-capacity

- 4.4 Impact of Macroeconomic Factors

- 4.5 Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Module Type

- 5.1.1 Intelligent Power Module (IPM)

- 5.1.2 SiC Power Module

- 5.1.3 GaN Power Module

- 5.1.4 IGBT Module

- 5.1.5 FET Module

- 5.2 By Power Rating

- 5.2.1 Up to 600 V

- 5.2.2 601 - 1200 V

- 5.2.3 Above 1200 V

- 5.3 By Packaging Technology

- 5.3.1 Wire-bond

- 5.3.2 Wire-bondless / Power Overlay

- 5.3.3 Press-fit / Direct Pressed-Die

- 5.3.4 PCB-embedded

- 5.4 By Propulsion Type

- 5.4.1 Battery-Electric Vehicle (BEV)

- 5.4.2 Hybrid Electric Vehicle (HEV)

- 5.4.3 Plug-in Hybrid (PHEV)

- 5.4.4 Fuel-Cell Electric Vehicle (FCEV)

- 5.5 By Vehicle Type

- 5.5.1 Passenger Cars

- 5.5.2 Light Commercial Vehicles

- 5.5.3 Heavy Commercial Vehicles and Buses

- 5.6 By Application

- 5.6.1 Traction Inverter

- 5.6.2 On-board Charger

- 5.6.3 DC-DC Converter

- 5.6.4 Auxiliary / Climate / EPS

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 Germany

- 5.7.3.2 France

- 5.7.3.3 United Kingdom

- 5.7.3.4 Rest of Europe

- 5.7.4 Asia-Pacific

- 5.7.4.1 China

- 5.7.4.2 Japan

- 5.7.4.3 India

- 5.7.4.4 South Korea

- 5.7.4.5 Rest of Asia-Pacific

- 5.7.5 Middle East and Africa

- 5.7.5.1 Middle East

- 5.7.5.1.1 Saudi Arabia

- 5.7.5.1.2 United Arab Emirates

- 5.7.5.1.3 Turkey

- 5.7.5.1.4 Rest of Middle East

- 5.7.5.2 Africa

- 5.7.5.2.1 South Africa

- 5.7.5.2.2 Rest of Africa

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Amkor Technology, Inc.

- 6.4.2 Kulicke & Soffa Industries, Inc.

- 6.4.3 Powertech Technology Inc. (PTI)

- 6.4.4 Infineon Technologies AG

- 6.4.5 STMicroelectronics N.V.

- 6.4.6 Fuji Electric Co., Ltd.

- 6.4.7 Toshiba Electronic Devices & Storage Corporation

- 6.4.8 SEMIKRON Danfoss GmbH & Co. KG

- 6.4.9 JCET Group Co., Ltd.

- 6.4.10 StarPower Semiconductor Ltd.

- 6.4.11 Mitsubishi Electric Corporation

- 6.4.12 ROHM Co., Ltd.

- 6.4.13 onsemi Corporation

- 6.4.14 Nexperia B.V.

- 6.4.15 Wolfspeed, Inc.

- 6.4.16 Microchip Technology Inc.

- 6.4.17 Littelfuse, Inc. (IXYS)

- 6.4.18 Vitesco Technologies Group AG

- 6.4.19 Vincotech GmbH

- 6.4.20 CISSOID SA

- 6.4.21 Hitachi Astemo, Ltd.

- 6.4.22 Danfoss Silicon Power GmbH

- 6.4.23 BYD Semiconductor Co., Ltd.

- 6.4.24 Dynex Semiconductor Ltd.

- 6.4.25 Shenzhen BASiC Semiconductor Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

功率模組封裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

功率模組封裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 功率模組封裝市場-2025-2030年預測

功率模組封裝市場-2025-2030年預測 功率模組封裝市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

功率模組封裝市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測