|

市場調查報告書

商品編碼

1846241

薄壁包裝:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)Thin Wall Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

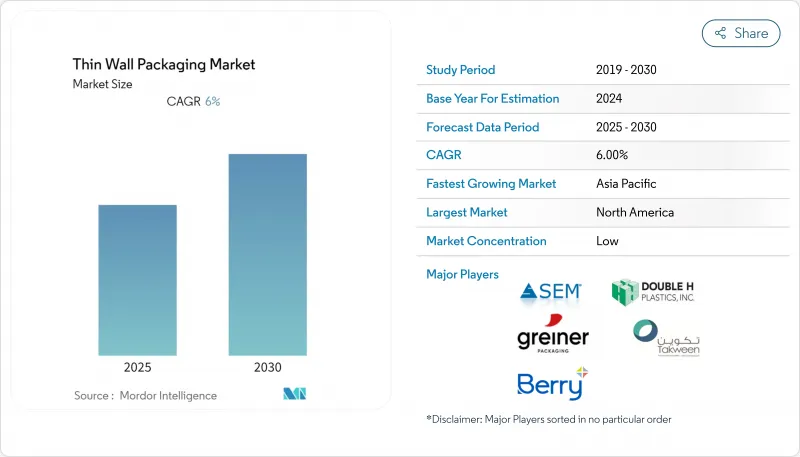

預計到 2025 年,薄壁包裝市場規模將達到 477.5 億美元,到 2030 年將達到 689.5 億美元。

這反映了 7.63% 的健康複合年成長率,凸顯了食品、食品飲料、化妝品和電子商務管道日益成長的需求。

推動薄壁包裝市場成長的因素包括:線上零售物流的蓬勃發展、降低運費的材料高效利用設計理念,以及對可回收包裝形式的立法支持力度不斷加大。儘管聚丙烯仍是市場主導樹脂,但隨著品牌商競相遵守生產者延伸責任法規,生物聚合物的應用正在加速。熱流道射出成型和在線擠出熱成型等製造技術的創新,在維持高產能的同時,還能將壁厚降低至1毫米以下。從區域來看,北美仍然是銷售領先者,但亞太地區由於都市化、外賣服務的興起以及可支配收入的成長,正以最快的速度擴張。這些因素共同作用,使得薄壁包裝市場在未來五年內成為品牌差異化、成本控制和減碳的關鍵平台。

全球薄壁包裝市場趨勢與洞察

電子商務物流的激增

線上零售的快速擴張正推動薄壁包裝市場朝著能夠承受自動化分類並最大限度降低體積重量費用的設計方向發展。像 Levain Bakery 這樣的品牌透過採用亞毫米級尺寸的包裝容器,將生產流程從八道工序簡化到四道工序,並將包裝效率提高了 50%。這些包裝容器隨後可在履約中心無縫流轉。 ReadyWise 透過按需使用合適尺寸的包裝,每週可交付 100 萬個包裝袋,同時降低運輸成本和儲存空間。易於自動化且空間最佳化的薄壁包裝容器,不再只是節約成本的措施,而是電子商務擴充性的關鍵基礎設施要素。

對便利已調理食品的需求

都市區消費者越來越傾向選擇可微波加熱、分量可控的餐食,這要求包裝能夠安全加熱而不破壞食材。 Curefit 目前每天出貨 35,000 份已調理食品,其包裝容器的設計旨在保持食物新鮮并快速加熱,這表明餐飲業的復甦正在推動對高阻隔性、薄壁包裝樹脂需求的成長。透明蓋可以促進衝動消費,而熱成型底座則利用精確的壁厚校準來節約樹脂並保持結構完整性。

塑膠稅和生產者責任延伸法

英國目前對再生材料含量低於30%的包裝課稅每噸200英鎊的稅,每年徵收7億英鎊,卻沒有為回收基礎建設提供資金。西班牙將於2023年開始對原生塑膠徵收每公斤課稅,而德國則將實施時間推遲到2025年,這讓投資預測蒙上了一層陰影。這些政策將推高合規成本,並加速向經認證的再生材料流和封閉式夥伴關係關係的轉變。

細分市場分析

受餐飲業重新開放和人們日益成長的便捷飲用習慣的推動,預計到2024年,杯子將佔據薄壁包裝市場36.3%的佔有率。此細分市場具有許多優勢,例如材料體積比低、相容自動填充系統以及便於品牌印刷的表面。隨著咖啡連鎖店和快餐店擴大試用能夠承受100°C填充溫度而不變形的永續杯子,這一成長勢頭將持續到2030年。

預計到2030年,碗和蓋品類將以7.9%的複合年成長率成長。業者優先選擇透明蓋,以保持產品新鮮度,並透過氣體沖洗延長保存期限。線上熱成型技術的進步使得碗的平均壁厚達到400微米,滿足了以往僅適用於較重競爭對手的跌落測試標準。托盤、軟管和罐子在乳製品、糖果甜點和個人護理等細分市場仍然十分重要,它們都透過形狀和阻隔性能的客製化來維持貨架差異化優勢。

聚丙烯憑藉其多功能的加工窗口、耐濕性和良好的性價比,將在2024年佔據薄壁包裝市場43.2%的佔有率。然而,隨著加工商努力滿足可堆肥性和再生材料含量的要求,薄壁包裝市場對PLA和PHA樹脂的採用率正在不斷提高,年複合成長率達到8.3%。

弗勞恩霍夫研究所推出了一種生物基含量高達80%的軟性PLA薄膜,可在傳統的LDPE生產線上生產。同時,PHA先驅Green Team檢驗了一種可在六個月內完全分解且不留微塑膠痕跡的家用可堆肥容器。 PET在對氧氣敏感的已調理沙拉中仍佔有一席之地,而聚苯乙烯和PVC在監管審查日益嚴格的背景下,市場佔有率持續下滑。

薄壁包裝市場依包裝類型(管狀、罐狀、盒狀及其他)、材料(聚丙烯、聚對苯二甲酸乙二醇酯、聚苯乙烯及其他)、製造程序(射出成型及其他)、終端用戶行業(食品飲料、化妝品及個人護理、藥品及營養補充劑、工業及家居用品)及地區進行細分。市場預測以美元計價。

區域分析

到2024年,北美將維持28.2%的薄壁包裝市場佔有率,這主要得益於其成熟的餐飲服務體系、完善的回收通路以及對輕量化套件包的早期應用。品牌擁有者為了獲得符合聯邦和州塑膠法規的合規包裝,繼續承擔高昂的樹脂價格。美國仍然是先進熱流道系統的創新中心,而加拿大則在引導公共部門採購政策,推動機構餐飲計畫中採用消費後回收樹脂(PCR)。

亞太地區預計到2030年將以9.5%的複合年成長率成長,這主要得益於快速的都市化、中階購買力的提升以及全管道食品雜貨消費模式的興起。中國在銷售方面領先,但印度和印尼的人均成長速度最快。印度食品安全標準局批准再生塑膠用於食品接觸領域,進一步降低了消費後再生塑膠(PCR)密集型薄壁塑膠設計的進入門檻。區域加工商正大力投資建造能夠同時加工聚丙烯和新興生物基樹脂的多層擠出和熱成型生產線,從而增強供應鏈的韌性。

由於歐洲較早推行永續性政策,並重視循環經濟,因此歐洲佔了相當大的市場。塑膠稅和生產者責任延伸制度雖然增加了成本壓力,但同時也獎勵了那些能夠在不犧牲密封完整性的前提下實現30%或更高回收率的企業。德國、法國和北歐國家一直是模內貼標(IML)技術的推廣中心,因為零售商正在推動使用單一材料包裝並搭配自有品牌產品。東歐國家受惠於低廉的勞動成本,正崛起為契約製造中心,在滿足西方需求的同時,也面臨同樣的監管門檻。

中東和非洲的叢集展現出早期但前景可觀的潛力,尤其是在冷凍乳製品出口和尋求耐高溫聚丙烯杯的區域性快餐連鎖店方面。南美洲的成長與農產品附加價值以及日益壯大的中階對便利消費品的需求密切相關。巴西本地樹脂生產具有成本優勢,但其不完善的回收基礎設施限制了循環材料的獲取,並減緩了富含消費後回收樹脂(PCR)的薄壁產品的普及。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 電子商務物流的激增

- 對方便的已調理食品的需求

- 減輕重量以降低成本和減少二氧化碳排放

- 套模貼標 (IML) 可提高可回收性

- 填充用的較薄包裝

- 低溫運輸食材自煮包熱潮

- 市場限制

- 塑膠稅和生產者責任延伸法

- 樹脂價格波動

- 轉向使用單一材料軟性薄膜

- 高空化模具資本投資

- 供應鏈分析

- 監管狀況

- 技術展望

- 五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

- 對宏觀經濟因素的市場評估

第5章 市場規模與成長預測

- 按包裝類型

- 管子

- 罐

- 鍋

- 杯子

- 托盤

- 碗和蓋子

- 按材質

- 聚丙烯(PP)

- 聚對苯二甲酸乙二醇酯(PET)

- 聚苯乙烯(PS)

- 聚乙烯(PE)

- 聚氯乙烯(PVC)

- 生物聚合物(PLA、PHA)

- 透過製造程序

- 射出成型

- 熱成型

- 擠壓成型等。

- 按最終用戶產業

- 飲食

- 乳製品

- 調理食品

- 水果和蔬菜

- 肉類、家禽和魚貝類

- 糖果甜點和零嘴零食

- 化妝品和個人護理

- 藥品和營養補充劑

- 工業/家用物品

- 飲食

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 其他亞太地區

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 埃及

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略舉措

- 市佔率分析

- 公司簡介

- Berry Global Group

- Greiner Packaging International

- Faerch Group

- Silgan Holdings Inc.

- Huhtamaki Oyj

- Novio Packaging BV

- Groupe Guillin SA

- Omniform SA

- Takween Advanced Industries

- Saudi Basic Industries Corporation(SABIC)

- Plastipak Holdings Inc.

- Sem Plastik Sanayi

- Dampack International

- Double H Plastics Inc.

- Greif Inc.

- Paccor Packaging

- Jabil Packaging Solutions

- IPL Plastics

- Visy Industries

- Supreme Industries

- Insta Polypack

第7章 市場機會與未來展望

The thin wall packaging market stands at USD 47.75 billion in 2025 and is forecast to reach USD 68.95 billion by 2030, reflecting a healthy 7.63% CAGR that underscores rising demand across food, beverage, cosmetics and e-commerce channels.

Upward momentum is fuelled by logistics growth tied to online retail, material-efficient design targets that cut freight charges, and tightening legislative support for recyclable formats. Polypropylene remains the workhorse resin, yet biopolymer penetration is accelerating as brand owners race to meet extended producer responsibility rules. Manufacturing innovation in hot-runner injection molding and inline extrusion-thermoforming keeps throughput high while driving wall thickness below 1 mm. Regionally, North America retains volume leadership, but Asia-Pacific is expanding fastest on the back of urbanization, meal-delivery adoption and rising disposable incomes. These converging factors combine to position the thin wall packaging market as a central platform for brand differentiation, cost containment and carbon reduction over the next five years.

Global Thin Wall Packaging Market Trends and Insights

Surge in E-commerce Logistics

Rapid online retail expansion pushes the thin wall packaging market toward designs that withstand automated sortation while minimizing dimensional weight fees. Brands such as Levain Bakery cut process steps from eight to four and achieved a 50% packaging-efficiency gain by adopting sub-millimeter containers that flow smoothly through fulfillment centers.ReadyWise uses on-demand right-sized packs to move 1 million pouches weekly, trimming freight costs and floor space simultaneously. Automation compatibility and space optimization make thin wall formats infrastructure-critical for e-commerce scalability rather than a simple cost lever.

Demand for Convenient Ready-to-Eat Meals

Urban consumers gravitate to microwave-ready, portion-controlled fare that requires packaging capable of safe heating without material distortion. Curefit now dispatches 35,000 ready meals daily in containers engineered for freshness retention and rapid reheat cycles, illustrating how food-service recovery steers incremental resin demand toward high-barrier thin wall designs. Transparent lids encourage impulse purchase while thermoformed bases exploit precise wall calibration to conserve resin and uphold structural integrity.

Plastic-tax and EPR Legislation

The United Kingdom now levies GBP 200 per tonne on packaging below 30% recycled content, extracting an anticipated GBP 700 million annually without earmarking funds for recycling infrastructure. Spain launched a per-kilogram tax on virgin plastic in 2023, while Germany's implementation delay until 2025 clouds investment forecasts. These policies inflate compliance costs and encourage accelerated transitions toward certified recyclate streams and closed-loop partnerships.

Other drivers and restraints analyzed in the detailed report include:

- Lightweighting for Cost-Down and CO2 Reduction

- In-mold Labelling (IML) Boosts Recyclability

- Resin Price Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cups generated a 36.3% share of the thin wall packaging market in 2024, underpinned by food-service reopenings and robust on-the-go beverage rituals. The segment benefits from low material-to-volume ratios, automated filling compatibility and brand-friendly print surfaces. Growth persists through 2030 as coffee chains and quick-service restaurants widen sustainable cup trials capable of withstanding 100 °C fill temperatures without deformation.

The bowls and lids category is projected to post a 7.9% CAGR to 2030, catalyzed by global meal-kit subscriptions and refrigerated fresh-cut produce. Operators prioritize transparent lids that showcase product freshness and support gas-flush shelf-life extensions. Advances in inline thermoforming enable bowls with 400-micron average wall sections that match drop-test standards formerly associated only with heavier rivals. Trays, tubs and jars remain vital for dairy, confectionery and personal-care niches, each leveraging geometry and barrier customization to maintain shelf differentiation.

Polypropylene captured 43.2% of thin wall packaging market share in 2024 due to its versatile processing window, moisture resistance and favorable price-performance ratio. Yet, the thin wall packaging market is witnessing brisk uptake of PLA and PHA resins, which are expanding at an 8.3% CAGR as converters scramble to meet compostability and recycled-content mandates.

The Fraunhofer Institute unveiled an 80% bio-based flexible PLA film that runs on conventional LDPE lines, signaling cost-effective integration potential for high-clarity applications. Meanwhile, PHA pioneer Green Team validated home-compostable pots that decompose within six months without microplastic traces. PET sustains niche relevance in oxygen-sensitive prepared salads, while polystyrene and PVC continue to lose share amid tightening regulatory scrutiny.

Thin Wall Packaging Marke is Segmented by Packaging Type (Tubs, Jars, Pots, and More), Material (Polypropylene, Polyethylene Terephthalate, Polystyrene, and More), Manufacturing Process (Injection Molding, and More), End-User Industry (Food and Beverage, Cosmetics and Personal Care, Pharmaceuticals and Nutraceuticals, Industrial and Household Goods), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 28.2% of the thin wall packaging market in 2024 on the back of entrenched meal-service businesses, sophisticated recycling channels and early adoption of light-weighting toolkits. Brand owners continue to absorb premium resin pricing in return for compliance-ready packs that navigate federal and state plastics legislation. The United States remains the innovation locus for advanced hot-runner systems, while Canada channels public-sector procurement policies toward PCR adoption in institutional food programmes.

Asia-Pacific is projected to achieve a 9.5% CAGR to 2030, underpinned by rapid urbanization, growing middle-class purchasing power and a sharp shift toward omni-channel grocery. China leads volume, but India and Indonesia post the fastest per-capita expansion. The Food Safety and Standards Authority of India's clearance for recycled plastic in food contact applications further lowers entry barriers for PCR-rich thin wall designs. Regional converters invest heavily in multilayer extrusion-thermoforming lines configurable for both polypropylene and emerging bio-resins, boosting supply resilience.

Europe commands significant share by virtue of early sustainability mandates and a continental focus on circularity. Plastic taxes and EPR regimes intensify cost pressures yet simultaneously reward companies capable of delivering 30% or greater recycled content without sacrificing seal integrity. Germany, France and the Nordics are hotbeds for IML adoption as retailers push mono-material packaging in private-label assortments. Eastern European nations, aided by lower labour costs, emerge as contract-manufacturing hubs that feed Western demand while navigating identical regulatory thresholds.

The Middle East and Africa cluster offers nascent but promising prospects, particularly in frozen-dairy exports and regional QSR chains that seek high-heat-resistant PP cups. South American growth is tethered to agricultural value-addition and an expanding middle class attracted to convenience formats. Local resin production in Brazil provides cost advantage; however, unreliable recycling infrastructure limits circular material sourcing, slowing penetration of PCR-rich thin wall offerings.

- Berry Global Group

- Greiner Packaging International

- Faerch Group

- Silgan Holdings Inc.

- Huhtamaki Oyj

- Novio Packaging B.V.

- Groupe Guillin SA

- Omniform SA

- Takween Advanced Industries

- Saudi Basic Industries Corporation (SABIC)

- Plastipak Holdings Inc.

- Sem Plastik Sanayi

- Dampack International

- Double H Plastics Inc.

- Greif Inc.

- Paccor Packaging

- Jabil Packaging Solutions

- IPL Plastics

- Visy Industries

- Supreme Industries

- Insta Polypack

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in e-commerce logistics

- 4.2.2 Demand for convenient ready-to-eat meals

- 4.2.3 Lightweighting for cost-down and CO2 reduction

- 4.2.4 In-mold labelling (IML) boosts recyclability

- 4.2.5 Refill-friendly thin-wall packs in cosmetics

- 4.2.6 Cold-chain meal-kit boom

- 4.3 Market Restraints

- 4.3.1 Plastic-tax and EPR legislation

- 4.3.2 Resin price volatility

- 4.3.3 Shift to mono-material flexible films

- 4.3.4 High-cavitation tooling cap-ex

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Assesment of macroeconomic Factors on the market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Packaging Type

- 5.1.1 Tubs

- 5.1.2 Jars

- 5.1.3 Pots

- 5.1.4 Cups

- 5.1.5 Trays

- 5.1.6 Bowls and Lids

- 5.2 By Material

- 5.2.1 Polypropylene (PP)

- 5.2.2 Polyethylene Terephthalate (PET)

- 5.2.3 Polystyrene (PS)

- 5.2.4 Polyethylene (PE)

- 5.2.5 Polyvinyl Chloride (PVC)

- 5.2.6 Biopolymers (PLA, PHA)

- 5.3 By Manufacturing Process

- 5.3.1 Injection Molding

- 5.3.2 Thermoforming

- 5.3.3 Extrusion and Others

- 5.4 By End-User Industry

- 5.4.1 Food and Beverage

- 5.4.1.1 Dairy Products

- 5.4.1.2 Ready Meals

- 5.4.1.3 Fruits and Vegetables

- 5.4.1.4 Meat, Poultry and Seafood

- 5.4.1.5 Confectionery and Snacks

- 5.4.2 Cosmetics and Personal Care

- 5.4.3 Pharmaceuticals and Nutraceuticals

- 5.4.4 Industrial and Household Goods

- 5.4.1 Food and Beverage

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Nigeria

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Berry Global Group

- 6.4.2 Greiner Packaging International

- 6.4.3 Faerch Group

- 6.4.4 Silgan Holdings Inc.

- 6.4.5 Huhtamaki Oyj

- 6.4.6 Novio Packaging B.V.

- 6.4.7 Groupe Guillin SA

- 6.4.8 Omniform SA

- 6.4.9 Takween Advanced Industries

- 6.4.10 Saudi Basic Industries Corporation (SABIC)

- 6.4.11 Plastipak Holdings Inc.

- 6.4.12 Sem Plastik Sanayi

- 6.4.13 Dampack International

- 6.4.14 Double H Plastics Inc.

- 6.4.15 Greif Inc.

- 6.4.16 Paccor Packaging

- 6.4.17 Jabil Packaging Solutions

- 6.4.18 IPL Plastics

- 6.4.19 Visy Industries

- 6.4.20 Supreme Industries

- 6.4.21 Insta Polypack

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

薄壁包裝市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測

薄壁包裝市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測 全球薄壁包裝市場成長、規模和趨勢分析(按產品類型、材料、製造流程和應用分類)-區域展望、競爭策略和細分市場預測(至2034年)薄壁包裝市場-2026年至2031年預測

全球薄壁包裝市場成長、規模和趨勢分析(按產品類型、材料、製造流程和應用分類)-區域展望、競爭策略和細分市場預測(至2034年)薄壁包裝市場-2026年至2031年預測 薄壁包裝市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

薄壁包裝市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測 薄壁包裝市場(按類型、材料、最終用戶行業、國家和地區)- 2024 年至 2032 年行業分析、市場規模、市場佔有率及預測

薄壁包裝市場(按類型、材料、最終用戶行業、國家和地區)- 2024 年至 2032 年行業分析、市場規模、市場佔有率及預測 全球薄壁包裝市場規模研究,依材料、產品類型、生產流程、應用和區域預測 2022-2032薄壁包裝市場報告:趨勢、預測和競爭分析(至 2031 年)

全球薄壁包裝市場規模研究,依材料、產品類型、生產流程、應用和區域預測 2022-2032薄壁包裝市場報告:趨勢、預測和競爭分析(至 2031 年)