|

市場調查報告書

商品編碼

1750298

薄壁包裝市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Thin Wall Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

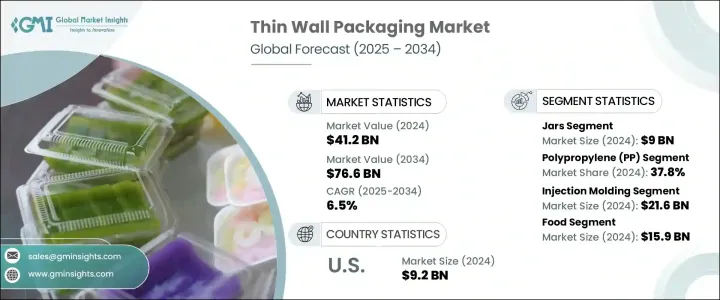

2024年,全球薄壁包裝市場規模達412億美元,預計到2034年將以6.5%的複合年成長率成長,達到766億美元,這主要得益於生活方式的轉變、對簡便食品的需求不斷成長以及餐飲服務管道的不斷拓展。隨著城市中心的擴張和消費者日常生活的日益繁忙,輕盈、耐用且經濟高效的包裝形式越來越受到青睞。薄壁包裝能夠縮短生產週期,減少材料使用,同時確保產品完整性。它還能透過適應當今快節奏零售和食品配送生態系統的形式,滿足現代供應鏈的需求。

隨著攜帶式、可微波加熱和可重複密封容器的需求不斷成長,薄壁包裝已成為城市食品消費中不可或缺的一部分。這些包裝迎合了消費者對便利餐點和速食零食的偏好,尤其是在人口密集地區。薄壁容器憑藉其優異的阻隔性和結構完整性,有助於延長保存期限,同時支持永續發展目標。如今,它們被廣泛用於包裝乳製品、冷凍食品和零食。消費者傾向於選擇這些包裝,因為它們實用,尤其是在包裝趨勢更傾向於極簡主義和環保意識的當下。罐裝包裝因其可重複使用的特性而廣受歡迎,適用於個人護理、家居用品和食品領域。它們密封性好,易於取用,同時保持新鮮。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 412億美元 |

| 預測值 | 766億美元 |

| 複合年成長率 | 6.5% |

2024年,罐裝包裝市場規模達90億美元,標誌著其在薄壁包裝領域佔據主導地位。這類容器結構輕巧、材料用量低且生產成本低廉,廣泛應用於食品、個人護理和家居用品等類別。罐裝包裝為各種應用提供了理想的包裝解決方案,為製造商和消費者提供了多功能性和實用性。罐裝包裝日益普及,不僅源自於其價格實惠,也源自於消費者對便利性、易用性和永續性的偏好。罐裝包裝可重複使用且易於儲存,尤其適合需要重複取用或控制份量的產品。

2024年,聚丙烯 (PP) 市場佔有 37.8% 的佔有率。這種聚合物兼具強度高、重量輕和價格實惠等特點,使其成為薄壁包裝的理想選擇,尤其是在快速循環注塑成型中。其防潮性和化學穩定性使其成為食品級應用的首選。增強型 PP 配方可在不影響耐用性的情況下實現更薄的壁厚,使企業能夠在滿足監管壓力的同時減少碳足跡。

2024年,美國薄壁包裝市場規模達92億美元。預製食品和零食消費的增加,刺激了對輕量化、保護性包裝解決方案的需求。此外,電子商務和送貨上門服務的興起,也推動了包裝創新,這些創新優先考慮材料節約和環保合規性。消費者意識的增強以及政府主導的永續發展措施進一步加速了這一趨勢。

全球薄壁包裝產業的領先公司包括 ILIP Srl、Paccor GmbH、Amcor plc、Greiner Packaging International GmbH 和 Berry Global Inc.。全球薄壁包裝市場的主要參與者正在大力投資永續創新、策略併購和區域擴張,以提升市場佔有率。各公司正專注於輕量化設計技術,並採用生物基聚丙烯等可回收材料,以符合綠色包裝法規。一些公司已與食品和飲料品牌合作,提供客製化解決方案,以提升貨架吸引力並延長保鮮期。擴大北美和亞太等高成長地區的產能是當務之急,同時採用先進的注塑機來提高速度和效率。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 川普政府關稅

- 對貿易的影響

- 貿易量中斷

- 報復措施

- 對產業的影響

- 供應方影響(原料)

- 主要材料價格波動

- 供應鏈重組

- 生產成本影響

- 需求面影響(售價)

- 價格傳導至終端市場

- 市佔率動態

- 消費者反應模式

- 供應方影響(原料)

- 受影響的主要公司

- 策略產業反應

- 供應鏈重組

- 定價和產品策略

- 政策參與

- 展望與未來考慮

- 對貿易的影響

- 供應商格局

- 利潤率分析

- 重要新聞和舉措

- 監管格局

- 衝擊力

- 成長動力

- 簡便食品和即食食品需求激增

- 永續性和輕量化措施的成長

- 食品配送和 QSR 通路的興起

- 新興經濟體的快速都市化

- 射出成型和模內貼標 (IML) 技術不斷進步

- 產業陷阱與挑戰

- 對塑膠使用的嚴格環境法規

- 易腐貨物的阻隔性能有限

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第5章:市場估計與預測:依產品類型,2021-2034

- 主要趨勢

- 杯子

- 浴缸

- 托盤

- 罐子

- 蓋子

- 其他容器

第6章:市場估計與預測:依材料類型,2021-2034 年

- 主要趨勢

- 聚丙烯(PP)

- 聚乙烯(PE)

- 高密度聚乙烯(HDPE)

- 低密度聚乙烯(LDPE)

- 聚苯乙烯(PS)

- 聚對苯二甲酸乙二醇酯(PET)

- 聚氯乙烯(PVC)

- 其他

第7章:市場估計與預測:按生產流程,2021-2034 年

- 主要趨勢

- 熱成型

- 射出成型

- 其他

第 8 章:市場估計與預測:按應用,2021 年至 2034 年

- 主要趨勢

- 食物

- 乳製品

- 即食食品

- 烘焙和糖果

- 肉類、家禽和海鮮

- 飲料

- 個人護理和化妝品

- 家居用品

- 電氣和電子產品

- 藥品和營養保健品

- 工業的

第9章:市場估計與預測:按地區,2021-2034

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- MEA

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- ALPLA Group

- Akshar Plastic

- Amcor Plc

- Berry Global Inc.

- Borouge

- Chemco Plast

- Cosmo Films

- Double H Plastics

- EVCO Plastics

- Greiner Packaging International GmbH

- ILIP Srl

- IPL Plastics Inc.

- Mold-Masters

- Paccor

- Prabhoti Plastic Industries

- SABIC

- SP International Industries Pvt. Ltd.

The Global Thin Wall Packaging Market was valued at USD 41.2 billion in 2024 and is estimated to grow at a CAGR of 6.5% to reach USD 76.6 billion by 2034, driven by shifting lifestyle patterns, increasing demand for convenience food options, and expanding foodservice channels. As urban centers grow and consumer routines become more hectic, the appeal of lightweight, durable, and cost-efficient packaging formats has intensified. Thin-wall packaging enables quicker production turnaround and reduced material use while delivering product integrity. It also supports modern supply chain needs with formats that fit today's fast-paced retail and food delivery ecosystems.

With rising demand for portable, microwaveable, and resealable containers, thin wall formats have become indispensable across urban food consumption. These packages align with consumers' preference for on-the-go meals and instant snacks, especially in high-density regions. Thanks to their barrier properties and structural integrity, thin wall containers help extend shelf life while supporting sustainability goals. They're now widely chosen for packaging dairy, frozen entrees, and snack foods. Consumers gravitate toward these options for practicality, especially as packaging trends lean more toward minimalism and eco-consciousness. Jars are popular for their reusable nature and suitability across personal care, household goods, and food applications. They offer an effective seal that maintains freshness while being easy to handle.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $41.2 Billion |

| Forecast Value | $76.6 Billion |

| CAGR | 6.5% |

The jars segment generated USD 9 billion in 2024, marking its dominance within the thin wall packaging landscape. These containers are extensively used across food, personal care, and household product categories due to their lightweight structure, reduced material usage, and cost-effective production. Jars offer an ideal packaging solution for a wide range of applications, providing both manufacturers and consumers with versatility and functionality. Their growing popularity stems not only from their affordability but also from consumer-driven preferences for convenience, ease of use, and sustainability. Reusability and easy storage make jars a preferred option, especially for products that require repeated access or portion control.

The polypropylene (PP) segment held a 37.8% share in 2024. This polymer's blend of strength, light weight, and affordability makes it ideal for thin wall packaging, especially in fast-cycle injection molding. Its moisture resistance and chemical stability make it a preferred choice for food-grade applications. Enhanced PP formulations allow thinner walls without compromising durability, enabling companies to reduce carbon footprints while meeting regulatory pressures.

United States Thin Wall Packaging Market generated USD 9.2 billion in 2024. Increased consumption of prepared meals and snacks has fueled demand for lightweight, protective packaging solutions. Additionally, the rise of e-commerce and home delivery services has prompted packaging innovations that prioritize material reduction and environmental compliance. This trend is further accelerated by growing consumer awareness and government-led sustainability initiatives.

Leading companies in the Global Thin Wall Packaging Industry comprise ILIP S.r.l., Paccor GmbH, Amcor plc, Greiner Packaging International GmbH, and Berry Global Inc. Key players in the Global Thin Wall Packaging Market are investing heavily in sustainable innovation, strategic mergers, and regional expansion to enhance market presence. Companies are focusing on lightweight design technologies and adopting recyclable materials like bio-based polypropylene to align with green packaging mandates. Several have partnered with food and beverage brands to offer customized solutions that improve shelf appeal and extend freshness. Expanding production capacity in high-growth regions such as North America and Asia Pacific is a top priority, alongside adopting advanced injection molding machinery to improve speed and efficiency.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Supplier landscape

- 3.4 Profit margin analysis

- 3.5 Key news & initiatives

- 3.6 Regulatory landscape

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Surge in demand for convenience and ready-to-eat foods

- 3.7.1.2 Growth in sustainability and lightweighting initiatives

- 3.7.1.3 Rise of food delivery and QSR channels

- 3.7.1.4 Rapid urbanization in emerging economies

- 3.7.1.5 Increasing advancements in injection molding and in-mold labeling (IML)

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 Stringent environmental regulations on plastic use

- 3.7.2.2 Limited barrier properties for perishable goods

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product Type, 2021-2034 (USD Million & Units)

- 5.1 Key trends

- 5.2 Cups

- 5.3 Tubs

- 5.4 Trays

- 5.5 Jars

- 5.6 Lids

- 5.7 Other containers

Chapter 6 Market Estimates & Forecast, By Material Type, 2021-2034 (USD Million & Units)

- 6.1 Key trends

- 6.2 Polypropylene (PP)

- 6.3 Polyethylene (PE)

- 6.3.1 High-density polyethylene (HDPE)

- 6.3.2 Low-density polyethylene (LDPE)

- 6.4 Polystyrene (PS)

- 6.5 Polyethylene terephthalate (PET)

- 6.6 Polyvinyl chloride (PVC)

- 6.7 Others

Chapter 7 Market Estimates & Forecast, By Production Process, 2021-2034 (USD Million & Units)

- 7.1 Key trends

- 7.2 Thermoforming

- 7.3 Injection molding

- 7.4 Others

Chapter 8 Market Estimates & Forecast, By Application, 2021-2034 (USD Million & Units)

- 8.1 Key trends

- 8.2 Food

- 8.2.1 Dairy products

- 8.2.2 Ready-to-eat meals

- 8.2.3 Bakery & confectionery

- 8.2.4 Meat, poultry & seafood

- 8.3 Beverages

- 8.4 Personal care & cosmetics

- 8.5 Household products

- 8.6 Electrical & electronics

- 8.7 Pharmaceuticals & nutraceuticals

- 8.8 Industrial

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Million & Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 ALPLA Group

- 10.2 Akshar Plastic

- 10.3 Amcor Plc

- 10.4 Berry Global Inc.

- 10.5 Borouge

- 10.6 Chemco Plast

- 10.7 Cosmo Films

- 10.8 Double H Plastics

- 10.9 EVCO Plastics

- 10.10 Greiner Packaging International GmbH

- 10.11 ILIP S.r.l.

- 10.12 IPL Plastics Inc.

- 10.13 Mold-Masters

- 10.14 Paccor

- 10.15 Prabhoti Plastic Industries

- 10.16 SABIC

- 10.17 SP International Industries Pvt. Ltd.

薄壁包裝市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測

薄壁包裝市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測 全球薄壁包裝市場成長、規模和趨勢分析(按產品類型、材料、製造流程和應用分類)-區域展望、競爭策略和細分市場預測(至2034年)薄壁包裝市場-2026年至2031年預測

全球薄壁包裝市場成長、規模和趨勢分析(按產品類型、材料、製造流程和應用分類)-區域展望、競爭策略和細分市場預測(至2034年)薄壁包裝市場-2026年至2031年預測 薄壁包裝:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)

薄壁包裝:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年) 薄壁包裝市場(按類型、材料、最終用戶行業、國家和地區)- 2024 年至 2032 年行業分析、市場規模、市場佔有率及預測

薄壁包裝市場(按類型、材料、最終用戶行業、國家和地區)- 2024 年至 2032 年行業分析、市場規模、市場佔有率及預測 全球薄壁包裝市場規模研究,依材料、產品類型、生產流程、應用和區域預測 2022-2032薄壁包裝市場報告:趨勢、預測和競爭分析(至 2031 年)

全球薄壁包裝市場規模研究,依材料、產品類型、生產流程、應用和區域預測 2022-2032薄壁包裝市場報告:趨勢、預測和競爭分析(至 2031 年)