|

市場調查報告書

商品編碼

1931743

工業幫浦:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Industrial Pump - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

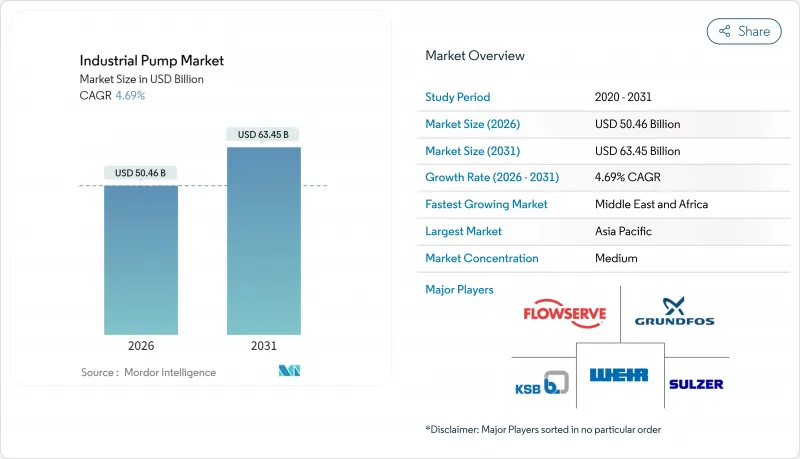

預計到 2025 年,工業幫浦市場價值將達到 482 億美元,從 2026 年的 504.6 億美元成長到 2031 年的 634.5 億美元。

預計在預測期(2026-2031 年)內,複合年成長率將達到 4.69%。

在供應鏈長期波動的情況下,老舊城市管網的持續更新、石化工廠的擴張以及日益嚴格的能源效率法規支撐了市場的韌性。水處理產業的資本支出仍是最大的需求推動要素,光是美國在2022年至2026年間累計超過500億美元用於水基礎設施升級。卡達和沙烏地阿拉伯的大型企劃持續推動了能夠處理乙烯裂解裝置和天然氣處理廠中腐蝕性和高溫介質的高規格泵浦的訂單。亞太地區憑藉中國、印度和東南亞的大規模工業化,繼續保持主導地位,而中東和非洲地區則由於其石化行業的加速多元化而實現了最快的成長。

全球工業幫浦市場趨勢及展望

全球對用水和污水處理的投資不斷增加

2024 年和 2025 年初創紀錄的市政預算導致大容量離心式幫浦和潛水式污水泵的競標量激增。美國環保署 (EPA) 估計,長期維修需求超過 7,440 億美元,推動了多階段升級項目,例如耗資 4.65 億美元的蘇城區域設施和耗資 2.39 億美元的卡羅來納州費爾角南區污水處理廠。先進的污水處理要求推動了對高壓逆滲透設備的需求,蘇爾壽的垂直多級系統被選中用於埃及的馬赫薩馬污水回收計劃。供水事業擴大採用無線感測器,將振動和溫度數據傳輸到雲端控制面板,以縮短關鍵資產的平均維修時間。採購框架強調總擁有成本 (TCO) 計算,並鼓勵採用節能設計,促使採購者選擇能夠輕鬆滿足歐盟 MEI 標準的高效率馬達。加強監控要求也擴大了售後市場的收入來源,並為原始設備製造商 (OEM) 的持續服務合約提供了基礎。

中東和非洲的石化工廠擴建

海灣產油國正在實現下游業務多元化,透過授予EPC合約的方式建造裂解裝置、聚合物裝置和天然氣處理廠,這些項目都需要總合台耐腐蝕泵。卡達耗資60億美元的拉斯拉凡聚合物綜合體計畫包括一套日產208萬噸乙烷的裂解裝置,計畫於2027年運作。沙烏地阿拉伯耗資110億美元的阿米拉爾計劃將新增165萬噸/日的乙烯產能,並與SATORP煉油廠整合,這顯著增加了對符合API 610標準、能夠承受400°F(約204°C)排放溫度的泵浦的需求。採購競標中的在地採購條款增強了國際原始設備製造商(OEM)本地化泵殼加工和最終組裝的獎勵。終端用戶優先考慮使用變頻驅動裝置以降電力消耗,這推動了智慧馬達控制技術的應用,符合區域節能目標。

鋼鐵和銅價波動會推高總擁有成本。

2024年,由於對供不應求,銅價飆升至每噸1萬美元以上,逼近1.1萬美元,導致銅密集型定子和繞組部件的生產成本上漲3.5%至4.2%。碳中和鋼鐵舉措進一步加劇了不確定性,因為鋼廠將與氫基生產相關的綠色溢價轉嫁給了消費者。製造商採取的應對措施包括加強避險計畫、重新設計泵殼以節省材料,以及在供應合約中引入浮動價格條款。同時,終端用戶推遲了自願更換計劃,延長了設備的使用壽命,並抑制了工業泵市場的短期出貨量。

細分市場分析

2025年,離心式幫浦浦機組佔總收入的61.85%,憑藉其在供水、化學品輸送和空調迴路中久經考驗的成本績效,為工業泵浦市場提供了有力支撐。市政系統平均三年一次的大修週期,為細分市場帶來了穩定的售後需求。然而,由於高黏度漿料處理的特殊需求,漸進式溶洞幫浦的市佔率有所成長,預計到2031年,其複合年成長率將達到7.45%。隨著石化和礦業客戶優先考慮低剪切輸送,漸進式溶洞泵在工業泵市場的佔有率正在擴大。同時,往復泵和隔膜泵分別在高壓注入和衛生生產領域繼續發揮重要作用,但其應用領域較為細分。物聯網改造在傳統離心式幫浦機組中也得到了廣泛應用,能夠進行振動分析以實現預測性維護,並將計劃外停機時間減少高達30%。

一家單軸偏心螺桿幫浦製造商大力投資耐磨轉子塗層,將磨損負荷下的維護週期延長至8000小時以上。旋轉齒輪幫浦和蠕動幫浦滿足了電池材料生產線中新興的微量計量需求,展現了終端應用領域的廣泛創新。基於感測器遙測技術建構的數位雙胞胎使操作人員能夠模擬整個液壓範圍內的空化風險,從而改善製程控制以保護葉輪。供應商繼續強調模組化盒式密封的重要性,這種密封件簡化了維護並減少了備件庫存。隨著監管機構日益關注能源強度,提高泵殼蝸殼和擴散葉片的效率已成為整個工業泵市場所有類型泵的競爭要務。

預計到2025年,電動驅動裝置將佔77.95%的市場佔有率,這得益於已開發國家近乎普及的電網接入以及變頻驅動裝置帶來的效率提升。格雷科QUANTM平台記錄的現場數據顯示,採用橫向磁通拓樸結構的馬達效率最高可達85%,進一步印證了電動驅動的全生命週期成本優勢。然而,太陽能驅動解決方案已成為工業泵浦產業成長最快的細分市場,年複合成長率高達11.1%,這主要得益於非洲和南亞農村灌溉計劃的推動。太陽能驅動解決方案的安裝成本從76.23歐元(89.13美元)到1219.59歐元(1425.95美元)不等,具有強大的平準化成本競爭力,尤其是在考慮到柴油發電機的燃料物流成本之後。

在電力系統可靠性仍存疑的油田壓裂和緊急雨水排放領域,柴油引擎組仍具有重要的戰略意義。液壓和氣動驅動裝置繼續應用於危險區域設施和移動設備,因為這些場所對功率密度和防火安全要求較高。結合太陽能光電陣列和鋰離子儲能的混合微電網解決方案已在印尼多家礦場進入試點階段,實現了無需柴油輔助的24小時運作。在連續運轉的海水淡化廠中,對現有電氣設備進行變頻驅動裝置(VFD)改造,已實現了高達20%的能源成本節約。總體而言,這種電力供應組合對終端用戶來說是一個切實可行的選擇,但預計在預測期內,電力驅動裝置在工業泵市場的主導地位仍將持續。

工業泵市場按泵類型(離心泵、往復泵、旋轉泵等)、動力來源(電力、柴油、太陽能等)、終端用戶行業(石油和天然氣、水和用水和污水、化工和石化、發電、採礦、食品和飲料等)、泵安裝類型(潛水式、地面安裝式)和地區(北美、南美、歐洲、亞太、中東和非洲)進行細分。

區域分析

亞太地區受益於數十年的工業基礎設施建設、大規模的城市基礎設施改造以及政策主導的製造地本地化,預計到2025年將以44.85%的市場佔有率引領市場。福建省新建的乙烯裂解裝置和澳洲的大型海水淡化專案推動了高效多級泵浦的採購。中國推廣污水回用以及印度針對化學工業的生產關聯激勵計畫(PLI)持續推動國內外泵製造商的訂單成長。日益嚴格的電力消耗強度和碳足跡監管促使營運商採用變頻驅動裝置(VFD)進行維修,從而擴大了工業泵浦市場中高效產品線的市場佔有率。

中東和非洲地區複合年成長率最高,達6.05%,主要得益於沙烏地阿拉伯、卡達和阿拉伯聯合大公國總合170億美元的石化投資。海水淡化項目,例如NEOM公司日處理量達100萬立方公尺的海水處理計劃,需要耐氯化物應力腐蝕的高壓雙相不鏽鋼幫浦。贊比亞和剛果民主共和國的非洲採礦業擴張,帶動了耐磨漿料泵訂單的成長。在地採購框架使得原始設備製造商(OEM)得以在阿曼和南非建立服務基地,從而縮短了檢修週期,並增強了品牌忠誠度。受《水利基礎設施法案》的推動,北美地區持續保持穩定的更新換代,加州、德克薩斯州和佛羅裡達州收到了大量離心式幫浦和立式渦輪泵的更換競標。能源政策激勵措施促進了氫電解的早期應用,從而帶來了耐腐蝕循環泵的利基訂單。歐洲嚴格的MEI法規刺激了對超高效設計的需求,並促使工廠業主重新評估整體擁有成本指標。儘管拉丁美洲面積較小,但智利和秘魯的農業灌溉幫浦需求以及採礦相關需求均穩定成長。在所有地區,包含預測性維護的數位化服務提案都是競標評估中的決定性因素,進一步塑造了工業泵浦市場的競爭格局。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 全球水和污水處理支出不斷成長

- 擴大中東和非洲的石化產品產能

- 亞太地區工業基礎建設的快速發展

- 綠色氫電解對耐腐蝕泵浦的需求

- 預測性維護物聯網服務模式創造售後市場收入

- 市場限制

- 鋼鐵和銅價波動推高了總擁有成本(TCO)。

- 由於泵浦效率法規更加嚴格,資本投資週期放緩。

- 在乾旱經濟中向無動力重力式微灌系統過渡

- 價值鏈分析

- 技術展望

- 監管環境

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 宏觀經濟因素的影響

第5章 市場規模與成長預測

- 按泵類型

- 離心式

- 往復式

- 旋轉

- 隔膜

- 單軸偏心螺絲

- 其他

- 透過電源

- 電

- 柴油引擎

- 太陽能發電

- 油壓

- 氣動

- 按最終用戶行業分類

- 石油和天然氣

- 水和污水

- 化學品和石油化工

- 發電

- 礦業

- 食品/飲料

- 製藥

- 紙漿和造紙

- 其他

- 按泵浦位置

- 水下

- 在水上

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 台灣

- 亞太其他地區

- 中東和非洲

- 中東

- 土耳其

- 以色列

- 海灣合作理事會國家

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 其他非洲地區

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Flowserve Corporation

- Grundfos Holding A/S

- Xylem Inc.

- Sulzer Ltd.

- KSB SE & Co. KGaA

- ITT Inc.

- Ebara Corporation

- The Weir Group PLC

- Schlumberger NV(REDA Pump)

- Baker Hughes Company

- SPX FLOW Inc.

- Wilo SE

- Dover Corporation

- Pentair plc

- Franklin Electric Co. Inc.

- Tsurumi Manufacturing Co. Ltd.

- Kirloskar Brothers Ltd.

- Atlas Copco AB

- Ruhrpumpen Group

- Zoeller Company

- Roto Pumps Ltd.

- Gardner Denver LLC(Ingersoll Rand)

- ClydeUnion Pumps(Celeros Flow Tech)

- LEWA GmbH

- Graco Inc.

第7章 市場機會與未來展望

The industrial pump market was valued at USD 48.2 billion in 2025 and estimated to grow from USD 50.46 billion in 2026 to reach USD 63.45 billion by 2031, at a CAGR of 4.69% during the forecast period (2026-2031).

Sustained replacement of aging municipal networks, petrochemical capacity additions, and tighter efficiency rules underpinned the market's resilience through prolonged supply-chain volatility. Capital spending on water treatment remained the single largest pull-forward of demand, with the United States alone earmarking more than USD 50 billion for water infrastructure upgrades between 2022 and 2026. Mega-projects in Qatar and Saudi Arabia continued to lift orders for high-specification pumps capable of handling corrosive, high-temperature media in ethylene crackers and gas-processing trains. Asia-Pacific retained volumetric leadership on the back of large-scale industrialization across China, India, and Southeast Asia, while the Middle East and Africa posted the fastest growth trajectory as petrochemical diversification accelerated.

Global Industrial Pump Market Trends and Insights

Rising Water and Wastewater Treatment Spending Globally

Record municipal budgets released in 2024 and early 2025 translated into larger tender volumes for high-capacity centrifugal and submersible sewage pumps. The US Environmental Protection Agency estimated long-term rehabilitation needs above USD 744 billion, prompting multi-phase upgrades such as Sioux City's USD 465 million regional facility and Cape Fear's USD 239 million Southside plant. Advanced treatment mandates drove interest in high-pressure reverse-osmosis trains, with Sulzer's vertical multistage systems underpinning Egypt's Al Mahsama drainage reclamation project. Utilities are increasingly embedding wireless sensors that stream vibration and temperature data into cloud dashboards, shortening mean-time-to-repair on critical units. Procurement frameworks began weighting total-cost-of-ownership calculations that favor energy-efficient designs, nudging buyers toward premium efficiency motors that comfortably clear EU MEI thresholds. Heightened monitoring obligations also expanded aftermarket revenue pools, anchoring recurring service contracts for OEMs.

Expansion of Petrochemical Capacity in MEA

Gulf producers pushed downstream diversification agendas, awarding EPC contracts for crackers, polymer units, and gas-processing trains that collectively require thousands of corrosion-resistant pumps. Qatar's Ras Laffan polymers complex, budgeted at USD 6 billion, incorporated a 2,080 KTA ethane cracker slated for 2027 on-stream dates. Saudi Arabia's USD 11 billion Amiral project added 1.65 million tons of ethylene nameplate capacity integrated with SATORP's refinery, multiplying demand for API 610 compliant pumps that withstand 400°F discharge temperatures. Local-content clauses inside procurement tenders intensified incentives for international OEMs to localize casing machining and final assembly. End-users prioritized variable-frequency drives to curb power draw, reinforcing adoption of smart motor controls that align with regional energy-efficiency ambitions.

Volatility in Steel and Copper Prices Inflating TCO

Copper cleared USD 10,000 per metric ton in 2024 and flirted with USD 11,000 amid looming supply deficits, hiking producer input costs by 3.5%-4.2% on copper-intensive stators and windings. Carbon-neutral steel initiatives added further unpredictability as mills passed on green-premium surcharges linked to hydrogen-based production. Manufacturers responded by tightening hedging programs, redesigning casings for material thrift, and introducing dynamic price clauses into supply contracts. End-users, meanwhile, deferred discretionary replacements, stretching the mean equipment life and tempering near-term shipment volumes in the industrial pump market.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Industrial Infrastructure Build-out Across Asia-Pacific

- Demand for Corrosion-Resistant Pumps in Green-Hydrogen Electrolyzers

- Stricter Pump-Efficiency Directives Delaying Cap-ex Cycles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Centrifugal units retained 61.85% of 2025 revenue, anchoring the industrial pump market through their proven cost-performance balance in water supply, chemical transfer, and HVAC loops. The segment generated steady aftermarket volumes, given typical mean-time-between-overhauls of three years in municipal duty cycles. However, specialty demands in viscous slurry handling shifted incremental share toward progressing cavity designs, which are projected to clock 7.45% CAGR through 2031. The progressing cavity cohort captured a rising slice of the industrial pump market size for petrochemical and mining customers that prize low-shear conveyance. Meanwhile, reciprocating and diaphragm pumps preserved critical roles in high-pressure injection and sanitary production, respectively, albeit with niche footprints. IoT retrofits became common even on legacy centrifugal sets, enabling predictive vibration analytics that cut unscheduled downtime by up to 30%.

Progressing cavity manufacturers invested heavily in wear-resistant rotor coatings to extend service intervals beyond 8,000 hours under abrasive duty. Rotary gear and peristaltic pumps addressed emerging micro-dosing tasks within battery-materials manufacturing lines, underscoring the breadth of end-use innovation. Digital twins built from sensor telemetry allowed operators to simulate cavitation risk across the hydraulic envelope, driving process-control refinements that protect impellers. Suppliers continued to emphasize modular cartridge seals that simplify maintenance and shrink spare inventory. With regulatory spotlight fixed on energy intensity, efficiency upgrades in casing volutes and diffuser vanes became a competitive must-have across all pump types in the broader industrial pump market.

Electric-driven assemblies held a commanding 77.95% share in 2025, benefitting from near-universal grid access in industrialized economies and the incremental efficiency yields of variable-frequency drives. Field data logged by Graco's QUANTM platform demonstrated up to 85% motor efficiency thanks to transverse-flux topology, reinforcing the narrative of electricity-based lifecycle cost advantage. Solar-powered solutions, however, emerged as the fastest expanding slice of the industrial pump industry, advancing at an 11.1% CAGR on the back of rural irrigation projects in Africa and South Asia. Installation costs ranging from EUR 76.23 (USD 89.13) to EUR 1,219.59 (USD 1,425.95) translated to competitive levelized costs, particularly once fuel-logistics premiums on diesel sets were factored in.

Diesel-engine packages retained strategic relevance for oilfield fracturing and emergency stormwater evacuation, where grid resilience remained questionable. Hydraulic and pneumatic drives continued to serve hazardous-area placements and mobile plant equipment that prized power density and ignition safety. Hybrid microgrid solutions that pair PV arrays with lithium-ion storage entered the pilot stage at several Indonesian mines, offering 24/7 uptime without diesel supplementation. VFD retrofits on existing electric fleets shaved energy bills by up to 20% in continuous-duty desalination applications. Altogether, the power-source mix illustrated end-user pragmatism, but electric leadership in the industrial pump market is expected to persist through the forecast horizon.

Industrial Pump Market is Segmented by Pump Type (Centrifugal, Reciprocating, Rotary, and More), Power Source (Electric, Diesel, Solar, and More), End-User Industry (Oil and Gas, Water and Waste-Water, Chemicals and Petrochemicals, Power Generation, Mining, Food and Beverage, and More), Pump Orientation (Submersible, and Surface), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa).

Geography Analysis

Asia-Pacific dominated with 44.85% revenue in 2025 after decades of industrial build-out, extensive municipal upgrades, and policy-driven manufacturing localization. New ethylene cracker complexes in Fujian and large-scale desalination schemes in Australia magnified the procurement of high-efficiency multistage pumps. China's stimulus for wastewater reuse and India's Production Linked Incentive program for chemicals continued to channel orders toward both global and domestic pump manufacturers. Regulatory pushes around electricity intensity and carbon footprints incentivized operators to retrofit VFDs, nudging market volume toward premium-efficiency product lines within the industrial pump market.

The Middle East and Africa posted the fastest 6.05% CAGR, propelled by USD 17 billion in combined petrochemical investments across Saudi Arabia, Qatar, and the United Arab Emirates. Desalination, such as NEOM's 1 million m3/day seawater project, demanded high-pressure duplex-steel pumps tolerant to chloride stress-corrosion. African mining expansions in Zambia and the Democratic Republic of Congo increased orders for abrasion-resistant slurry units. Local content frameworks pushed OEMs to open service hubs in Oman and South Africa, shortening turnaround times on overhauls and reinforcing brand loyalty. North America experienced a steady replacement cycle driven by water infrastructure bills, with California, Texas, and Florida aggregating the bulk of tenders for replacement centrifugal and vertical turbine pumps. Energy policy incentives supported early adoption of hydrogen electrolysis, sparking niche orders for corrosion-resistant circulation pumps. Europe's stringent MEI regulations stimulated demand for ultra-high-efficiency designs and encouraged plant owners to reassess total-cost-of-ownership metrics. Latin America, though smaller, witnessed steady uptake in agricultural irrigation pumps and mining-related demand in Chile and Peru. Across all regions, digital service propositions featuring predictive maintenance became a decisive factor in bid evaluations, further shaping competitive standings in the industrial pump market.

- Flowserve Corporation

- Grundfos Holding A/S

- Xylem Inc.

- Sulzer Ltd.

- KSB SE & Co. KGaA

- ITT Inc.

- Ebara Corporation

- The Weir Group PLC

- Schlumberger NV (REDA Pump)

- Baker Hughes Company

- SPX FLOW Inc.

- Wilo SE

- Dover Corporation

- Pentair plc

- Franklin Electric Co. Inc.

- Tsurumi Manufacturing Co. Ltd.

- Kirloskar Brothers Ltd.

- Atlas Copco AB

- Ruhrpumpen Group

- Zoeller Company

- Roto Pumps Ltd.

- Gardner Denver LLC (Ingersoll Rand)

- ClydeUnion Pumps (Celeros Flow Tech)

- LEWA GmbH

- Graco Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising water and waste-water treatment spending globally

- 4.2.2 Expansion of petrochemical capacity in MEA

- 4.2.3 Rapid industrial infrastructure build-out across Asia-Pacific

- 4.2.4 Demand for corrosion-resistant pumps in green-hydrogen electrolyzers

- 4.2.5 Predictive-maintenance IoT service models unlocking aftermarket revenue

- 4.3 Market Restraints

- 4.3.1 Volatility in steel and copper prices inflating TCO

- 4.3.2 Stricter pump-efficiency directives delaying cap-ex cycles

- 4.3.3 Shift to motor-less gravity micro-irrigation systems in arid economies

- 4.4 Value Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Landscape

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Pump Type

- 5.1.1 Centrifugal

- 5.1.2 Reciprocating

- 5.1.3 Rotary

- 5.1.4 Diaphragm

- 5.1.5 Progressing Cavity

- 5.1.6 Others

- 5.2 By Power Source

- 5.2.1 Electric

- 5.2.2 Diesel

- 5.2.3 Solar

- 5.2.4 Hydraulic

- 5.2.5 Pneumatic

- 5.3 By End-user Industry

- 5.3.1 Oil and Gas

- 5.3.2 Water and Waste-water

- 5.3.3 Chemicals and Petrochemicals

- 5.3.4 Power Generation

- 5.3.5 Mining

- 5.3.6 Food and Beverage

- 5.3.7 Pharmaceuticals

- 5.3.8 Pulp and Paper

- 5.3.9 Others

- 5.4 By Pump Orientation

- 5.4.1 Submersible

- 5.4.2 Surface

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Russia

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 Taiwan

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Turkey

- 5.5.5.1.2 Israel

- 5.5.5.1.3 GCC Countries

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Flowserve Corporation

- 6.4.2 Grundfos Holding A/S

- 6.4.3 Xylem Inc.

- 6.4.4 Sulzer Ltd.

- 6.4.5 KSB SE & Co. KGaA

- 6.4.6 ITT Inc.

- 6.4.7 Ebara Corporation

- 6.4.8 The Weir Group PLC

- 6.4.9 Schlumberger NV (REDA Pump)

- 6.4.10 Baker Hughes Company

- 6.4.11 SPX FLOW Inc.

- 6.4.12 Wilo SE

- 6.4.13 Dover Corporation

- 6.4.14 Pentair plc

- 6.4.15 Franklin Electric Co. Inc.

- 6.4.16 Tsurumi Manufacturing Co. Ltd.

- 6.4.17 Kirloskar Brothers Ltd.

- 6.4.18 Atlas Copco AB

- 6.4.19 Ruhrpumpen Group

- 6.4.20 Zoeller Company

- 6.4.21 Roto Pumps Ltd.

- 6.4.22 Gardner Denver LLC (Ingersoll Rand)

- 6.4.23 ClydeUnion Pumps (Celeros Flow Tech)

- 6.4.24 LEWA GmbH

- 6.4.25 Graco Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

集中式冷卻液分配單元市場:依產品類型、流量、壓力、控制類型、部署方式、應用、最終用戶產業、通路分類,全球預測,2026-2032年定排量柱塞泵市場:按類型、流量、排氣量範圍、材質、驅動方式、壓力、應用、最終用戶分類,全球預測(2026-2032年)礦用噴霧泵市場:按泵類型、動力源、材質、壓力範圍、應用、分銷管道、最終用戶分類,全球預測(2026-2032年)高壓軸柱塞泵市場:按類型、設計、驅動系統、壓力範圍、流量、應用和分銷管道分類,全球預測,2026-2032年水泵控制面板市場:按類型、水泵類型、電壓、安裝方式、應用、最終用戶、分銷管道分類,全球預測(2026-2032年)無軸輪緣驅動推進器市場:船舶、額定功率、螺旋槳直徑、推力能力、最終用戶、全球預測,2026-2032年全球熱交換油泵市場(按泵類型、驅動頻率、額定功率、流量和最終用途產業分類),2026-2032年預測

集中式冷卻液分配單元市場:依產品類型、流量、壓力、控制類型、部署方式、應用、最終用戶產業、通路分類,全球預測,2026-2032年定排量柱塞泵市場:按類型、流量、排氣量範圍、材質、驅動方式、壓力、應用、最終用戶分類,全球預測(2026-2032年)礦用噴霧泵市場:按泵類型、動力源、材質、壓力範圍、應用、分銷管道、最終用戶分類,全球預測(2026-2032年)高壓軸柱塞泵市場:按類型、設計、驅動系統、壓力範圍、流量、應用和分銷管道分類,全球預測,2026-2032年水泵控制面板市場:按類型、水泵類型、電壓、安裝方式、應用、最終用戶、分銷管道分類,全球預測(2026-2032年)無軸輪緣驅動推進器市場:船舶、額定功率、螺旋槳直徑、推力能力、最終用戶、全球預測,2026-2032年全球熱交換油泵市場(按泵類型、驅動頻率、額定功率、流量和最終用途產業分類),2026-2032年預測 工業泵浦市場:依類型、安裝位置、驅動類型和行業劃分 - 全球預測至 2036 年

工業泵浦市場:依類型、安裝位置、驅動類型和行業劃分 - 全球預測至 2036 年 日本工業泵浦市場規模、佔有率、趨勢及預測(按產品、通路、應用及地區分類,2026-2034年)日本工業泵閥市場規模、佔有率、趨勢及預測(按產品類型、安裝位置、促進因素、最終用途和地區分類,2026-2034年)

日本工業泵浦市場規模、佔有率、趨勢及預測(按產品、通路、應用及地區分類,2026-2034年)日本工業泵閥市場規模、佔有率、趨勢及預測(按產品類型、安裝位置、促進因素、最終用途和地區分類,2026-2034年)