|

市場調查報告書

商品編碼

1844714

碳纖維增強熱塑性(CFRTP)複合材料:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030)Carbon Fiber Reinforced Thermoplastic (CFRTP) Composite - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

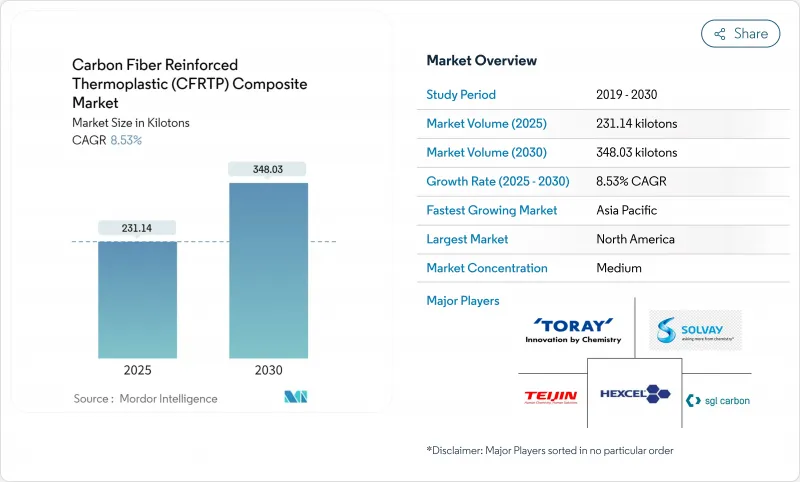

碳纖維增強熱塑性 (CFRTP) 複合材料市場規模預計在 2025 年為 231.14 千噸,預計到 2030 年將達到 348.03 千噸,預測期內(2025-2030 年)的複合年成長率為 8.53%。

這一強勁成長反映了該材料兼具航太級強度重量比和完全可回收性的能力,這與交通運輸、能源和建築行業的脫碳目標相一致。電動車產量的上升、商用飛機製造率的回升以及蓬勃發展的儲氫計畫推動了需求的成長。同時,節能纖維生產和積層製造領域的突破性創新正在降低進入門檻,區域性回收法規正在為供應商創造新的收益來源。隨著綜合性現有企業為抵禦區域性產能擴張和專業回收商的衝擊而爭奪市場佔有率,競爭日益激烈。

全球碳纖維增強熱塑性 (CFRTP) 複合材料市場趨勢與洞察

輕型電動車結構需求激增

汽車製造商擴大將碳纖維熱塑性塑膠用於電池機殼、車身面板和底盤零件,以延長續航里程並縮短充電時間。該材料的可逆熔化特性支持使用後回收,並符合中國和歐盟目前正在製定的循環經濟法規。車隊營運商受益於更便捷的維修,因為損壞的零件可以重新加熱和再形成,而無需更換。特斯拉在其人形機器人中採用碳纖維複合材料,凸顯了其在汽車以外的多功能性,並暗示了其擴展到多個移動平台的潛力。中國將在2024年消耗6.9萬噸碳纖維,顯示亞洲的需求基礎正在持續成長。

加速民航機生產擴張

機身原始設備製造商正在重組其供應鏈,以滿足737 MAX和787夢幻飛機的生產目標,從而滿足用於降低燃油消耗的二級結構複合材料的需求。赫氏在第一季的財務業績中報告銷售額下降,但重申了對輕質熱塑性解決方案的投資。電動飛機的轉變將推動熱塑性塑膠的應用,因為基質材料可用於絕緣線路並整合防冰加熱器。歐洲熱塑性複合材料研究中心(TPRC)下屬的舉措加速了大批量零件的認證,縮短了從設計到飛行的時間表。與金屬相比,熱塑性塑膠卓越的抗疲勞性能可延長維修間隔,此優勢在新冠疫情爆發後受到航空公司的高度重視。

初期投資和製造成本高

高壓釜、壓機和自動纖維鋪放單元每條生產線的成本可能超過3000萬美元,阻礙了價格敏感產業的進入,並減緩了其應用。西格里碳素公司(SGL Carbon)報告稱,2024年碳纖維銷售額下降了35.2%,因為需求波動導致高固定成本資產利用不足。利默里克大學示範的等離子和微波加熱技術可將能耗降低高達70%,但商業化仍需數年時間。由於原始纖維仍然比鋁和鋼更昂貴,複合材料尚未被經濟型汽車採用。只有當產量允許工具攤銷時,經濟效益才會改善,這導致原始設備製造商(OEM)在下游需求得到確認之前猶豫不決。

細分分析

到2024年,PAN基牌號將佔總產量的78.12%,這印證了其成熟的生產線和航太的悠久歷史。其高拉伸模量使設計人員能夠在滿足安全裕度的同時減輕結構重量。隨著現有企業維修連續生產線以提高產量,PAN基碳纖維增強熱塑性複合材料市場規模預計將以7.9%的複合年成長率穩定成長。經濟高效的再加熱循環可降低廢品率,並增強工廠經濟效益。

包括再生纖維在內的其他原料的複合年成長率為9.71%,在原料中最高。目前,再生纖維的拉伸強度可達原生纖維的93.6%,這拓寬了其在二次負荷路徑中的適用性。 Syensqo和Trillium正在探索的生物基丙烯腈,標誌著公司將長期轉向更環保的原料。利基瀝青基材料具有類似金屬的導電性,有助於電池組的溫度控管。雖然產量較低,但高昂的定價平衡了供應限制,並維持了相當吸引人的利潤率。

到2024年,PEEK將佔據34.51%的市場佔有率,以9.82%的複合年成長率引領成長,這得益於其250°C的連續使用溫度和化學惰性。碳纖維增強熱塑性複合材料市場的主導地位將在對可燃性和煙霧毒性有嚴格規定的領域尤為突出,例如噴射引擎和海上平台。醫療設備應用將實現收益多元化,並分散各行業的風險。

成本敏感型產業依賴聚氨酯 (PU)、聚醚碸 (PES) 和聚醚醯亞胺 (PEI),這些材料以降低峰值溫度來換取價格。這些樹脂用於中等負載的內裝面板和家用電器。目前正在研發的生物基聚醚醯亞胺 (PEI) 可以在不犧牲機械性能的情況下,增加永續性的差異化優勢。樹脂複合材料製造商正在添加奈米填料,以增強導電性,並在航太系統中建造整合除冰層。

碳纖維增強熱塑性複合材料市場報告按原料(PAN基、瀝青基、其他)、樹脂(PEEK、PU、其他)、製造程序(模壓成型、AFP/鋪帶、其他)、終端用戶行業(航太和國防、汽車、其他)和地區(亞太地區、北美、其他)細分。市場預測以千噸為單位。

區域分析

到2024年,北美將佔據36.19%的市場佔有率,這得益於美國航太和國防綜合體以及加拿大的MRO中心的支持。東麗、赫氏和索爾維等公司在當地的佈局縮短了前置作業時間,並保護了專案免受地緣政治風險的影響。 《通膨控制法》下的政府補貼鼓勵了國內氫氣罐的生產,從而刺激了下游需求。

到2030年,亞太地區的複合年成長率將達到9.21%,位居榜首。中國正在加大電動車產量,目前擁有多條千噸級碳纖維生產線,正在減少先前對進口的依賴。日本的先驅企業東麗和帝人正在將其產能加倍,以支持該地區的風電和海上計劃。韓國正在利用其電子技術,將EMI屏蔽複合材料整合到5G基礎設施中。

歐洲市場需求強勁,但監管方面也面臨新的阻力。德國汽車產業仍然是最大的消費國,但即將訂定的可回收性法規正推動熱塑性塑膠替代品的快速普及。荷蘭熱塑性複合材料研究中心支援原始設備製造商和供應商之間的研發合作。北歐風能投資和法國航太叢集抵消了一般工業需求的疲軟。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場狀況

- 市場概況

- 市場促進因素

- 輕型電動車結構需求激增

- 加速民航機生產

- 全球更嚴格的排放法規和回收義務

- 在建築業的使用日益增多

- 氫氣壓力容器計畫快速擴大規模

- 市場限制

- 初期投資和製造成本高

- 大型熱成型壓機產能的局限性

- 航太供應鏈武器化的風險

- 價值鏈分析

- 五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章市場規模及成長預測(數量)

- 按原料

- 聚丙烯腈(PAN)基碳纖維增強複合材料(CFRTP)

- 瀝青基碳纖維增強複合材料(CFRTP)

- 其他原料(再生碳纖維等)

- 按樹脂

- 聚醚醚酮(PEEK)

- 聚氨酯(PU)

- 聚醚碸(PES)

- 聚醚醯亞胺(PEI)

- 其他(聚醯胺、聚碳酸酯等)

- 按製造程序

- 壓縮/沖壓成型

- 自動纖維鋪放/鋪帶

- 射出成型和包覆成型

- 積層製造(碳纖維長絲)

- 按最終用戶產業

- 航太和國防

- 車

- 建造

- 電氣和電子

- 風力發電機

- 海洋

- 運動器材

- 其他最終用戶產業(醫療保健等)

- 按地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 東南亞國協

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭態勢

- 市場集中度

- 策略舉措

- 市佔率(%)/排名分析

- 公司簡介

- Arkema

- ARRIS Composites, Inc.

- Avient Corporation

- BASF

- Celanese Corporation

- DuPont

- Gurit Services AG, Zurich

- Hexcel Corporation

- Markforged

- Mitsubishi Chemical Corporation

- Quickstep

- SABIC

- SGL Carbon

- Syensqo

- Teijin Limited

- Toray Industries Inc.

- Victrex plc

第7章 市場機會與未來展望

The Carbon Fiber Reinforced Thermoplastic Composite Market size is estimated at 231.14 kilotons in 2025, and is expected to reach 348.03 kilotons by 2030, at a CAGR of 8.53% during the forecast period (2025-2030).

Robust growth reflects the material's ability to pair aerospace-grade strength-to-weight ratios with full recyclability, aligning with decarbonization targets across transportation, energy, and construction. Rising electric-vehicle production, a rebound in commercial aircraft build rates, and fast-moving hydrogen storage programs form the core demand pillars. At the same time, breakthroughs in energy-efficient fiber production and additive manufacturing lower entry barriers, while regional recycling mandates open fresh revenue pools for suppliers. Competitive intensity is building as integrated incumbents defend share against regional capacity buildouts and specialist recyclers.

Global Carbon Fiber Reinforced Thermoplastic (CFRTP) Composite Market Trends and Insights

Surging Demand for Lightweight EV Structures

Automakers increase carbon fiber thermoplastic use in battery enclosures, body panels, and chassis members to extend driving range and cut charging time. The material's reversible melt behavior supports end-of-life recycling, satisfying circular-economy rules now unfolding in China and the European Union. Fleet operators benefit from easier repair because damaged parts can be reheated and reshaped instead of replaced. Tesla's application of carbon fiber composites in its humanoid robot underscores versatility beyond vehicles, suggesting spillover into multiple mobility platforms. China consumed 69,000 metric tons of carbon fiber in 2024, evidence of a deepening Asian demand base.

Accelerating Commercial Aircraft Production Ramp-ups

Airframe OEMs are rebuilding supply chains to meet higher 737 MAX and 787 Dreamliner output targets, sustaining composite demand for secondary structures that cut fuel burn. Hexcel reaffirmed investment in lightweight thermoplastic solutions in its Q1 2025 earnings report, despite lower top-line sales. The shift to more-electric aircraft fosters thermoplastic adoption because the matrix insulates wiring and integrates anti-icing heaters. European initiatives under the ThermoPlastic Composites Research Center (TPRC) accelerate certification of large-volume parts, shortening design-to-flight timelines. Superior fatigue resistance over metals lengthens service intervals, an advantage keenly valued by airlines after COVID-19 disruptions.

High Initial Investment and Manufacturing Cost

Autoclaves, compression presses, and automated fiber placement cells can top USD 30 million per line, curbing entry and slowing adoption in price-sensitive segments. SGL Carbon reported a 35.2% sales drop in its Carbon Fibers unit in 2024, citing demand swings that leave high fixed-cost assets under-utilized. Plasma + microwave heating demonstrated at the University of Limerick cuts energy up to 70%, yet commercial readiness remains several years out. Raw fiber remains costlier than aluminum or steel, keeping composites out of economy-class vehicles. Economics improve only when volumes amortize tooling, thus OEMs hesitate until downstream demand is locked.

Other drivers and restraints analyzed in the detailed report include:

- Stringent Global Emission and Recyclability Mandates

- Rapid Scale-up of Hydrogen Pressure-Vessel Programs

- Limited Large-scale Thermoforming Press Capacity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

PAN-based grades delivered 78.12% of 2024 volume, underlining their entrenched production lines and aerospace heritage. High tensile modulus lets designers trim structural weight while meeting safety margins. The carbon fiber reinforced thermoplastic composite market size for PAN-based grades is projected to expand at a stable 7.9% CAGR as incumbents retrofit continuous lines for higher throughput. Cost-effective reheat cycles improve scrap rates, enhancing plant economics.

Other Raw Materials, including recycled fiber, register a 9.71% CAGR-the highest within raw materials-as end-users adopt circular procurement goals. Recycled fiber now retains 93.6% of virgin tensile strength, widening suitability for secondary load paths. Bio-sourced acrylonitrile under study by Syensqo and Trillium signals a longer-term pivot to greener feedstocks. Niche pitch-based grades serve thermal management in battery packs because of metal-like conductivity. Though volume small, premium pricing balances supply constraint, keeping margins attractive.

PEEK secured 34.51% 2024 share and leads growth at 9.82% CAGR thanks to 250 °C continuous-use temperature and chemical inertness. The carbon fiber reinforced thermoplastic composite market share advantage strengthens where flammability and smoke toxicity rules are strict, notably in jet engines and offshore platforms. Medical device usage diversifies revenue, spreading risk across sectors.

Cost-focused segments rely on PU, PES, or PEI which trade peak temperature for price. These resins feed interior panels and consumer electronics where operating loads are moderate. Bio-based PEI under exploration could add a sustainability differentiator without forfeiting mechanical properties. Resin formulators also blend nano-fillers to enhance conductivity, fostering integrated de-icing layers in aerospace systems.

The Carbon Fiber Reinforced Thermoplastic Composite Market Report is Segmented by Raw Material (PAN-Based, Pitch-Based, and More), Resin (PEEK, PU, and More), Manufacturing Process (Compression Molding, AFP/Tape Laying, and More), End-User Industry (Aerospace and Defense, Automotive, and More), and Geography (Asia-Pacific, North America, and More). The Market Forecasts are Provided in Terms of Volume (Kilotons).

Geography Analysis

North America held 36.19% share in 2024, anchored by the United States' aerospace and defence complex and supported by Canada's MRO hubs. Local presence of Toray, Hexcel, and Solvay shortens lead times, safeguarding programs against geopolitical risk. Government grants under the Inflation Reduction Act encourage domestic hydrogen tank production, widening downstream pull.

Asia-Pacific posts the fastest 9.21% CAGR to 2030. China scales electric-vehicle output and now hosts multiple kiloton-scale carbon fiber lines, reducing earlier import dependence. Japanese pioneers Toray and Teijin double capacity to serve regional wind and marine projects. South Korea leverages electronics know-how to integrate EMI-shielding composites into 5G infrastructure.

Europe mixes strong demand with new regulatory headwinds. Germany's auto base remains the largest segment consumer, but looming recyclability rules fast-track thermoplastic substitution. The ThermoPlastic Composites Research Center in the Netherlands anchors R&D alliances across OEMs and suppliers. Nordic wind investments and French aerospace clusters offset softness in general industrial demand.

- Arkema

- ARRIS Composites, Inc.

- Avient Corporation

- BASF

- Celanese Corporation

- DuPont

- Gurit Services AG, Zurich

- Hexcel Corporation

- Markforged

- Mitsubishi Chemical Corporation

- Quickstep

- SABIC

- SGL Carbon

- Syensqo

- Teijin Limited

- Toray Industries Inc.

- Victrex plc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging demand for lightweight EV structures

- 4.2.2 Accelerating commercial aircraft production ramp-ups

- 4.2.3 Stringent global emission and recyclability mandates

- 4.2.4 Incresaing usage in the construction sector

- 4.2.5 Rapid scale-up of hydrogen pressure-vessel programs

- 4.3 Market Restraints

- 4.3.1 High initial investment and manufacturing cost

- 4.3.2 Limited large-scale thermoforming press capacity

- 4.3.3 Supply-chain weaponisation risk in aerospace

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Raw Material

- 5.1.1 Polyacrylonitrile (PAN)-based Carbon Fiber Reinforced Composites (CFRTP)

- 5.1.2 Pitch-based Carbon Fiber Reinforced Composites (CFRTP)

- 5.1.3 Other Raw Materials (Recycled Carbon Fibers, etc.)

- 5.2 By Resin

- 5.2.1 Polyether Ether Ketone (PEEK)

- 5.2.2 Polyurethane (PU)

- 5.2.3 PolyetherSulfone (PES)

- 5.2.4 Polyetherimide (PEI)

- 5.2.5 Others (Polyamide, Polycarbonate, etc.)

- 5.3 By Manufacturing Process

- 5.3.1 Compression and Stamp Moulding

- 5.3.2 Automated Fibre Placement / Tape Laying

- 5.3.3 Injection and Over-Moulding

- 5.3.4 Additive Manufacturing (Carbon Fiber-filled filaments)

- 5.4 By End-user Industry

- 5.4.1 Aerospace and Defence

- 5.4.2 Automotive

- 5.4.3 Construction

- 5.4.4 Electrical and Electronics

- 5.4.5 Wind Turbines

- 5.4.6 Marine

- 5.4.7 Sporting Equipments

- 5.4.8 Other End-user Industries (Healthcare, etc.)

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 Japan

- 5.5.1.3 India

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 NORDIC Countries

- 5.5.3.8 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Arkema

- 6.4.2 ARRIS Composites, Inc.

- 6.4.3 Avient Corporation

- 6.4.4 BASF

- 6.4.5 Celanese Corporation

- 6.4.6 DuPont

- 6.4.7 Gurit Services AG, Zurich

- 6.4.8 Hexcel Corporation

- 6.4.9 Markforged

- 6.4.10 Mitsubishi Chemical Corporation

- 6.4.11 Quickstep

- 6.4.12 SABIC

- 6.4.13 SGL Carbon

- 6.4.14 Syensqo

- 6.4.15 Teijin Limited

- 6.4.16 Toray Industries Inc.

- 6.4.17 Victrex plc

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

纖維增強複合材料市場:依纖維類型、樹脂類型、製造流程、增強材料形式和應用分類-2026-2032年全球市場預測CFRTP市場:2026-2032年全球市場預測(按樹脂類型、產品類型、纖維類型、製造流程、應用和最終用戶分類)雙組分纖維市場:依纖維類型、製造流程、應用和分銷管道分類-2026-2032年全球預測半導體CFC設備市場:按類型、技術和終端用戶產業分類,全球預測,2026-2032年

纖維增強複合材料市場:依纖維類型、樹脂類型、製造流程、增強材料形式和應用分類-2026-2032年全球市場預測CFRTP市場:2026-2032年全球市場預測(按樹脂類型、產品類型、纖維類型、製造流程、應用和最終用戶分類)雙組分纖維市場:依纖維類型、製造流程、應用和分銷管道分類-2026-2032年全球預測半導體CFC設備市場:按類型、技術和終端用戶產業分類,全球預測,2026-2032年 全球雙組分纖維市場規模、佔有率、趨勢和成長分析報告:2026-2034年CFRT預浸料市場按樹脂類型、纖維類型、產品形式、製造流程、最終用途產業和應用分類-2026-2032年全球預測植物纖維增強複合材料市場:依應用、基體類型、纖維類型、製造流程及纖維處理方式分類-2026-2032年全球預測碳纖維增強熱塑性複合材料(CFRTP)市場-2025-2030年預測

全球雙組分纖維市場規模、佔有率、趨勢和成長分析報告:2026-2034年CFRT預浸料市場按樹脂類型、纖維類型、產品形式、製造流程、最終用途產業和應用分類-2026-2032年全球預測植物纖維增強複合材料市場:依應用、基體類型、纖維類型、製造流程及纖維處理方式分類-2026-2032年全球預測碳纖維增強熱塑性複合材料(CFRTP)市場-2025-2030年預測 全球短纖維增強複合材料 (SFRC) 市場、需求、產能、數量、價格分佈

全球短纖維增強複合材料 (SFRC) 市場、需求、產能、數量、價格分佈 全球雙組分纖維市場

全球雙組分纖維市場