|

市場調查報告書

商品編碼

1844621

銀行業的 UCaaS:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)UCaaS In Banking - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

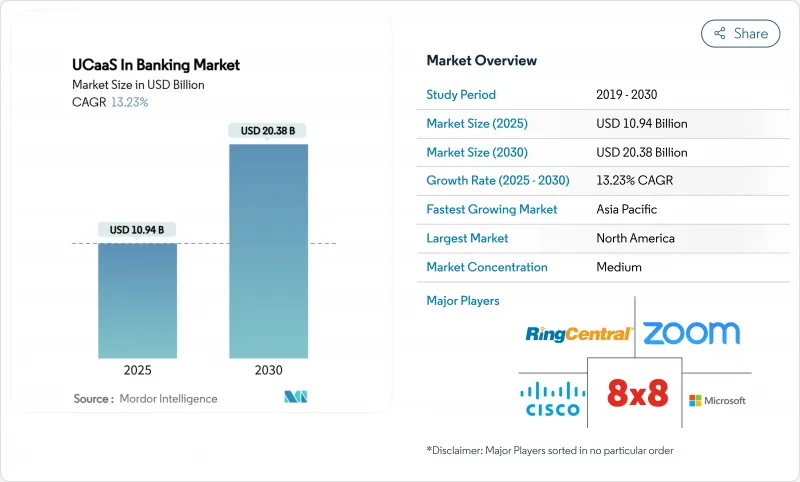

預計到 2025 年銀行市場 UCaaS 將達到 109.4 億美元,到 2030 年將達到 203.8 億美元,複合年成長率為 13.23%。

這項市場擴張反映了產業向雲端原生通訊的決定性轉變,以維持混合勞動力並滿足嚴格的監管審核追蹤。對無縫客戶參與、加速的金融科技夥伴關係以及更快的新數位產品上市時間日益成長的需求進一步推動了採用。雖然公共雲端UCaaS 仍然很受歡迎,但隨著銀行尋求在不犧牲靈活容量的情況下獲得細粒度的資料主權,混合架構正在興起。巴克萊銀行在全球推出 Microsoft Teams 等策略性採用正在推動整合平台的興起,這些平台可簡化傳統語音安裝、整合協作工具並降低整體擁有成本。隨著通訊業者與結合人工智慧 (AI) 功能(例如即時語言翻譯、情緒評分和合規性監控)的雲端原生專家競爭,競爭正在加劇。

全球銀行 UCaaS 市場趨勢與洞察

BYOD 和行動辦公

隨著混合型員工逐漸將個人設備使用標準化,銀行機構正逐漸擺脫對桌上型電話的依賴。 UCaaS 工具能夠端對端加密流量、強制執行基於角色的策略並聯合身份,使員工能夠從任何地方進行連接,且不影響合規性。瑞穗證券決定將外部通訊遷移至 Zoom,並採用其主動主機收費模式,這清楚地表明了靈活的許可機制如何在保持審核的同時降低暫停狀態席位成本。 BYOD 策略可以降低硬體支出並提高員工滿意度,但需要先進的行動裝置管理和地理圍籬功能才能滿足預防資料外泄法規的要求。行動性支援與 UCaaS 安全性之間的相互作用,鞏固了能夠兼顧靈活性和嚴格監管的銀行的競爭優勢。

企業範圍 UC 整合的需求

過去,語音、聊天和交易大廳管道彼此孤立,阻礙了流暢的協作。現代 UCaaS 平台統一了這些接觸點,並整合了工作流程觸發器,以確保警報和文件在分店、客服中心和合規部門之間流暢地流動。 NTT Communications 透過單一租戶全球 UC 架構支援 190 多個國家/地區,使跨國銀行能夠標準化撥號計畫、報告和策略執行,同時降低維護開銷。在合併期間,新收購的分店必須快速過渡,因此對整合的需求更加迫切。領先的解決方案現在應用人工智慧將問詢路由到最合適的專家,從而提高首次呼叫解決率指標並最佳化人員配置。統一跨管道的血緣關係也簡化了電子取證請求,監管機構預計該請求將在數小時內完成。

二、三線銀行對雲端統一通訊的認知度較低

區域性金融機構通常缺乏專業人員來評估統一通訊即服務 (UCaaS)提案,並預設透過現有業者進行傳統電話通訊。美國評估警告稱,有限的雲端知識會使中小型銀行面臨潛在的彈性和網路風險,延長傳統系統的使用時間,並限制其現代化進程。因此,教育加速器、藍圖模板和託管服務包在降低准入門檻方面發揮著至關重要的作用。提供遷移獎勵、承包安全管理和監管文件的提供者可以解鎖這一服務不足的群體。

細分分析

到2024年,語音通訊將佔銀行統一通訊即服務(UCaaS)市場規模的42.5%,因為語音對於詐欺偵測、交易執行和客戶身份驗證至關重要。然而,隨著視訊、持續聊天和共用文件工作區整合到單一管理平台,預計到2030年,協作套件的複合年成長率將達到18.50%。這種融合減少了客戶關係經理的「椅子旋轉」時間,加快了入職和問題解決速度。 Five9報告稱,自然語言處理路由器現在可將80%的入境轉接給合適的技能組,無需人工分類,從而降低了放棄率。統一通訊將電子郵件、簡訊和安全聊天訊息壓縮成一個執行緒歷史記錄,提高了合規性的審核。視訊銀行自助服務終端將諮詢服務擴展到農村地區,通訊平台API將雙重認證語音通話直接嵌入到行動應用程式中。這種模組化設計使銀行無需重新設計後端核心即可添加管道,從而增強了平台黏性並增加了轉換成本。

隨著銀行透過應用程式內橫幅廣告、RCS 和 OTT 即時通訊應用程式等方式推出貸款核准通知、外匯提醒和卡片使用異常等情境通知,對嵌入式通訊的需求日益成長。 Webex CPaaS 銀行模組透過 WhatsApp 和 Apple Messages 的開箱即用範本加速部署,同時保留加密和審核日誌記錄功能。這種 API 優先的模型使開發人員能夠編配各種流程,例如當高價值交易超過預設閾值時,聊天機器人會升級到安全視訊。 Gartner 預測,到 2030 年,API主導的管道將佔金融服務出站流量的一半,這凸顯了語音通訊正逐漸從獨立產品轉變為整合套件中的基礎服務。

在承包可擴展性和消費定價的推動下,公共雲端將在2024年佔據銀行UCaaS市場佔有率的61.4%。然而,預計到2030年,混合雲的複合年成長率將達到19.20%,反映出董事會對司法合規性和延遲敏感型工作負載的關注度日益提高。 First Horizon Bank遷移到Webex Contact Center採用了分層架構,將受監管的員工記錄保存在本地,同時AI分析在思科的多租戶雲端中處理匿名資料。這一藍圖使該銀行能夠在單一主機上維護2萬個終端和750名座席,而不會違反受託資料處理義務。

雖然私有雲端仍然是擁有客製化加密和主權授權的全球性、系統重要性銀行的一種選擇,但資本和人員配置要求限制了其吸引力。混合策略支援分階段遷移,允許逐步淘汰每個站點老化的PBX,並將流量透過會話邊界控制器傳輸到雲端核心。持續整合管道支援降級功能,例如噪音抑制和自動重新編輯,而無需停機。隨著環境、社會和管治承諾的不斷增加,工作負載彈性還可以減少閒置能源消耗,幫助銀行實現碳減排目標。

全球銀行整合通訊即服務 (UCaaS) 市場根據組件(語音通訊、統一通訊、客服中心、協作平台等)、部署模型(公共雲端、混合雲端、私有雲端)、組織規模(中小企業、大型企業)、銀行應用(零售銀行、企業和批發銀行等)和地區進行細分。

區域分析

至2024年,北美銀行業UCaaS市佔率將維持36.7%,並利用成熟的雲端法規和雄厚的預算進行企業現代化。巴克萊銀行、瑞銀集團和花旗集團是大規模部署的典範,它們將AI Copilot與協作套件結合,以簡化顧問工作流程。雖然正在取得進展,但只有不到40%的公司完成了遷移,許多地區性銀行仍然依賴老舊的PBX。因此,混合部署正成為主流,在轉型動能與審慎的風險管理之間取得平衡。

到2030年,亞太地區將以14.80%的複合年成長率引領成長,因為行動優先的人口結構促使數位銀行將語音和訊息直接嵌入其應用程式中。 NTT和Softbank Corporation等日本通訊業者將其UCaaS業務拓展至全球,而Vonage與當地整合商的夥伴關係則將東南亞各地的客服中心設施數位化。對話式人工智慧的採用正在加速,提高了首次解決率,並實現了全天候多語言支援。

在歐洲,對資料主權的日益重視促使銀行青睞區域鎖定的雲端服務和主權夥伴關係關係。義大利裕信銀行 (UniCredit) 斥資 4 億美元收購 Vodeno,提供了一個包含智慧合約引擎的雲端原生平台,滿足 PSD2 開放銀行要求並擴展了白牌功能。在中東和非洲,雲端技術的採用正在超越傳統的 PBX。例如,Ecobank 與Google雲端合作,正在 35 個國家/地區推進一項由分析主導的包容性計劃。這些市場凸顯了統一通訊即服務 (UCaaS) 在實體店稀少地區彌合服務缺口方面的作用。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場狀況

- 市場概況

- 市場促進因素

- BYOD 和行動辦公

- 企業範圍 UC 整合的需求

- 純數位銀行的興起

- 支援 AI 的 UCaaS,用於合規性監控

- 5G專網

- 將 CPaaS 嵌入銀行應用程式

- 市場限制

- 二、三線銀行對雲端統一通訊的認知度較低

- 嚴格的資料安全和居住要求

- 傳統的本地 PBX 鎖定

- 供應商 API 鎖定風險

- 關鍵法規結構的評估

- 價值鏈分析

- 技術展望

- 五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 關鍵用例和案例研究

- 宏觀經濟因素對市場的影響

- 投資分析

第5章市場區隔

- 按組件

- 語音通訊

- 統一通訊

- 客服中心

- 協作平台

- 視訊會議

- 通訊平台API

- 按部署模型

- 公共雲端

- 私有雲端

- 混合雲端

- 按組織規模

- 主要企業

- 小型企業

- 透過銀行申請

- 零售銀行

- 企業及批發銀行業務

- 投資銀行

- 支付及金融科技子公司

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲和紐西蘭

- 其他亞太地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 埃及

- 其他非洲國家

- 北美洲

第6章 競爭態勢

- 市場集中度

- 策略舉措

- 市佔率分析

- 公司簡介

- Microsoft Corporation

- Cisco Systems, Inc.

- RingCentral, Inc.

- 8x8, Inc.

- Zoom Video Communications, Inc.

- Avaya LLC

- Fuze, Inc.

- West Technology Group, LLC(formerly West UC)

- VOSS Solutions

- NetFortris, Inc.

- TetraVX(Netrix, LLC)

- Kurmi Software SAS

- Vonage Holdings Corp.

- Dialpad, Inc.

- Mitel Networks Corporation

- Revation Systems, Inc.

- NICE Ltd.

- Genesys Telecommunications Labs, Inc.

- Google LLC

- Amazon Web Services, Inc.

第7章 市場機會與未來展望

The UCaaS in banking market size stood at USD 10.94 billion in 2025 and is forecast to reach USD 20.38 billion by 2030, advancing at a 13.23% CAGR.

The expansion reflects a decisive industry shift toward cloud-native communications that sustain hybrid workforces and satisfy strict regulatory audit trails. Heightened demand for seamless customer engagement, accelerated fintech partnerships, and accelerated time-to-market for new digital products further uplift adoption. Public-cloud UCaaS remains pervasive, yet hybrid architectures are gaining ground as banks seek fine-grained data-sovereignty control without forfeiting the flexibility of elastic capacity. Strategic deployments-such as Barclays' global roll-out of Microsoft Teams-spotlight how integrated platforms rationalize legacy voice estates, consolidate collaboration tools and contain total cost of ownership. Competitive intensity is shaped by telecom incumbents battling cloud-native specialists that embed artificial-intelligence (AI) functions such as real-time language translation, sentiment scoring and compliance surveillance.

Global UCaaS In Banking Market Trends and Insights

BYOD and Workforce Mobility

Banking institutions are dismantling desk-phone dependencies as hybrid workforces normalize personal device use. UCaaS tools that encrypt traffic end-to-end, enforce role-based policies and federate identity allow staff to connect from any location without jeopardizing compliance. Mizuho Securities' decision to migrate external communications to Zoom under an active-host billing model underscores how flexible licensing reduces dormant seat costs while sustaining auditability. BYOD strategies cut hardware outlays and elevate employee satisfaction, yet they demand advanced mobile-device-management and geo-fencing to meet sectoral data-loss-prevention rules. The interplay between mobility enablement and UCaaS security solidifies competitive advantage for banks able to blend flexibility with rigorous supervision.

Need for Enterprise-wide UC Integration

Historically, siloed voice, chat and trading-floor channels obstructed fluid collaboration. Contemporary UCaaS platforms unify these touchpoints and embed workflow triggers so alerts and documents flow between branches, contact centers and compliance desks. NTT Communications underpins more than 190 countries with a single-tenant global UC fabric, allowing multinational banks to standardize dial plans, reporting and policy enforcement while trimming maintenance overhead. Integration imperatives intensify during mergers, when newly acquired branches must migrate rapidly. Leading solutions now apply AI to route queries to the best-suited specialist, elevating first-call-resolution metrics and optimizing workforce allocation. Unified lineage across channels also simplifies e-discovery requests, which regulators expect within hours.

Low Cloud-UC Awareness in Tier-2/3 Banks

Community institutions often lack specialist staff to evaluate UCaaS proposals, defaulting to incumbent telcos for plain-old telephony. A U.S. Treasury-commissioned assessment warns that limited cloud acumen exposes smaller banks to hidden resiliency and cyber risks, prolonging legacy usage and constraining modernization. Educational accelerators, blueprint templates and managed-service bundles therefore play a pivotal role in lowering entry barriers. Providers that extend migration incentives, turnkey security controls and regulatory documentation can unlock this underserved cohort.

Other drivers and restraints analyzed in the detailed report include:

- Digital-only Banking Expansion

- AI-Enabled UCaaS for Compliance Monitoring

- Stringent Data-Security and Residency Mandates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Telephony accounted for 42.5% of the UCaaS in banking market size in 2024 as voice remains indispensable for fraud verification, trade execution and customer identity confirmation. Collaboration suites, however, are projected to drive an 18.50% CAGR through 2030 as video, persistent chat and shared-document workspaces coalesce into a single pane. The convergence reduces swivel-chair actions for relationship managers, speeding onboarding and issue resolution. Five9 reports that natural-language-processing routers now direct 80% of inbound calls to the correct skill group without human triage, trimming abandonment rates. Unified messaging compresses email, SMS and secure chat feeds into threaded histories, boosting compliance auditability. Video-banking kiosks extend advisory services to rural zones, while communication-platform APIs embed two-factor-authentication voice calls directly into mobile apps. This modularity ensures banks add channels without re-architecting back-end cores, reinforcing platform stickiness and raising switching costs.

Demand for embedded communications intensifies as banks deploy contextual notifications-loan-approval pings, FX-rate alerts and card-usage anomalies-through in-app banners, RCS and OTT messengers. Webex CPaaS banking modules deliver out-of-the-box templates for WhatsApp and Apple Messages, accelerating deployment while retaining encryption and audit logging. Such API-first models empower developers to orchestrate journeys where a chatbot escalates to secure video when high-value transactions exceed preset thresholds. Gartner predicts that by 2030, API-driven channels will account for half of financial-services outbound traffic, underscoring telephony's gradual transition from standalone product to foundational service within integrated suites.

Public-cloud captured 61.4% of UCaaS in banking market share in 2024 on the back of turnkey scalability and consumption pricing. Yet hybrid approaches, forecasting a 19.20% CAGR to 2030, reflect heightened boardroom focus on jurisdictional compliance and latency-sensitive workloads. First Horizon Bank's Webex Contact Center migration showcased a layered architecture where recordings of regulated staff remained on-prem while AI analytics processed anonymized data in Cisco's multitenant cloud. This blueprint allowed the bank to maintain 20,000 endpoints and 750 agents under one console without breaching fiduciary data-handling obligations.

Private-cloud remains an option for global systemically important banks with bespoke encryption and sovereignty mandates, although capital and staffing requirements curb its wider appeal. Hybrid strategies support phased migration: institutions can retire aging PBXs site by site, funneling traffic via session-border controllers to a cloud core. Continuous-integration pipelines then deliver feature drops such as noise suppression or auto-redaction without downtime. Given rising environmental, social and governance commitments, workload elasticity also lowers idle energy use, helping banks hit carbon-cut targets.

Global Unified Communication-As-A-Service (UCaaS) in Banking Market is Segmented by Component (Telephony, Unified Messaging, Contact Center, Collaboration Platform, and More), Deployment Model (Public Cloud, Hybrid Cloud, and Private Cloud), Organization Size (Small and Medium-Sized Enterprises, Large Enterprises), Banking Application (Retail Banking, Corporate and Wholesale Banking, and More), and Geography.

Geography Analysis

North America retained 36.7% UCaaS in banking market share in 2024, capitalizing on mature cloud regulations and sizeable budgets for enterprise modernization. Barclays, UBS and Citigroup exemplify large-scale deployments that marry collaboration suites with AI copilots to streamline advisor workflows . Despite headway, many regional banks remain tethered to depreciating PBXs, as less than 40% of businesses have completed migration. Hybrid rollouts therefore dominate, balancing transformation momentum with risk-management caution.

Asia-Pacific leads growth at 14.80% CAGR through 2030 as mobile-first demographics spur digital banks to embed voice and messaging directly in apps. Japanese carriers such as NTT and SoftBank export UCaaS footprints globally, while partnerships between Vonage and local integrators digitize contact-center estates throughout Southeast Asia. Conversational-AI adoption rises in concert, lifting first-contact resolution and enabling 24/7 multilingual servicing.

Europe emphasizes data-sovereignty, prompting banks to prefer region-locked clouds or sovereign partnerships. UniCredit's USD 400 million acquisition of Vodeno delivers a cloud-native platform with built-in smart-contract engines, aligning with PSD2 open-banking requisites while expanding white-label capabilities. In the Middle East and Africa, cloud adoption leapfrogs legacy PBX phases; for instance, Ecobank's alliance with Google Cloud powers analytics-driven inclusion programs across 35 nations. These markets underline UCaaS' role in bridging service gaps where physical branches remain sparse.

- Microsoft Corporation

- Cisco Systems, Inc.

- RingCentral, Inc.

- 8x8, Inc.

- Zoom Video Communications, Inc.

- Avaya LLC

- Fuze, Inc.

- West Technology Group, LLC (formerly West UC)

- VOSS Solutions

- NetFortris, Inc.

- TetraVX (Netrix, LLC)

- Kurmi Software SAS

- Vonage Holdings Corp.

- Dialpad, Inc.

- Mitel Networks Corporation

- Revation Systems, Inc.

- NICE Ltd.

- Genesys Telecommunications Labs, Inc.

- Google LLC

- Amazon Web Services, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 BYOD and workforce mobility

- 4.2.2 Need for enterprise-wide UC integration

- 4.2.3 Digital-only banking expansion

- 4.2.4 AI-enabled UCaaS for compliance monitoring

- 4.2.5 5G private branch networks

- 4.2.6 Embedded CPaaS in banking apps

- 4.3 Market Restraints

- 4.3.1 Low cloud-UC awareness in tier-2/3 banks

- 4.3.2 Stringent data-security and residency mandates

- 4.3.3 Legacy on-prem PBX lock-ins

- 4.3.4 Vendor API lock-in risk

- 4.4 Evaluation of Critical Regulatory Framework

- 4.5 Value Chain Analysis

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Key Use Cases and Case Studies

- 4.9 Impact on Macroeconomic Factors of the Market

- 4.10 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 By Component

- 5.1.1 Telephony

- 5.1.2 Unified Messaging

- 5.1.3 Contact Center

- 5.1.4 Collaboration Platform

- 5.1.5 Video Conferencing

- 5.1.6 Communication-Platform APIs

- 5.2 By Deployment Model

- 5.2.1 Public Cloud

- 5.2.2 Private Cloud

- 5.2.3 Hybrid Cloud

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-Sized Enterprises

- 5.4 By Banking Application

- 5.4.1 Retail Banking

- 5.4.2 Corporate and Wholesale Banking

- 5.4.3 Investment Banking

- 5.4.4 Payment and FinTech Subsidiaries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Egypt

- 5.5.5.2.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Microsoft Corporation

- 6.4.2 Cisco Systems, Inc.

- 6.4.3 RingCentral, Inc.

- 6.4.4 8x8, Inc.

- 6.4.5 Zoom Video Communications, Inc.

- 6.4.6 Avaya LLC

- 6.4.7 Fuze, Inc.

- 6.4.8 West Technology Group, LLC (formerly West UC)

- 6.4.9 VOSS Solutions

- 6.4.10 NetFortris, Inc.

- 6.4.11 TetraVX (Netrix, LLC)

- 6.4.12 Kurmi Software SAS

- 6.4.13 Vonage Holdings Corp.

- 6.4.14 Dialpad, Inc.

- 6.4.15 Mitel Networks Corporation

- 6.4.16 Revation Systems, Inc.

- 6.4.17 NICE Ltd.

- 6.4.18 Genesys Telecommunications Labs, Inc.

- 6.4.19 Google LLC

- 6.4.20 Amazon Web Services, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

全球整合通訊即服務市場研究報告-產業分析、規模、佔有率、成長、趨勢及預測(2025 年至 2033 年)

全球整合通訊即服務市場研究報告-產業分析、規模、佔有率、成長、趨勢及預測(2025 年至 2033 年) 統一通訊即服務 (UCaaS):市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)

統一通訊即服務 (UCaaS):市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年) 2025-2029 年整合通訊即服務 (UCAAS) 市場2026 年至 2032 年統一通訊即服務 (UCaaS) 市場(按部署類型、組織規模、最終用戶產業和地區分類)

2025-2029 年整合通訊即服務 (UCAAS) 市場2026 年至 2032 年統一通訊即服務 (UCaaS) 市場(按部署類型、組織規模、最終用戶產業和地區分類) 統一通訊即服務 (UCaaS) 市場規模、佔有率、成長分析、按組件、按通訊類型、按交付模式、按部署、按組織規模、按最終用戶、按地區 - 2025 年至 2032 年行業預測

統一通訊即服務 (UCaaS) 市場規模、佔有率、成長分析、按組件、按通訊類型、按交付模式、按部署、按組織規模、按最終用戶、按地區 - 2025 年至 2032 年行業預測 2025年整合通訊即服務(UCaaS)全球市場報告UCaaS 市場:亞太地區,2024-2030 年東南亞國協UCaaS(統一通訊即服務)市場:佔有率分析、產業趨勢、成長預測(2025-2030)歐洲IP電話與 UCaaS(統一通訊即服務)-市場佔有率分析、產業趨勢、成長預測(2025-2030 年)能源領域的 UCaaS -市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

2025年整合通訊即服務(UCaaS)全球市場報告UCaaS 市場:亞太地區,2024-2030 年東南亞國協UCaaS(統一通訊即服務)市場:佔有率分析、產業趨勢、成長預測(2025-2030)歐洲IP電話與 UCaaS(統一通訊即服務)-市場佔有率分析、產業趨勢、成長預測(2025-2030 年)能源領域的 UCaaS -市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)