|

市場調查報告書

商品編碼

1844567

分子篩:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030)Zeolite Molecular Sieves - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

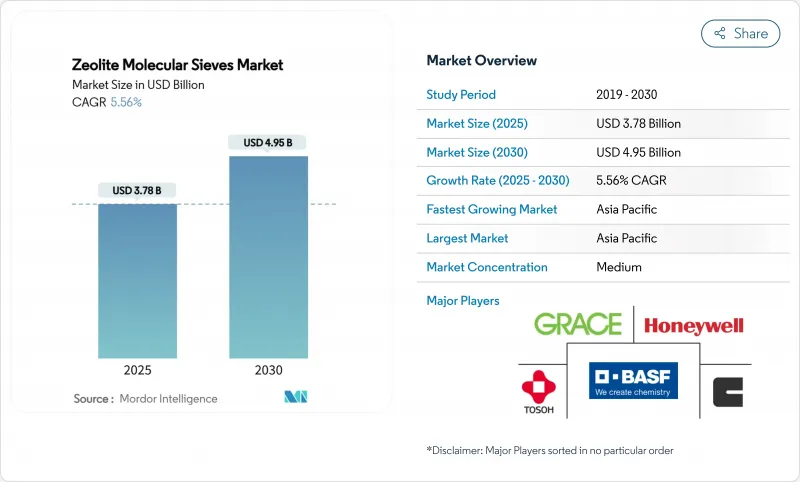

沸石分子篩市場規模預計在 2025 年達到 37.8 億美元,預計到 2030 年將達到 49.5 億美元,預測期內(2025-2030 年)的複合年成長率為 5.56%。

需求成長受到四種結構性力量的催化作用:更嚴格的環境法規要求替代清潔劑中的磷酸鹽,全球石化綜合體的產能不斷提高,新興經濟體的快速都市化推動了衛生產品的使用,以及加速追求有利於基於沸石的吸附和催化的低碳工業流程。競爭差異化依賴專有的合成技術,該技術可根據特定的分離和催化作用客製化孔徑、二氧化矽與氧化鋁的比例以及晶體形態。雖然氧化鋁和高純度二氧化矽原料的成本波動對利潤構成挑戰,但循環原料策略,特別是煤飛灰和其他工業殘渣的轉化,正在降低原料風險,同時支持企業的永續性目標。碳捕獲和 PFAS 修復的突破性進展正在拓展商業性前沿,並將先進的沸石配方定位為下一代環境系統中活性碳和胺溶劑的可行替代品。

全球沸石分子篩趨勢與洞察

禁止在清潔劑中使用磷酸鹽,促使建築商轉向使用沸石

由於水體富營養化風險,全球清潔劑法規禁止使用磷酸鹽,助洗劑需求轉向沸石 4A。歐盟 (EU) 於 2017 年禁止使用磷酸鹽,導致磷酸鹽年消耗量減少 250 萬噸。目前,沸石以粉末和液體形式取代了其中約 60% 的消耗量。北美也有類似的法規,而印度和巴西的法規也日益嚴格,這使得產量維持可預測的成長。沸石 4A 比碳酸鹽具有更高的鈣結合能力,即使在硬水地區也能確保洗滌效果。跨國清潔劑品牌已將沸石助洗劑納入其全球產品組合,從技術和商業性來看,這種逆轉不太可能發生。新興國家準備將無磷酸鹽法規延長至 2027 年,將加強沸石分子篩市場的長期需求軌跡。

石化脫水和氣體純化繁榮

中國、印度和沙烏地阿拉伯對新乙烯和丙烯聯合裝置的投資超過 500 億美元,這推動了對 3A 和 4A分子篩的需求,這些分子篩可對裂解氣進行脫水並將二氧化碳去除至百萬分之一的水平。單一全球規模的乙烯裂解裝置會消耗 500 至 800 噸分子篩,用於初始裝載和年度補充。由於傳統型原料的高水分和酸性氣體負荷,北美頁岩氣的成長正在加速這一趨勢。合成技術的最新進展已經生產出具有增強的傳質性能的更大的沸石晶體,將再生能源需求降低了 25%,並降低了石化營運商的生命週期成本。因此,沸石分子篩市場有望從以更高純度規格為目標的維修綠地計畫和修井作業中吸引越來越多的需求。

洗衣配方中酵素和化學品的替代品

高階清潔劑品牌越來越青睞蛋白酶和脂肪酶,它們以較低的用量提供相當的去污效果,可使液體配方中的沸石含量減少高達20%。聚羧酸鹽和磷酸酯洗劑在濃縮液中易於分散,而沸石的不溶性使加工和包裝變得複雜。由於液體清潔劑是新興市場成長最快的類別,高階市場的沸石使用量面臨下降的風險。然而,尤其是在新興經濟體,粉末清潔劑和低價產品仍依賴4A沸石來控制硬度,減輕了對整個沸石分子篩市場的影響。

細分分析

到2024年,合成A型沸石將佔據全球銷售量的57.89%,這得益於精確的矽鋁比控制,從而能夠設計出適用於石化脫水和分離應用的孔徑。成本最佳化的熱液合成、微波輔助合成和無模板合成技術,在持續提高產品純度的同時,能耗降低了35%。相較之下,天然斜發沸石和絲光沸石的複合年成長率為6.12%,主要應用於農業、氣味控制和低壓水處理領域,這些領域的性價比優於晶體完整性。土耳其和保加利亞的天然礦床提供的礦石只需極少的離子交換即可達到規格要求,帶來30%-40%的成本優勢。歐盟綠色新政等法規對非合成礦物的青睞,進一步推動了它們的應用。展望未來,合成沸石將在高壓脫水和催化作用保持其地位,而天然沸石將擴大佔據環境和農業領域,在沸石分子篩市場中開闢互補的成長通道。

沸石分子篩報告按原料(天然沸石和合成沸石)、最終用戶產業(清潔劑、石化和煉油、工業氣體生產、廢棄物和水處理、空氣淨化和暖通空調、農業和動物飼料、其他終端用戶產業)和地區(亞太地區、北美、歐洲、南美、中東和非洲)細分。

區域分析

至2024年,亞太地區將貢獻全球37.56%的收入,複合年成長率為6.21%。中國在乙烯裂解裝置和煤化工聯合裝置的投資方面處於領先地位,每個裝置都需要數百噸分子篩用於脫水。亞太地區的生產規模、日益嚴格的環保規範以及龐大的消費群,共同推動其在該地區的領先地位。中國浙江省和廣東省的乙烯計劃要求分子篩脫水裝置將水分去除至1 ppm以下,而當地污水標準對氨含量有所限制,刺激了沸石三級脫水系統的推廣。

北美是該技術成熟且潛力巨大的市場。德克薩斯州頁岩氣加工廠正在部署3A分子篩,用於在低溫NGL回收之前去除水分,以期提高效率並延長床層壽命。美國關於PFAS排放的提案正在加速高矽沸石的測試,這種沸石可以捕獲PPT級的全氟烷基化合物,這將為特種產品製造商創造新的收益來源。

歐洲優先考慮永續性和循環性。德國和荷蘭的工廠正在商業規模檢驗飛灰衍生沸石,與原生礦物路線相比,實現了40%的體積碳減量。中東和非洲正在應對石化產品多樣化和水資源短缺問題。沙烏地阿拉伯的「願景2030」樹脂工廠依賴大型分子篩塔進行原料製備。南非的採礦業正在採用斜發沸石淨化酸性礦山廢水,受益於其國內天然礦床,降低了進口成本。總而言之,這些區域發展代表著沸石分子篩市場地理範圍的不斷擴大。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場狀況

- 市場概況

- 市場促進因素

- 禁止在清潔劑中使用磷酸鹽,導致助洗劑轉向使用沸石

- 石化脫水和氣體純化繁榮

- 嚴格的污水排放法規

- 新興國家衛生主導的清潔劑需求

- 生物精煉轉向形狀選擇性催化劑

- 市場限制

- 洗衣配方中酵素和化學品的替代品

- 揮發性氧化鋁/二氧化矽原料價格

- ESG投資者質疑高能源足跡

- 價值鏈分析

- 五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章市場規模及成長預測

- 按原料

- 天然沸石

- 合成沸石

- 按最終用戶產業

- 清潔劑

- 石化和煉油

- 工業氣體生產

- 廢棄物和水處理

- 空氣淨化及暖通空調

- 農業和飼料

- 其他最終用戶產業

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 俄羅斯

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭態勢

- 市場集中度

- 策略舉措

- 市佔率分析

- 公司簡介

- Arkema

- Axens

- BASF

- CLARIANT

- CWK Chemiewerk Bad Kostritz GmbH

- HengYe Inc.

- Honeywell International Inc.

- JIUZHOU CHEMICALS

- KMI Zeolite Inc.

- KNT Group

- KURARAY CO., LTD.

- Luoyang Jalon Micro-Nano New Material

- Sorbchem India Pvt Ltd.

- Tosoh Corporation

- WR Grace & Co.

- Zeochem

- Zeolyst International

第7章 市場機會與未來展望

The Zeolite Molecular Sieves Market size is estimated at USD 3.78 billion in 2025, and is expected to reach USD 4.95 billion by 2030, at a CAGR of 5.56% during the forecast period (2025-2030).

Demand growth is anchored in four structural forces: tightening environmental regulations that substitute phosphates in detergents, capacity additions across global petrochemical complexes, rapid urbanization in emerging economies that drives hygiene product uptake, and the accelerated pursuit of low-carbon industrial processes that favor zeolite-based adsorption and catalysis. Competitive differentiation rests on proprietary synthesis know-how that tailors pore size, silica-to-alumina ratio, and crystal morphology to specific separation or catalytic duties. Cost volatility in alumina and high-purity silica feedstocks poses a margin challenge, but circular feedstock strategies, especially the conversion of coal fly ash and other industrial residues, are mitigating raw-material risk while supporting corporate sustainability goals. Breakthrough deployments in carbon-capture and PFAS remediation are expanding the commercial frontier, positioning advanced zeolite formulations as viable alternatives to activated carbon and amine solvents in next-generation environmental systems

Global Zeolite Molecular Sieves Market Trends and Insights

Phosphate Bans in Detergents Shifting Builders to Zeolites

Global detergent regulations prohibit phosphates because of eutrophication risks, redirecting builder demand toward zeolite 4A. The European Union's 2017 ban eliminated 2.5 million tons of phosphate consumption annually, and zeolites now replace roughly 60% of that volume in both powder and liquid formulations. Similar mandates in North America, along with phased restrictions in India and Brazil, sustain predictable volume growth. Performance advantages compound the regulatory pull: zeolite 4A exhibits higher calcium-binding capacity than carbonates, securing wash performance in hard-water regions. Multinational detergent brands have embedded zeolite builders across their global portfolios, making a reversal technically and commercially unlikely. Emerging economies are poised to expand phosphate-free regulations through 2027, reinforcing the long-run demand trajectory for the zeolite molecular sieve market.

Petrochemical Dehydration and Gas-Purification Boom

Investment exceeding USD 50 billion in new ethylene and propylene complexes across China, India, and Saudi Arabia is elevating demand for 3A and 4A molecular sieves that dehydrate cracked gas and strip CO2 to parts-per-million levels. A single world-scale ethylene cracker consumes 500-800 tons of sieves in initial charging and annual top-ups. Shale-gas growth in North America accelerates the trend, because unconventional feedstocks carry higher moisture and acid-gas loads. Recent synthesis advances have produced larger zeolite crystals with enhanced mass-transfer characteristics, cutting regeneration energy by 25% and reducing lifecycle cost for petrochemical operators. Consequently, the zeolite molecular sieve market is poised to capture incremental offtake from greenfield projects and from revamps that target higher purity specifications.

Enzyme and Chemical Substitutes in Laundry Formulations

Premium detergent brands increasingly favor protease and lipase enzymes that deliver comparable soil removal at lower builder dosage, cutting zeolite content by up to 20% in liquid formats. Polycarboxylate and phosphonate builders disperse easily in concentrated liquids, where zeolite's insolubility complicates processing and packaging. As liquid detergents represent the fastest-growing category in developed markets, zeolite volumes risk erosion in the top-tier segment. Yet powder detergents and value-priced products, particularly in emerging economies, still depend on zeolite 4A for hardness control, mitigating the overall impact on the zeolite molecular sieve market.

Other drivers and restraints analyzed in the detailed report include:

- Stringent Wastewater Discharge Norms

- Hygiene-Driven Detergent Demand in Emerging Economies

- Volatile Alumina/Silica Feedstock Pricing

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Synthetic zeolite A captured 57.89% of global volume in 2024 thanks to precise Si/Al control that engineers pore size for petrochemical dehydration and separation tasks. Cost-optimized hydrothermal, microwave-assisted, and template-free syntheses continue to elevate product purity while trimming energy consumption by 35%. In contrast, natural clinoptilolite and mordenite grades are growing at 6.12% CAGR, primarily in agriculture, odor control, and low-pressure water treatment applications where the performance-to-price ratio outranks crystal perfection. Natural deposits in Turkey and Bulgaria deliver ore that requires minimal ion-exchange to reach specification, offering a 30-40% cost edge. Regulatory drivers such as the EU's Green Deal favor non-synthetic minerals, further stimulating adoption. Looking forward, synthetic grades maintain their hold in high-pressure dehydration and catalysis, but natural zeolites increasingly claim environmental and agricultural niches, carving a complementary growth lane within the zeolite molecular sieve market.

The Zeolite Molecular Sieve Report is Segmented by Raw Material (Natural Zeolite and Synthetic Zeolite), End-User Industry (Detergents, Petrochemical and Refining, Industrial Gas Production, Waste and Water Treatment, Air Purification and HVAC, and Agriculture and Animal Feed, Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa).

Geography Analysis

Asia Pacific generated 37.56% of global sales in 2024 and is set to grow at a 6.21% CAGR. China spearheads investment in ethylene crackers and coal-to-chemicals complexes, each requiring hundreds of tons of molecular sieves for dehydration duty. Asia Pacific's convergence of production scale, tightening environmental norms, and large consumer bases drives the region's leadership. China's Zhejiang and Guangdong ethylene projects require molecular-sieve dehydration units that remove moisture to below 1 ppm, while local wastewater standards enforce ammonia limits that spur zeolite tertiary systems.

North America exhibits mature but technology-rich demand. Shale-gas processing plants in Texas deploy 3A molecular sieves to strip moisture before cryogenic NGL recovery, seeking higher efficiency and longer bed life. EPA PFAS discharge proposals accelerate trials of high-silica zeolites that capture perfluoro-alkyl compounds at parts-per-trillion levels, an emerging revenue stream for specialty producers.

Europe prioritizes sustainability and circularity. Plants in Germany and the Netherlands validate fly-ash-derived zeolites at commercial scale, delivering 40% embodied-carbon reduction relative to virgin mineral routes. Middle-East and Africa capitalize on petrochemical diversification and water scarcity. Saudi Arabia's Vision 2030 resin capacities rely on large-format molecular-sieve towers for feedstock preparation. South Africa's mining sector adopts clinoptilolite for acid-mine drainage remediation, benefitting from domestic natural deposits that eliminate import costs. Collectively, these regional developments underscore the expanding geographic canvas for the zeolite molecular sieve market.

- Arkema

- Axens

- BASF

- CLARIANT

- CWK Chemiewerk Bad Kostritz GmbH

- HengYe Inc.

- Honeywell International Inc.

- JIUZHOU CHEMICALS

- KMI Zeolite Inc.

- KNT Group

- KURARAY CO., LTD.

- Luoyang Jalon Micro-Nano New Material

- Sorbchem India Pvt Ltd.

- Tosoh Corporation

- W. R. Grace & Co.

- Zeochem

- Zeolyst International

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Phosphate Bans in Detergents Shifting Builders to Zeolites

- 4.2.2 Petrochemical Dehydration and Gas-Purification Boom

- 4.2.3 Stringent Wastewater Discharge Norms

- 4.2.4 Hygiene-Driven Detergent Demand in Emerging Economies

- 4.2.5 Bio-Refinery Shift Demanding Shape-Selective Catalysts

- 4.3 Market Restraints

- 4.3.1 Enzyme And Chemical Substitutes in Laundry Formulations

- 4.3.2 Volatile Alumina/Silica Feedstock Pricing

- 4.3.3 High Energy Footprint Questioned by ESG Investors

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Raw Material

- 5.1.1 Natural Zeolite

- 5.1.2 Synthetic Zeolite

- 5.2 By End-user Industry

- 5.2.1 Detergents

- 5.2.2 Petrochemical and Refining

- 5.2.3 Industrial Gas Production

- 5.2.4 Waste and Water Treatment

- 5.2.5 Air Purification and HVAC

- 5.2.6 Agriculture and Animal Feed

- 5.2.7 Other End-user Industries

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Russia

- 5.3.3.6 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Arkema

- 6.4.2 Axens

- 6.4.3 BASF

- 6.4.4 CLARIANT

- 6.4.5 CWK Chemiewerk Bad Kostritz GmbH

- 6.4.6 HengYe Inc.

- 6.4.7 Honeywell International Inc.

- 6.4.8 JIUZHOU CHEMICALS

- 6.4.9 KMI Zeolite Inc.

- 6.4.10 KNT Group

- 6.4.11 KURARAY CO., LTD.

- 6.4.12 Luoyang Jalon Micro-Nano New Material

- 6.4.13 Sorbchem India Pvt Ltd.

- 6.4.14 Tosoh Corporation

- 6.4.15 W. R. Grace & Co.

- 6.4.16 Zeochem

- 6.4.17 Zeolyst International

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessmen

- 7.2 Increasing Demand for Using Green Technologies

沸石分子篩市場:依形態、純度等級、應用及終端用戶產業分類-2026-2032年全球市場預測

沸石分子篩市場:依形態、純度等級、應用及終端用戶產業分類-2026-2032年全球市場預測 沸石分子篩市場報告:依材料、等級、應用、終端用戶產業及地區分類(2026-2034 年)分子篩市場:依形態、孔徑、終端用戶產業及應用分類-2026-2032年全球預測分子篩市場規模、佔有率、趨勢及預測(按類型、材料類型、應用、形狀、尺寸、最終用途產業及地區分類),2026-2034年

沸石分子篩市場報告:依材料、等級、應用、終端用戶產業及地區分類(2026-2034 年)分子篩市場:依形態、孔徑、終端用戶產業及應用分類-2026-2032年全球預測分子篩市場規模、佔有率、趨勢及預測(按類型、材料類型、應用、形狀、尺寸、最終用途產業及地區分類),2026-2034年 全球分子篩市場,2026-2030年分子篩市場在PSA制氫的應用:按吸附劑類型、工廠產能、純度等級、應用和終端用戶產業分類的全球預測(2026-2032年)環境催化分子篩市場按類型、形狀、應用、終端用戶產業及通路分類,全球預測(2026-2032年)石油化學催化分子篩市場按類型、等級、形狀、合成方法和應用分類,全球預測(2026-2032年)碳分子篩市場按產品類型、純度等級、活化方法、應用和最終用途產業分類-2026-2032年全球預測

全球分子篩市場,2026-2030年分子篩市場在PSA制氫的應用:按吸附劑類型、工廠產能、純度等級、應用和終端用戶產業分類的全球預測(2026-2032年)環境催化分子篩市場按類型、形狀、應用、終端用戶產業及通路分類,全球預測(2026-2032年)石油化學催化分子篩市場按類型、等級、形狀、合成方法和應用分類,全球預測(2026-2032年)碳分子篩市場按產品類型、純度等級、活化方法、應用和最終用途產業分類-2026-2032年全球預測 沸石分子篩市場:市場機會、成長促進因素、產業趨勢分析及預測(2026-2035)

沸石分子篩市場:市場機會、成長促進因素、產業趨勢分析及預測(2026-2035)