|

市場調查報告書

商品編碼

1844544

電動方向盤:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)Electric Power Steering - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

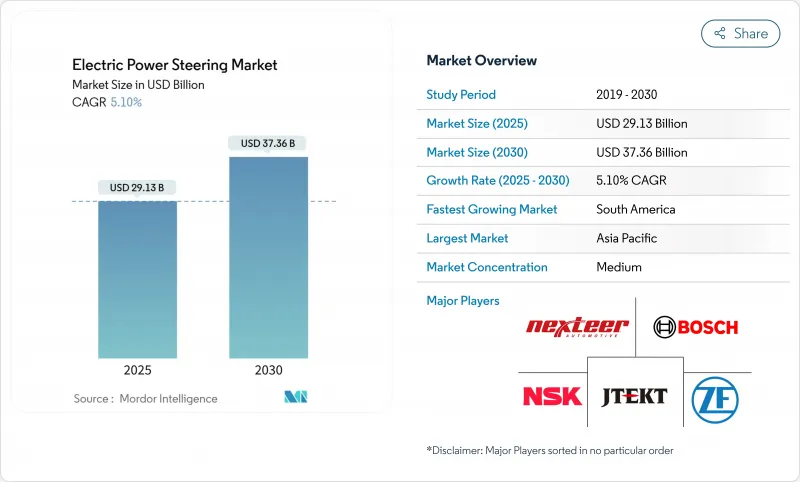

預計電動方向盤市場在 2025 年將達到 291.3 億美元,到 2030 年將達到 373.6 億美元,複合年成長率為 5.10%。

線傳轉向的普及、燃油經濟性法規的收緊以及向軟體定義汽車的轉變,都在支持這一穩定的發展軌跡。汽車製造商現在將轉向系統作為大規模客製化的門戶,強調透過無線更新實現智慧軟體校準。供應商正在將重點從純機械專業知識轉向符合 ISO/SAE 21434 和 UN R155 網路安全法規的整合電子架構。同時,亞太地區的主導地位受到中國電動車規模和日本精密組件傳統的推動。南美洲電動車的加速普及正在推動成本敏感市場的下一波需求。現有的一級公司正在透過將電控系統、感測器和電機設計捆綁到承包模組中來捍衛自己的地位,這些模組可以根據不斷發展的 ADAS 要求進行檢驗。

全球電動方向盤市場趨勢與洞察

汽車平臺快速電氣化

汽車電氣化將從根本上改變電動輔助轉向系統 (EPS) 的採用模式,因為它消除了液壓系統固有的寄生損耗,而液壓系統會消耗內燃機車輛的引擎功率。電動車需要節能的轉向解決方案,而混合動力 EPS 系統已證明,與商用車應用中的傳統液壓動力方向盤相比,其能耗可降低 50% 以上。隨著汽車製造商認知到 EPS 是整合再生煞車和最佳化電池續航里程的重要基礎設施,這一轉變正在加速。美國國家公路交通安全管理局 (NHTSA) 針對 2027-2031 年車型製定的企業平均燃油經濟性標準要求每年燃油經濟性提高 2%,這使得 EPS 的採用成為內燃機車輛的經濟必需品,也是電動車的競爭優勢。這種監管壓力創造了雙重市場動態:對於傳統車輛而言,EPS 以合規性主導;而對於電動平台而言,EPS 則以性能提升為導向。

對燃油經濟性和減少排放氣體的需求不斷增加

根據美國國家研究委員會的研究,更換液壓系統可使中型車輛的油耗降低1.3%,重型車輛的油耗降低1.1%。由於整個車隊的效率提升是疊加的,因此對於面臨燃油成本上升和碳定價機制挑戰的商用車營運商而言,EPS 具有經濟吸引力。歐盟《通用安全法規 II》(2024 年 7 月生效)要求使用與 EPS 系統無縫整合的先進安全技術,從而形成監管協同效應,加速 EPS 的普及。效率要求與安全性的整合要求 EPS 成為一項基礎技術,而非可選的附加技術。車隊營運商擴大將 EPS 視為一項基礎設施投資,它將賦能未來的自動駕駛能力,同時帶來即時的營運成本節約。

單位成本高,而低成本車輛的液壓系統則不然

在價格驅動的細分市場中,成本競爭仍然激烈,儘管營運效率低下,液壓系統仍保持經濟優勢。印度汽車製造商展示了不同的成本管理方法,塔塔汽車公司將其 Harrier EV 的 80% 零件本地化,而 Ola Electric 等公司則開發無磁電機以避免對稀土材料的依賴。隨著中國稀土出口限制對供應鏈造成壓力,以及印度考慮放寬 50% 的本地化要求以維持電動車製造的可行性,成本差異變得更加明顯。製造規模經濟有利於大眾市場中的現有液壓系統供應商,從而造成市場分化,高檔車採用 EPS,而經濟型車則抵制轉型。在商用車應用中,挑戰更加嚴峻,初始資本成本直接影響車輛盈利,必須證明明顯的營運成本節約才能證明更高的購置價格是合理的。

細分分析

到2024年,管柱式EPS系統將佔據54.23%的市場佔有率,這反映了其在主流汽車平臺中已確立的整合優勢和成本效益。然而,雙小齒輪配置將成為成長最快的細分市場,到2030年,複合年成長率將達到11.50%,這主要得益於自動駕駛應用對精度的要求以及轉向響應特性的提升。小齒輪式系統在成本和性能之間實現了良好的平衡,在中階應用中保持了穩定的市場影響。此細分市場的演變反映了製造商對未來出行需求的策略性定位,其中轉向精度對於安全至關重要的自動駕駛功能至關重要。

蔚來ET9採用採埃孚線傳技術,展現了先進的架構如何助力全新方向盤設計與更佳操控性,尤其有利於電動車平台。管柱式轉向系統在改裝應用和成本敏感型細分市場中保持主導地位,而雙小齒輪轉向系統則吸引了尋求差異化駕駛體驗的高階製造商。技術進步標誌著市場的分化:大眾市場車輛優先考慮管柱式轉向系統久經考驗的可靠性,而性能驅動型應用則轉向雙小齒輪轉向系統的精準性能。

2024年,轉向齒條/轉向柱組件將維持42.61%的市場佔有率,成為所有車型EPS系統的機械基礎。到2030年,感測器組件的複合年成長率將達到10.20%,成長最快,這反映了整合高階駕駛輔助系統(ADAS)所需的回饋機制日益複雜。方向盤馬達作為主要的驅動組件,性能穩定,而其他組件類型則融合了網路安全模組和無線更新功能等新興技術。組件組合的演變表明,市場正從基礎電氣化向智慧型系統架構邁進。

感測器的成長軌跡與增強型車輛安全系統的監管要求一致,旨在提供準確的回饋,以實現緊急轉向干預和車道維持輔助功能。 NSK 開發的力回饋致致動器和車輪致動器表明,下一代轉向系統所需組件的複雜性日益提高。傳統機械組件面臨商品化的壓力,而電子組件則因其先進的功能而擁有高昂的價格,從而重塑了供應商的價值提案和競爭態勢。

區域分析

2024年,亞太地區將佔電動方向盤市場收益的46.80%。中國垂直整合的電動車生態系統將國產馬達控制器、整車模組和轉向裝置整合成具有成本競爭力的模組,用於國內和出口專案。蔚來汽車採用採埃孚(ZF)的線傳,凸顯了中國已準備好直接進入先進架構。同時,日本正在捍衛其在高精度軸承和角度感測器領域的領先地位,這使得本地供應商能夠向全球一級供應商銷售關鍵次組件。政府的碳中和獎勵正在加速需求成長,而區域產能則確保了零件的供應。

歐洲是一個成熟但受法規主導的市場。歐盟通用安全法規II要求原始設備製造商(OEM)必須提供依賴EPS精度的車道維持和行人避讓功能。供應商受益於穩定的規劃週期和固定的實施日期。 2010年代中期的網路安全法規將進一步提高門檻,使車隊管理集中在擁有專門軟體團隊的公司手中。

北美專注於能源效率法規。美國國家公路交通安全管理局(NHTSA)的CAFE標準要求乘用車燃油經濟性在2031年之前每年提高2%。以巴西為首的南美是成長最快的地區,到2030年的複合年成長率將達到9%。 2024年,電動車銷量飆升90%,顯示免除進口電池模組關稅後,電動車需求將持續成長。 Stellantis緊隨其後,投資56億歐元開發一款整合式電動輔助轉向(EPS)的生物混合動力傳動系統,用於雙燃料運作。該地區的成長標誌著一項突破現有液壓技術的技術飛躍。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場狀況

- 市場概況

- 市場促進因素

- 汽車平臺快速電氣化

- 對燃油效率和減少排放氣體的要求日益提高

- ADAS整合監理更加嚴格

- 線傳研發突破

- 與一級/二級供應商合作開發48V電動動力傳動系統模組

- 面向大規模客製化的OTA軟體轉向校準

- 市場限制

- 在低成本車輛中,單位成本高於液壓系統

- 新興市場的轉向感有限且有安全隱患

- 馬達控制器半導體供應鏈不穩定

- 電子控制欄網路安全風險

- 價值/供應鏈分析

- 監管狀況

- 技術展望

- 五力分析

- 新進入者的威脅

- 買家/消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭強度

第5章市場規模及成長預測

- 按類型

- 列類型

- 小齒輪類型

- 雙小齒輪型

- 依組件類型

- 轉向齒條/轉向柱

- 感應器

- 方向盤馬達

- 其他

- 按車輛類型

- 搭乘用車

- 商用車

- 依推進類型

- 內燃機汽車

- 混合動力汽車

- 純電動車

- 按地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太地區

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 土耳其

- 南非

- 埃及

- 其他中東和非洲地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 北美洲

第6章 競爭態勢

- 市場集中度

- 策略舉措

- 市佔率分析

- 公司簡介

- JTEKT Corporation

- Robert Bosch GmbH

- Nexteer Automotive

- ZF Friedrichshafen AG

- Denso Corporation

- NSK Ltd.

- Hyundai Mobis Co. Ltd.

- Mitsubishi Electric Corporation

- Hitachi Astemo Ltd.

- Thyssenkrupp Presta AG

- Mando Corporation

- Continental AG

第7章 市場機會與未來展望

The electric power steering market generated USD 29.13 billion in 2025 and will reach USD 37.36 billion by 2030, representing a 5.10% CAGR.

Rising penetration of steer-by-wire, tighter fuel-efficiency rules, and the shift toward software-defined vehicles underpin this steady trajectory. Automakers now emphasize intelligent software calibration delivered through over-the-air updates, using the steering system as a gateway for mass customization. Suppliers are pivoting from purely mechanical expertise to integrated electronic architectures that comply with ISO/SAE 21434 and UN R155 cybersecurity rules. At the same time, Asia-Pacific's dominant share rests on China's EV scale and Japan's precision-component heritage. South America's accelerating EV adoption signals the next demand wave in cost-sensitive markets. Incumbent Tier-1s defend their position by bundling electronic control units, sensors, and motor designs into turnkey modules that can be validated against evolving ADAS mandates.

Global Electric Power Steering Market Trends and Insights

Rapid Electrification of Vehicle Platforms

Vehicle electrification fundamentally reshapes EPS adoption patterns by eliminating the parasitic losses inherent in hydraulic systems that drain ICE engine power. Electric vehicles demand energy-efficient steering solutions, with hybrid EPS systems demonstrating over 50% energy consumption reduction compared to conventional hydraulic power steering in commercial vehicle applications. The transition accelerates as automakers recognize EPS as an essential infrastructure for regenerative braking integration and battery range optimization. NHTSA's Corporate Average Fuel Economy standards for model years 2027-2031 mandate 2% annual fuel efficiency improvements, making EPS adoption economically inevitable for ICE vehicles while providing competitive advantages for EVs. This regulatory pressure creates a dual-market dynamic where EPS becomes compliance-driven for traditional vehicles and performance-enhancing for electric platforms.

Increasing Demand for Fuel Efficiency and Emission Reduction

Fuel efficiency mandates drive EPS adoption through measurable consumption benefits, with National Research Council studies indicating 1.3% fuel reduction for midsize cars and 1.1% for large cars when replacing hydraulic systems. Efficiency gains compound across fleet operations, making EPS economically attractive for commercial vehicle operators facing rising fuel costs and carbon pricing mechanisms. European Union's General Safety Regulation II, effective July 2024, mandates advanced safety technologies that integrate seamlessly with EPS systems, creating regulatory synergies that accelerate adoption. The convergence of efficiency requirements and safety mandates EPS as a foundational technology rather than optional equipment. Fleet operators increasingly recognize EPS as an infrastructure investment that delivers immediate operational cost reductions while enabling future autonomous capabilities.

Higher Unit Cost vs. Hydraulic Systems in Low-Cost Cars

Cost competitiveness remains challenging in price-sensitive market segments where hydraulic systems maintain economic advantages despite operational inefficiencies. Indian automakers demonstrate varied approaches to cost management, with Tata Motors achieving 80% localization for Harrier EV components while companies like Ola Electric develop magnet-less motors to avoid rare-earth material dependencies. The cost differential becomes more pronounced as China's rare-earth export restrictions create supply chain pressures, with India considering the relaxation of 50% localization requirements to maintain EV manufacturing viability. Manufacturing scale economics favor established hydraulic system suppliers in volume segments, creating market bifurcation where premium vehicles adopt EPS while economy segments resist transition. The challenge intensifies in commercial vehicle applications where initial capital costs directly impact fleet profitability, requiring a clear operational savings demonstration to justify higher acquisition prices.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Mandates for ADAS Integration

- Steer-by-Wire R&D Breakthroughs

- Limited Steering Feel and Safety Concerns in Emerging Markets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Column Type EPS systems commanded a 54.23% market share in 2024, reflecting their established integration advantages and cost-effectiveness for mainstream vehicle platforms. However, dual-pinion type configurations emerge as the fastest-growing segment at 11.50% CAGR through 2030, driven by precision requirements for autonomous driving applications and enhanced steering response characteristics. Pinion Type systems maintain a steady market presence in mid-range applications, offering balanced performance between cost and capability. The segment evolution reflects manufacturers' strategic positioning for future mobility requirements, where steering precision becomes critical for safety-critical autonomous functions.

ZF's steer-by-wire technology deployment in NIO's ET9 demonstrates how advanced architecture enables new steering wheel designs and improved maneuverability, particularly benefiting electric vehicle platforms. Column Type systems retain advantages in retrofit applications and cost-sensitive segments, while Dual Pinion configurations attract premium manufacturers seeking differentiated driving experiences. Technology progression suggests market bifurcation where volume segments prioritize proven Column Type reliability while performance-oriented applications migrate toward Dual Pinion precision capabilities.

Steering Rack/Column components maintained 42.61% market share in 2024, representing the mechanical foundation of EPS systems across all vehicle types. Sensor components accelerate fastest at 10.20% CAGR through 2030, reflecting the increasing sophistication of feedback mechanisms required for advanced driver assistance systems integration. Steering Motor segments provide consistent performance as the primary actuation component, while Other Component Types encompass emerging technologies like cybersecurity modules and OTA update capabilities. The component mix evolution indicates market maturation beyond basic electrification toward intelligent system architectures.

The sensor growth trajectory aligns with regulatory requirements for enhanced vehicle safety systems, where precise feedback enables emergency steering interventions and lane-keeping assistance functions. NSK's development of Force Feedback Actuators and Road Wheel Actuators for steer-by-wire applications exemplifies the component sophistication required for next-generation steering systems. Traditional mechanical components face commoditization pressure while electronic components command premium pricing through advanced functionality, reshaping supplier value propositions and competitive dynamics.

The Electric Power Steering Market Report is Segmented by Type (Column Type, Pinion Type, and Dual Pinion Type), Component Type (Steering Rack/Column, Sensor, Steering Motor, and More), Vehicle Type (Passenger Cars and Commercial Vehicles), Propulsion Type (Internal Combustion Engine Vehicles, Battery Electric Vehicles, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Geography Analysis

Asia-Pacific anchored 46.80% of the electric power steering market revenue in 2024. China's vertically integrated EV ecosystem packages domestic motor controllers, vehicle domains, and steering gears into cost-competitive modules serving local and export programs. NIO's adoption of steer-by-wire from ZF underscores China's readiness to leap directly into advanced architectures. Japan, meanwhile, protects leadership in high-precision bearings and angle sensors, enabling local suppliers to sell critical sub-assemblies to global Tier-1s. Government incentives for carbon neutrality accelerate demand, and regional capacity ensures component availability.

Europe represents a mature but regulation-driven arena. The EU General Safety Regulation II forces OEMs to fit lane-keeping and pedestrian-avoidance functions that rely on EPS precision. Suppliers gain from stable planning cycles as implementation dates are locked. Mid-decade cybersecurity rules further elevate barriers, consolidating volume among companies with dedicated software teams.

North America focuses on efficiency mandates. NHTSA's CAFE standards impose 2% annual gains for passenger fleets through 2031. South America, led by Brazil, is the fastest-expanding region with a 9% CAGR through 2030. A 90% spike in EV sales in 2024 demonstrated pent-up demand once taxes were waived for imported battery modules. Stellantis followed with a EUR 5.6 billion commitment to develop Bio-Hybrid powertrains that integrate EPS for dual-fuel flexibility. The region's growth illustrates tech leapfrogging, bypassing hydraulic incumbency.

- JTEKT Corporation

- Robert Bosch GmbH

- Nexteer Automotive

- ZF Friedrichshafen AG

- Denso Corporation

- NSK Ltd.

- Hyundai Mobis Co. Ltd.

- Mitsubishi Electric Corporation

- Hitachi Astemo Ltd.

- Thyssenkrupp Presta AG

- Mando Corporation

- Continental AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid electrification of vehicle platforms

- 4.2.2 Increasing demand for fuel efficiency and emission reduction

- 4.2.3 Regulatory mandates for ADAS integration

- 4.2.4 Steer-by-wire RandD breakthroughs

- 4.2.5 Tier-1/2 collaboration on 48-V e-Powertrain modules

- 4.2.6 OTA software steering calibration for mass customisation

- 4.3 Market Restraints

- 4.3.1 Higher unit cost vs. hydraulic systems in low-cost cars

- 4.3.2 Limited steering feel and safety concerns in emerging markets

- 4.3.3 Semiconductor supply-chain volatility for motor controllers

- 4.3.4 Cyber-security risks in electronically actuated columns

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Type

- 5.1.1 Column Type

- 5.1.2 Pinion Type

- 5.1.3 Dual Pinion Type

- 5.2 By Component Type

- 5.2.1 Steering Rack/Column

- 5.2.2 Sensor

- 5.2.3 Steering Motor

- 5.2.4 Other Component Types

- 5.3 By Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.2 Commercial Vehicles

- 5.4 By Propulsion Type

- 5.4.1 Internal Combustion Engine Vehicles

- 5.4.2 Hybrid Vehicles

- 5.4.3 Battery Electric Vehicles

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Russia

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 United Arab Emirates

- 5.5.4.2 Saudi Arabia

- 5.5.4.3 Turkey

- 5.5.4.4 South Africa

- 5.5.4.5 Egypt

- 5.5.4.6 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 JTEKT Corporation

- 6.4.2 Robert Bosch GmbH

- 6.4.3 Nexteer Automotive

- 6.4.4 ZF Friedrichshafen AG

- 6.4.5 Denso Corporation

- 6.4.6 NSK Ltd.

- 6.4.7 Hyundai Mobis Co. Ltd.

- 6.4.8 Mitsubishi Electric Corporation

- 6.4.9 Hitachi Astemo Ltd.

- 6.4.10 Thyssenkrupp Presta AG

- 6.4.11 Mando Corporation

- 6.4.12 Continental AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and unmet-need assessment